After almost 15 years of persistently low (and sometimes even negative) interest rates, yield has finally returned to fixed-income markets. As 2023 approaches, we believe rising volatility—an offshoot of heightened geopolitical turbulence and tightening liquidity conditions—has created a historic entry point to investing in credit. With interest rates at their highest levels since the 2008 Great Financial Crisis (GFC), investors can deploy capital at attractive yields across a wide spectrum of credit investments, from direct lending to dislocated debt.

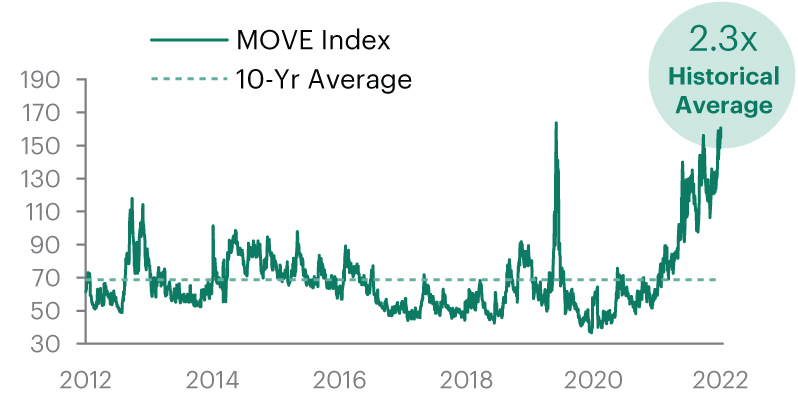

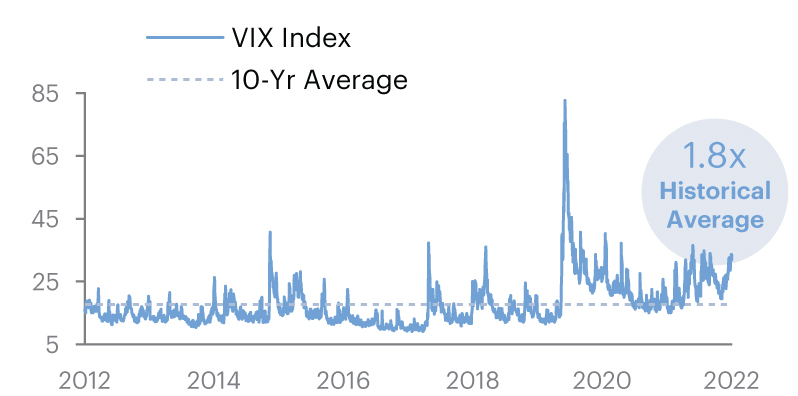

As the Federal Reserve continues to tighten monetary conditions—both through rate hikes and quantitative tightening (QT)—price volatility has been on the rise across asset classes, including foreign exchange and equities. However, volatility in interest rates, and by extension bond and loan markets, has been particularly eye-catching during this cycle. As shown in Exhibit 1, as of October 2022, the Merrill Lynch Option Volatility Estimate (MOVE) Index, an interest-rate volatility barometer, stood at 2.3 times above its 10-year historical average. Comparatively, the Cboe VIX Index, a gauge of equity volatility, was at 1.8 times its historical average during the same period.

Exhibit 1: Volatility in the interest rate market has reached historically high levels

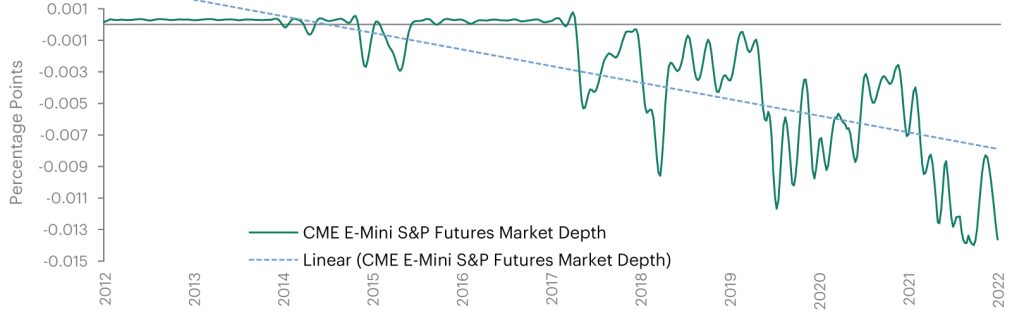

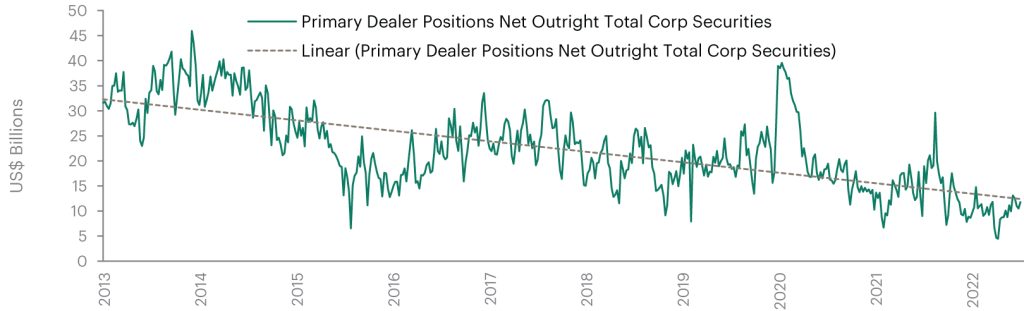

Tightening monetary policy (in response to elevated inflation) is not the sole explanation for the heightened volatility across markets this year. The ongoing war in Ukraine, which is entering its ninth month, has destabilized Europe, and souring US-China relations are threatening to turn back the clock on globalization. Policy mistakes, such as the proposed UK mini-budget and the ensuing sell-off in European credit markets, have also contributed to market instability. Unsurprisingly, liquidity conditions in both equity and fixed-income markets have deteriorated (Exhibit 2).

Exhibit 2: Deteriorating liquidity conditions have worsened market dislocations

Liquidity is worsening in both equity…

Source: Bloomberg, Apollo Analysts

…and bond markets

Source: Bloomberg, Apollo Analysts

Through a historical lens, we believe today’s market environment offers a unique entry point for investors looking to allocate to credit. We expect this opportunity to unfold over the next 12 to 24 months, as the Fed tightens monetary policy, market volatility stays historically elevated, and liquidity remains challenged. In our view, this environment will continue to create periodic forced-selling dynamics that can, in turn, generate attractive opportunities for investors who can act as liquidity providers in times of market stress and distress.

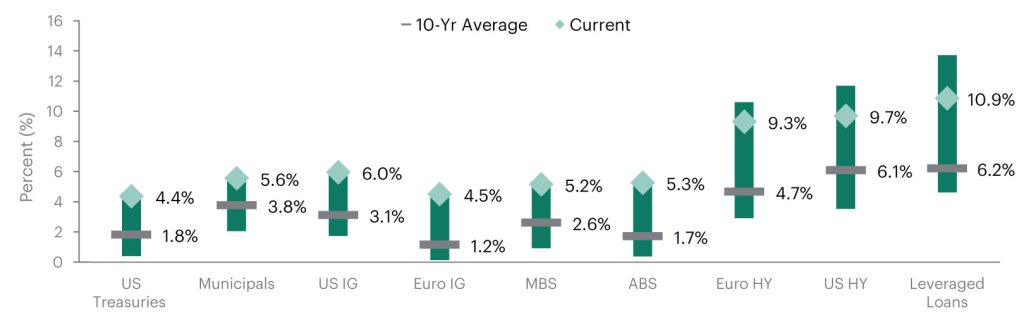

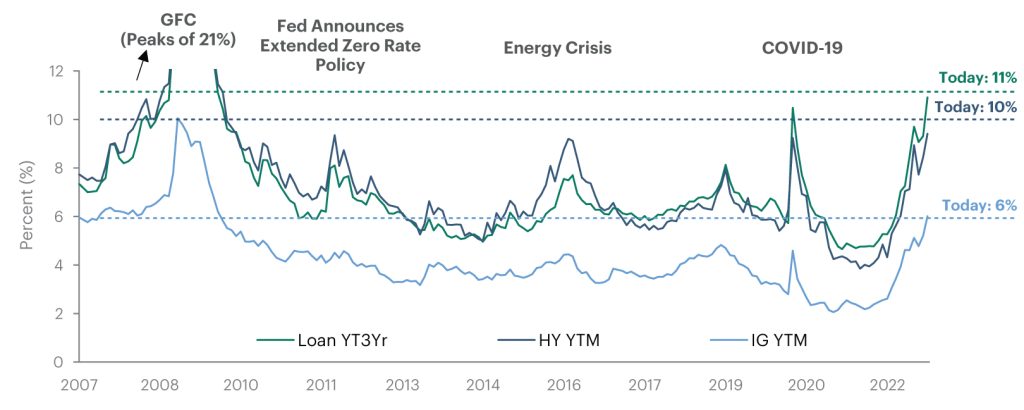

Exhibit 3 captures this point. As seen in the first chart below, yields have surged to historical highs across fixed-income asset classes, with US Treasury and investment grade yields well wide to their 10-year average. Today, US high yield bonds and leveraged loans offer returns that are 300 to 400 basis points above their 10-year average. The second chart below dimensions this opportunity in historical terms, as yields today sit at the loftiest levels in almost 15 years.

Exhibit 3: As yields surge, we see a historic entry point for investing in credit

Yields across fixed-income sectors reach decade highs

Source: Bloomberg, J.P. Morgan, Apollo Analysts

Yields at the highest since the Great Financial Crisis

Source: Bloomberg, J.P. Morgan, Apollo Analysts

However, to fully capitalize on this opportunity, investors must successfully navigate a variety of pitfalls including a potential global recession, future monetary and fiscal policy missteps, and heightened geopolitical risk. That is why we believe a sharp focus on pricing and underwriting discipline when selecting potential investment options is key. In this context, we have detected two key underlying trends shaping the most attractive opportunities we see in the credit space today. They are:

1. Capitalizing on challenged syndicated loan markets

Syndicated markets continued to show signs of stress in the second half of 2022. Legacy bank commitments remain high as the market struggles to absorb the remaining pipeline of deals and investors demand significant concessions to complete transactions. This difficulty syndicating new leveraged loans has constrained access to capital, creating two main opportunities for credit investors: a) partnering with banks on offtake solutions for their financing backlog at attractive prices and terms, and b) providing private credit on new deals where banks have pulled back.

As of September 30, 2022, for example, year-on-year issuance in the US high yield market plummeted 78%, while leveraged loans issuance dropped 69%. This compared to a more modest—yet still significant—drop of 7% in US investment grade issuance volume. In the meantime, a looming maturity wall is fast approaching. Following a strong issuance year in 2021, the need for refinancing in the US leverage loan market is expected to grow from $12 billion in 2023 to $105 billion in 2024, $207 billion in 2025 and $242 billion in 2026.1

Additionally, the opportunity to provide private capital at attractive rates has expanded as excess spreads in the space have continued to rise throughout the second half of 2022, as we had predicted in a previous article. Typical direct deals are now pricing at SOFR + 650 with 2.0-3.0-point original discount (OID) versus SOFR + 500 with a 1.5-point OID in 2021. Coupled with higher short-term interest rates, all-in yields on direct deals now average 11% vs. 7% last year. We expect spreads to widen further, reaching SOFR + 650-750 basis points with yields between 12% and 14% in 2023.2

2. Capitalizing on dislocation

Tightening monetary conditions and ill-fated policies have also generated dislocations across capital markets. Take, for example, the failed attempt to implement a deficit-funded stimulus plan in the UK in September. The announcement kickstarted a wave of forced selling by pension plans facing margin calls related to their liability-driven investment (LDI) programs. The UK LDI contagion spread globally across equity and fixed-income markets.

Against this backdrop, AA- and A-rated senior tranches of collateralized loan obligations came into forced selling pressure, creating an opportunity for investors able to provide credit to step in and purchase high-quality paper at steep discounts. With the Fed and other global central banks at risk of upsetting market stability in their quest to rein in inflation, we believe the opportunity remains strong for investors who are ready to deploy when things break down.

All in all, as we advance into 2023, we believe that the current market environment has created a unique entry point for credit investors. Dislocated public and syndicated markets can open a window of opportunity for investors to benefit from discounted investments in the primary and secondary public markets and provide private capital alternatives for businesses that need to access the debt markets.

1 Source: Morningstar and Bloomberg, as of September 2022.

2 Source: Apollo analysts, as of October 2022.

The information herein is provided for educational purposes only and should not be construed as financial or investment advice, nor should any information in this document be relied on when making an investment decision. Opinions and views expressed reflect the current opinions and views of the authors and Apollo Analysts as of the date hereof and are subject to change. Please see the end of this document for important disclosure information.

Important Disclosure Information

This presentation is for educational purposes only and should not be treated as research. This presentation may not be distributed, transmitted or otherwise communicated to others, in whole or in part, without the express written consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

The views and opinions expressed in this presentation are the views and opinions of the author(s) of the White Paper. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Further, Apollo and its affiliates may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this presentation. There can be no assurance that an investment strategy will be successful. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. Target allocations contained herein are subject to change. There is no assurance that the target allocations will be achieved, and actual allocations may be significantly different than that shown here. This presentation does not constitute an offer of any service or product of Apollo. It is not an invitation by or on behalf of Apollo to any person to buy or sell any security or to adopt any investment strategy, and shall not form the basis of, nor may it accompany nor form part of, any right or contract to buy or sell any security or to adopt any investment strategy. Nothing herein should be taken as investment advice or a recommendation to enter into any transaction.

Hyperlinks to third-party websites in this presentation are provided for reader convenience only. There can be no assurance that any trends discussed herein will continue. Unless otherwise noted, information included herein is presented as of the dates indicated. This presentation is not complete and the information contained herein may change at any time without notice. Apollo does not have any responsibility to update the presentation to account for such changes. Apollo has not made any representation or warranty, expressed or implied, with respect to fairness, correctness, accuracy, reasonableness, or completeness of any of the information contained herein, and expressly disclaims any responsibility or liability therefore. The information contained herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Investors should make an independent investigation of the information contained herein, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients.

Certain information contained herein may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such information. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.

The Standard & Poor’s 500 (“S&P 500”) Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies by market value.

Additional information may be available upon request.