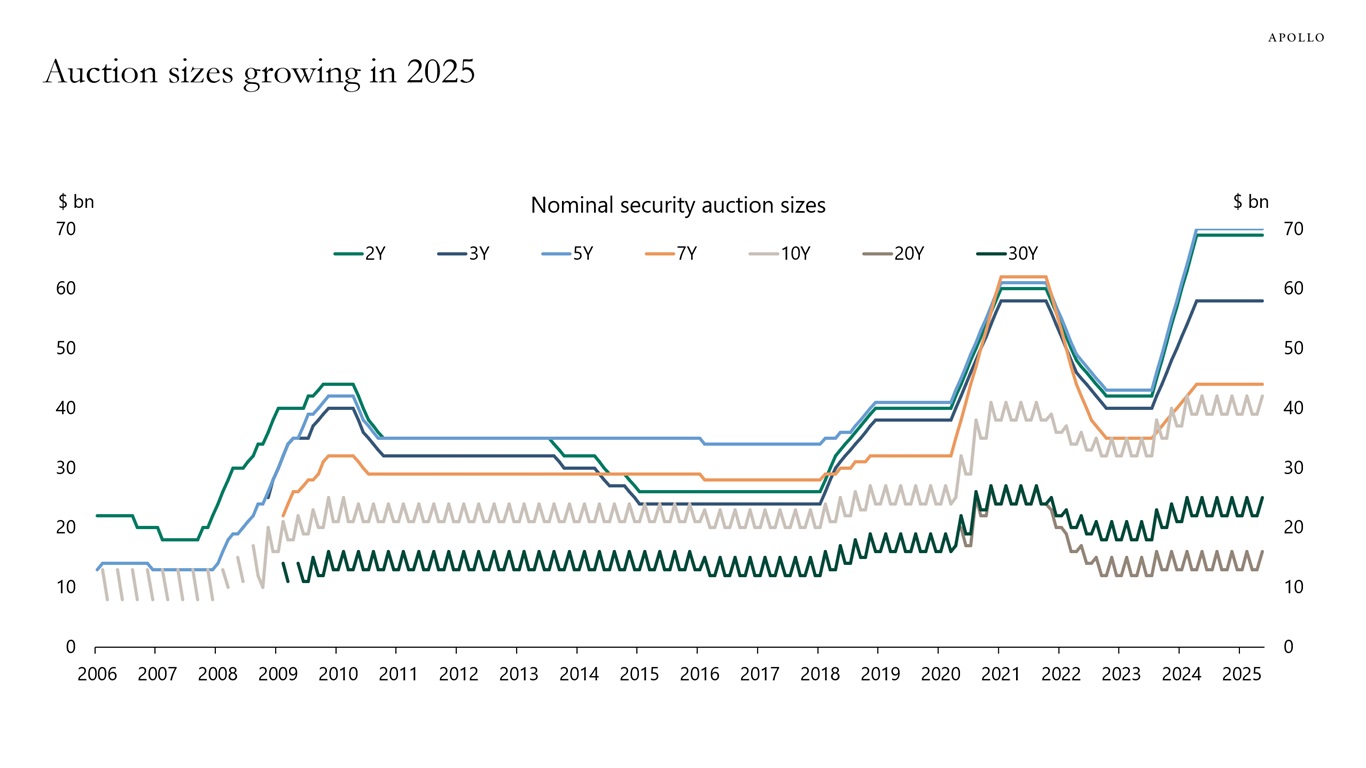

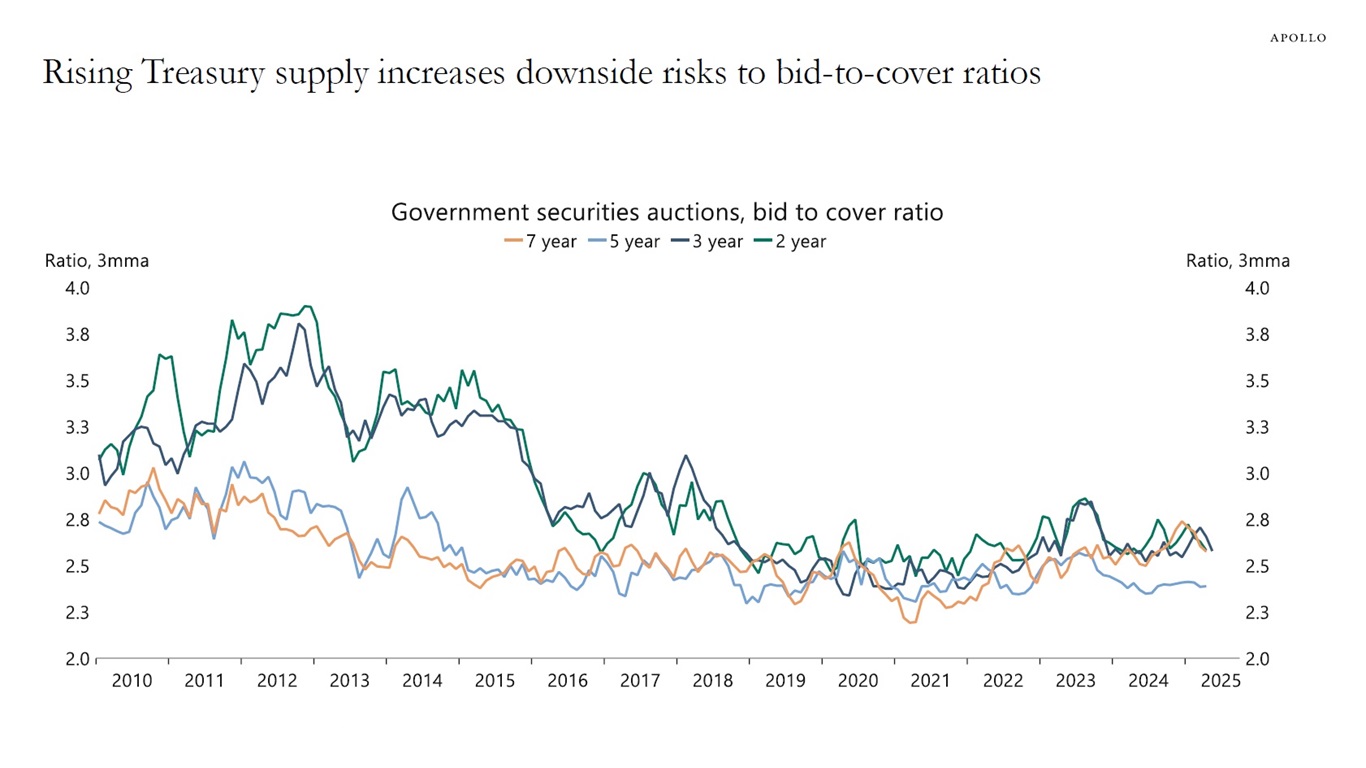

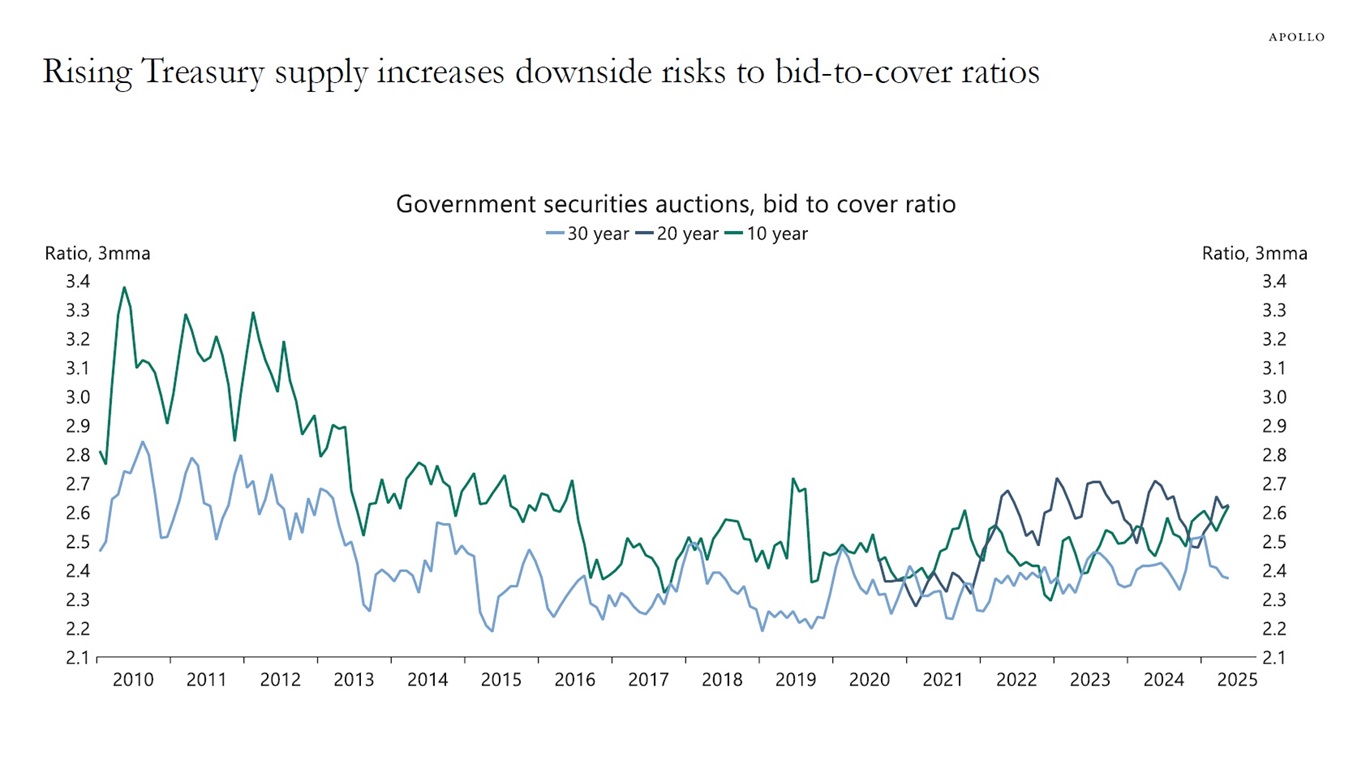

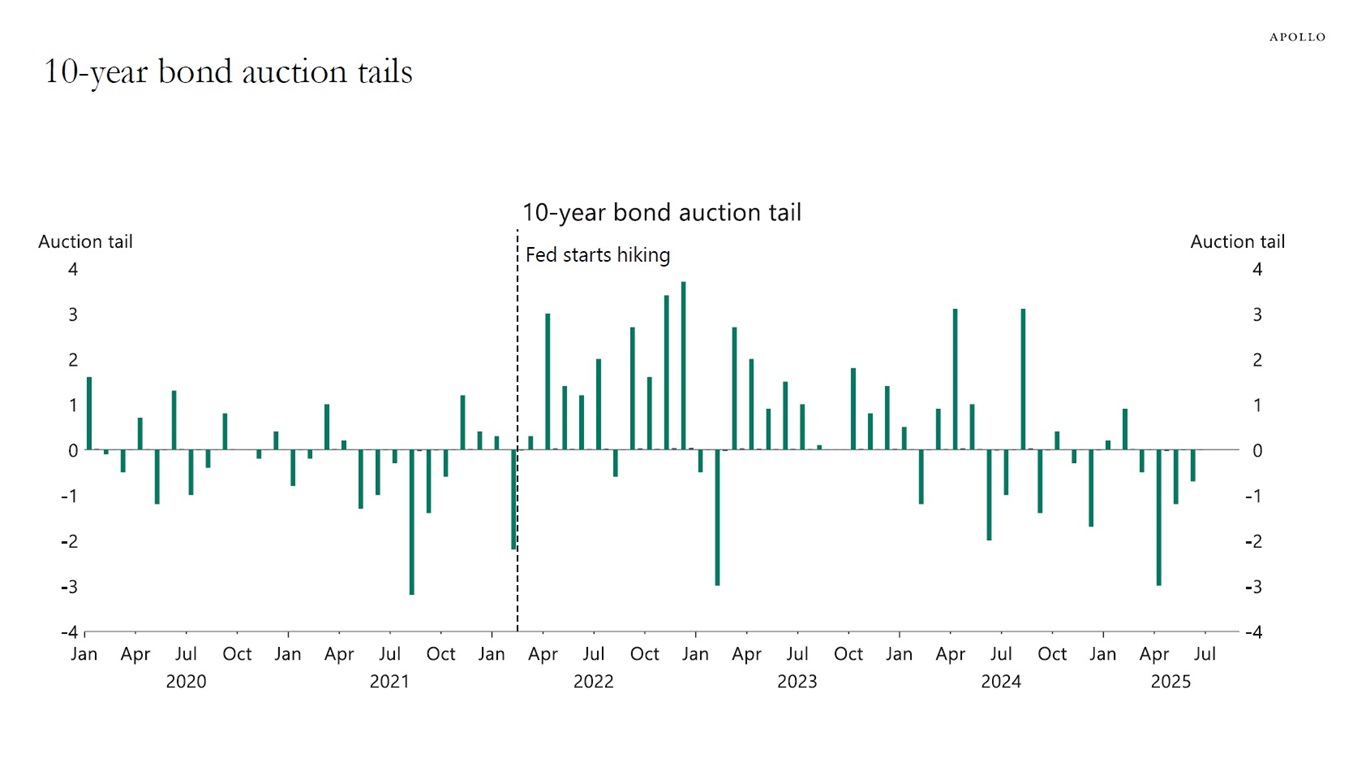

Examining Treasury auction metrics across the curve reveals no signs of weakness in demand for US Treasuries at present. Bid-to-cover ratios are stable, and there is no evidence of auctions systematically tailing, see the first four charts below.

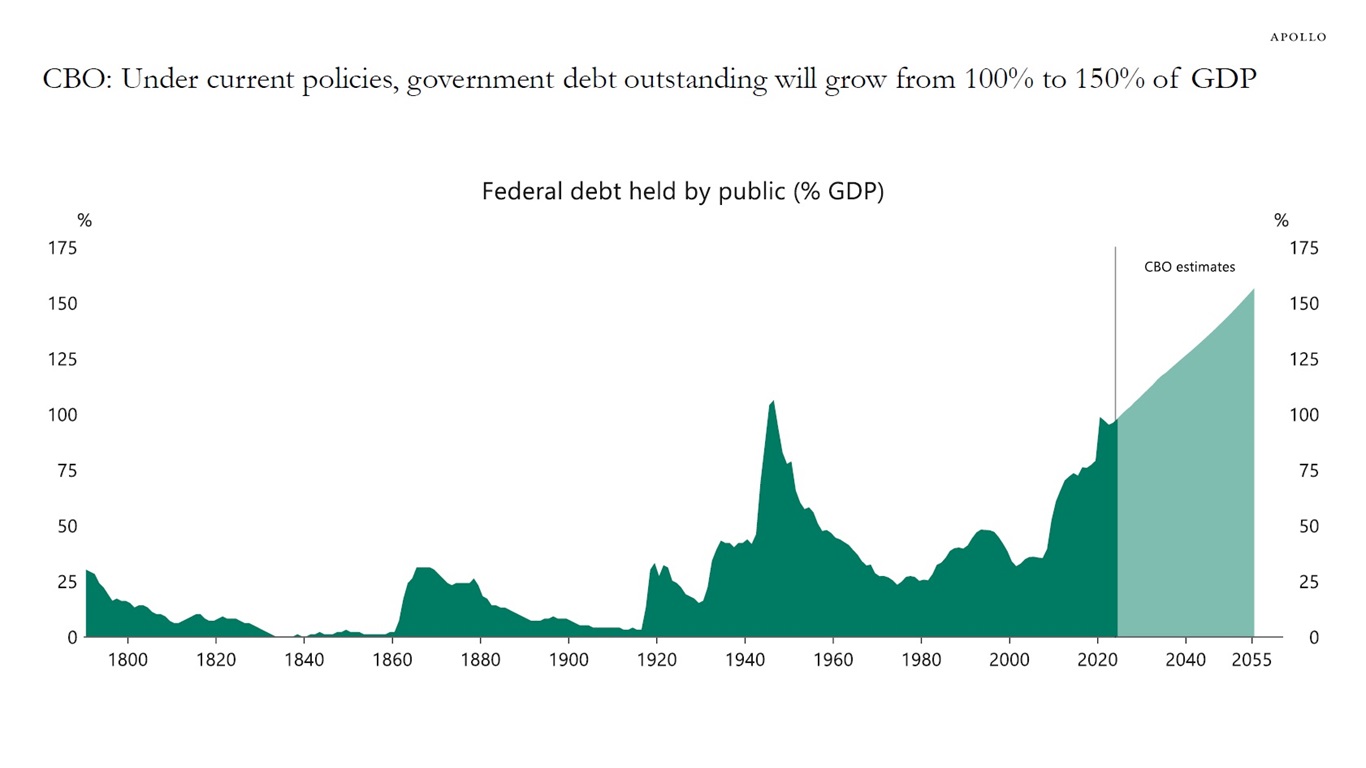

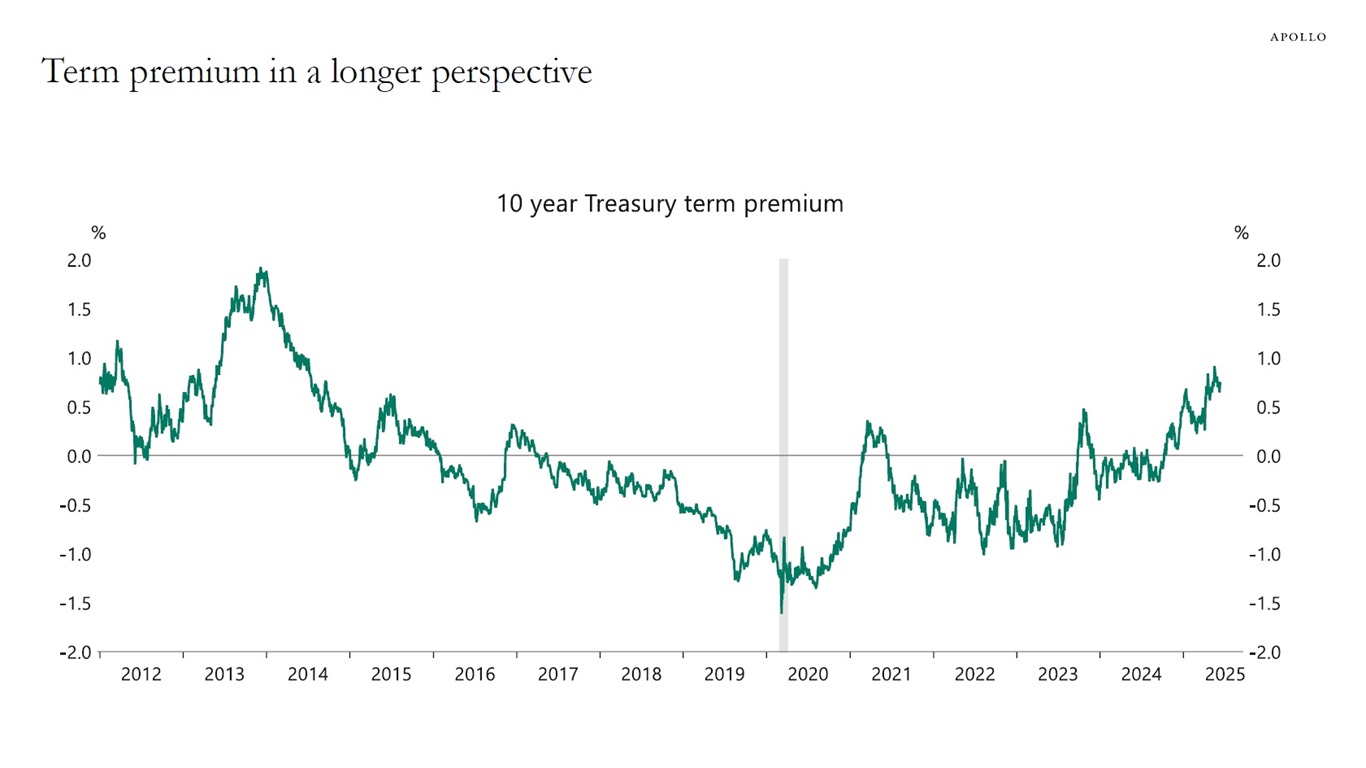

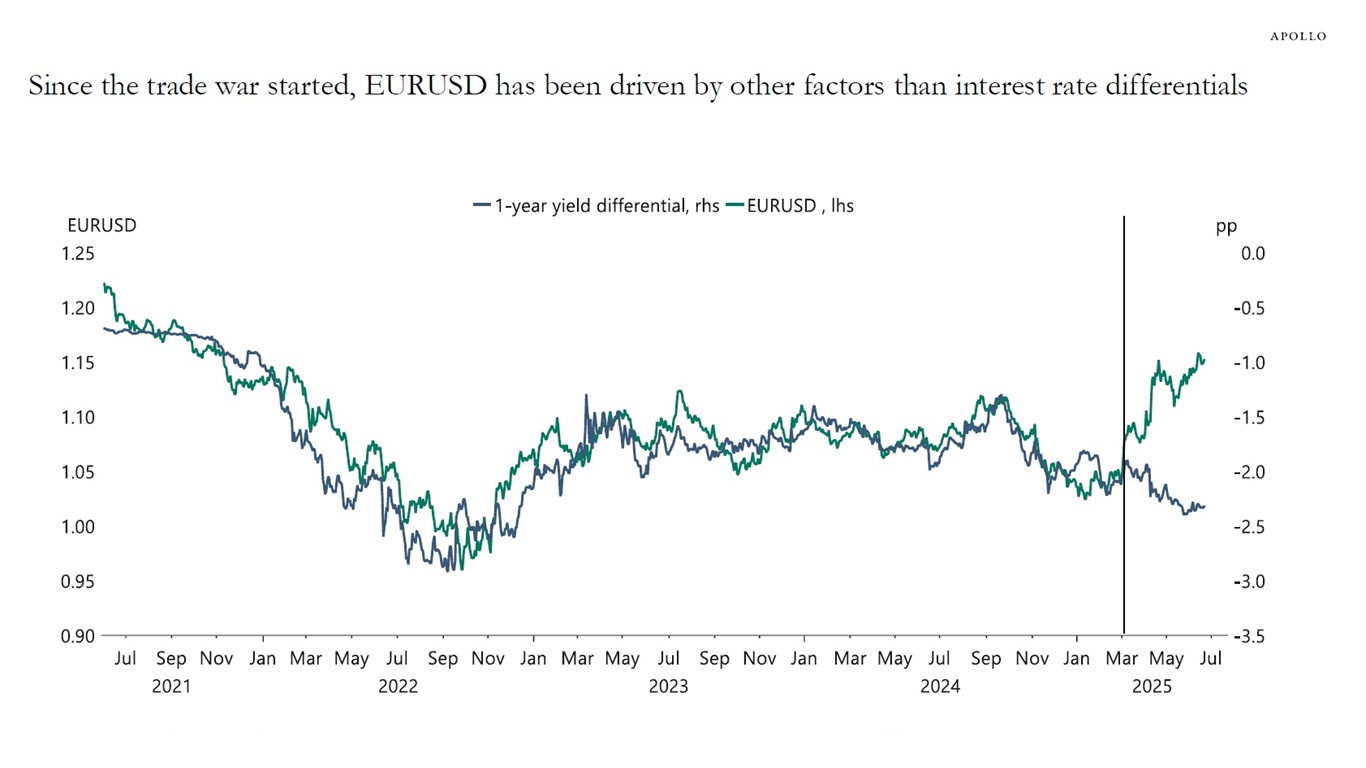

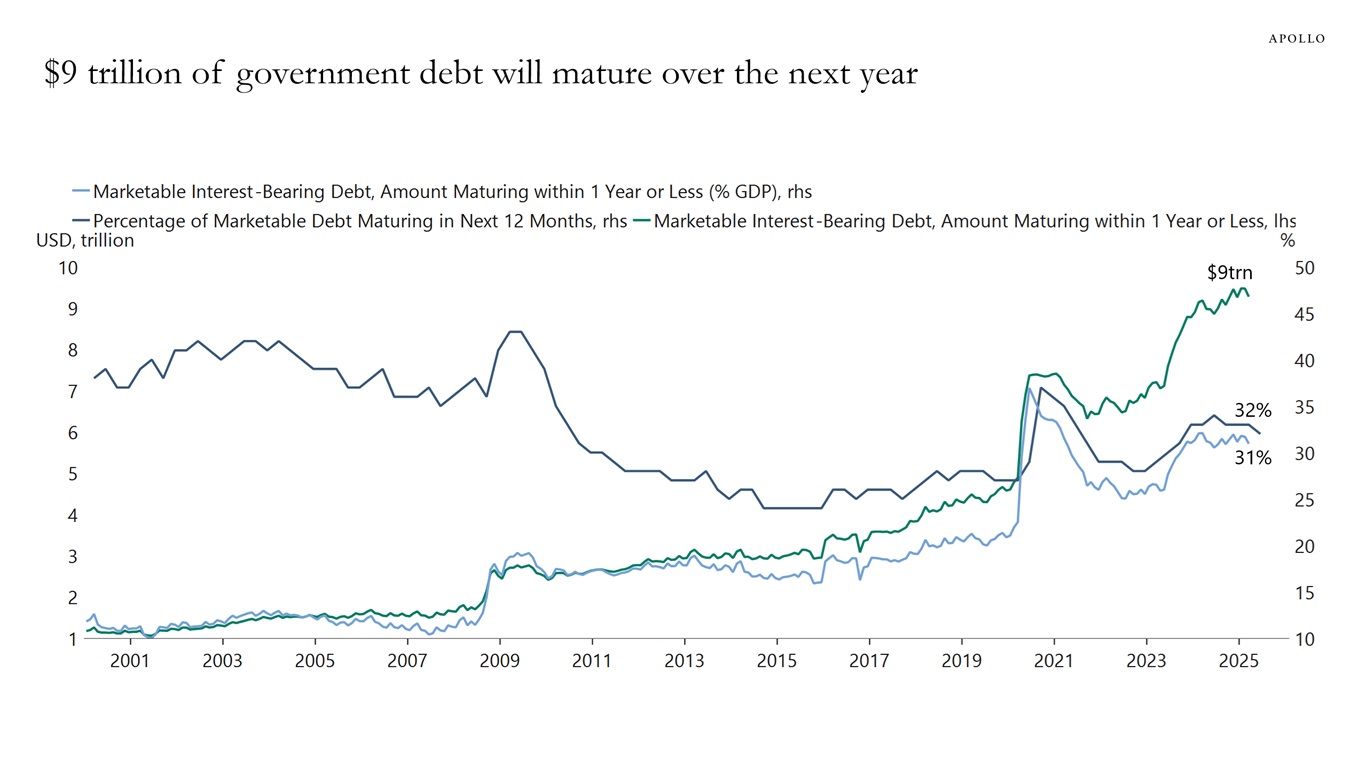

These charts, however, offer little comfort when considering the rising trend in debt-to-GDP, the increasing term premium, the falling dollar, and the $9 trillion that the US government needs to refinance over the next 12 months, see the following four charts below.

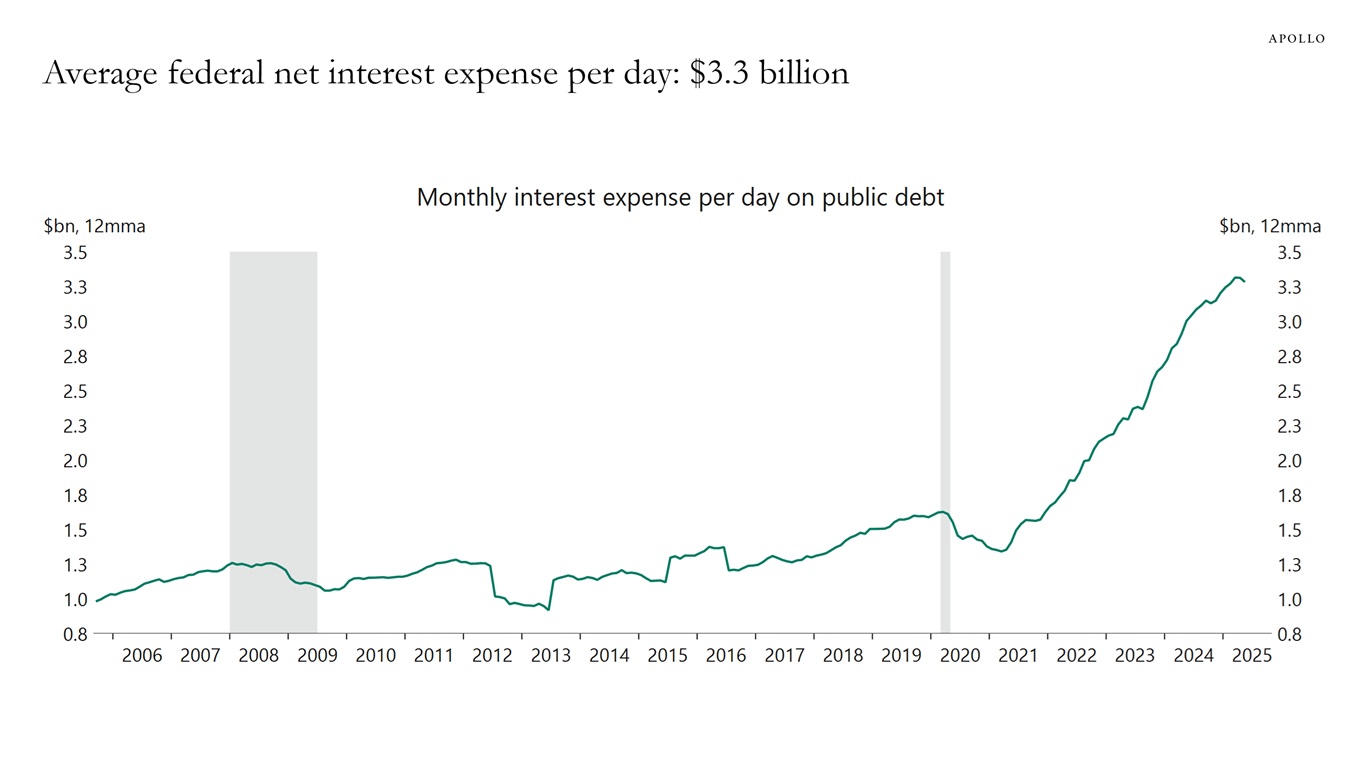

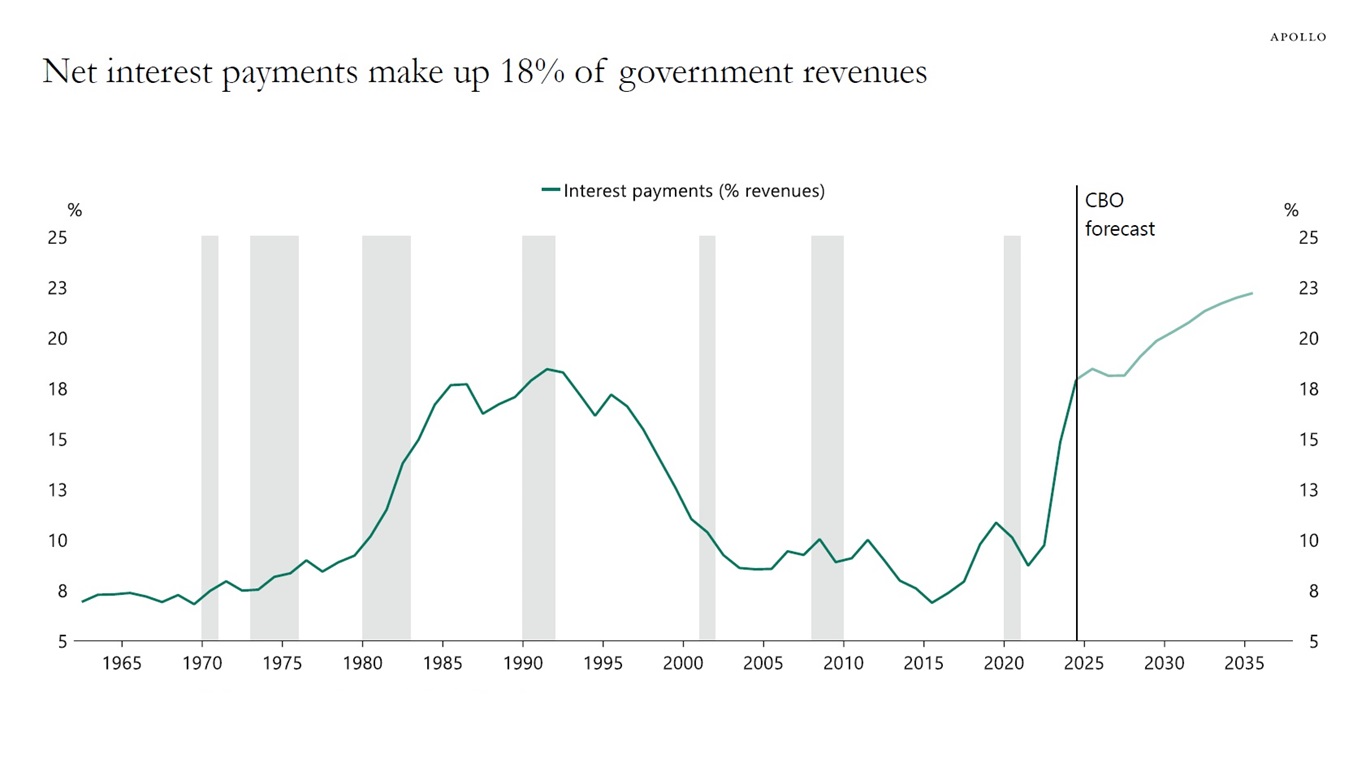

In particular, debt-servicing costs are rising rapidly, and the US government currently pays a record-high $3.3 billion in interest payments every day, and for every dollar the US government collects in tax revenue, about 20 cents go to paying interest on debt.

With debt levels growing much faster than GDP, the bottom line is that Treasury issuance will continue to grow faster than the economy, and the most likely outcome is that investors will demand compensation in the form of higher long-term interest rates.

In sum, there is upside pressure on short rates from higher oil prices, higher tariffs, and restrictions on immigration, and there is upside pressure on long rates because of fiscal challenges.

This is obviously very important for investors in both public and private markets.

Our updated chart book looking at demand and supply for US Treasuries is available here.