The Nobel Prize–winning economist Robert Solow said in 1987, “You can see the computer age everywhere but in the productivity statistics.” This observation is the so‑called Solow productivity paradox.

The same can be said today: AI is everywhere except in the incoming macroeconomic data.

Today, you don’t see AI in the employment data, productivity data or inflation data. Similarly, for the S&P 493, there are no signs of AI in profit margins or earnings expectations.

Maybe there is a J‑curve effect for AI, where it takes time for AI to show up in the macro data. Maybe not.

Whether there is a J-curve effect depends on the value creation from AI. There is fierce competition between the builders of large language models (LLMs), which is driving the price of LLMs toward zero for end-users. This is the opposite of what the finance textbook says, namely that an innovator will have monopoly pricing power until others arrive with a similar product. This is what we saw during the computer age in the 1980s.

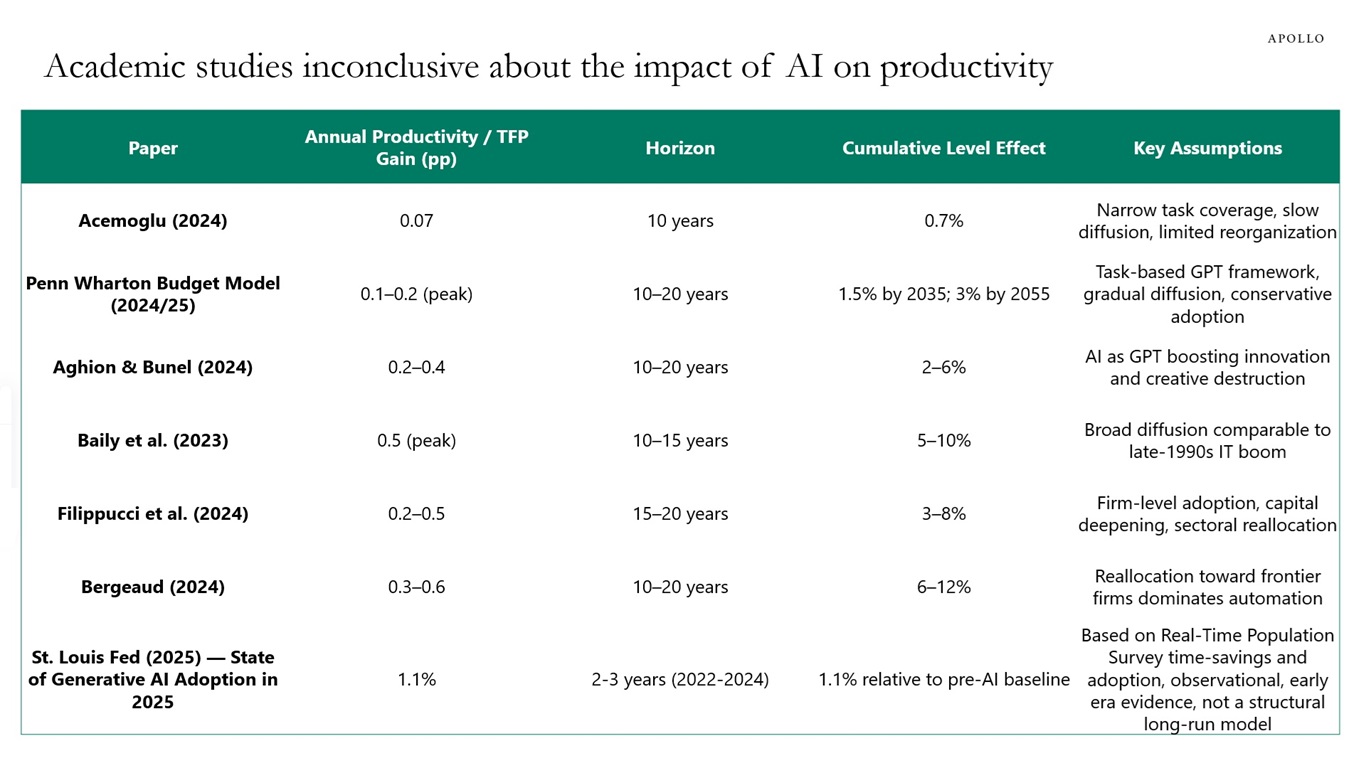

In other words, from a macro perspective, the value creation is not the product, but how generative AI is used and implemented in different sectors in the economy. The academic literature is still inconclusive about the potential macro effects of AI, see table below.

After three years with ChatGPT and still no signs of AI in the incoming data, it looks like AI will likely be labor enhancing in some sectors rather than labor replacing in all sectors.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.