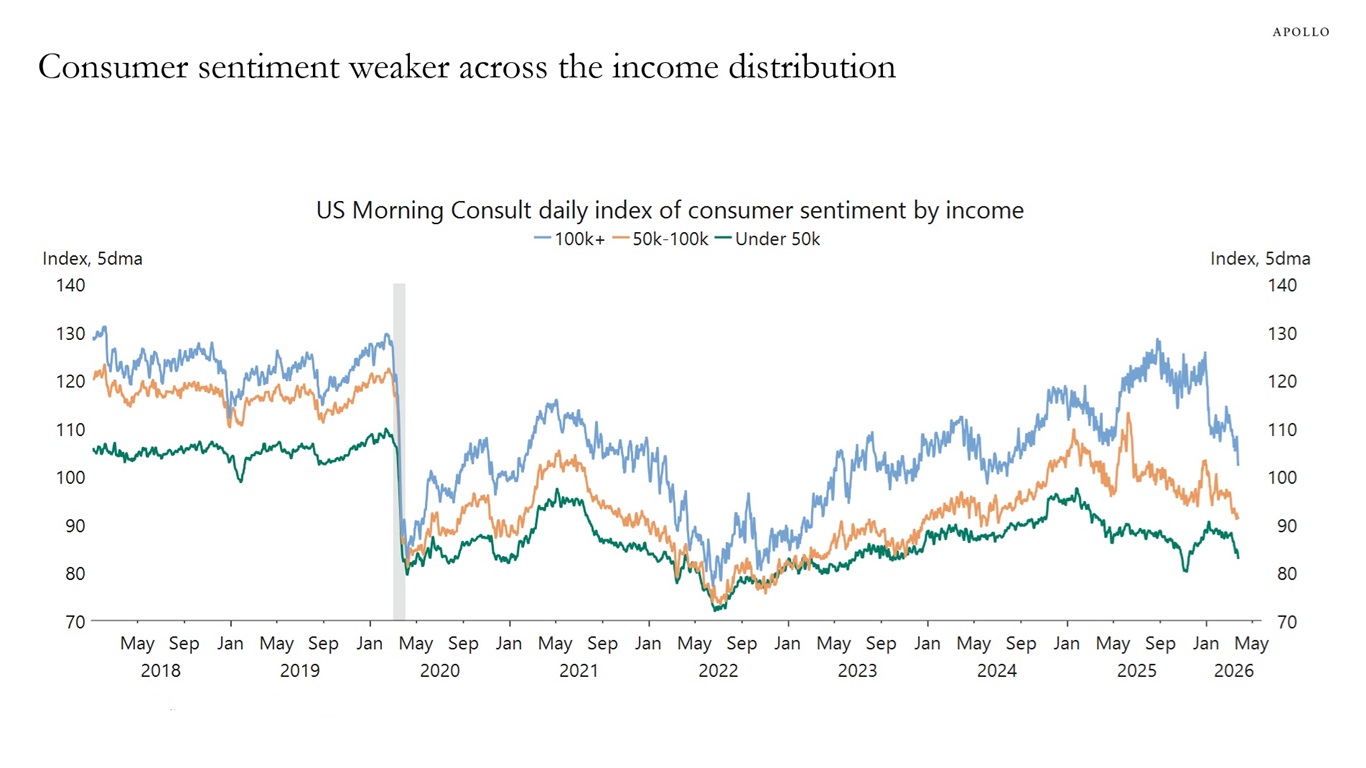

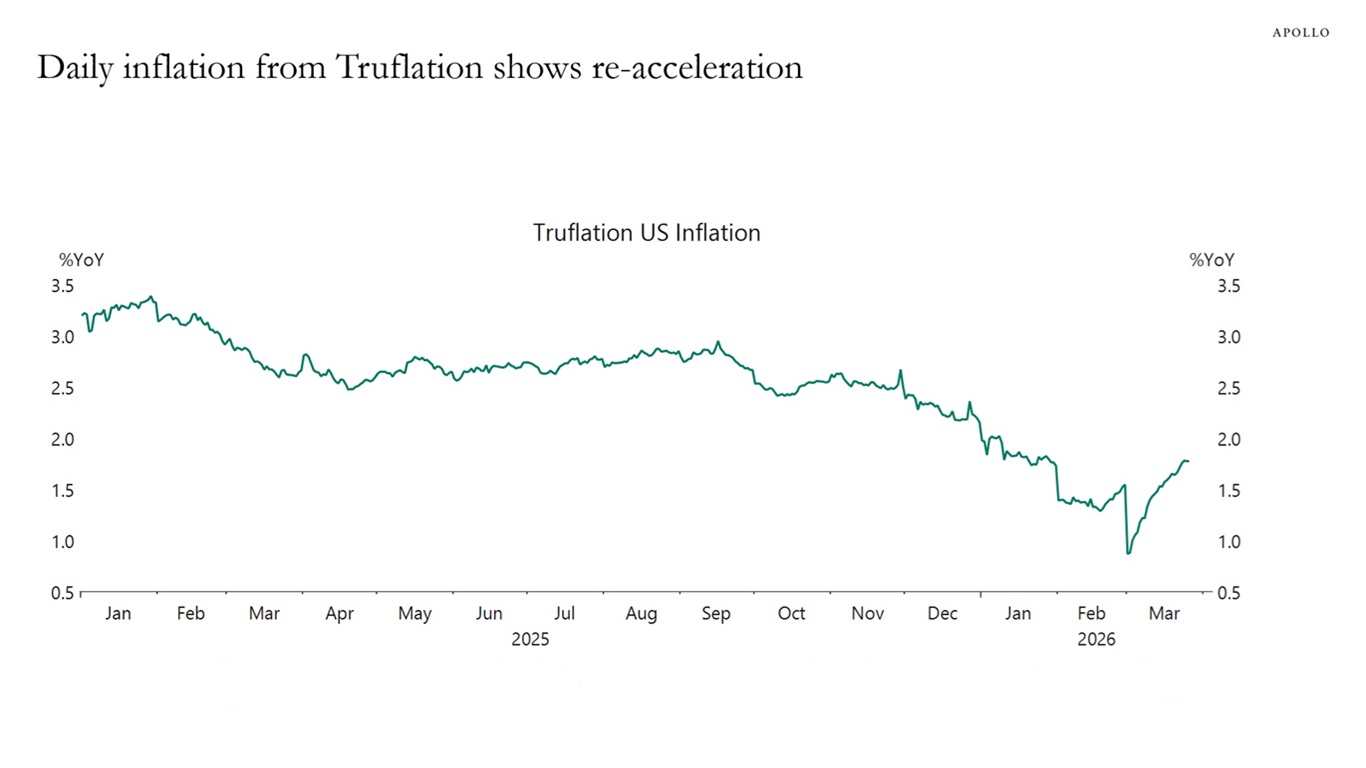

Daily data are starting to show a significant deterioration in inflation expectations and consumer sentiment across the income distribution, see the first two charts below.

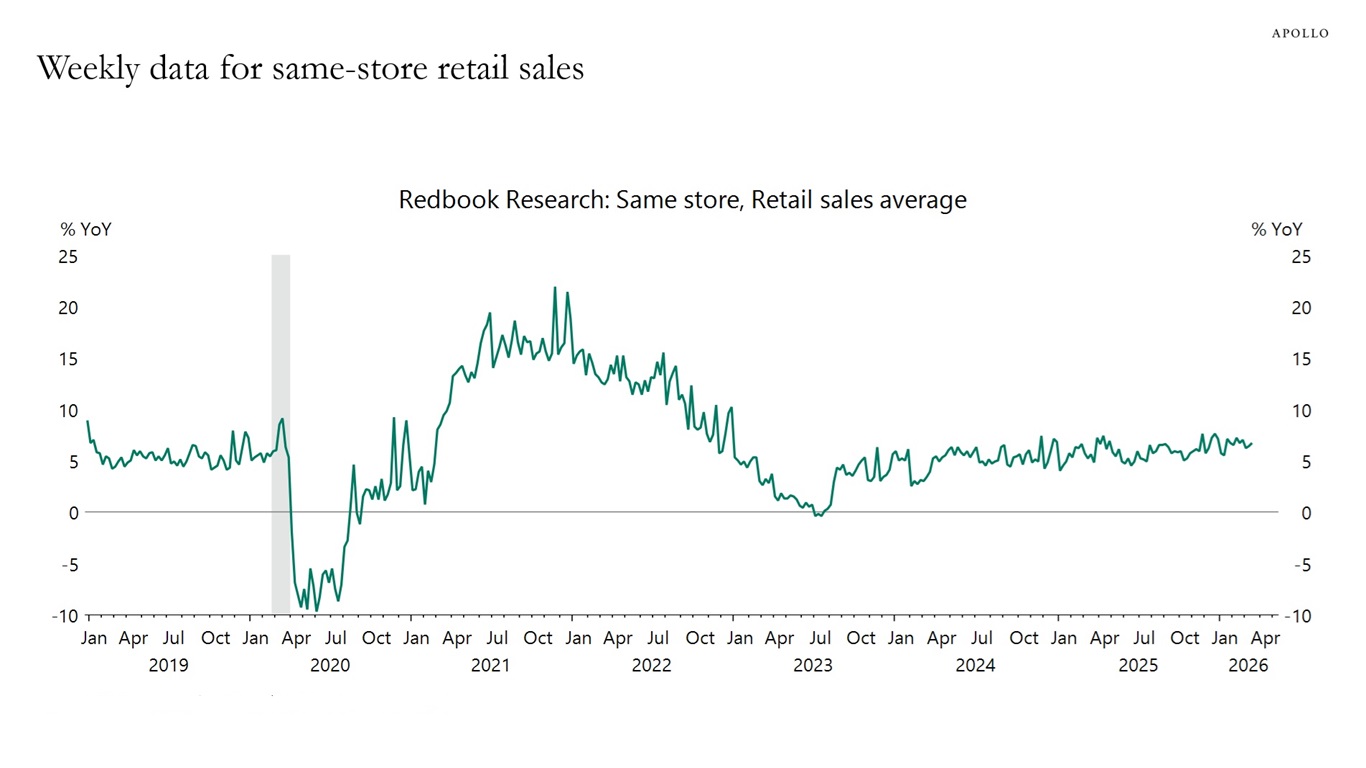

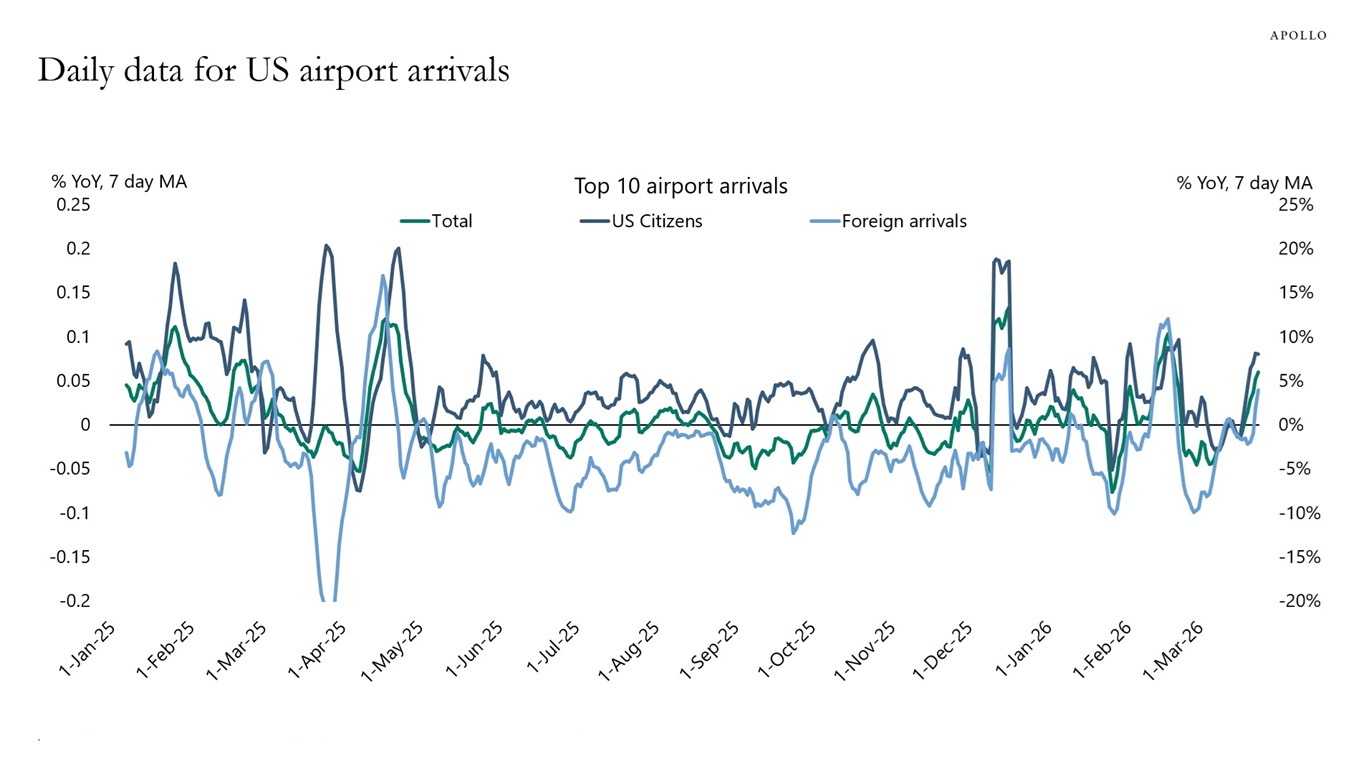

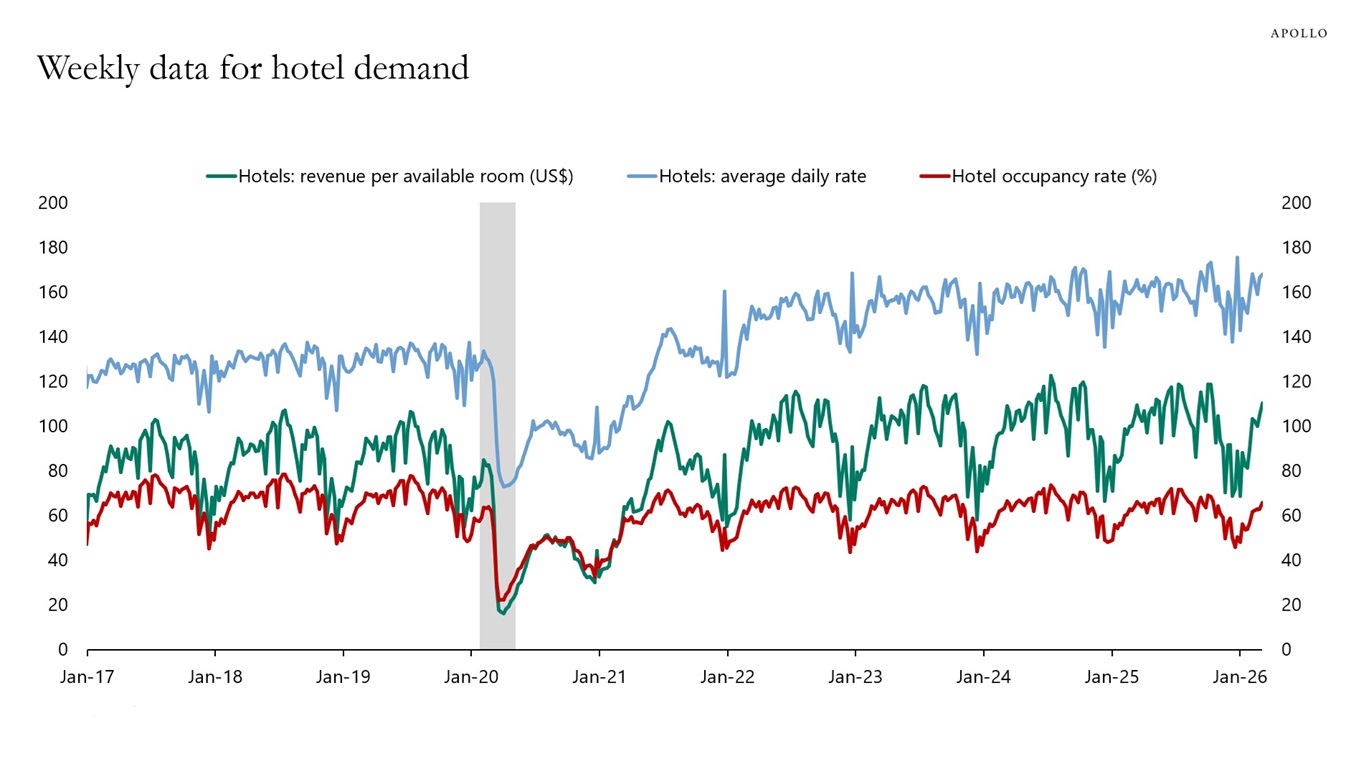

But there is a difference between what consumers are saying and what they are doing. The third, fourth and fifth charts below show that weekly data on consumer spending remain strong, daily data on airline travel remain strong and weekly data on hotel demand remain strong. A full review of all publicly available daily and weekly indicators shows no signs of demand destruction, see our chart book here.

Markets are overreacting to what will likely be a 4- to 6-week period of volatility, which will ultimately result in 50 years of stability in oil markets, supply chains and geopolitics. The Gulf region will become more stable and even more closely integrated with the global economy. For the Fed, the rise in inflation due to higher oil prices is temporary; once the conflict is over, Fed cuts will be priced in again, and long rates will decline.

The bottom line is that the Iran shock is not big enough to offset the strong tailwinds to the US economy from AI spending, the industrial renaissance and the One Big Beautiful Bill.

Sources: Morning Consult, Bloomberg, Macrobond, Apollo Chief EconomistNote: The Truflation US Inflation Index is a daily measure of US inflation based on data from over 30 sources, including major retailers like Amazon and Walmart, and real estate data from sources like Zillow. It tracks price changes from a consumer cost of living perspective across 12 spending categories and is differentiated from the traditional Consumer Price Index (CPI) by its daily updates, use of digital data and a methodology that leverages blockchain for immutability and decentralization. Sources: Truflation, Bloomberg, Macrobond, Apollo Chief EconomistSources: Redbook Research Inc., Macrobond, Apollo Chief EconomistNote: Airports included are ATL, LAX, DFW, MIA, ORD, DEN, IAD, SFO, MCO and JFK. Sources: CBP, Apollo Chief EconomistSources: STR, Haver Analytics, Apollo Chief Economist

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.