The Daily Spark is moving to Apollo.com— read the latest from Torsten Slok here.

Want it delivered daily to your inbox?

-

To gauge the health of the US consumer, we typically examine the monthly data on retail sales from the Census Bureau and the personal consumption expenditures from the BEA. But with the shutdown continuing, we are not getting this government data at the moment.

Instead, we have to look at alternative data from the private sector. Unfortunately, the alternative data is not sending a consistent message about the US consumer.

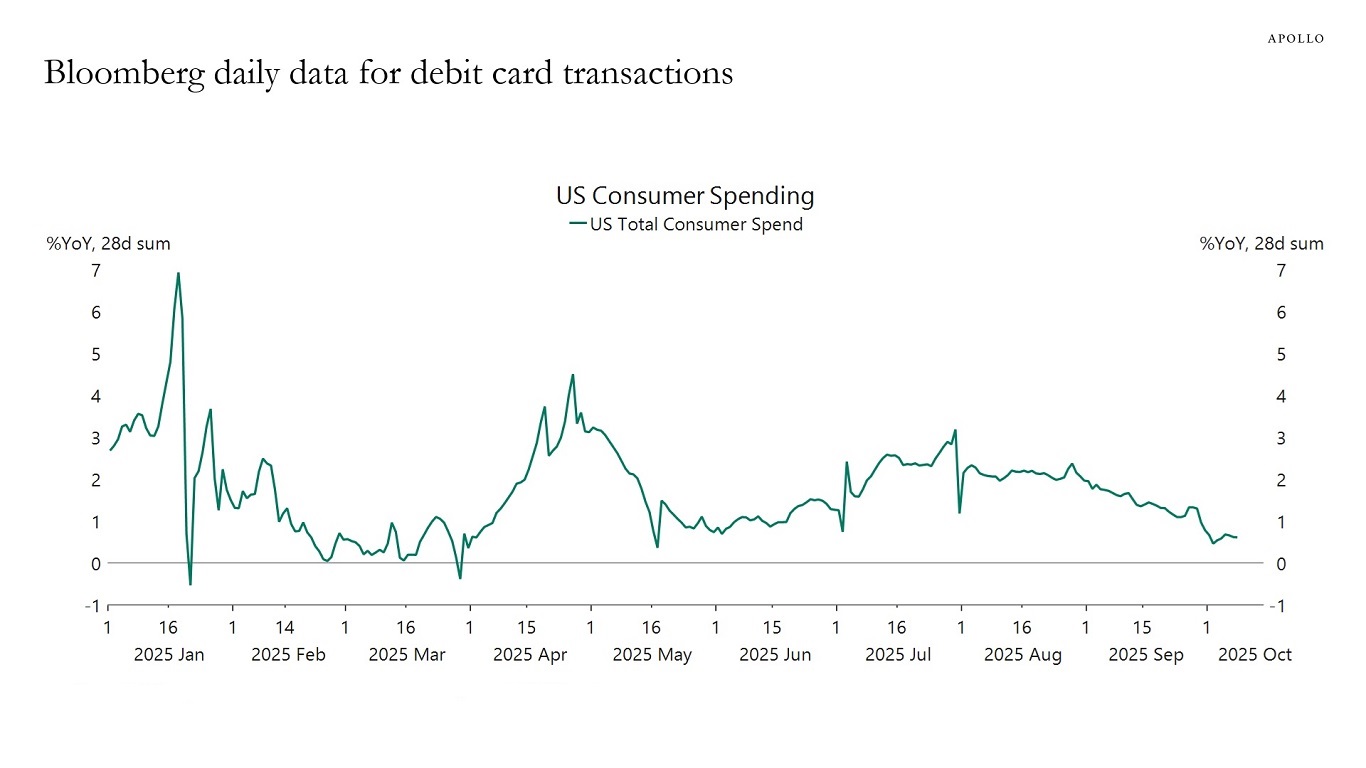

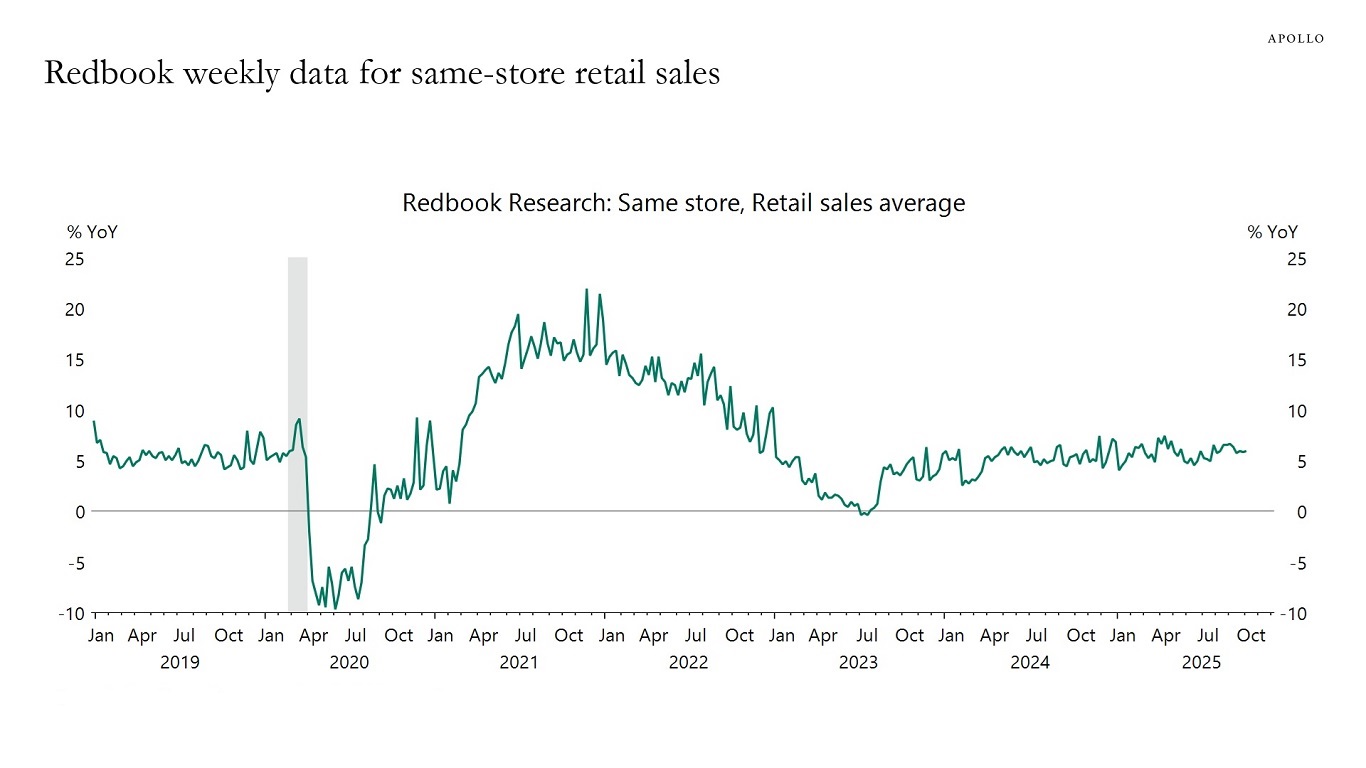

The daily data for debit and credit card spending from Bloomberg shows a slowdown in recent weeks, see the first chart below. This is in contrast to the Redbook weekly same-store retail sales, which show continued strength, see the second chart.

We are monitoring this divergence closely.

Our updated chart book with private sector data for consumer spending, the labor market, inflation, housing, production and consumer sentiment is available here.

Sources: US Bloomberg Second Measure Consumer Spend, Macrobond, Apollo Chief Economist

Sources: Redbook Research Inc., Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

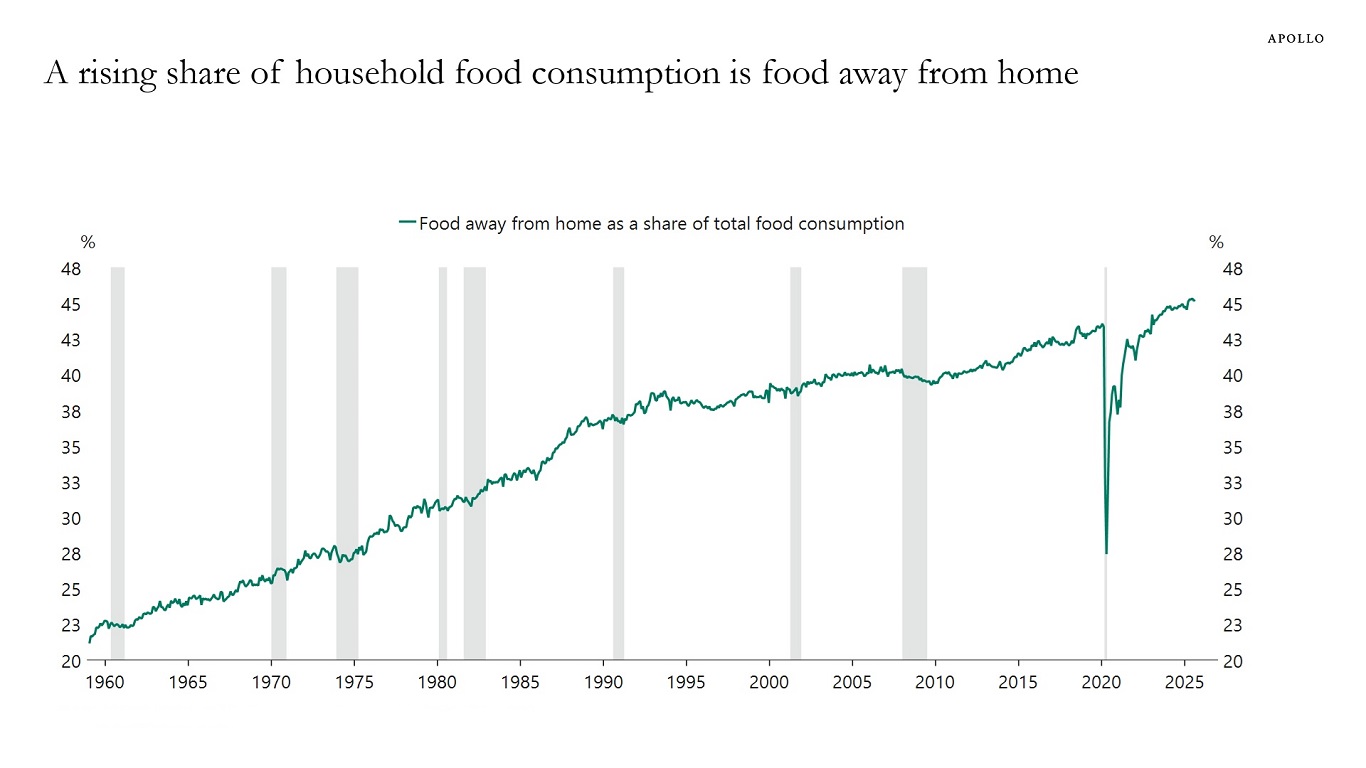

Households now spend almost as much on restaurants, takeout and delivery as on groceries eaten at home.

Sources: US Bureau of Economic Analysis (BEA), Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

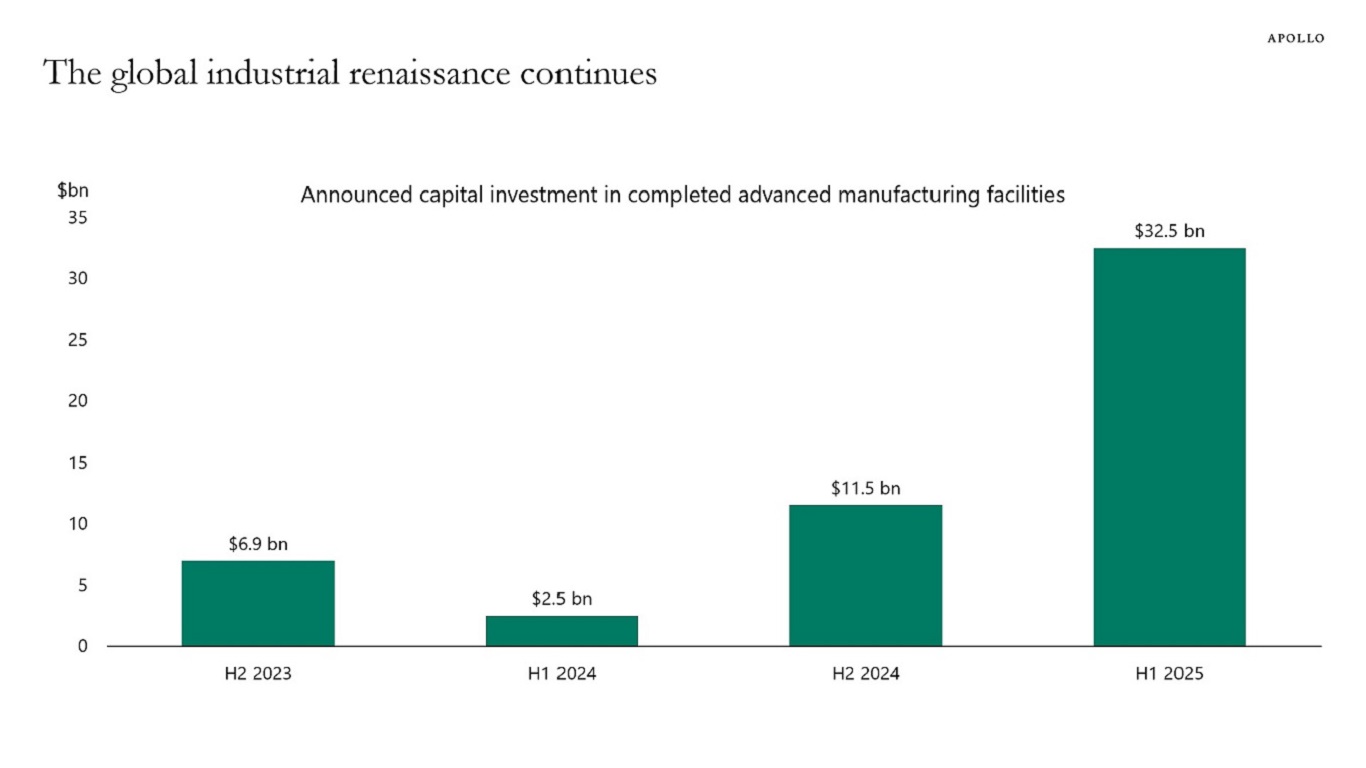

The US manufacturing cycle is gaining traction. With nearly 200 factory completions since mid-2023 and a $590 billion pipeline led by $5 billion-plus megaprojects, advanced manufacturing is set to be a durable growth engine for the US economy with positive spillovers to industrial real estate, private credit and nationwide employment, see chart below.

Sources: Bridge Investment Group, publicly available reports and press releases from Industry Select, Industry Week, Manufacturing Dive, Reuters and US Manufacturing report, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

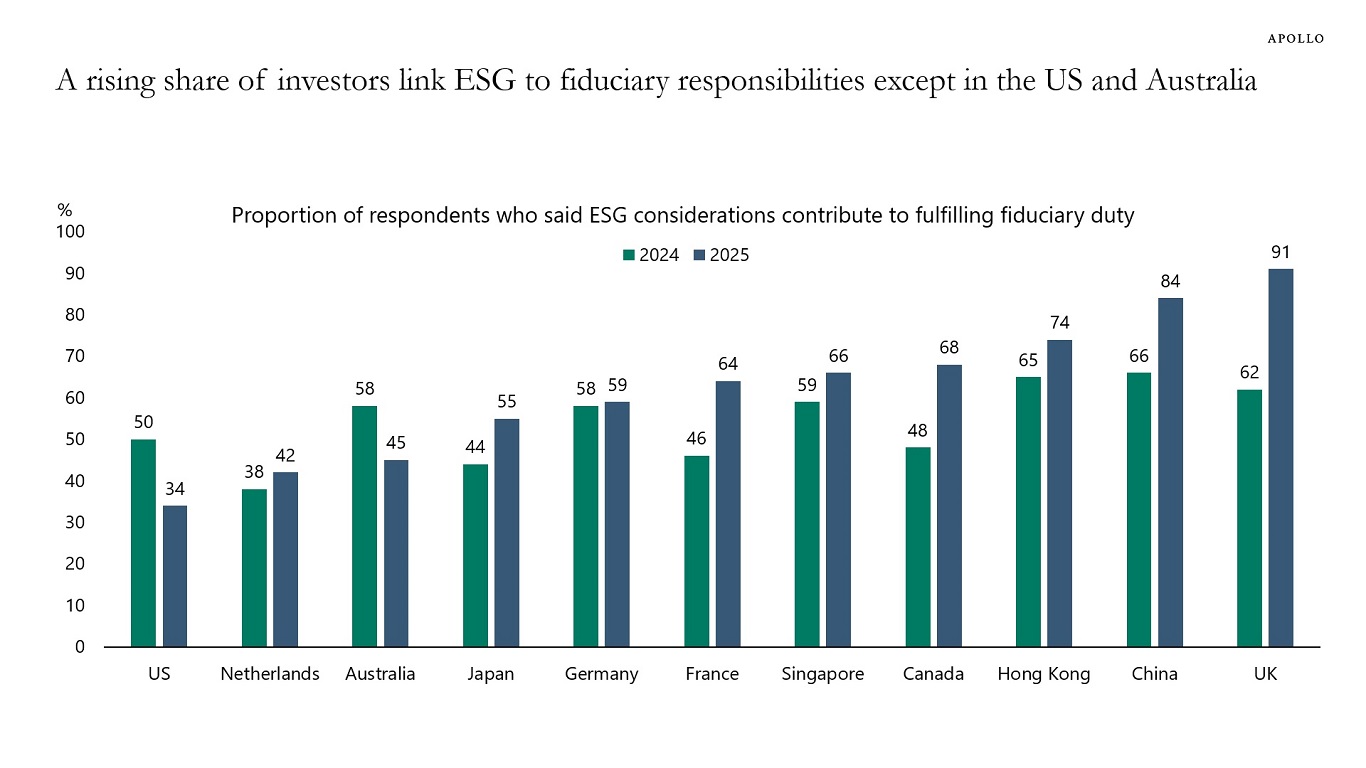

According to a recent Morningstar survey, the proportion of investors who view ESG as part of their fiduciary duty has increased in most surveyed countries, with notable declines in the US and Australia, see chart below.

Sources: Morningstar (Voice-of-the-Asset-Owner-Survey-2025-Quantitative-Analysis.pdf), Apollo Chief Economist See important disclaimers at the bottom of the page.

-

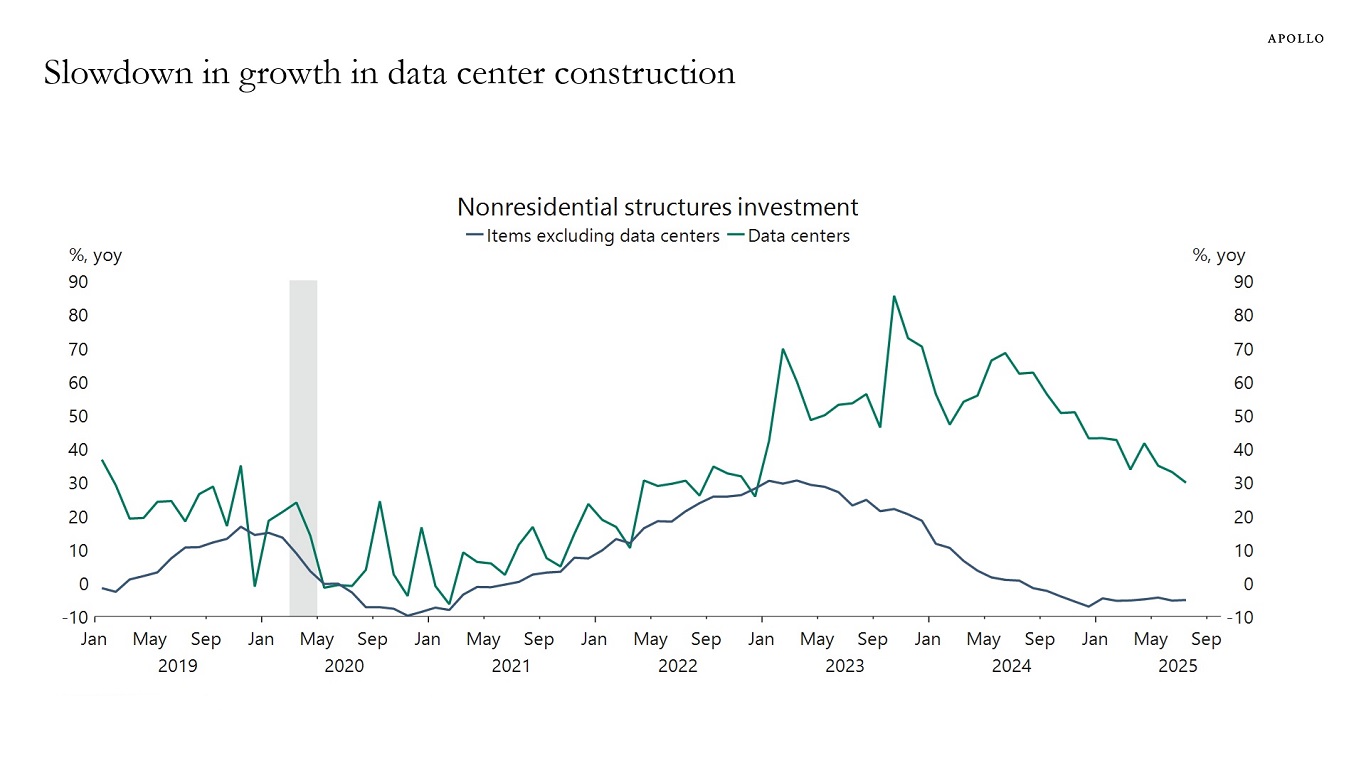

There is still strong growth in data center construction, but the current growth rate at 30% is lower than the 80% observed two years ago, see chart below.

Sources: US Census Bureau, Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

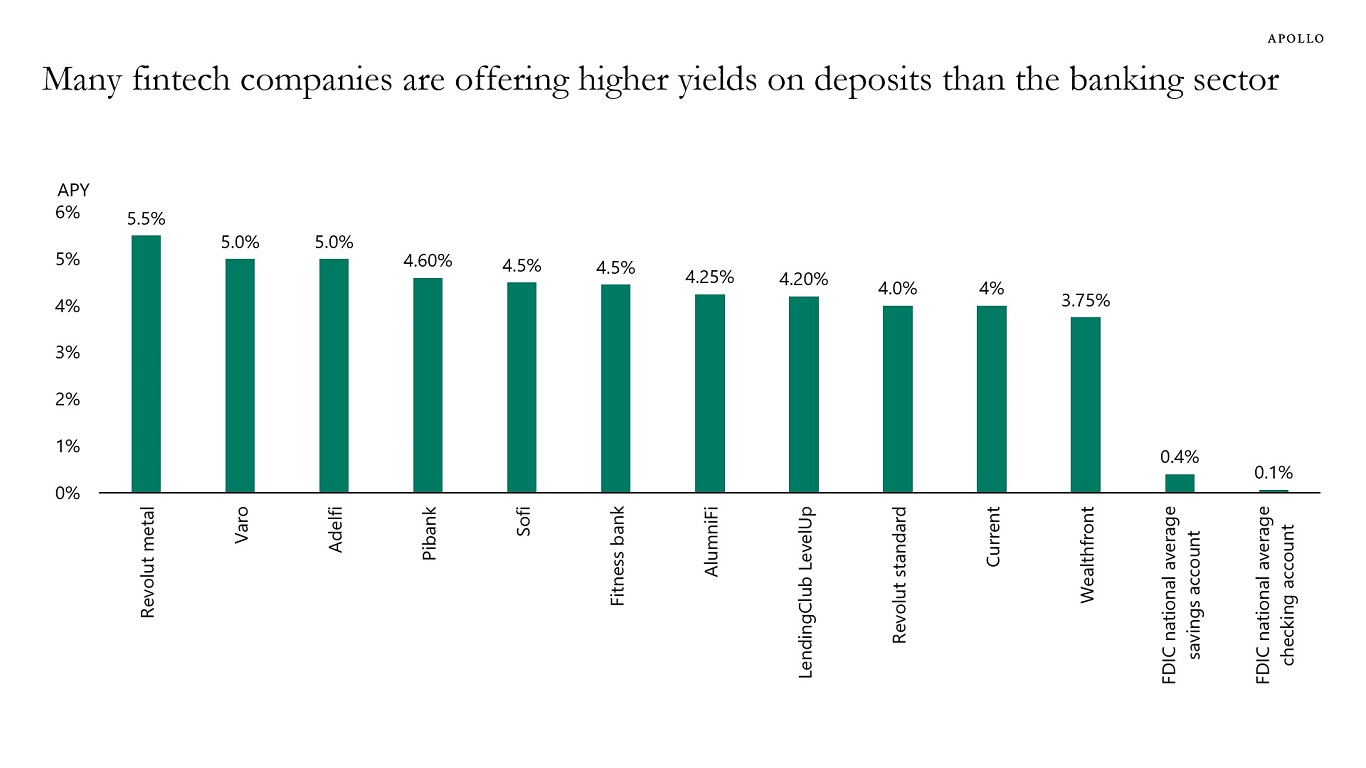

Yield levels on deposits in many fintech companies are dramatically higher than yield levels on deposits in the banking sector, see chart below. It is a fundamental imprudence in banking to finance long-horizon assets with short-term liabilities.

Sources: Revolut, Varo Bank, Adelfi, Pibank, Sofi, FitnessBank, AlumniFi, LendingClub, Current, Wealthfront, FDIC, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

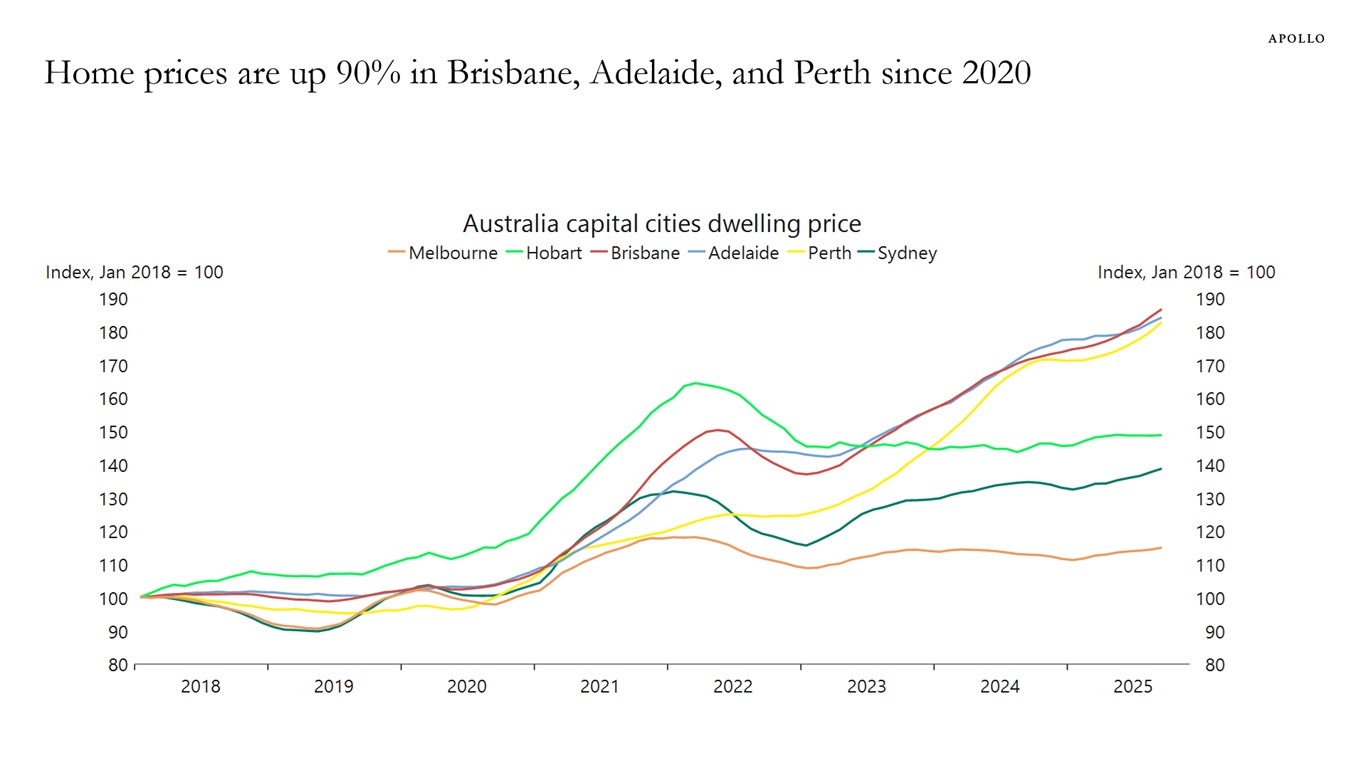

House prices in Brisbane, Adelaide and Perth are up roughly 90% since 2020, see chart below. Home prices in Sydney are up “only” 40% over the same period.

Sources: Cotality Australia, Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

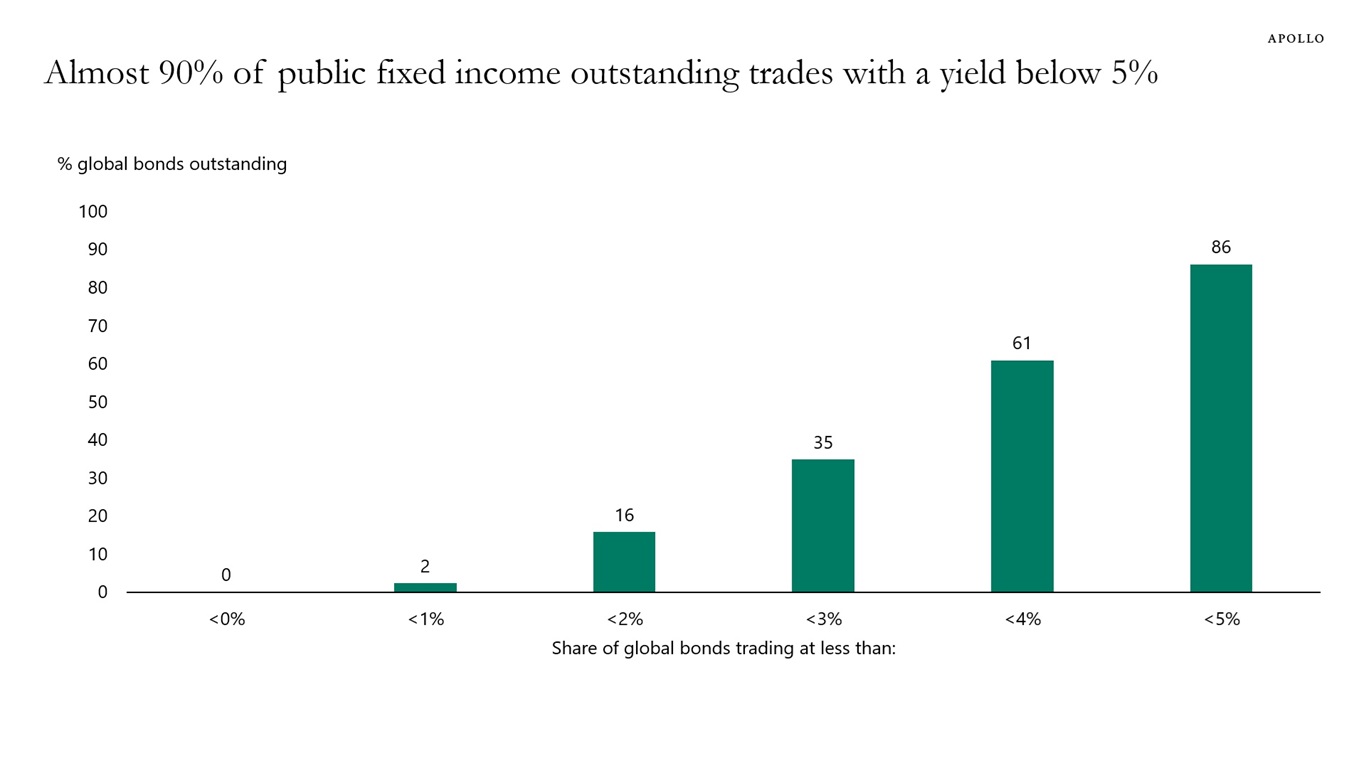

Almost 90% of all public fixed income outstanding in the world trades at a yield below 5%, see chart below.

With inflation at 3%, the real return for investors in public fixed income is a meager 2% or less.

Sources: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

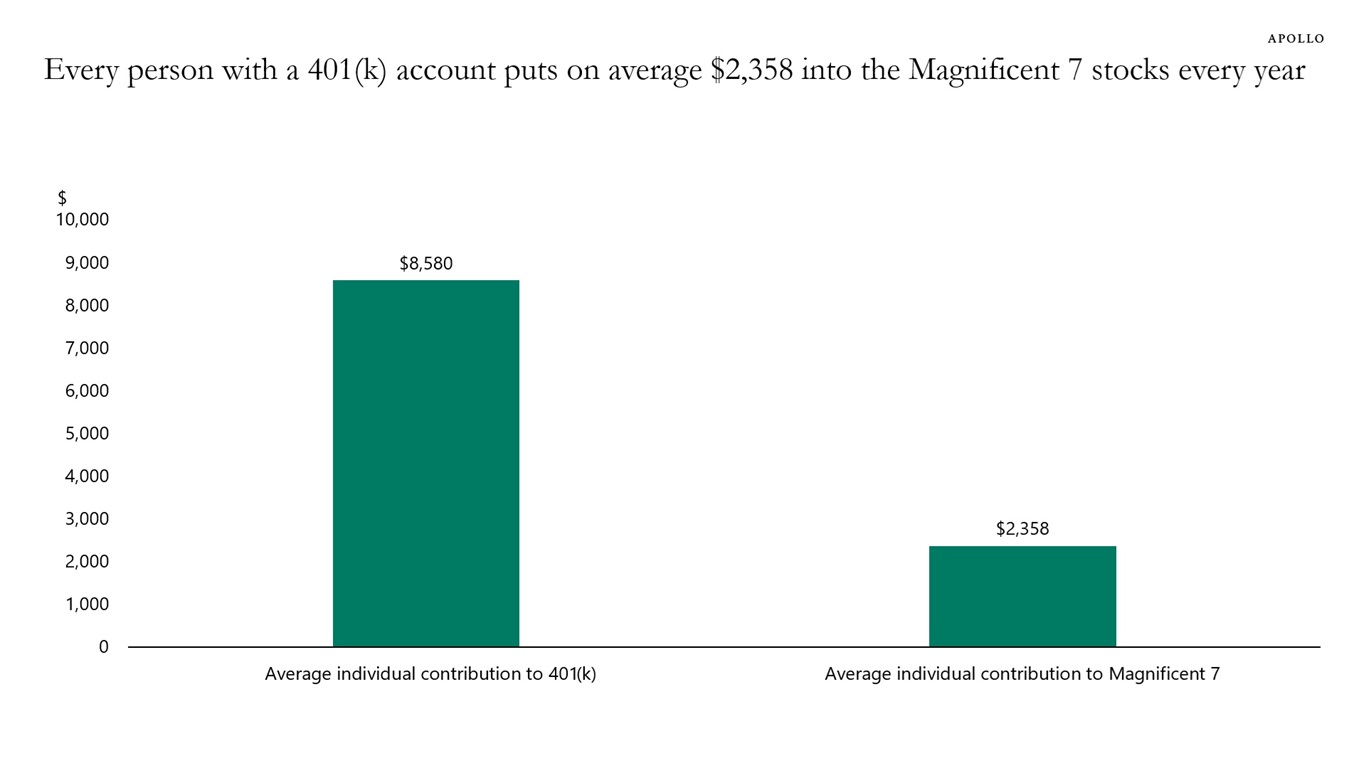

US workers contribute on average around $8,500 to their 401(k) accounts every year, and with 71% of 401(k) assets allocated to equities—and the Magnificent Seven having a weight of almost 40% in the S&P 500—the bottom line is that each worker in the US puts an estimated $2,300 into the Magnificent Seven stocks every year, see chart below.

This is passive money going into the Magnificent Seven regardless of whether their outlook is good or bad.

Note: Average salary is $60,000 and combined average contribution rate is 14.3% and 71% of 401(k) assets are allocated to equities. Source: Apollo Chief Economist See important disclaimers at the bottom of the page.

-

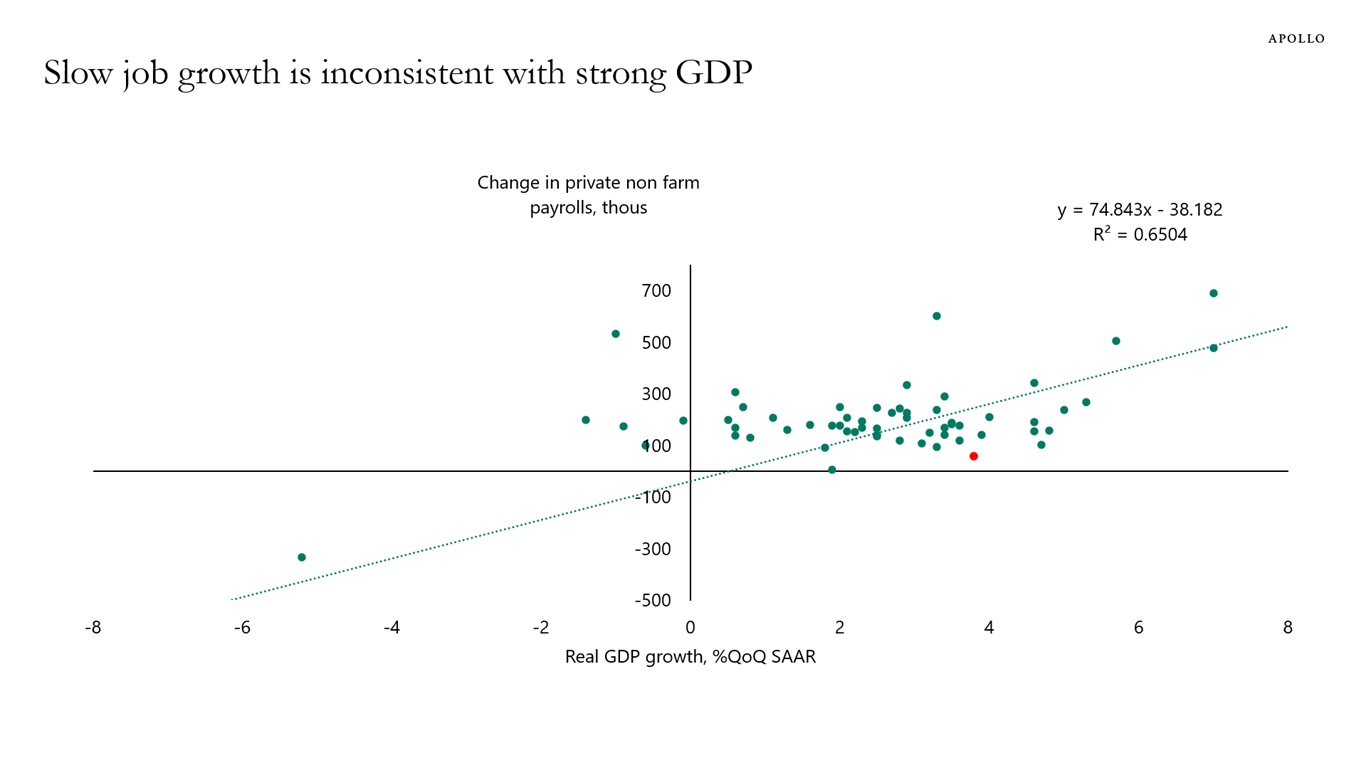

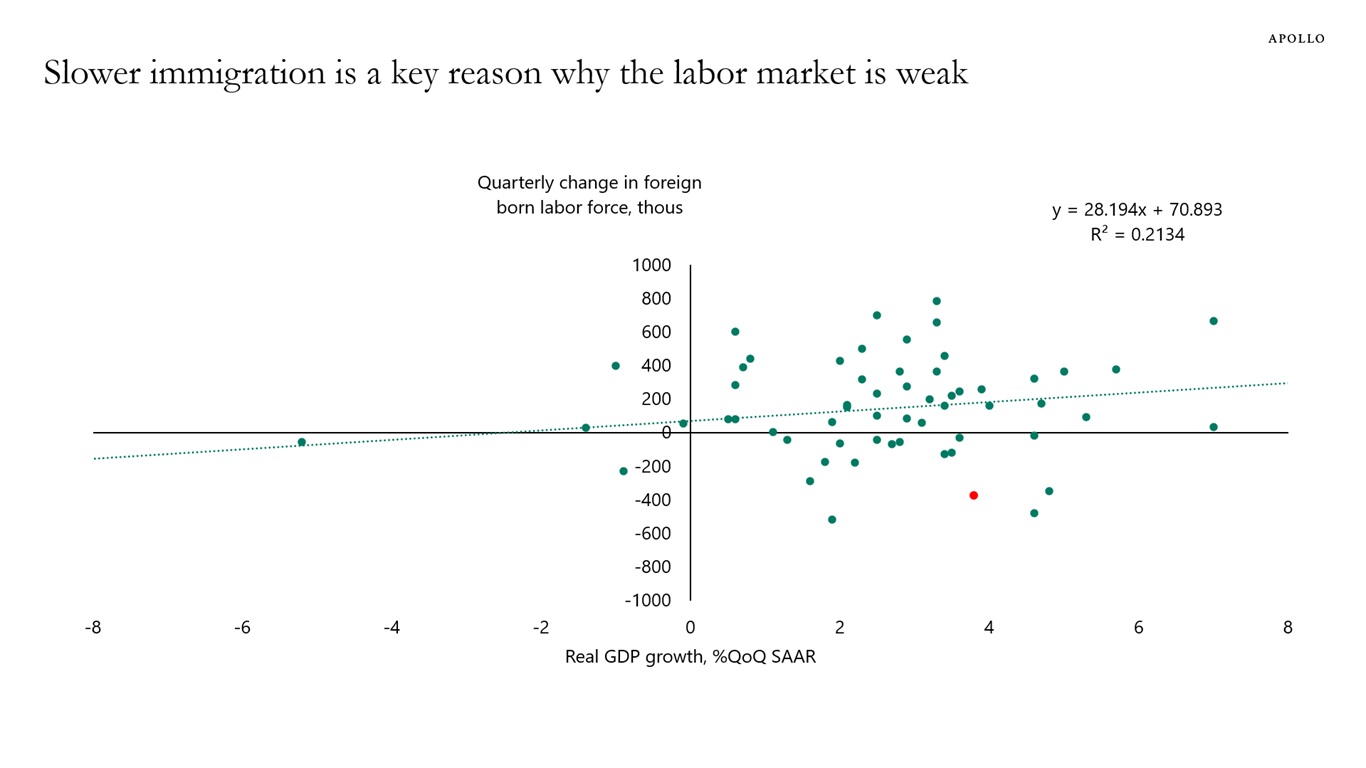

There are three reasons why job growth is slow: 1) Lower immigration, 2) AI implementation and 3) fewer government jobs.

Specifically:

The first chart below shows that at the current level of GDP growth, nonfarm payrolls should be 263k every month.

The second chart indicates that a key reason for the slow job growth is that the growth rate in the foreign-born labor force has been significantly weaker than normal. Fewer people looking for jobs means fewer people get hired.

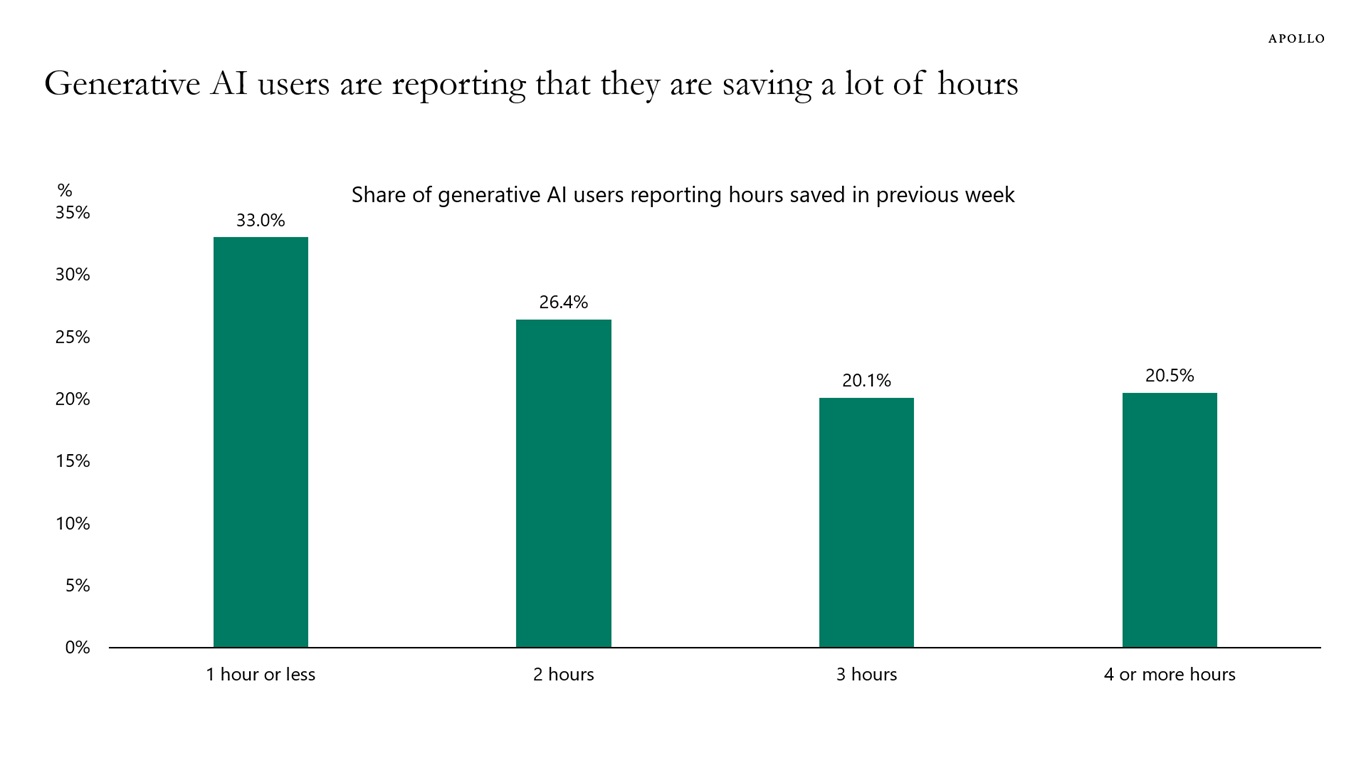

The third chart indicates that AI implementation is likely improving productivity.

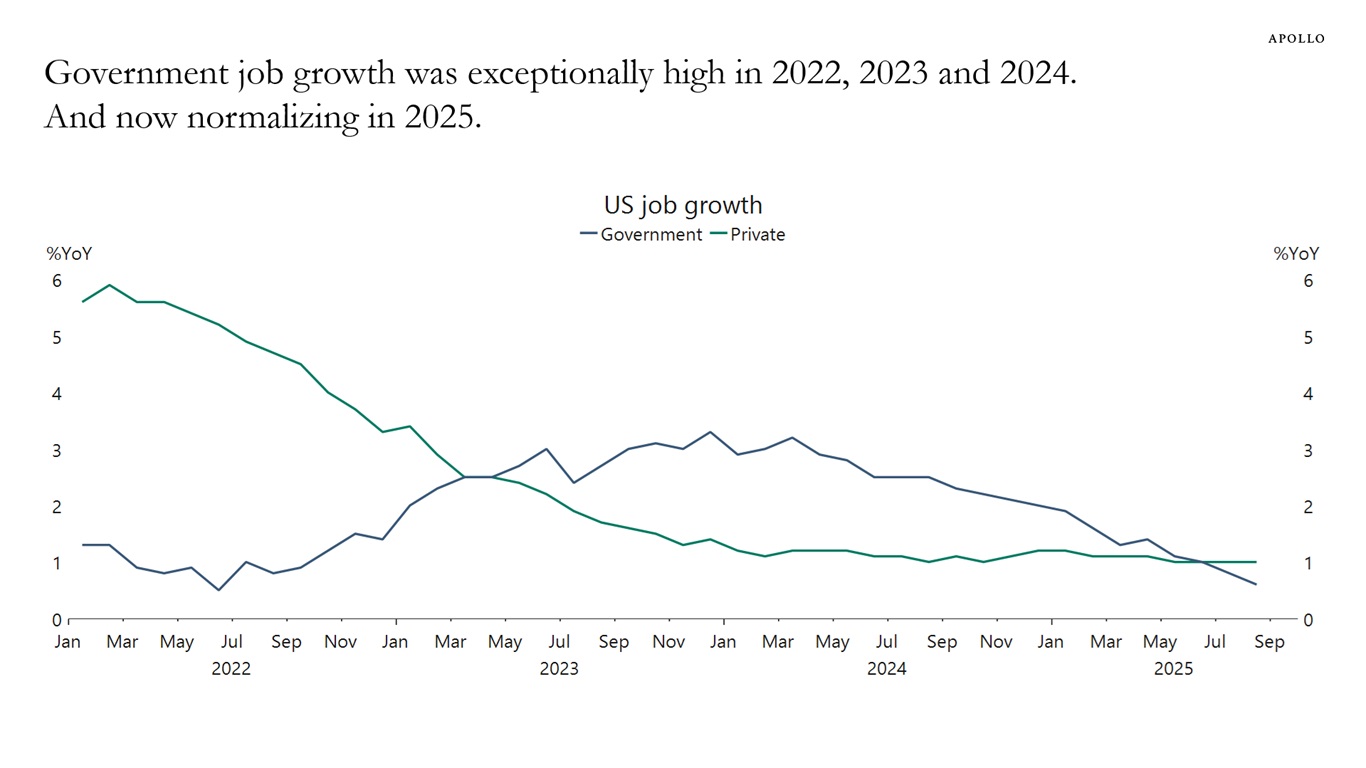

The fourth chart shows that government job growth was artificially high in 2022, 2023 and 2024. Combined with DOGE, government job growth is now returning to more normal levels.

The bottom line is that the weak labor market is not due to weaker labor demand, but rather to weaker labor supply because of immigration, AI implementation and a normalization of job growth in the public sector.

In short, slow job growth is not the result of a slowing economy. Because if it were, then GDP, consumer spending and capex spending would also be slowing.

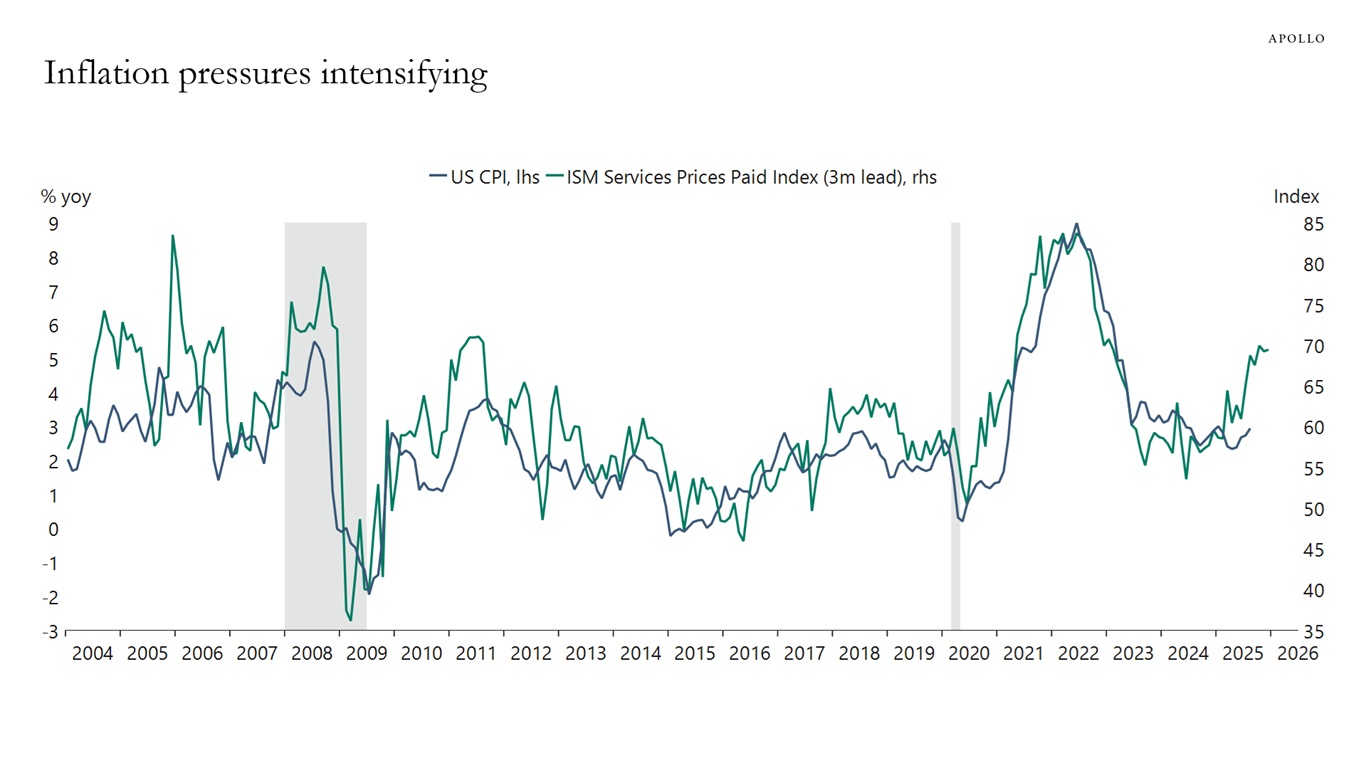

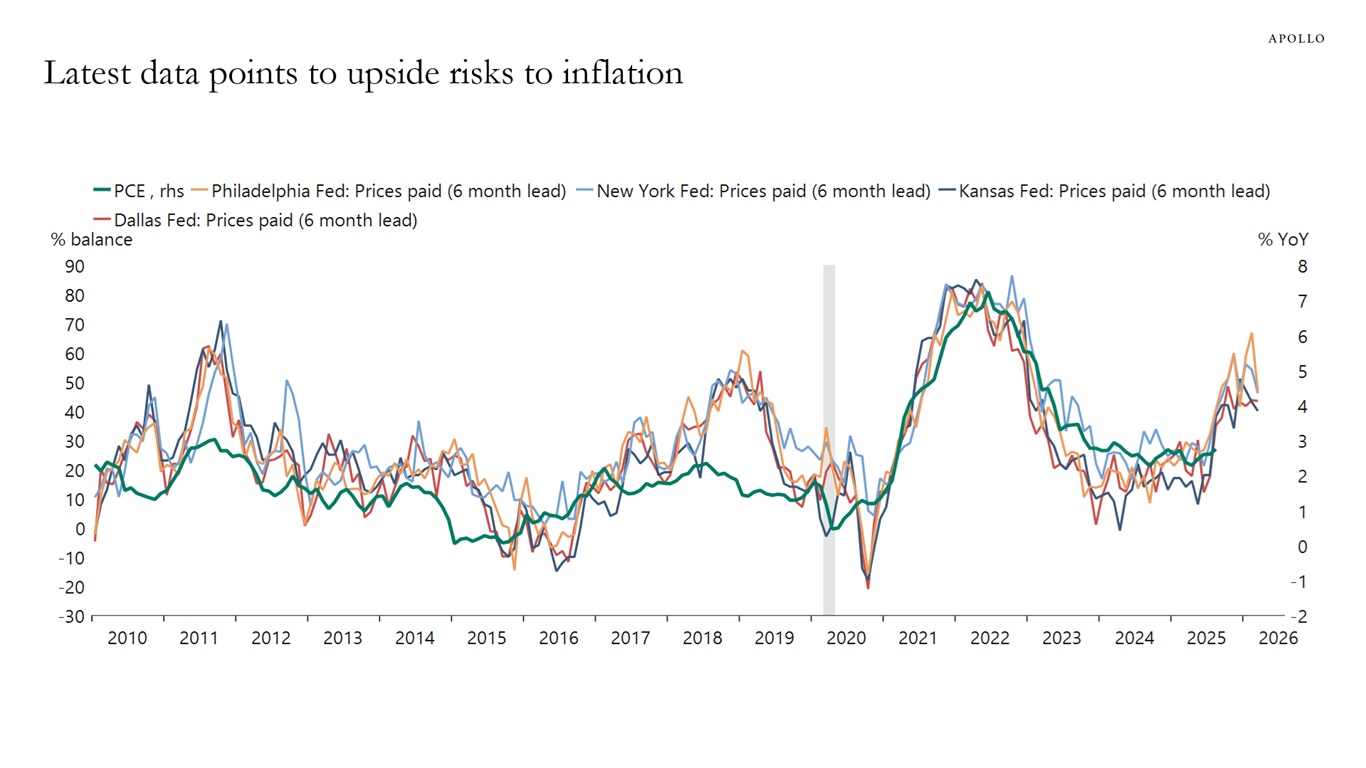

The conclusion is that the Fed should focus less on the slowdown in job growth and more on the ongoing uptrend in inflation, see the fifth and sixth charts.

Sources: BEA, BLS, Haver Analytics, Apollo Chief Economist

Sources: BEA, BLS, Haver Analytics, Apollo Chief Economist

Note: Survey from November 2024. Sources: The Impact of Generative AI on Work Productivity | St. Louis Fed, Apollo Chief Economist

Sources: US Bureau of Labor Statistics (BLS), Macrobond, Apollo Chief Economist

Sources: Institute for Supply Management (ISM), US Bureau of Labor Statistics (BLS), Macrobond, Apollo Chief Economist

Sources: Federal Reserve Bank of Dallas, Federal Reserve Bank of Kansas City, Federal Reserve Bank of New York, Federal Reserve Bank of Philadelphia, US Bureau of Economic Analysis (BEA), Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.