The Daily Spark is moving to Apollo.com— read the latest from Torsten Slok here.

Want it delivered daily to your inbox?

-

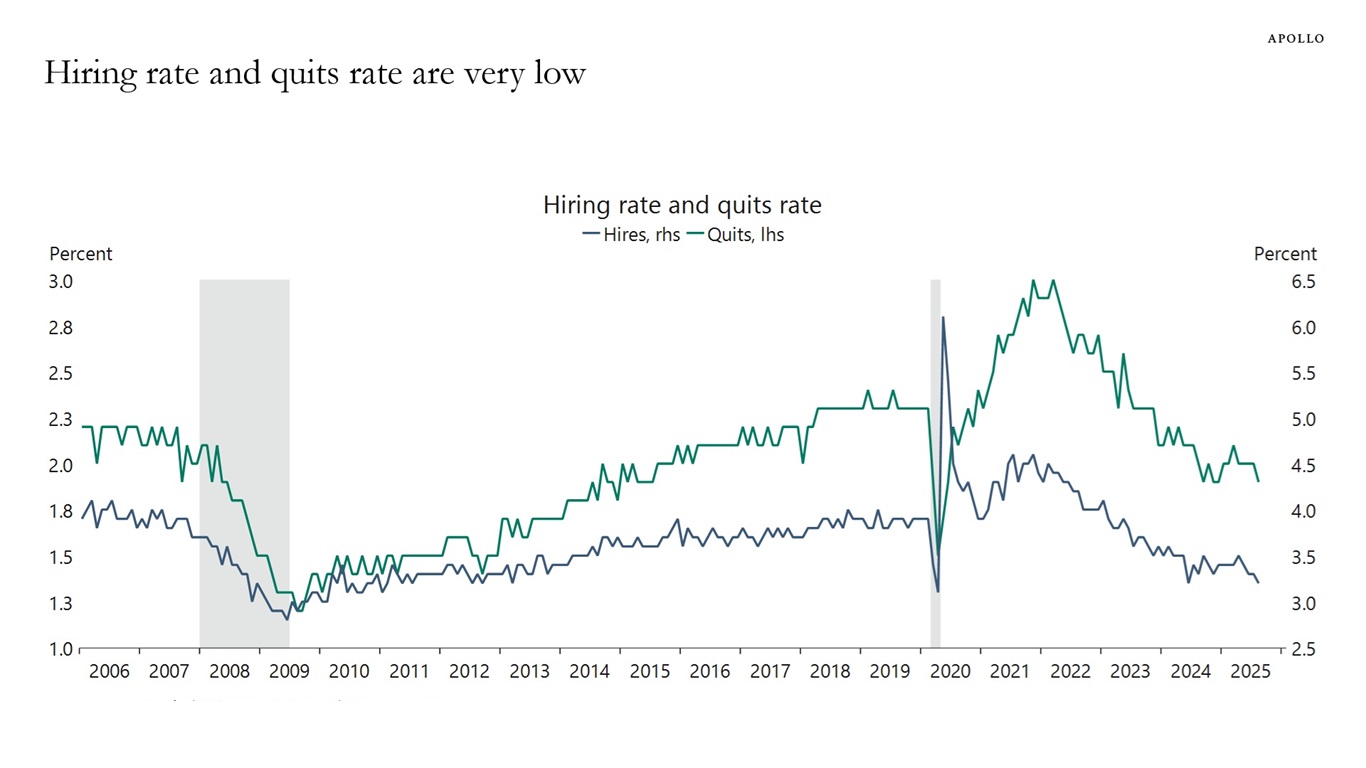

The hiring rate measures the number of hires during the entire month as a percentage of total employment, and it is currently at recessionary levels, see chart below.

Similarly, the quits rate measures the number of employees who voluntarily left their jobs during a month, expressed as a percentage of total employment, and the quits rate is also low.

Combined with a declining number of job openings, rising unemployment, and slower job growth, the bottom line is that the labor market is at a standstill, where workers are not getting hired or voluntarily changing jobs.

Sources: US Bureau of Labor Statistics (BLS), Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

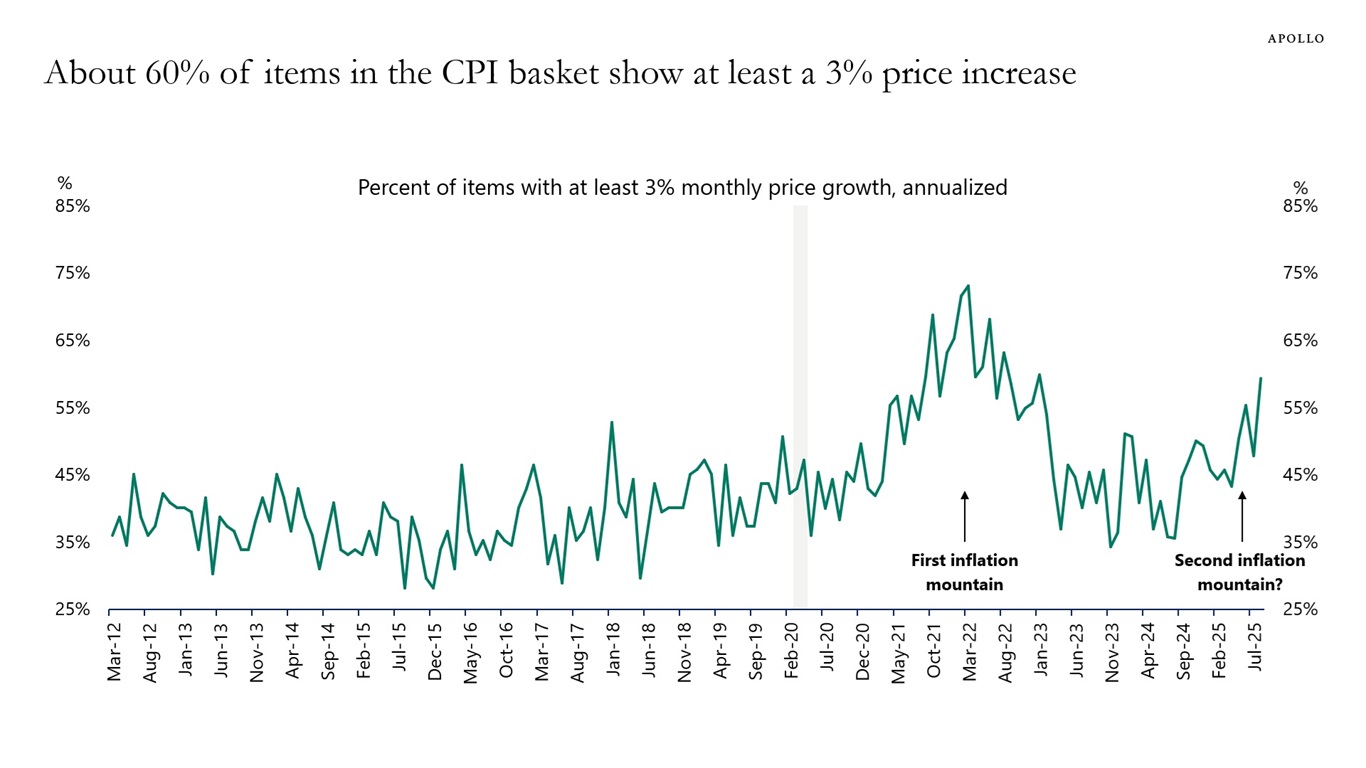

Looking at annualized month-over-month growth rates shows that 60% of items in the CPI basket are growing faster than 3%, see chart below. Is a second inflation mountain emerging?

Sources: BLS, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

We have put together a 75-page chart book with private sector data to monitor during the shutdown, and it is available here. We will update and publish this going forward as long as the shutdown continues.

See important disclaimers at the bottom of the page.

-

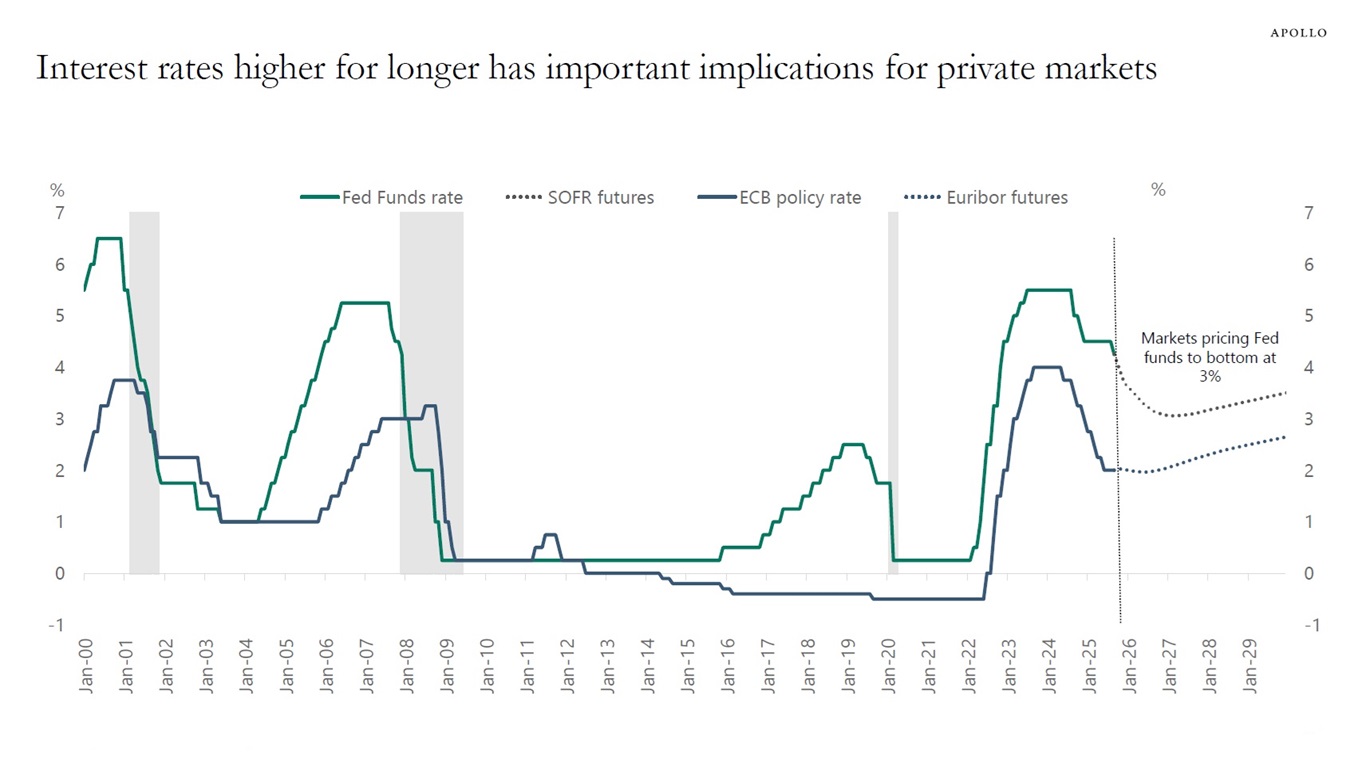

We have updated our outlook for private markets, it is available here.

Sources: Bloomberg, Apollo Chief Economist Source: Apollo Chief Economist See important disclaimers at the bottom of the page.

-

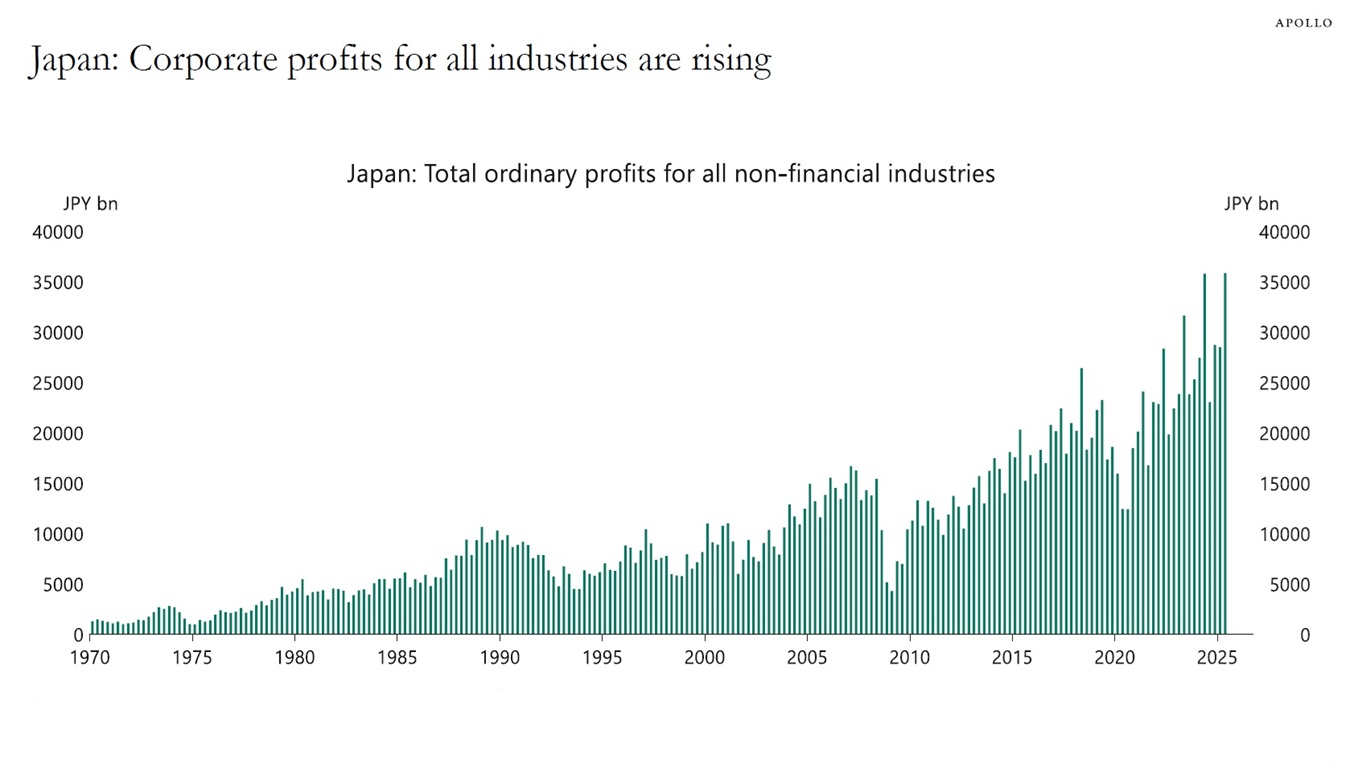

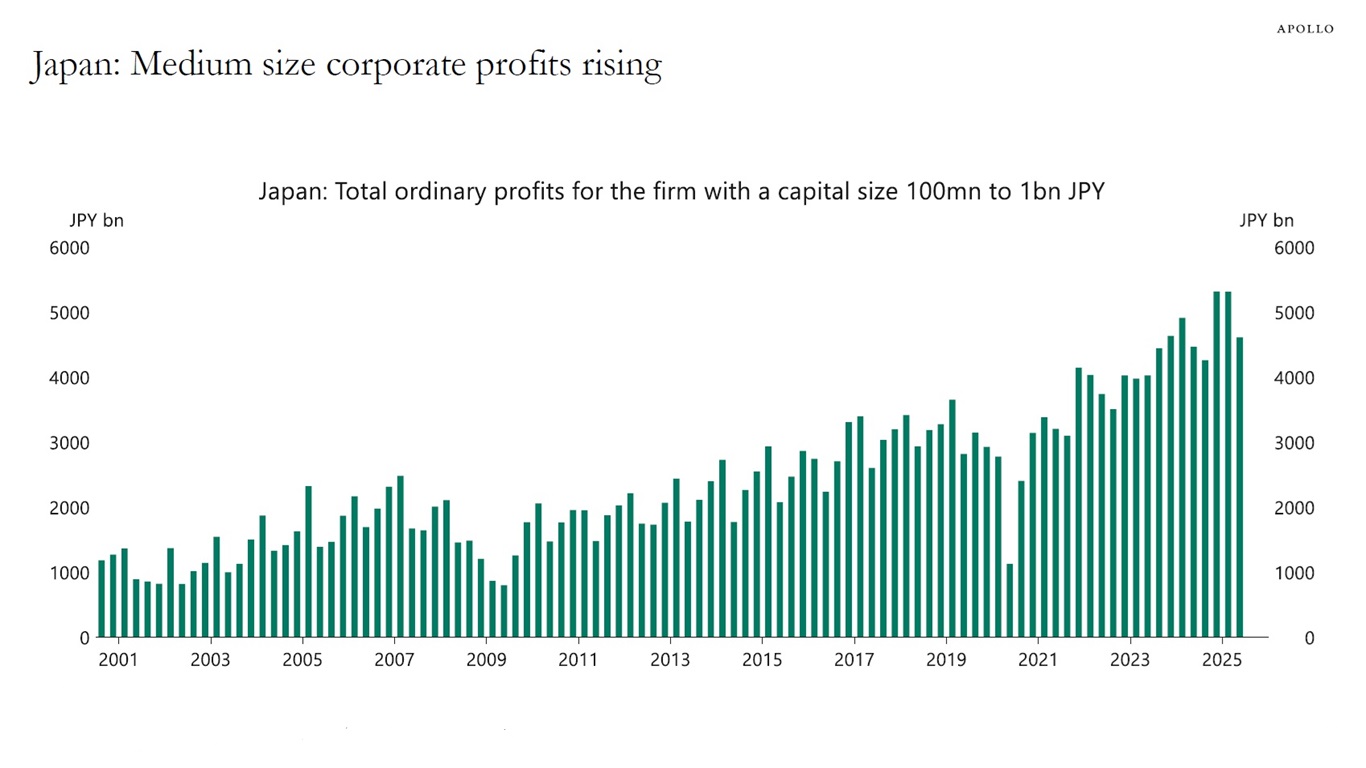

We are bullish on Japan. Corporate profits are trending higher, growth is expected to accelerate over the next 12 months and inflation is expected to decline from its current elevated levels. For more, see charts below and our latest outlook for Japan here.

We are hosting our Apollo Global Industrial Renaissance Conference in Tokyo on October 20, where Apollo’s senior management and investment professionals will discuss opportunities to invest in key sectors like digital infrastructure, the energy transition and manufacturing, see also here.

Sources: Ministry of Finance Japan, Bloomberg, Macrobond, Apollo Chief Economist Sources: Ministry of Finance Japan, Bloomberg, Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

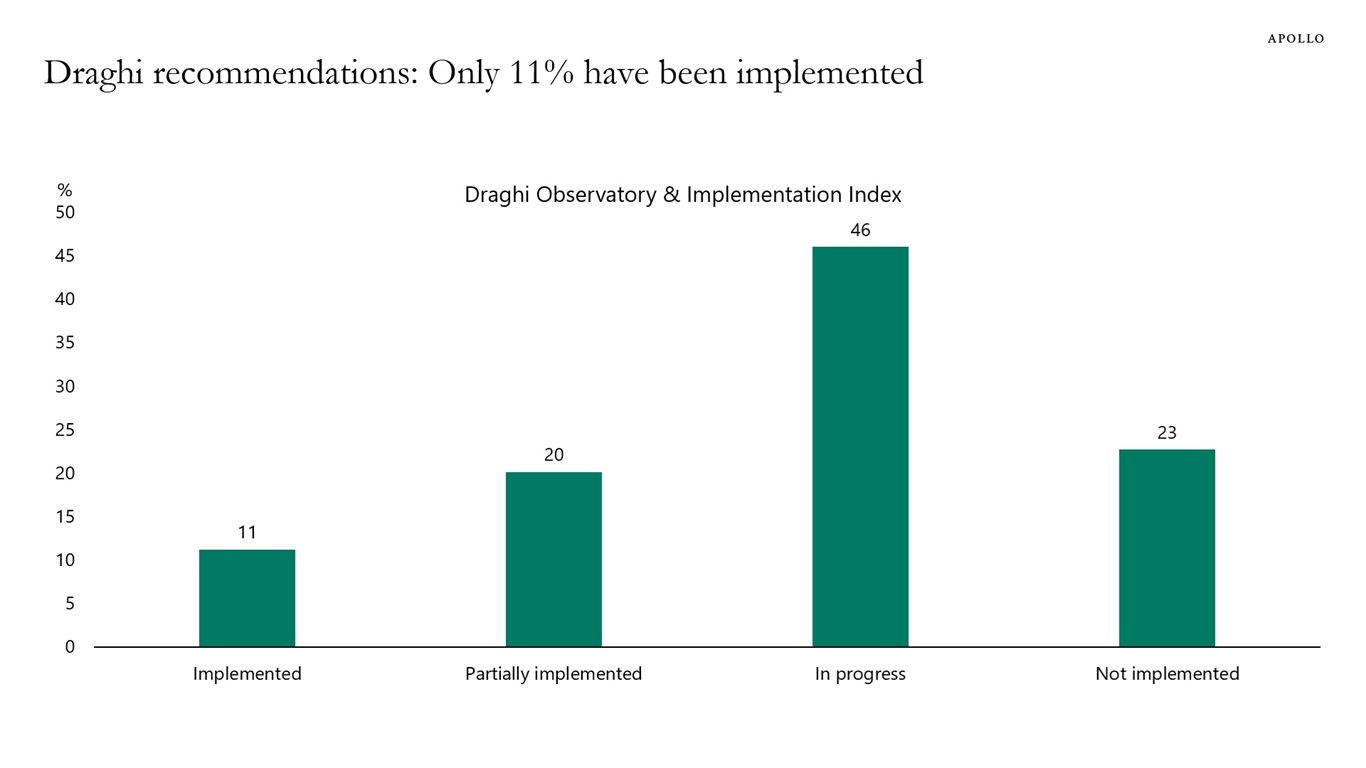

A year ago, former ECB president and Italian prime minister Mario Draghi laid out 383 policy recommendations to make the European economy more competitive, and so far, only 11% of his proposals have been implemented, see chart below.

Growth is weak in Europe, and European politicians need to move much faster if they want to make the European economy more competitive.

Sources: European Policy Innovation Council (EPIC), Apollo Chief Economist See important disclaimers at the bottom of the page.

-

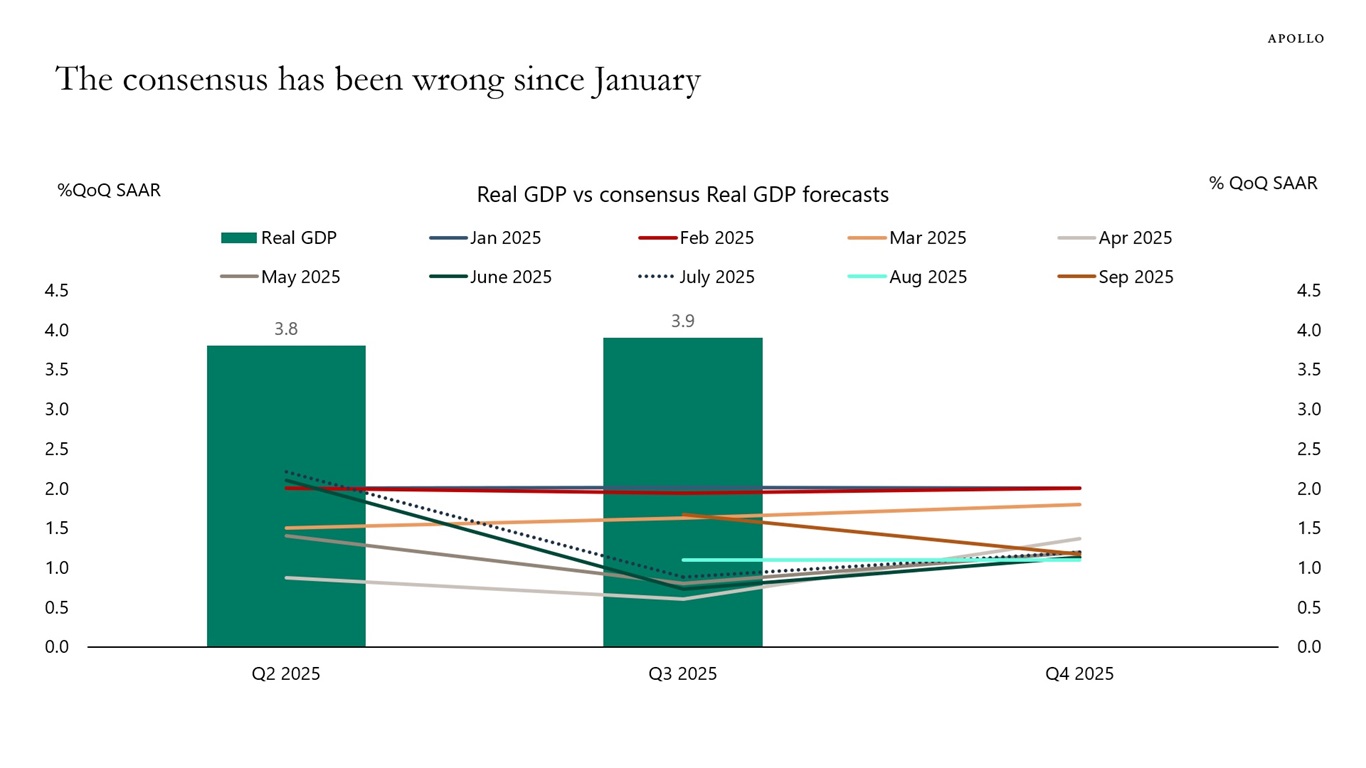

The consensus has been wrong since January. The forecast for the past nine months has been that the US economy would slow down. But the reality is that it has simply not happened, see chart below. GDP growth in the second quarter was 3.8%, and the Atlanta Fed predicts that GDP in the third quarter will be 3.9%. Yes, job growth is slowing, but this is the result of slowing immigration.

The bottom line is that the US economy remains remarkably resilient, and it is becoming increasingly difficult to argue that we are still waiting for the delayed negative effects of what happened six months ago on Liberation Day in April.

For investors, this means that the upside risks to inflation are growing, particularly if the Fed continues to cut rates.

Note: Q3 2025 GDP = Atlanta Fed GDPNow estimate. Sources: BEA, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

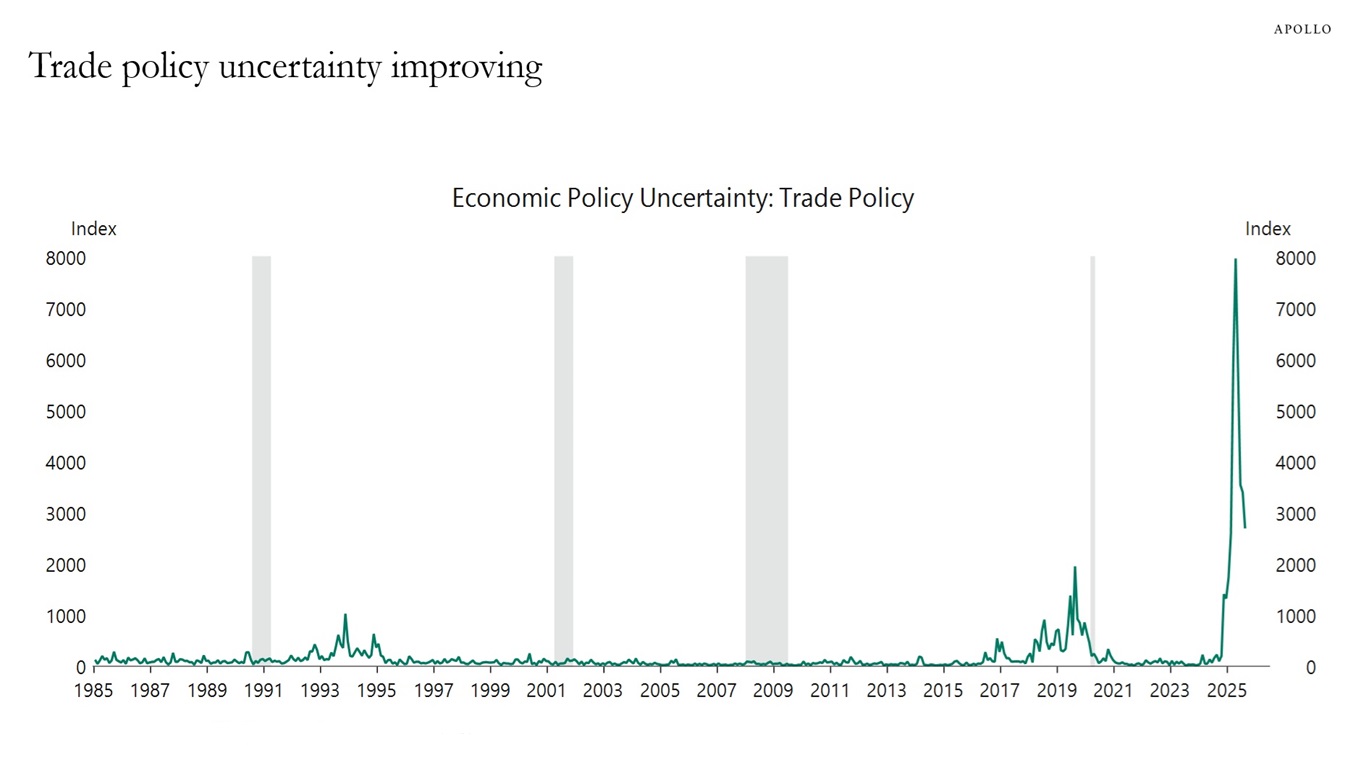

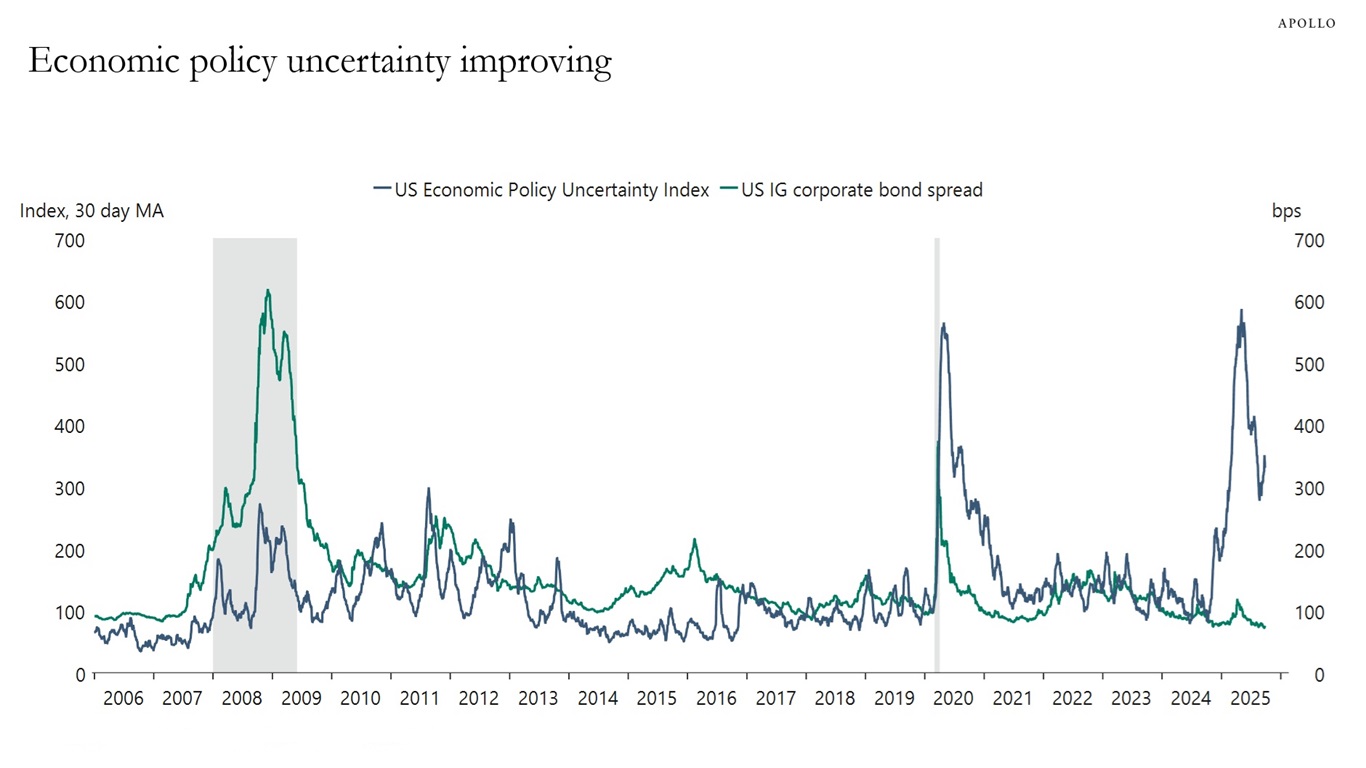

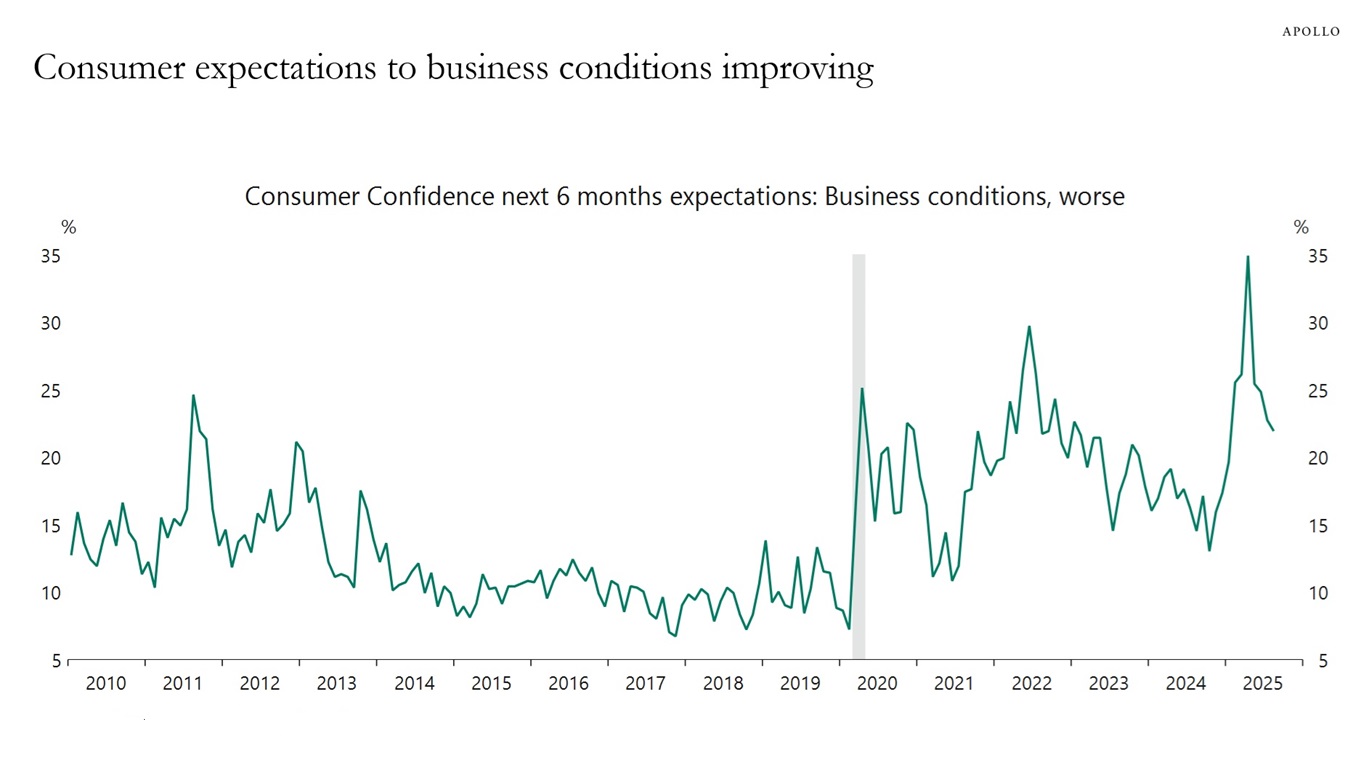

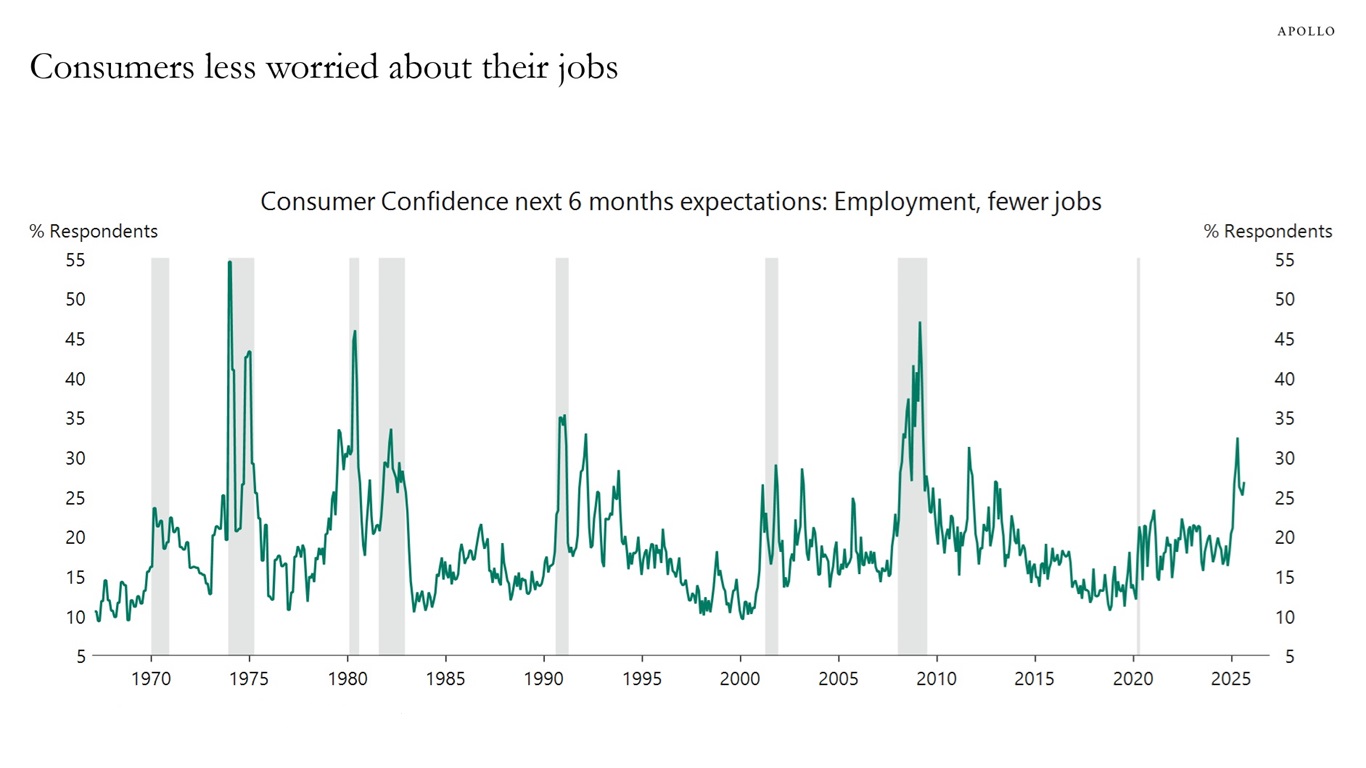

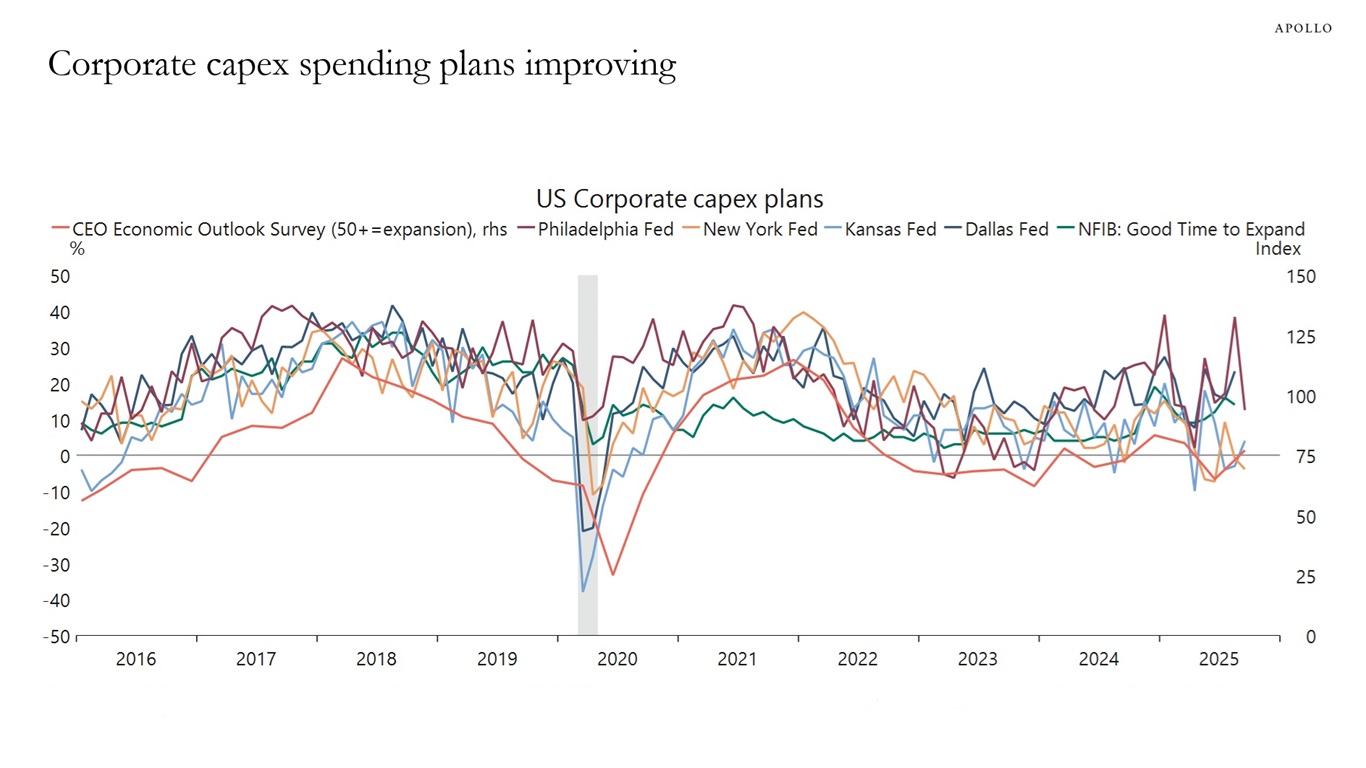

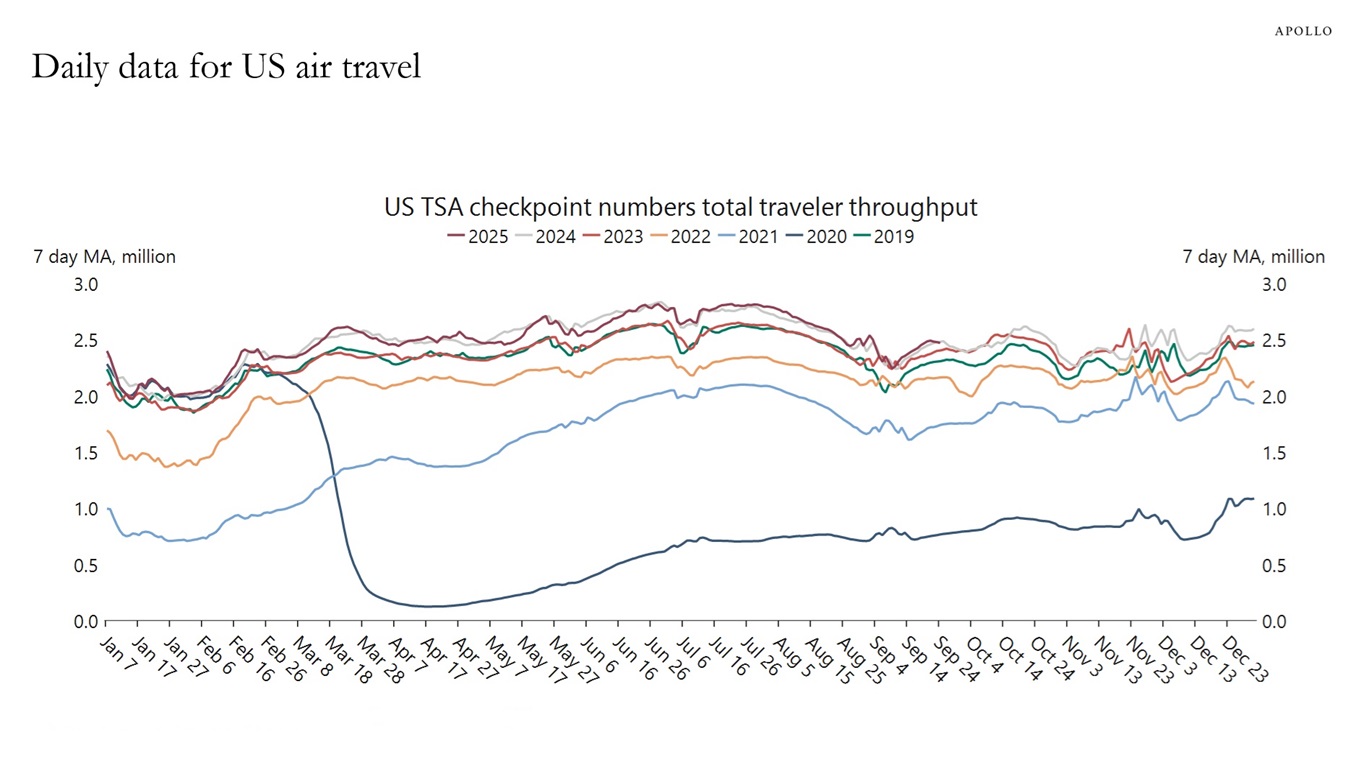

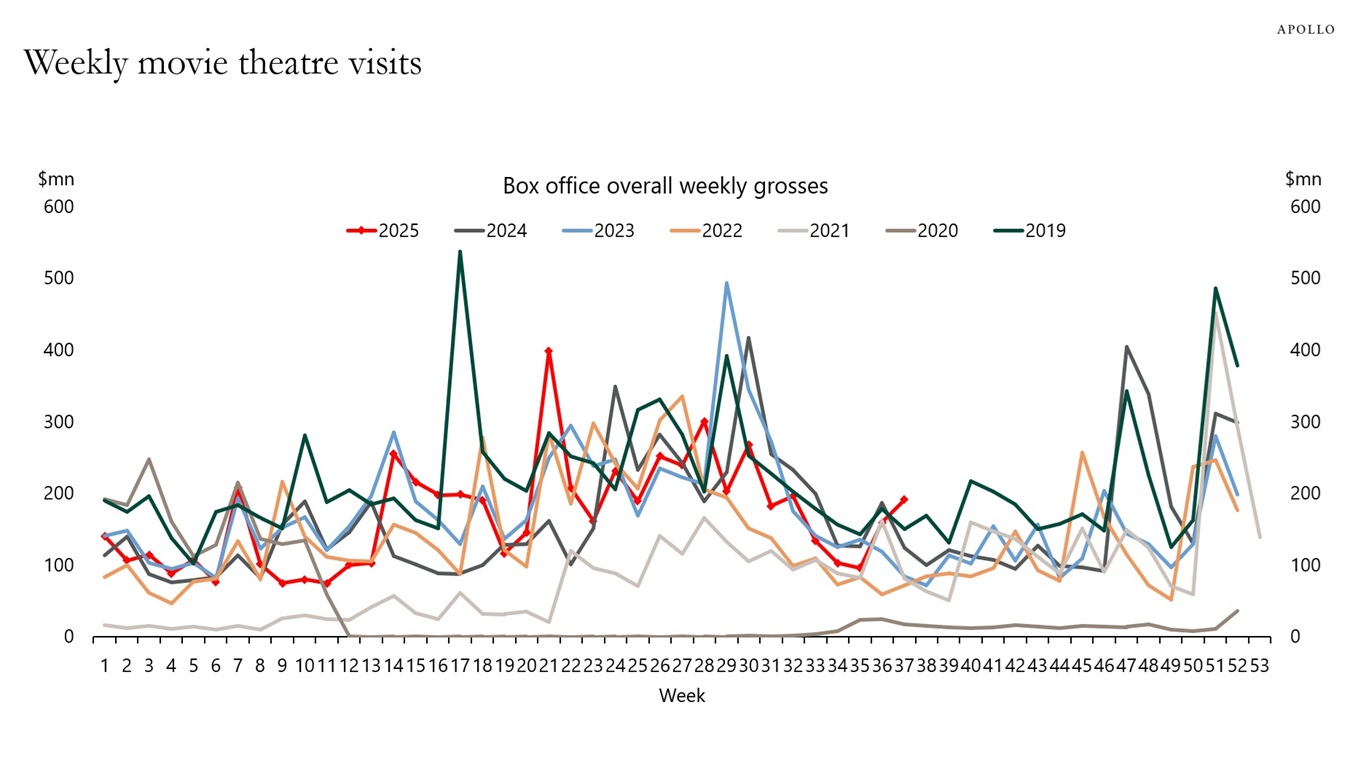

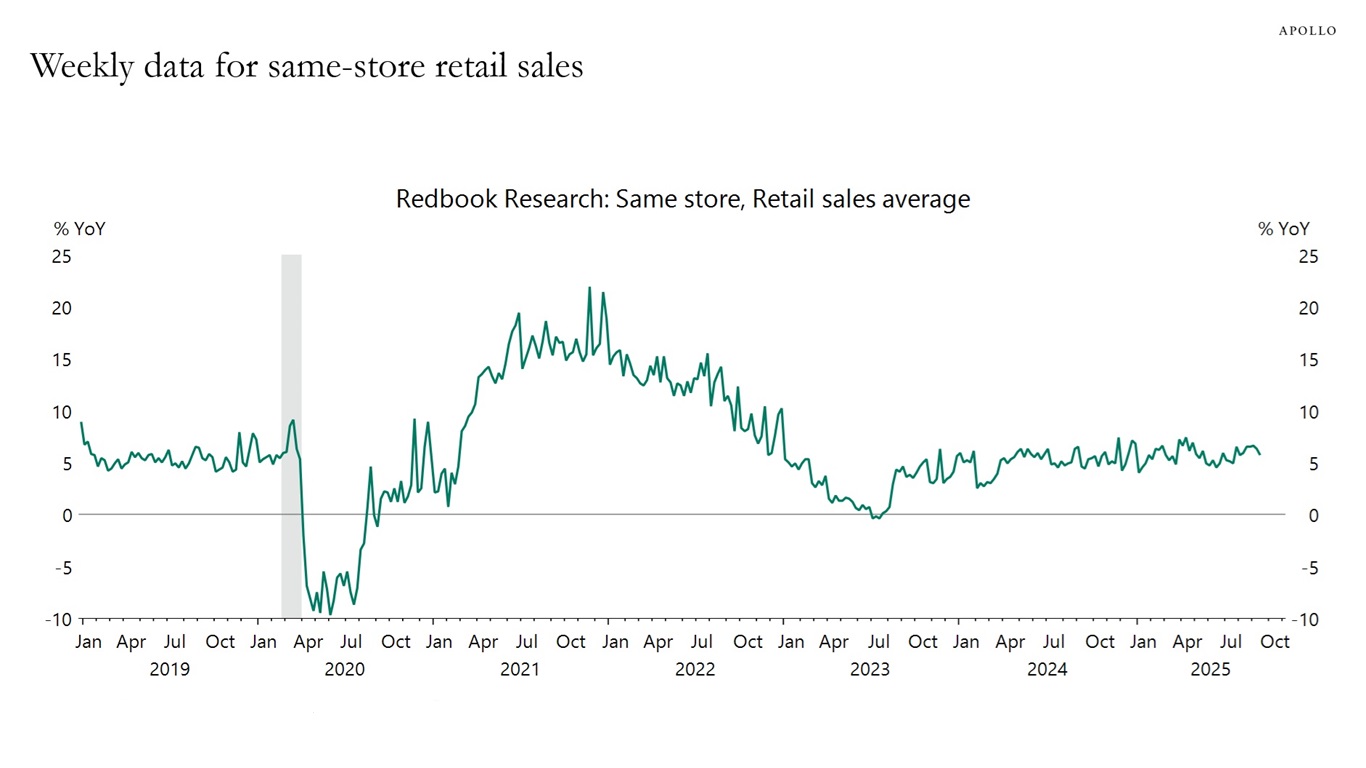

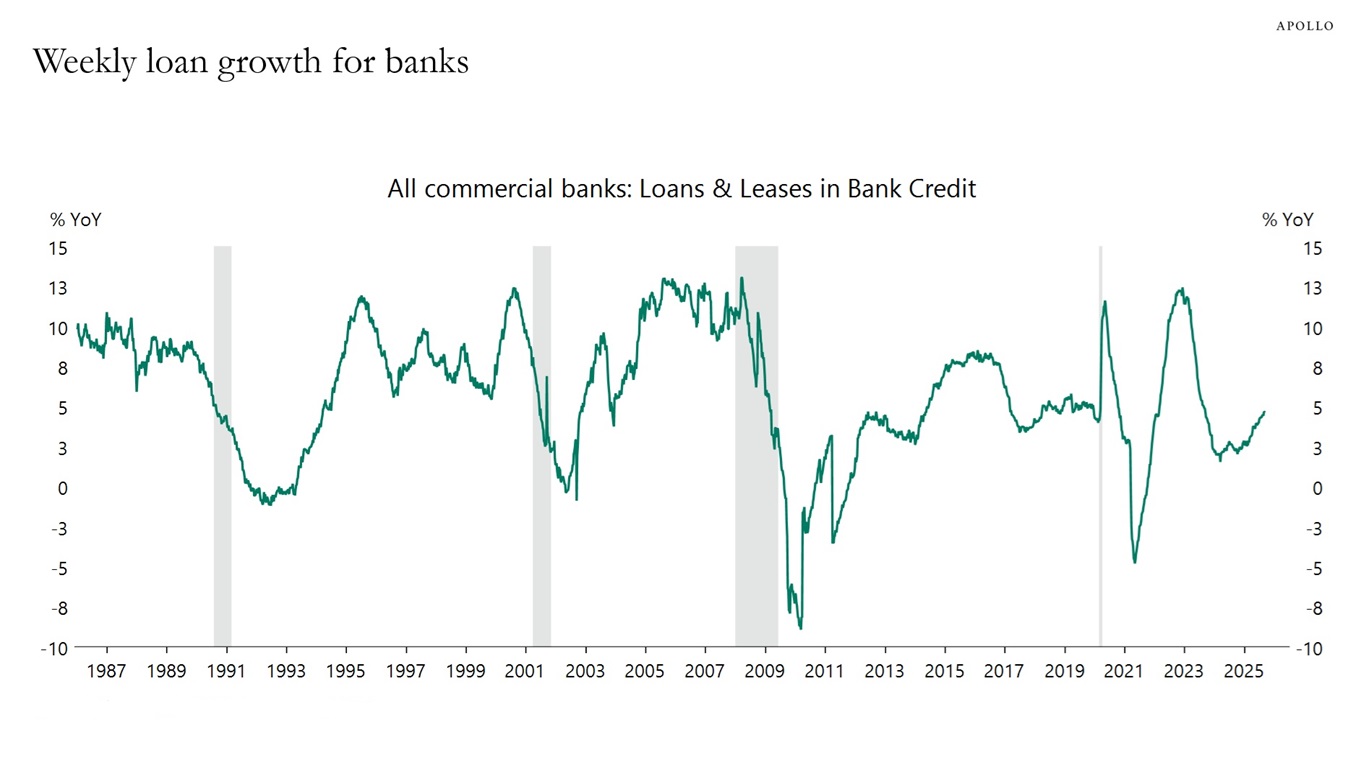

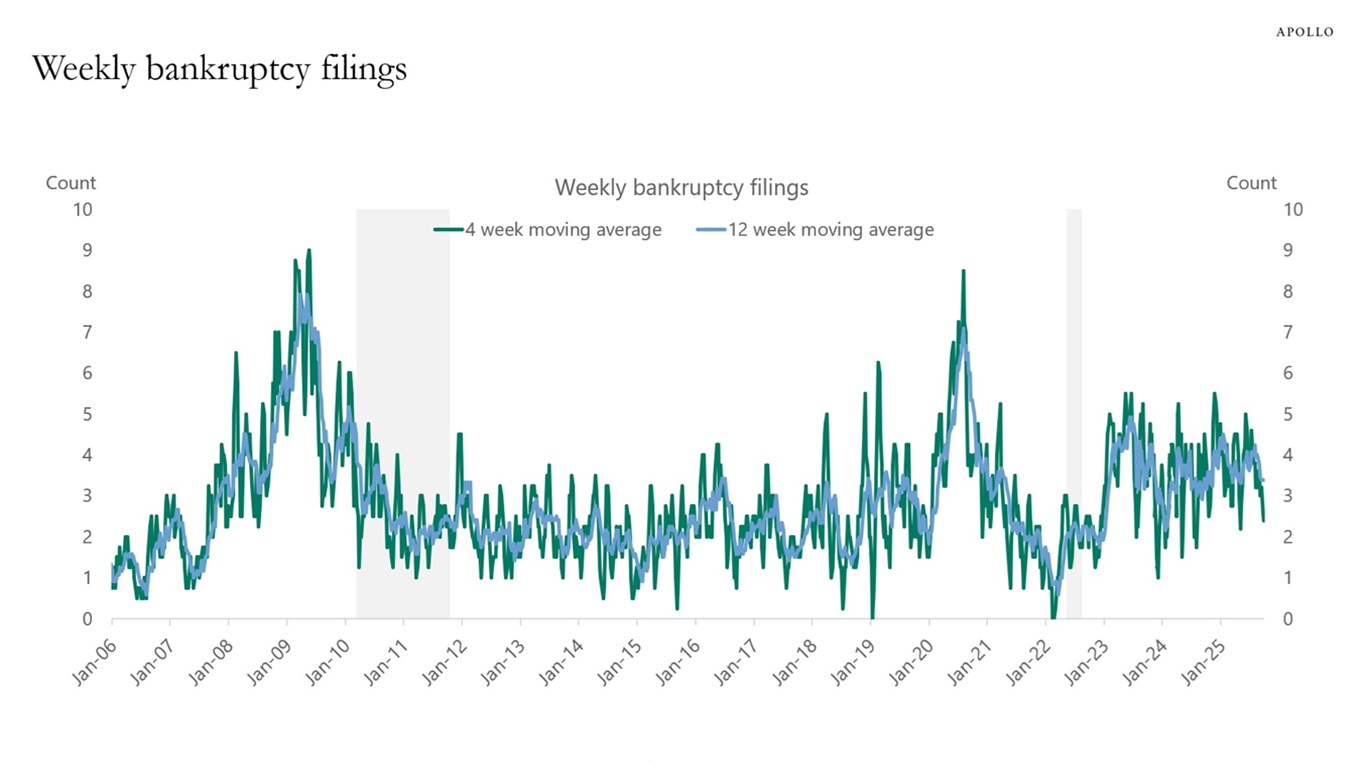

The consensus expects nonfarm payrolls for September to come in at 50,000, and I think that is too pessimistic. The charts below with incoming daily and weekly data for September show that:

1) Trade policy uncertainty is improving

2) Economic policy uncertainty is improving

3) Consumer expectations to business conditions are improving

4) Consumers are less worried about losing their jobs

5) Corporate capex plans are improving, and jobless claims are still low

6) The daily TSA data for the number of people traveling on airplanes is strong

7) Data for the number of people going to Broadway shows, the movies and visiting the Statue of Liberty is strong

8) Weekly data for same-store retail sales is strong

9) Weekly data for bank lending is accelerating

10) Weekly bankruptcy filings are starting to trend lower

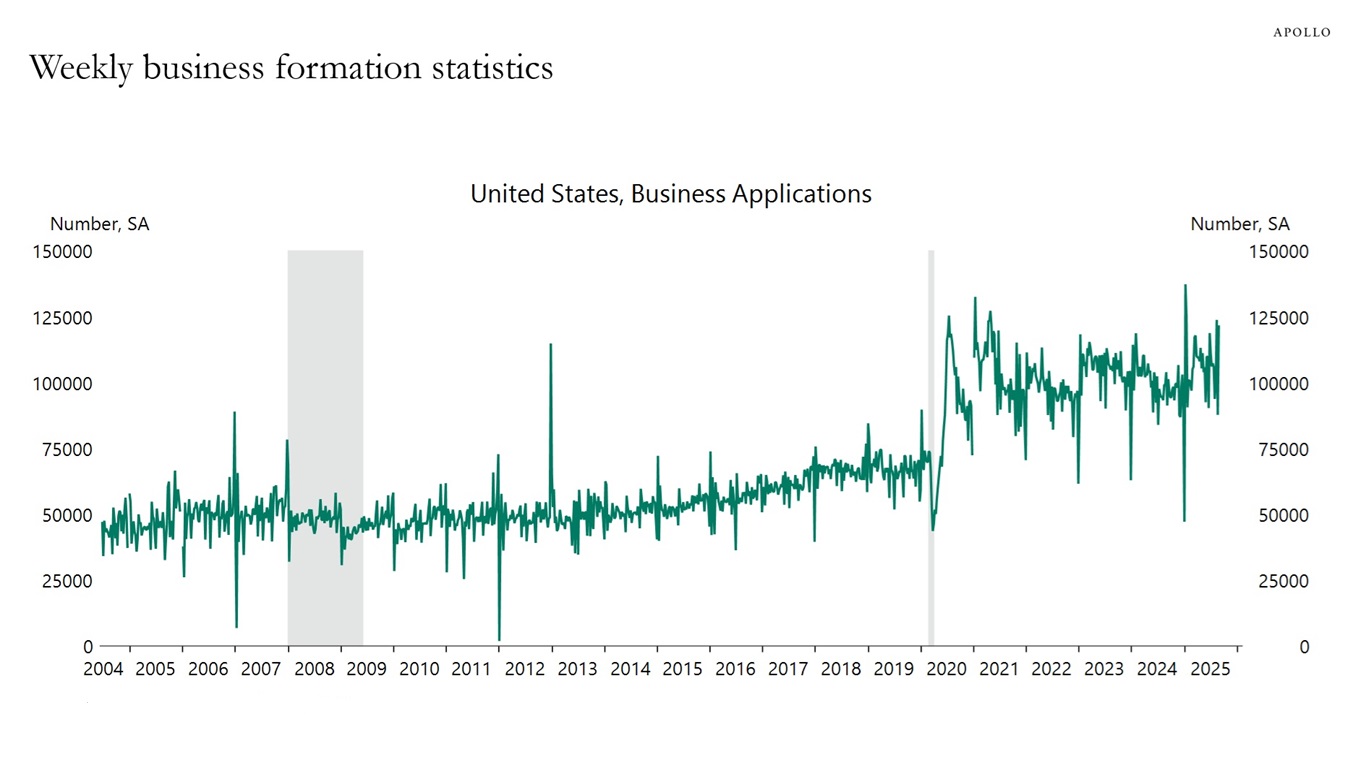

11) Weekly data for business formation is still strong

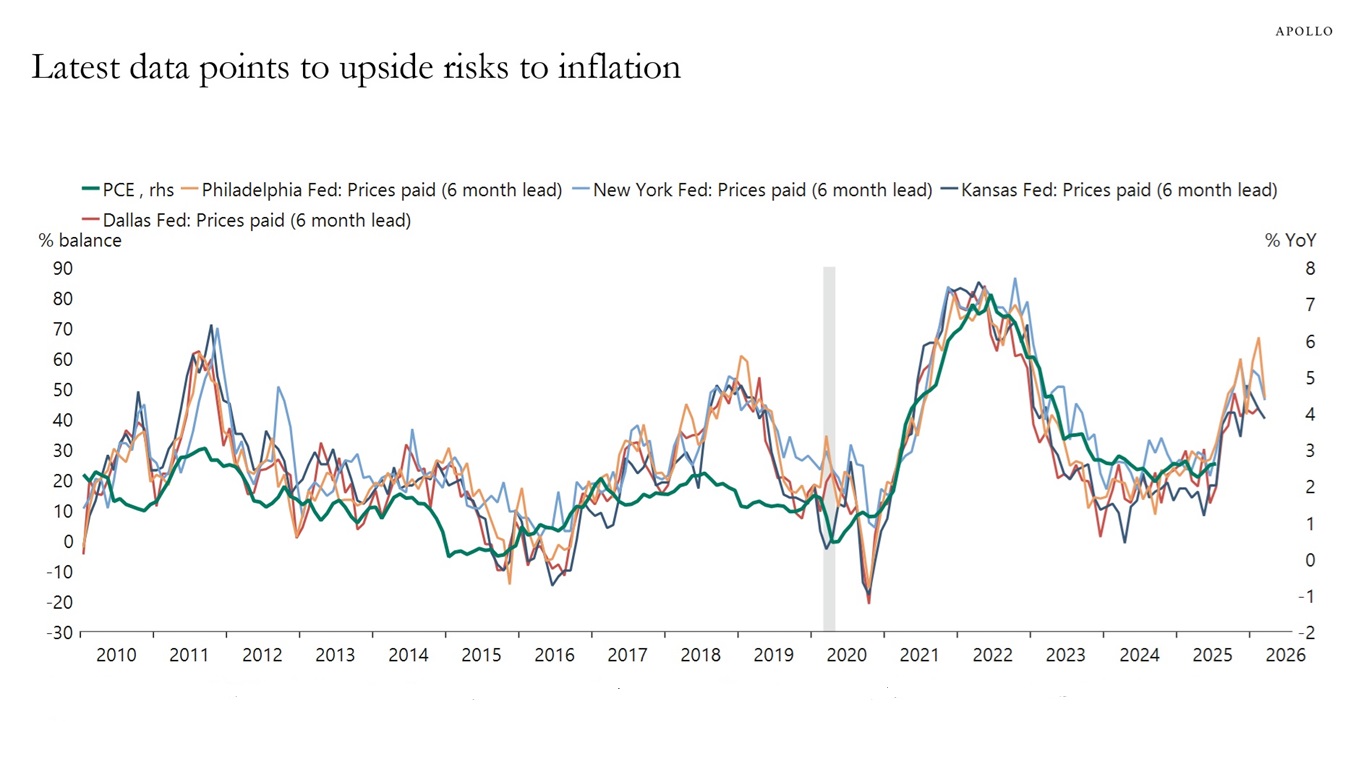

12) There are significant upside risks to inflation in the regional Fed surveys and in ISM services price paid

Combined with the Atlanta Fed expecting GDP growth in the third quarter at 3.9%, the bottom line is that the economy continues to do better than the consensus expects, and the labor market has likely weakened because of lower immigration and perhaps also AI implementation.

With continued strong growth and upside pressures on inflation from tariffs, immigration restrictions, and the declining dollar, the FOMC should really be talking about rate hikes rather than rate cuts.

Our chart book with high-frequency indicators for the US economy is available here.

Sources: Economic Policy Uncertainty, Macrobond, Apollo Chief Economist Sources: Economic Policy Uncertainty, Macrobond, Apollo Chief Economist Sources: Conference Board, Macrobond, Apollo Chief Economist Sources: Conference Board, Macrobond, Apollo Chief Economist Sources: National Federation of Independent Business, Federal Reserve Bank of Dallas, Federal Reserve Bank of Kansas City, Federal Reserve Bank of New York, Federal Reserve Bank of Philadelphia, Business Roundtable, Macrobond, Apollo Chief Economist Sources: US Dept of Homeland Security, Macrobond, Apollo Chief Economist Sources: Boxofficemojo.com, Apollo Chief Economist Sources: Redbook Research Inc., Macrobond, Apollo Chief Economist Sources: Federal Reserve, Macrobond, Apollo Chief Economist Note: Filings are for companies with more than $50 million in liabilities. For week ending on September 26, 2025. Sources: Bloomberg, Apollo Chief Economist Sources: US Census Bureau, Macrobond, Apollo Chief Economist Sources: Federal Reserve Bank of Dallas, Federal Reserve Bank of Kansas City, Federal Reserve Bank of New York, Federal Reserve Bank of Philadelphia, US Bureau of Economic Analysis (BEA), Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

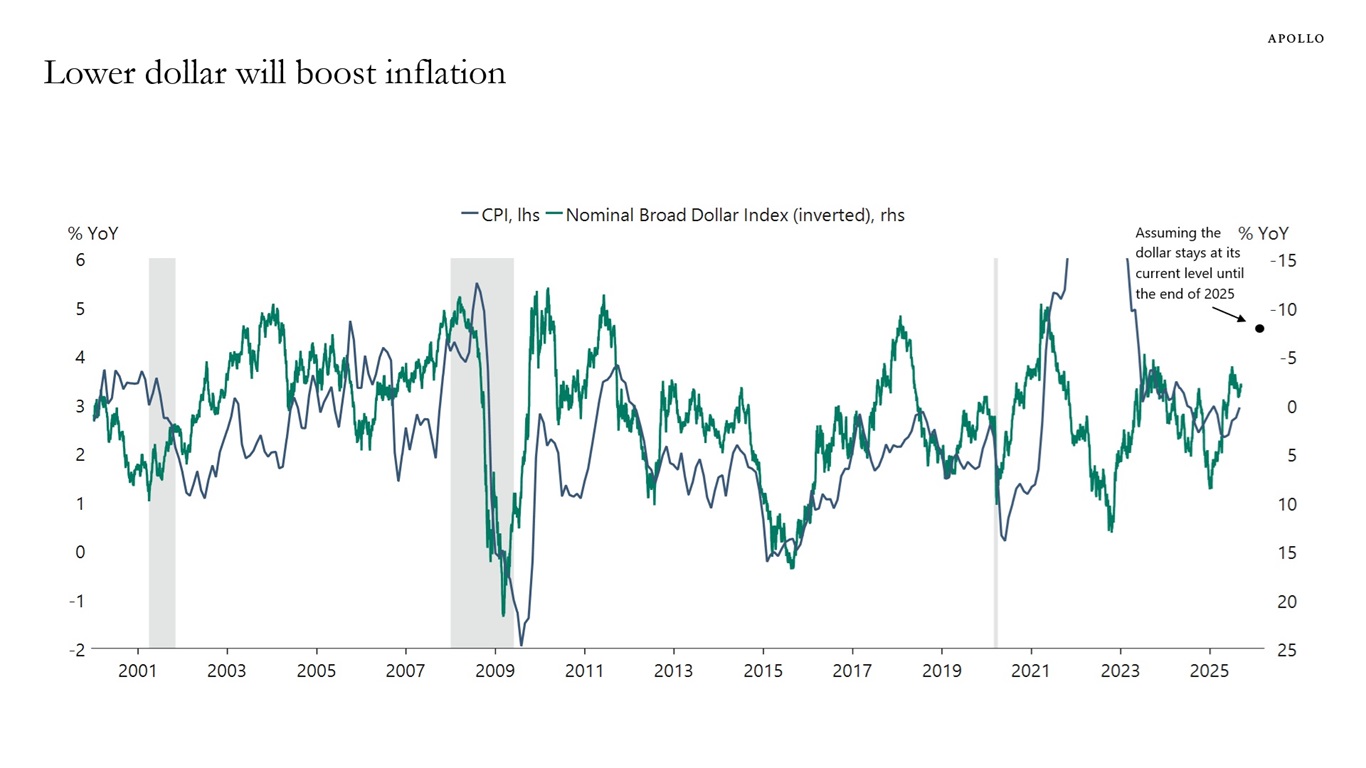

The US dollar has depreciated almost 10% since the beginning of the year, and the Fed’s model for the US economy finds that a 10% depreciation results in a 0.3% boost to inflation. Put differently, there is not only upward pressure on inflation from tariffs and immigration restrictions but also from the ongoing dollar depreciation, see chart below.

Sources: Federal Reserve, US Bureau of Labor Statistics (BLS), Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

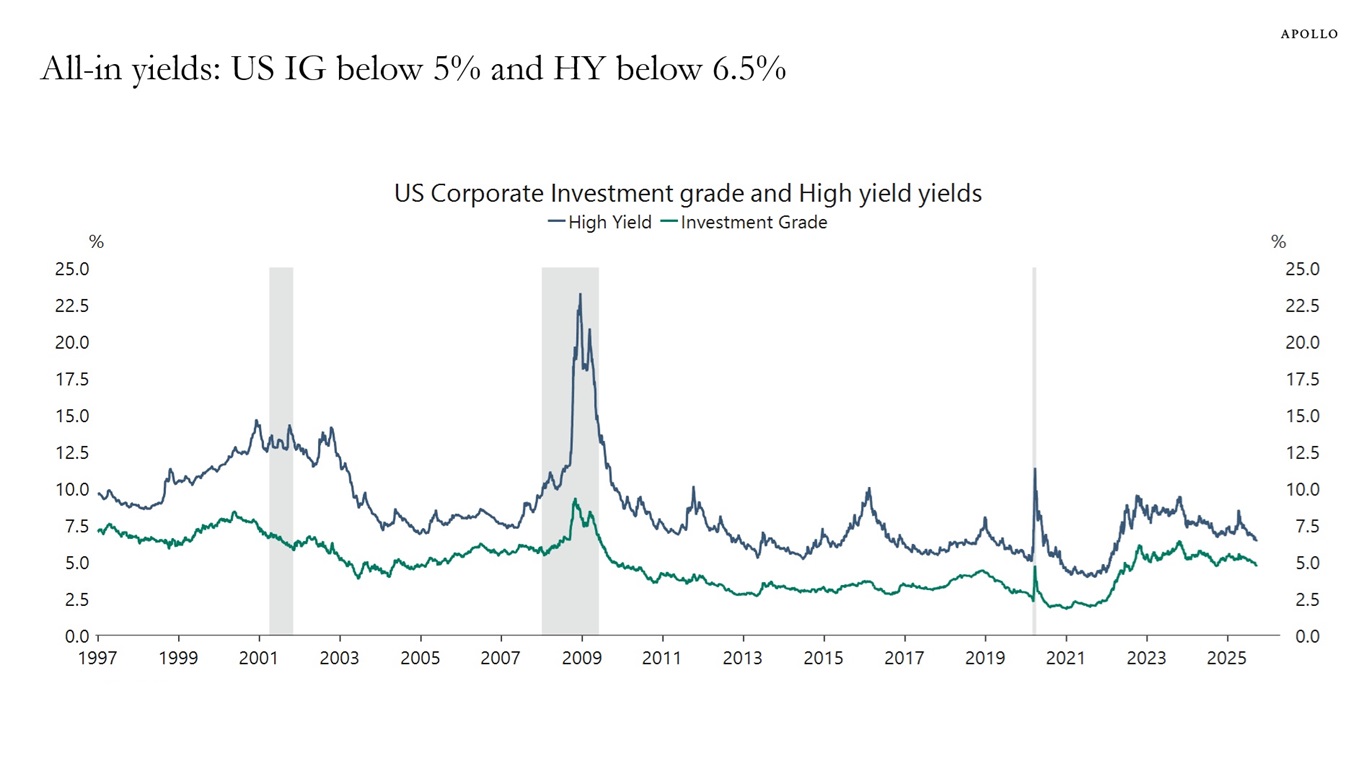

The all-in yield for public IG is now below 5%, and the all-in yield for public HY is below 6.5%, see chart below.

Sources: ICE BofAML, Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.