The Daily Spark is moving to Apollo.com— read the latest from Torsten Slok here.

Want it delivered daily to your inbox?

-

It normally takes 18 months on average for the US to negotiate a trade deal, see chart below.

Why does it take so long? Because trade negotiations involve going through what is imported into each country line by line and then negotiating the tariff for each product category (t-shirts, pencils, cars, pharmaceuticals, lawnmowers, services, etc.). The negotiations also involve discussions about non-tariff barriers, tax differences, rules of origin discussions, IP rights, labor standards, environmental standards, anti-dumping, dispute resolution, digital trade and e-commerce, government procurement, and sometimes security and defense considerations.

The bottom line is that trade negotiations take time because they are complex.

While markets wait for trade negotiations with 90 countries at the same time, global trade is grinding to a standstill with problems similar to what we saw during Covid: growing supply chain challenges with potential shortages in US stores within a few weeks, higher US inflation, and lower tourism to the US. We reiterate our view that if current policies do not change, then the probability of a US recession in 2025 is 90%, see also our discussion in the Daily Spark yesterday.

Sources: PIIE (Freund and McDaniel), Apollo Chief Economist See important disclaimers at the bottom of the page.

-

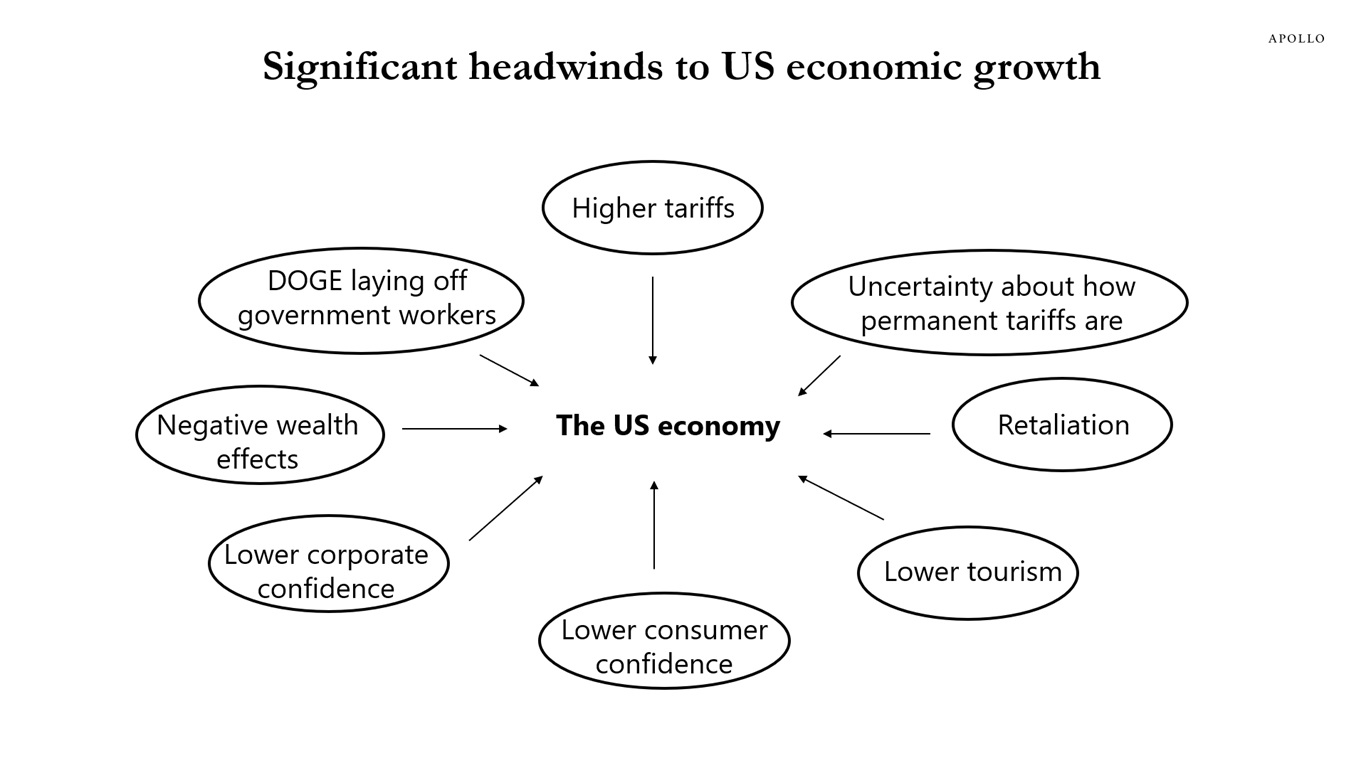

The US economy has been the envy of the world for decades—the biggest economy in the world with strong economic performance and open access for the rest of the world to consumers, investments, and capital markets.

The US is also the freest trading market in the world (2nd freest considering just financial friction/1st considering financial and non-financial barriers), and the administration is not wrong to want to adjust the terms of trade to position the US fairly and to insist on a level playing field for US consumers.

However, tariffs have been implemented in a way that has not been effective, and there is now a 90% chance of what can be called a Voluntary Trade Reset Recession (“VTRR”), see the first chart below.

The administration inherited an economy with strong growth, 4% unemployment, positive hiring, and a substantial tailwind from investments. US and international investors are building infrastructure, next-generation factories, and data centers. The Inflation Reduction Act increased capex, and the US was poised for a substantial increase due to energy supply additions, increased defense production, and deregulation.

But implementing extremely high tariffs overnight hurts many businesses; particularly small businesses because the tariff must be paid by the business when the imported goods arrive in the US. Small businesses that have for decades relied on a stable US system will have to adjust immediately and do not have the working capital to pay tariffs. Expect ships to sit offshore, orders to be canceled, and well-run generational retailers to file for bankruptcy.

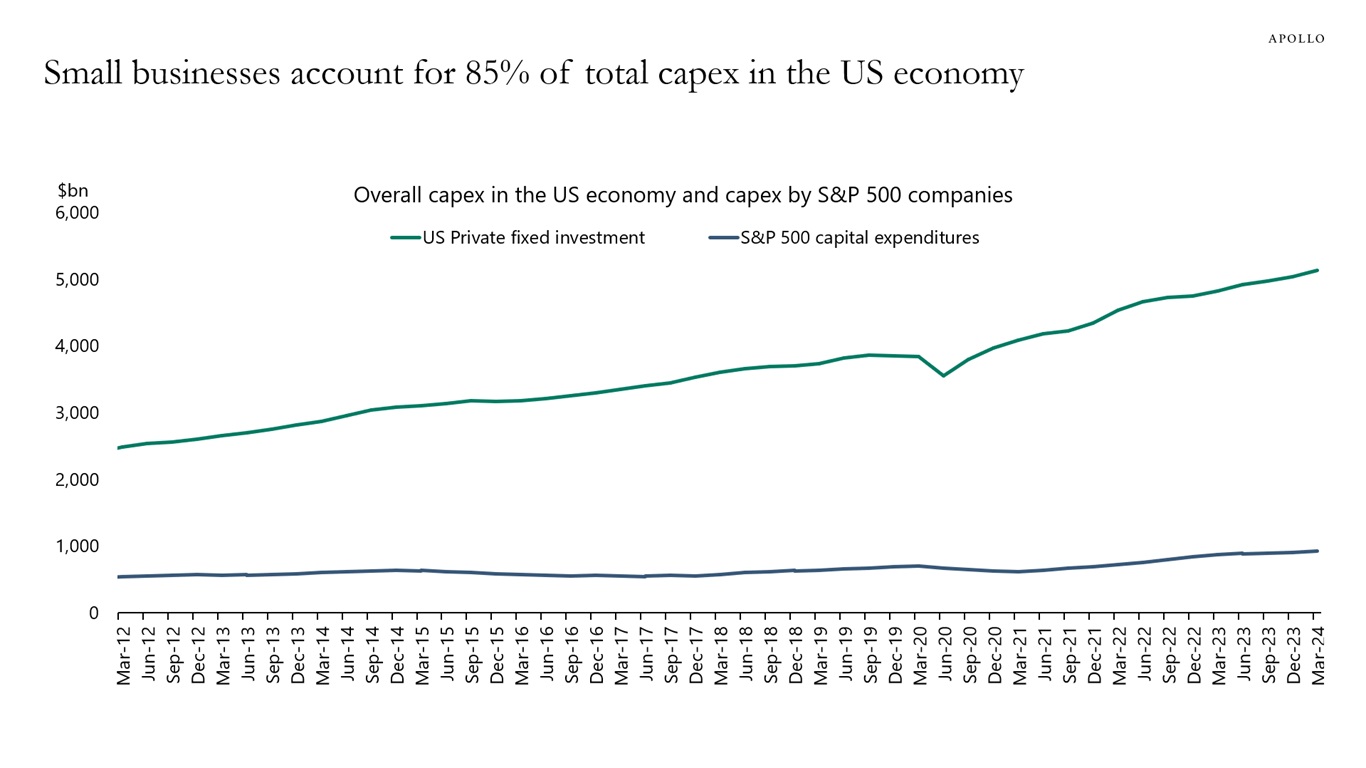

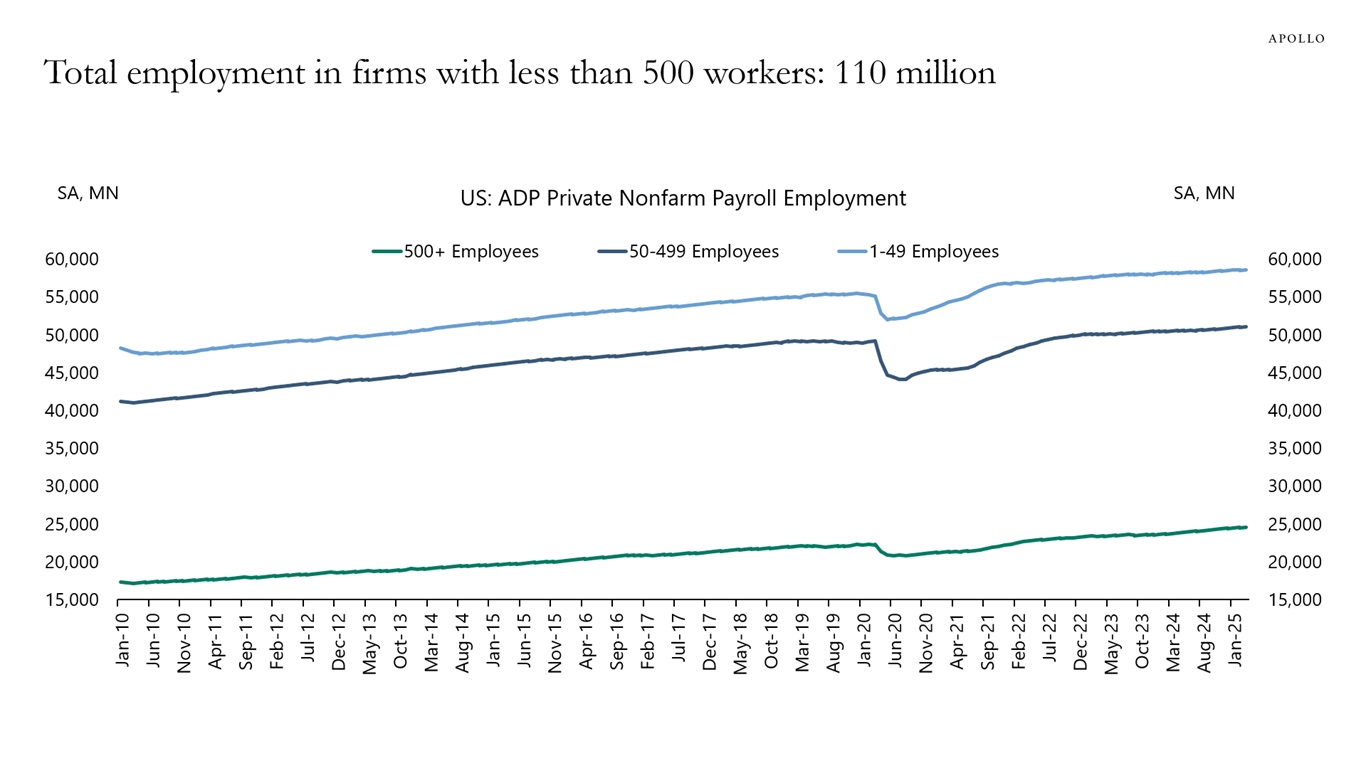

To make exceptions for large businesses that have the flexibility and resources to handle unforeseen expenses but not small businesses does not make sense. The challenges for small- and medium-sized enterprises are now a macro problem for the US economy, where small businesses account for more than 80% of US employment and capex, see the second and third chart below.

One way to quantify the coming negative impact on GDP is to compare the current tariff increase with the tariff increase observed during the trade war in 2018. During the 2018 trade war with China, the US average tariff rate increased from 2% to 3%, and studies show (here and here) that the impact on GDP was between 0.25% and 0.7%. Using the smallest of these estimates for the current tariff increase from 3% to 18% shows that the negative impact on GDP in 2025 could be almost 4 percentage points, not including additional non-linear effects because of the current increase in uncertainty for consumer spending decisions and business planning.

What can be done to avoid a recession? It is not too late to modify the course. For Mexico and Canada, there is a unique opportunity for the US to move first and get an agreement where labor, capital, and natural resources can be efficiently used in the North American economy. For any country that reduces tariffs to zero, the 10% tariff could stay in place, giving 180 days to negotiate non-tariff barriers, at which time, if agreed, the 10% is removed. For China, one approach could be to keep tariffs in place on autos, solar, and other strategic product groups. For all other products from China, tariffs can be gradually phased in over a period of, say, 18 or 24 months.

The bottom line: If the current level of tariffs continues, a sharp slowdown in the US economy is coming.

Source: Apollo Chief Economist

Sources: S&P, BEA, Haver Analytics, Apollo Chief Economist

Sources: ADP, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

The share of Chinese exports going to the US has declined from 20% to 14% since 2017, see chart below.

With China’s market share in the US declining, the economies that have gained market share in the US include Vietnam, Taiwan, Mexico, India, and South Korea, and studies show (see here and here) that about two percentage points of the rise in the market share of other regions is because of an increase in China’s share of their goods imports.

In other words, some exports from China to the US may be rerouted elsewhere or used as input in production in other areas.

The bottom line is that more than 80% of exports from China end up in other places than the US.

It should also be noted that de minimis exports from China to the US (direct shipments to US consumers with a value less than $800) are around $20 billion, much less than the $500 billion in total goods exports from China to the US seen in the chart below.

Sources: General Administration of Customs, China; Haver Analytics; Apollo Chief Economist See important disclaimers at the bottom of the page.

-

The term premium in US Treasuries is rising, see first chart below. The market does not know if this is because of the fiscal situation, inflation expectations becoming unanchored, or discussions about who the next Fed Chair will be.

Some of the move higher in rates has been technical, driven by unwinds of levered basis trades and swap trades.

In addition, the move lower in the dollar is telling us that the move higher in rates is also because of foreigners selling Treasuries.

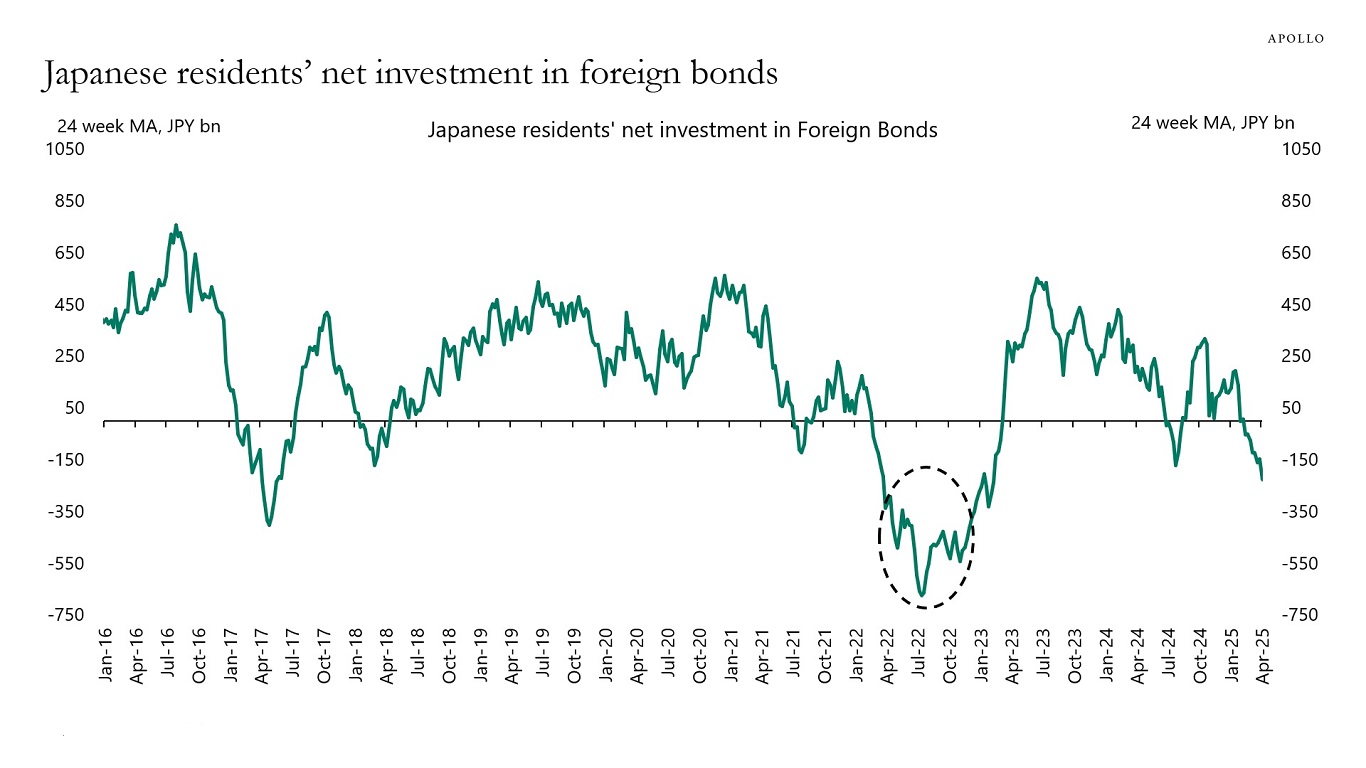

For example, Japanese investors have in recent weeks been significant sellers of foreign bonds, and this has been associated with a significant appreciation of the yen relative to the dollar. This does not necessarily mean that Japanese investors are questioning American exceptionalism. In fact, in 2022, when the Fed started raising interest rates, Japanese investors were also significant sellers of foreign bonds, see second chart below.

We are hosting a conference call today at 9 am EDT to discuss what is going on in markets and the outlook for the economy, you can register here.

Note: The NY Fed measure for the term premium is based on a five-factor, no-arbitrage term structure model. Sources: New York Fed, Bloomberg, Apollo Chief Economist

Sources: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

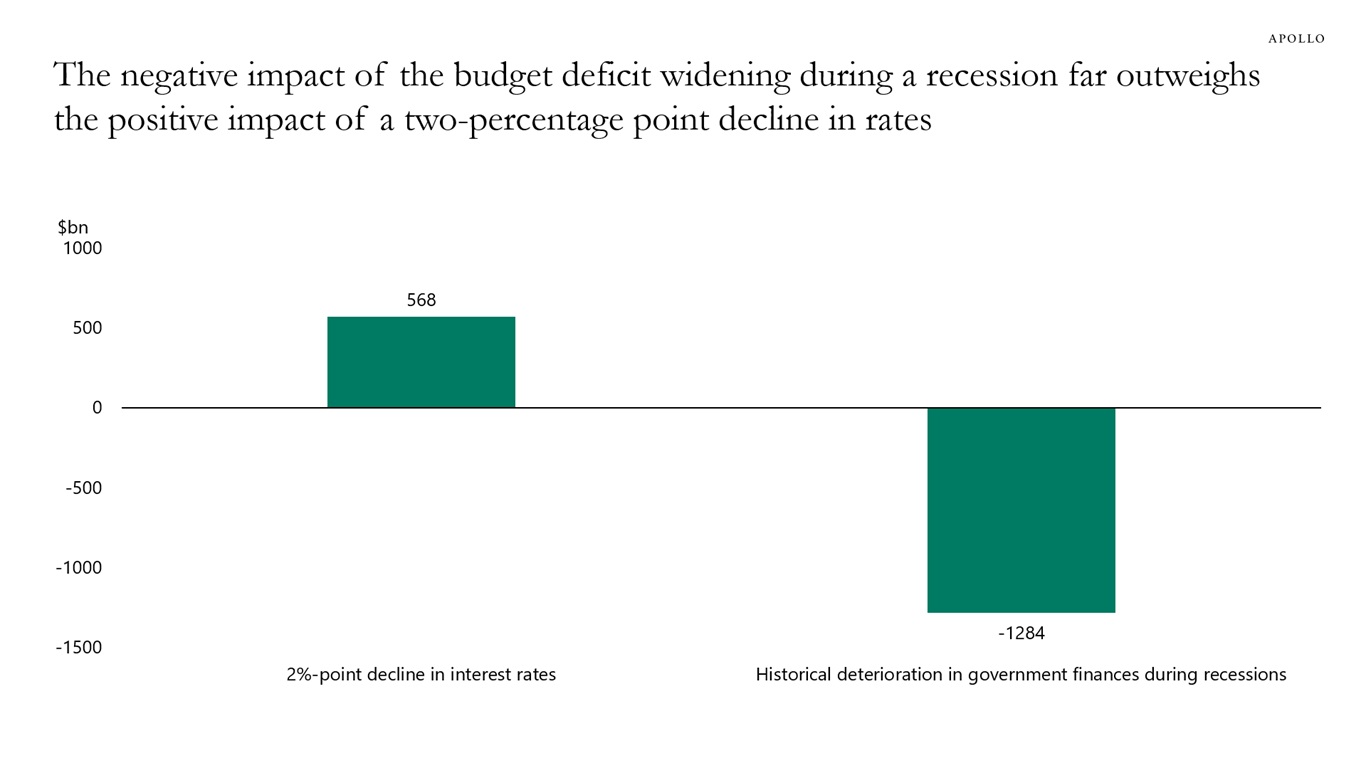

If the US enters a recession, long-term interest rates are likely to go down, and it would be cheaper for the US government to refinance existing government debt.

However, the chart below shows that the interest payments saved if interest rates decline by two percentage points would be more than offset by the deterioration in government finances associated with a recession.

Specifically, if interest rates decline by two percentage points, the US government would save around $500 billion in annual interest payments. But if the US enters a recession, the government will have lower tax collections and pay more in unemployment benefits, and the historical deepening of the budget deficit during recessions of around 4% of GDP would correspond to an additional $1.3 trillion erosion of US government finances measured in 2025 dollars.

The bottom line is that it is not possible to improve the budget deficit by creating a recession because during a recession government finances would deteriorate by double the amount saved in interest payments, see chart below.

Note: Assuming a decline in interest rates by two percentage points relative to current CBO assumption resulting in $568 billion interest expense savings on Federal debt. Fiscal deficit rising by 4.4% GDP on average in the past recessions since 1968. Sources: US Treasury, CBO, Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

My colleague Shobhit Gupta has calculated bid-ask spreads for investment grade (IG) bonds based on trader quotes, see chart below.

Liquid securities are defined as $1 billion-plus deals issued in the past year. Off-the-run bonds are those issued more than two years ago with deal sizes less than $900 million, and these bonds make up 50% of the IG market by count.

The chart shows that bid-ask spreads have spiked post the April 2 tariff announcement.

The gap between liquid and illiquid bonds is particularly noteworthy. In 2020, the bid-ask spread widened across the whole market. But this time around, transaction costs have increased materially more for off-the-run paper. This highlights the growing liquidity divide in the public IG market. Liquidity in on-the-run bonds has improved, but off-the-run paper has become virtually untradeable and effectively a buy-and-hold investment.

Note: Chart shows estimated bid-ask for IG bonds based on trader quotes. Liquid securities defined as $1 billion-plus deals issued in the past year. Off-the-run bonds are those issued more than two years ago with deal size <$900 million. (These bonds make up 50% of the IG market by count.) Sources: Shobhit Gupta, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

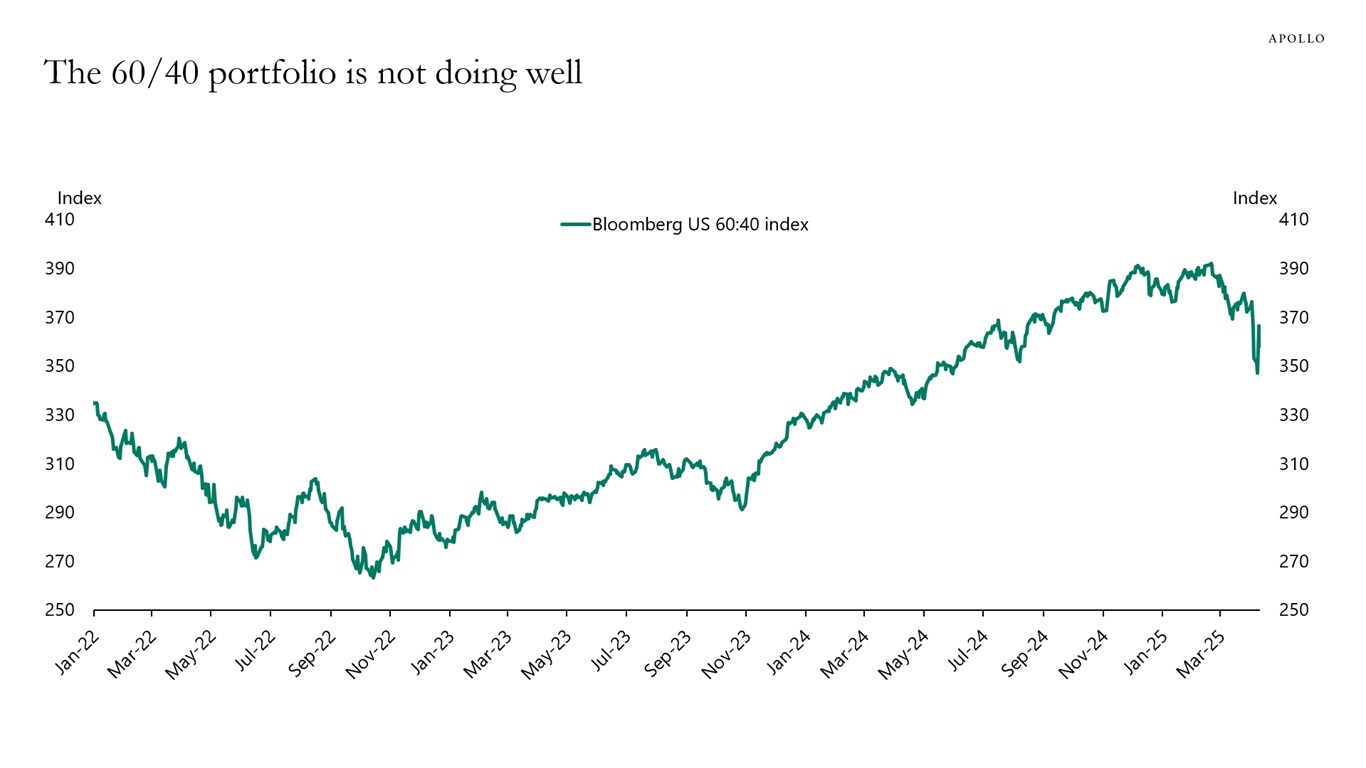

The 60/40 portfolio has basically gone nowhere since the beginning of 2022, with only a 2% annual return for the past three and a half years, see chart below.

Sources: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

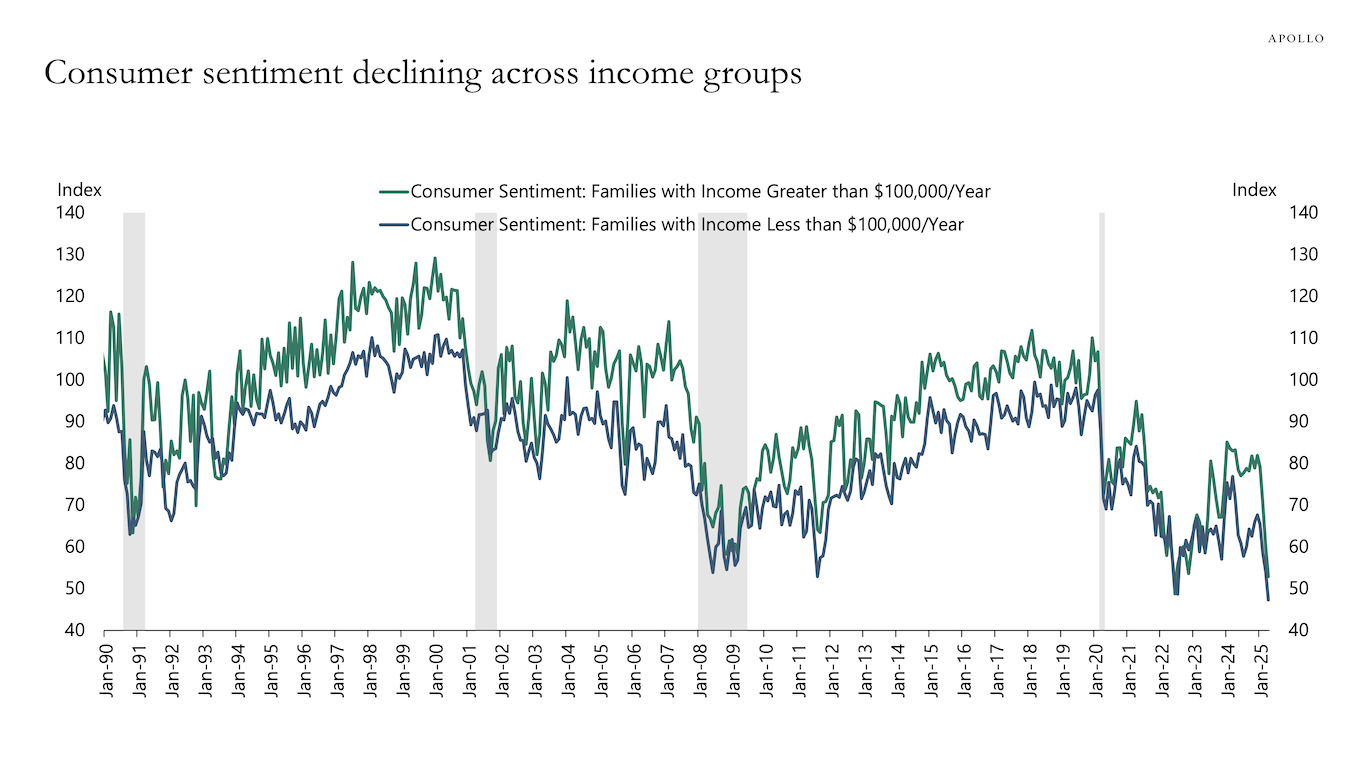

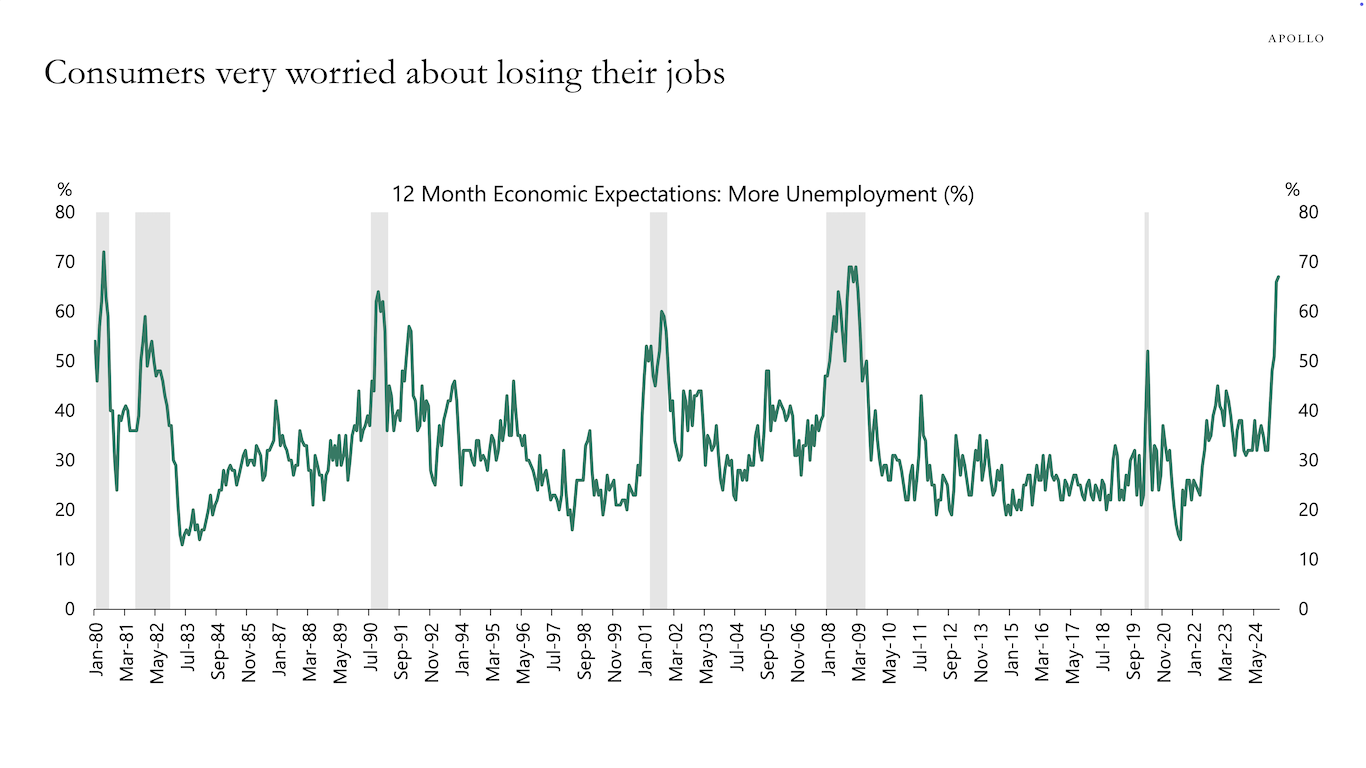

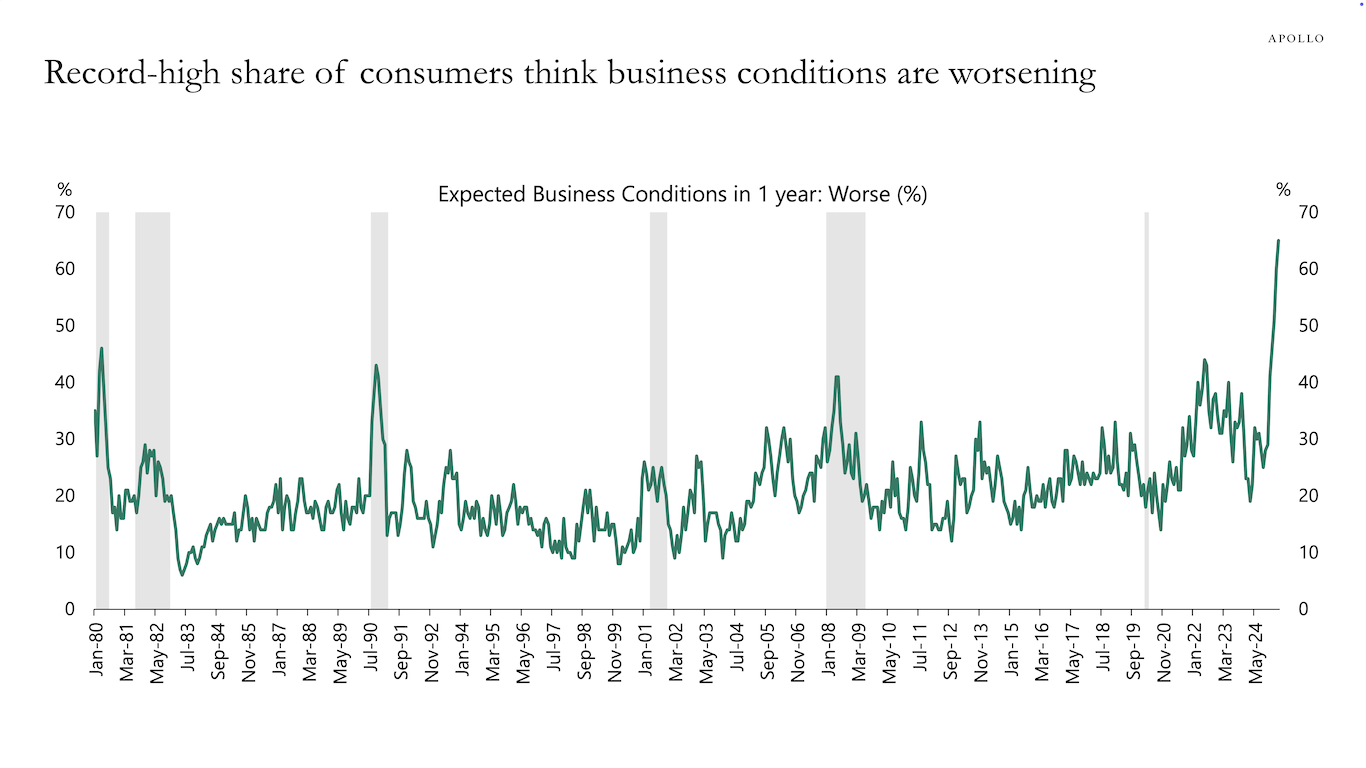

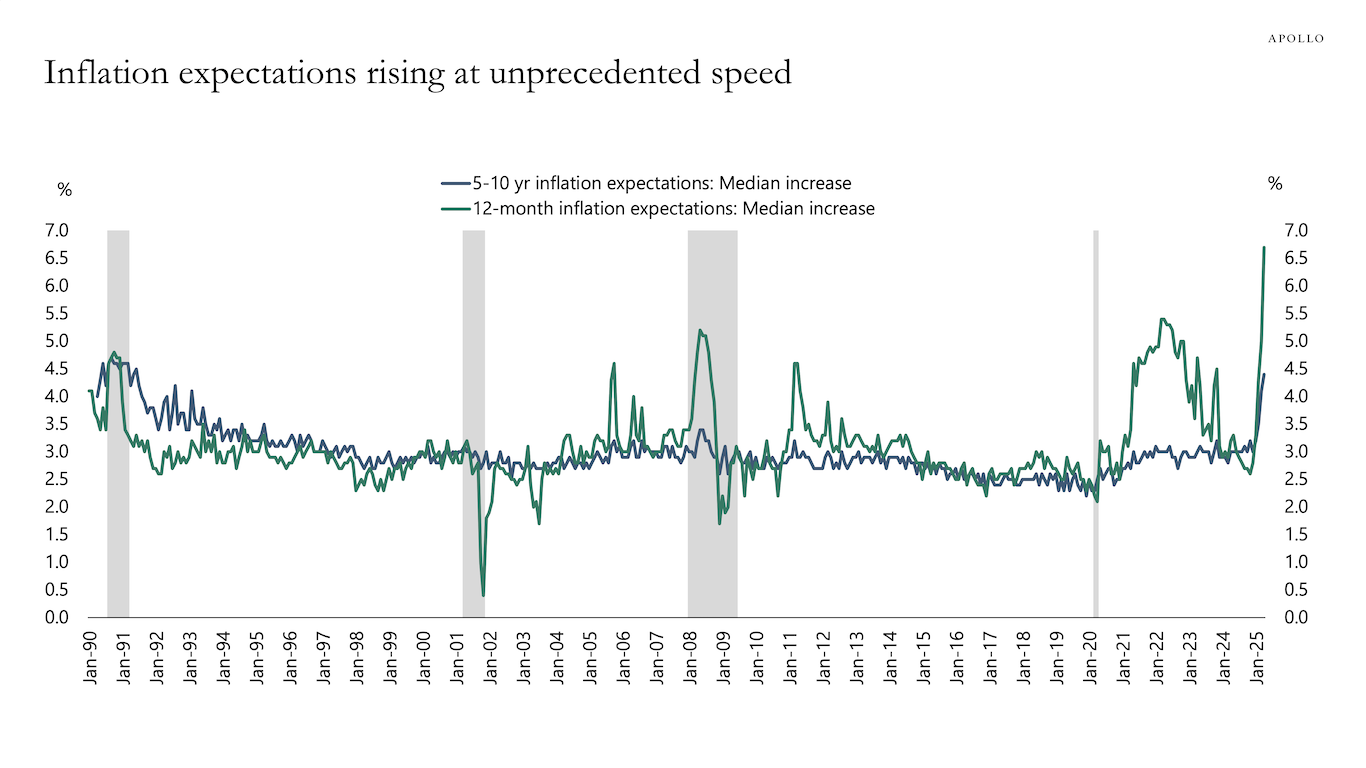

The April survey of consumer sentiment from the University of Michigan shows the following:

- Consumer sentiment is declining rapidly both for households making more than $100,000 and less than $100,000 (see the first chart).

- Consumers’ worries about losing their jobs are at levels normally seen during recessions (see the second chart).

- A record-high share of consumers think business conditions are worsening (see the third chart).

- Households’ income expectations are declining (see the fourth chart).

- Inflation expectations are rising at an unprecedented speed (see the fifth chart).

The bottom line is that consumer sentiment is very weak, and the fear is that this will spill over to weaker actual spending.

Sources: University of Michigan, Haver Analytics, Apollo Chief Economist

Sources: University of Michigan, Haver Analytics, Apollo Chief Economist

Sources: University of Michigan, Haver Analytics, Apollo Chief Economist

Sources: University of Michigan, Bloomberg, Apollo Chief Economist

Sources: University of Michigan, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

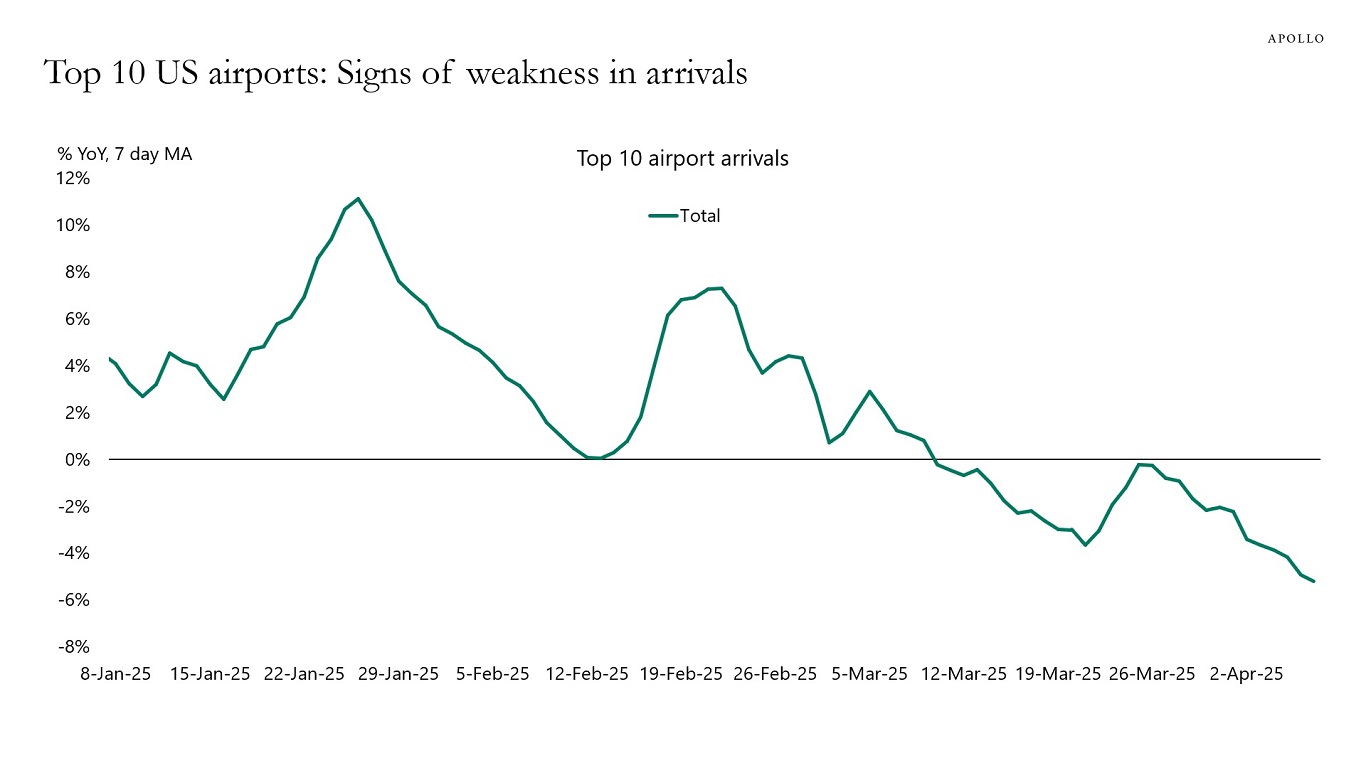

Daily data of the number of arrivals at the top 10 airports in the US has shown a rapid decline since late February, see chart below. This is likely a mix of declines in business travel, tourism, and government travel.

Note: Airports included are ATL, LAX, DFW, MIA, ORD, DEN, IAD, SFO, MCO, and JFK. Sources: CBP, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

The textbook would be saying that when the stock market is going down, long-term interest rates should also be going down.

But this is not what is happening at the moment, see chart below.

What could be the reasons why long-term interest rates are moving higher when the stock market is moving lower?

1) With the yen, euro, and Canadian dollar strengthening at the same time, this could be foreigners selling US Treasuries.

2) With the VIX at elevated levels around 50, there is a lot of hedging activity going on, and it could, therefore, be risk reduction among large asset managers managing rates, credit, and equities.

3) With almost $1 trillion in the basis trade, it could be an unwinding of the basis trade among levered hedge funds.

The answer is likely some combination of these three forces.

Note: Data starts from January 2020. Sources: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.