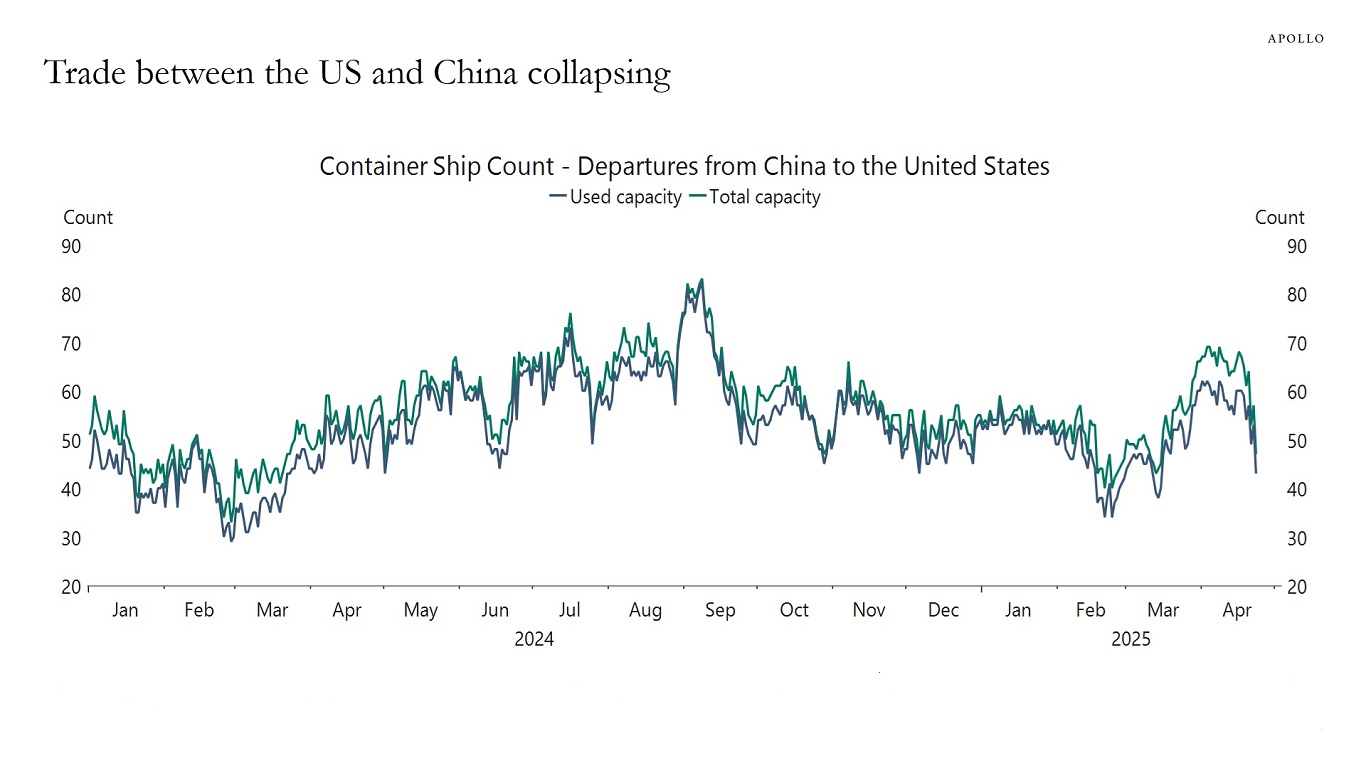

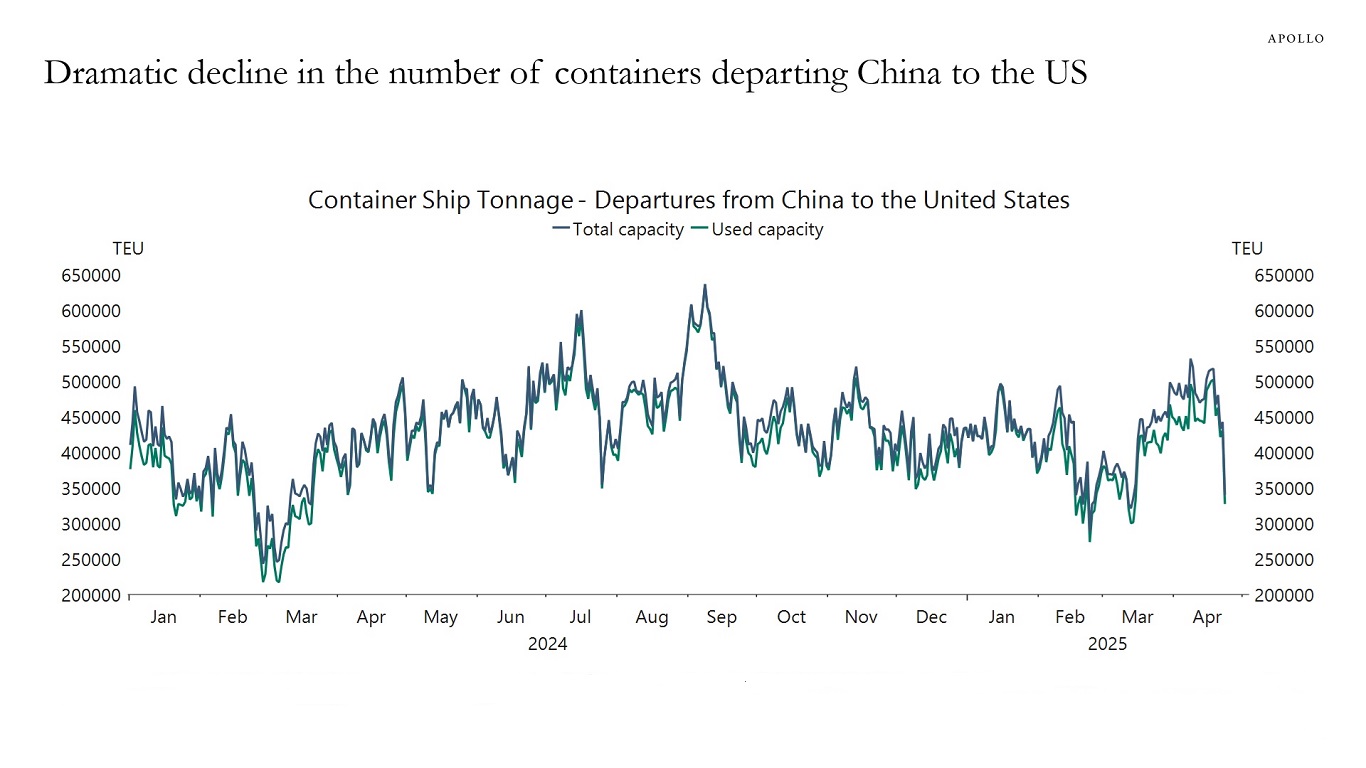

Daily data for container traffic from China to the US is collapsing, see charts below.

The consequence will be empty shelves in US stores in a few weeks and Covid-like shortages for consumers and for firms using Chinese products as intermediate goods.

In addition, we will soon begin to see higher inflation because there are a significant number of product categories where China is the main provider of certain goods into the US market.

In May, we will begin to see significant layoffs in trucking, logistics, and retail—particularly in small businesses such as your independent toy store, your independent hardware store, and your independent men’s clothing store. With 9 million people working in trucking-related jobs and 16 million people working in the retail sector, the downside risks to the economy are significant.

Note: Displays the estimated number of container vessels departing China for the United States, focusing on dry cargo chips. Aggregates data using a 15-day rolling average to reduce short-term volatility and provide a clearer view of broader trends in vessel activity. Sources: Bloomberg, Macrobond, Apollo Chief EconomistNote: Represents the aggregated container volume, measured in twenty-foot equivalent units (TEU), of vessels departing China for the United Sates over a 15-day rolling period. Accounts for the shipping capacity being utilized, irrespective of the number of vessels. Sources: Bloomberg, Macrobond, Apollo Chief Economist

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.