The Daily Spark is moving to Apollo.com— read the latest from Torsten Slok here.

Want it delivered daily to your inbox?

-

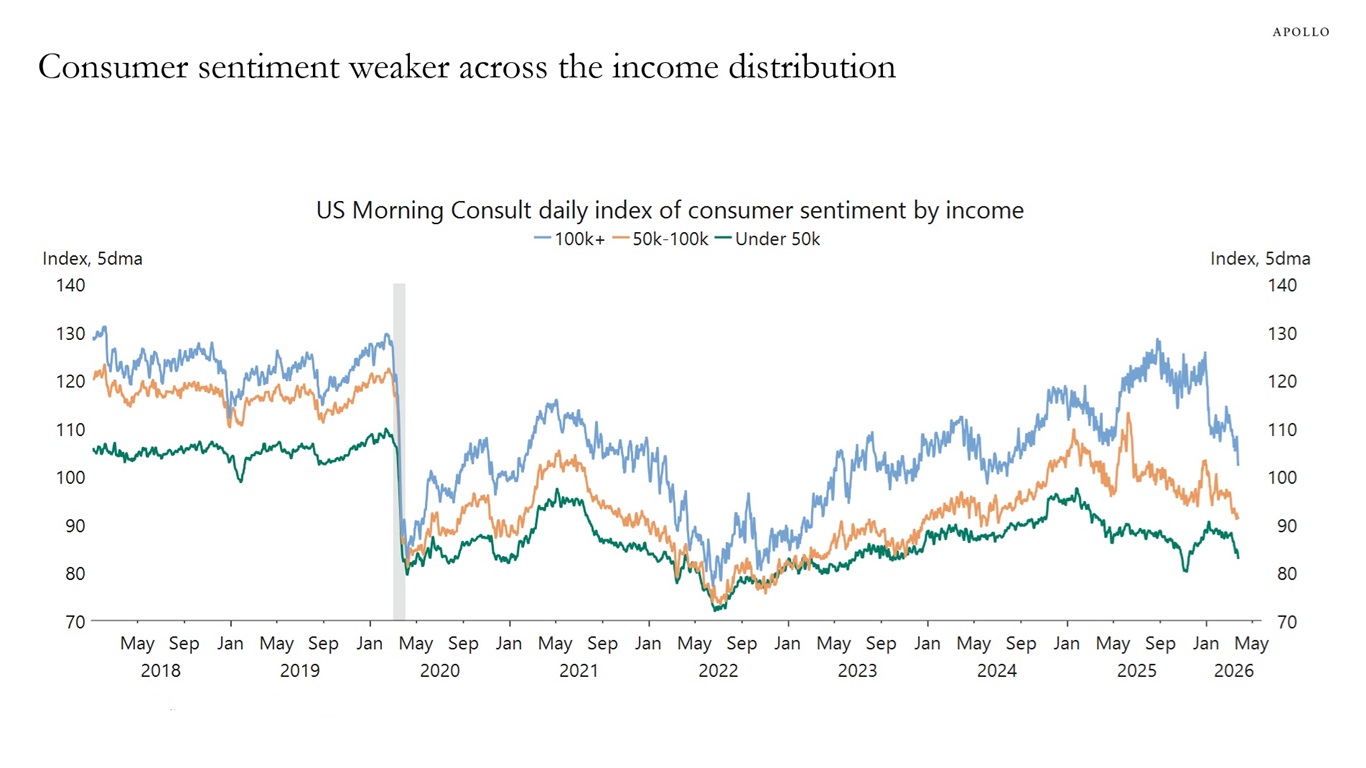

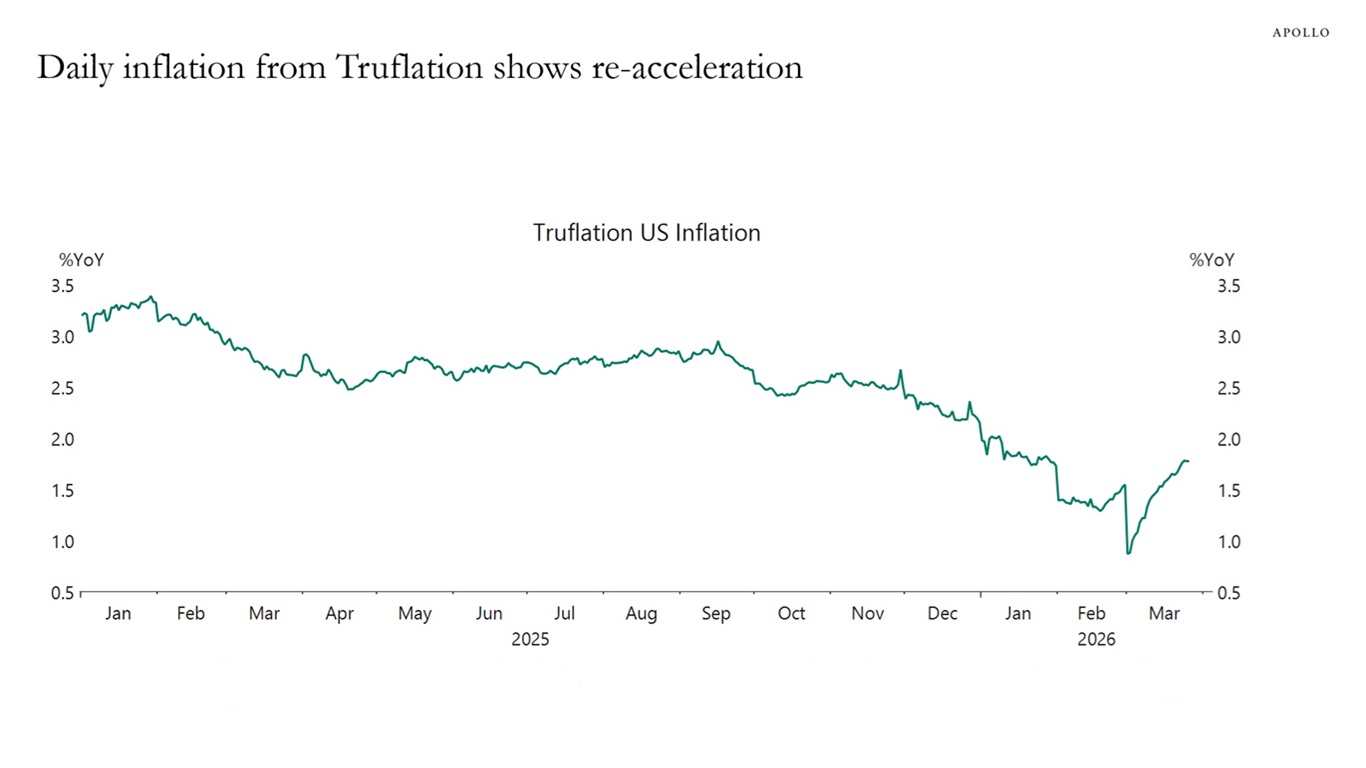

Daily data are starting to show a significant deterioration in inflation expectations and consumer sentiment across the income distribution, see the first two charts below.

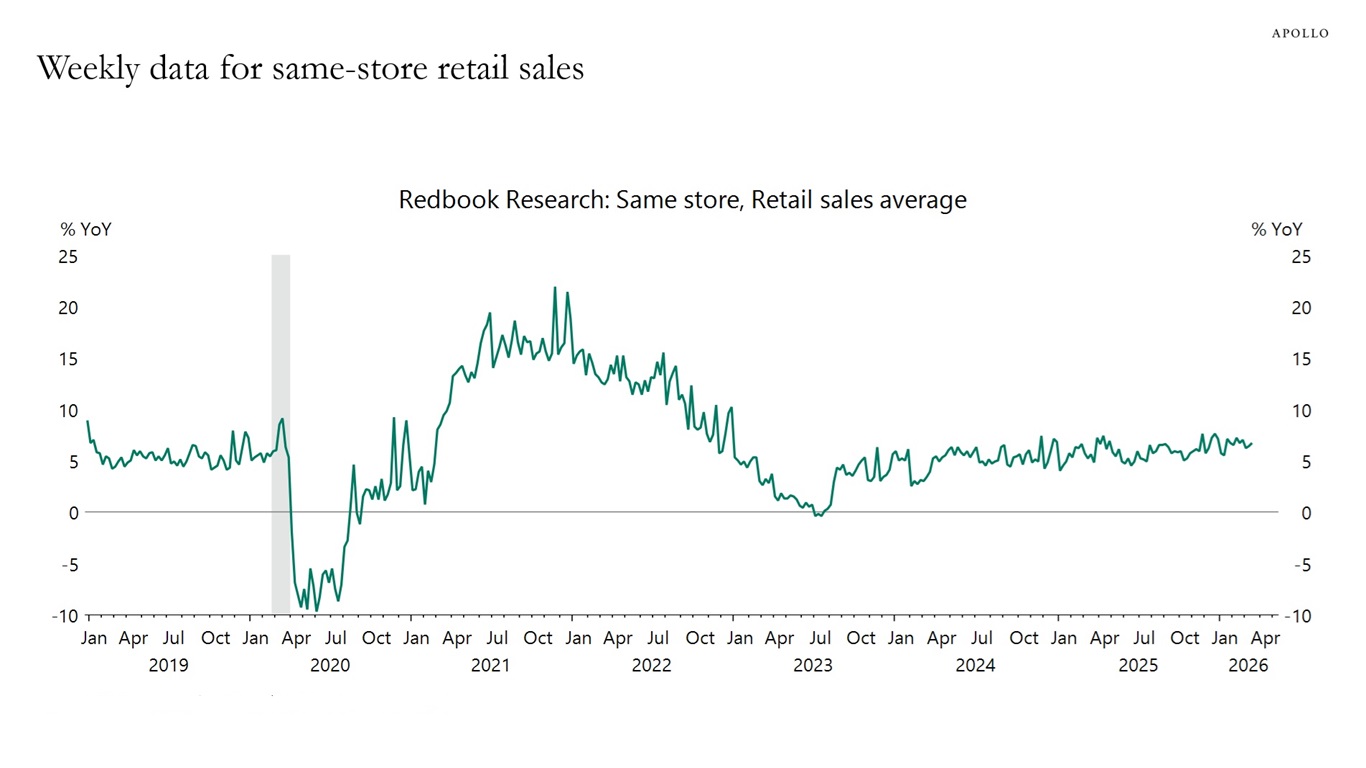

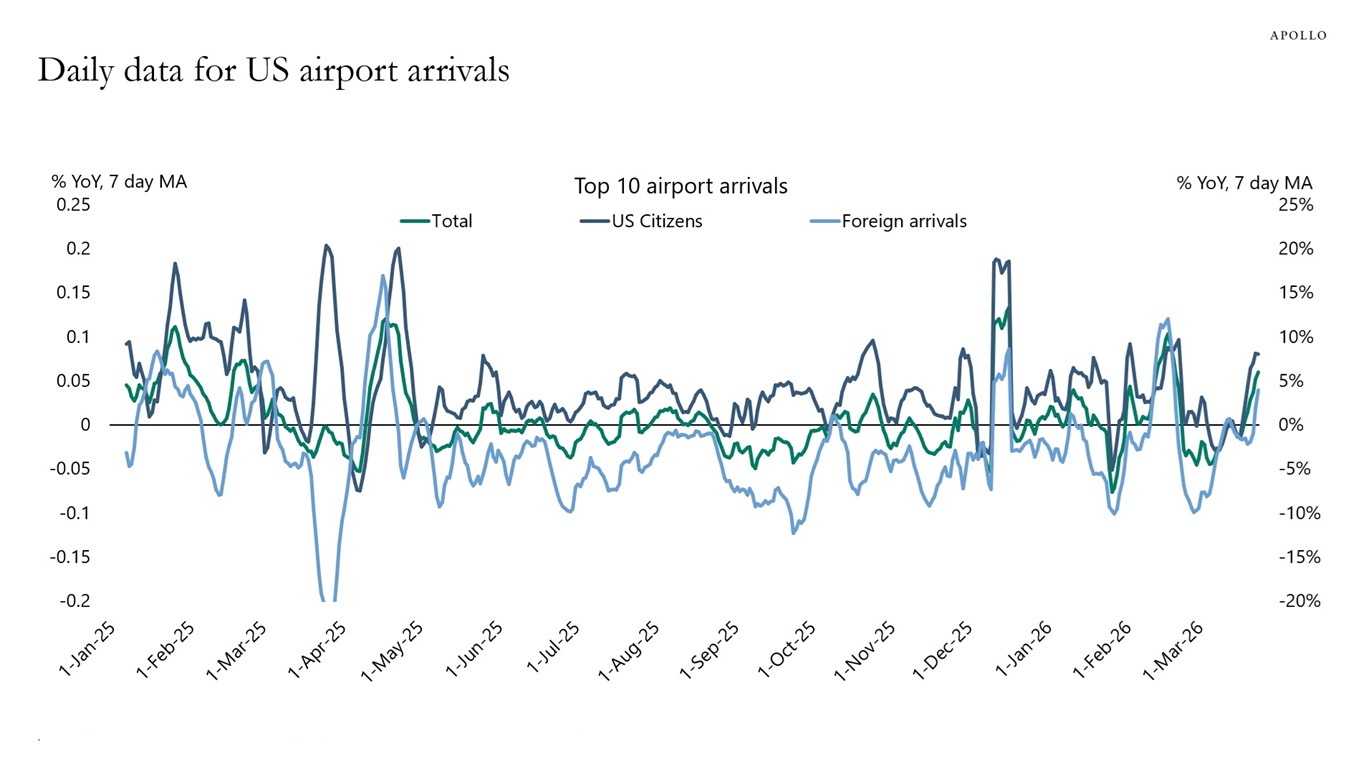

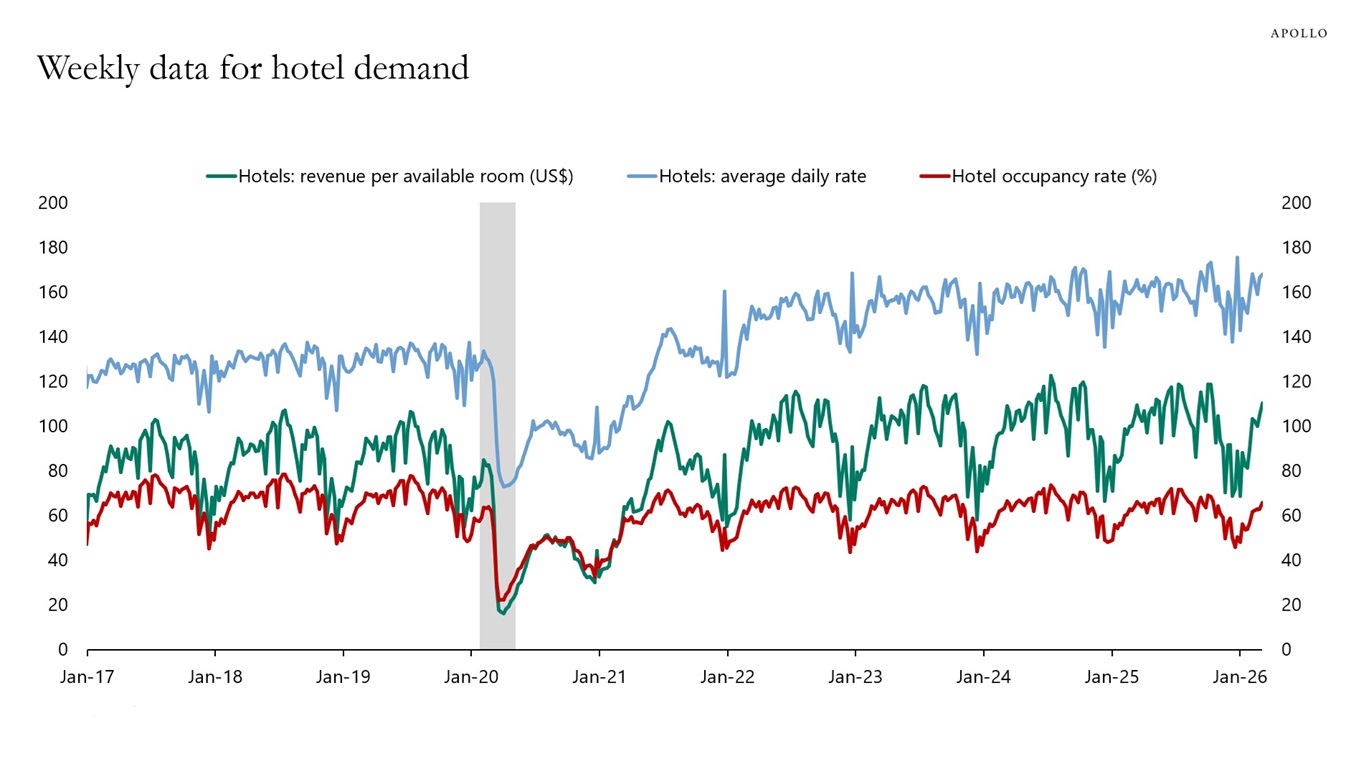

But there is a difference between what consumers are saying and what they are doing. The third, fourth and fifth charts below show that weekly data on consumer spending remain strong, daily data on airline travel remain strong and weekly data on hotel demand remain strong. A full review of all publicly available daily and weekly indicators shows no signs of demand destruction, see our chart book here.

Markets are overreacting to what will likely be a 4- to 6-week period of volatility, which will ultimately result in 50 years of stability in oil markets, supply chains and geopolitics. The Gulf region will become more stable and even more closely integrated with the global economy. For the Fed, the rise in inflation due to higher oil prices is temporary; once the conflict is over, Fed cuts will be priced in again, and long rates will decline.

The bottom line is that the Iran shock is not big enough to offset the strong tailwinds to the US economy from AI spending, the industrial renaissance and the One Big Beautiful Bill.

Sources: Morning Consult, Bloomberg, Macrobond, Apollo Chief Economist Note: The Truflation US Inflation Index is a daily measure of US inflation based on data from over 30 sources, including major retailers like Amazon and Walmart, and real estate data from sources like Zillow. It tracks price changes from a consumer cost of living perspective across 12 spending categories and is differentiated from the traditional Consumer Price Index (CPI) by its daily updates, use of digital data and a methodology that leverages blockchain for immutability and decentralization. Sources: Truflation, Bloomberg, Macrobond, Apollo Chief Economist Sources: Redbook Research Inc., Macrobond, Apollo Chief Economist Note: Airports included are ATL, LAX, DFW, MIA, ORD, DEN, IAD, SFO, MCO and JFK. Sources: CBP, Apollo Chief Economist Sources: STR, Haver Analytics, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

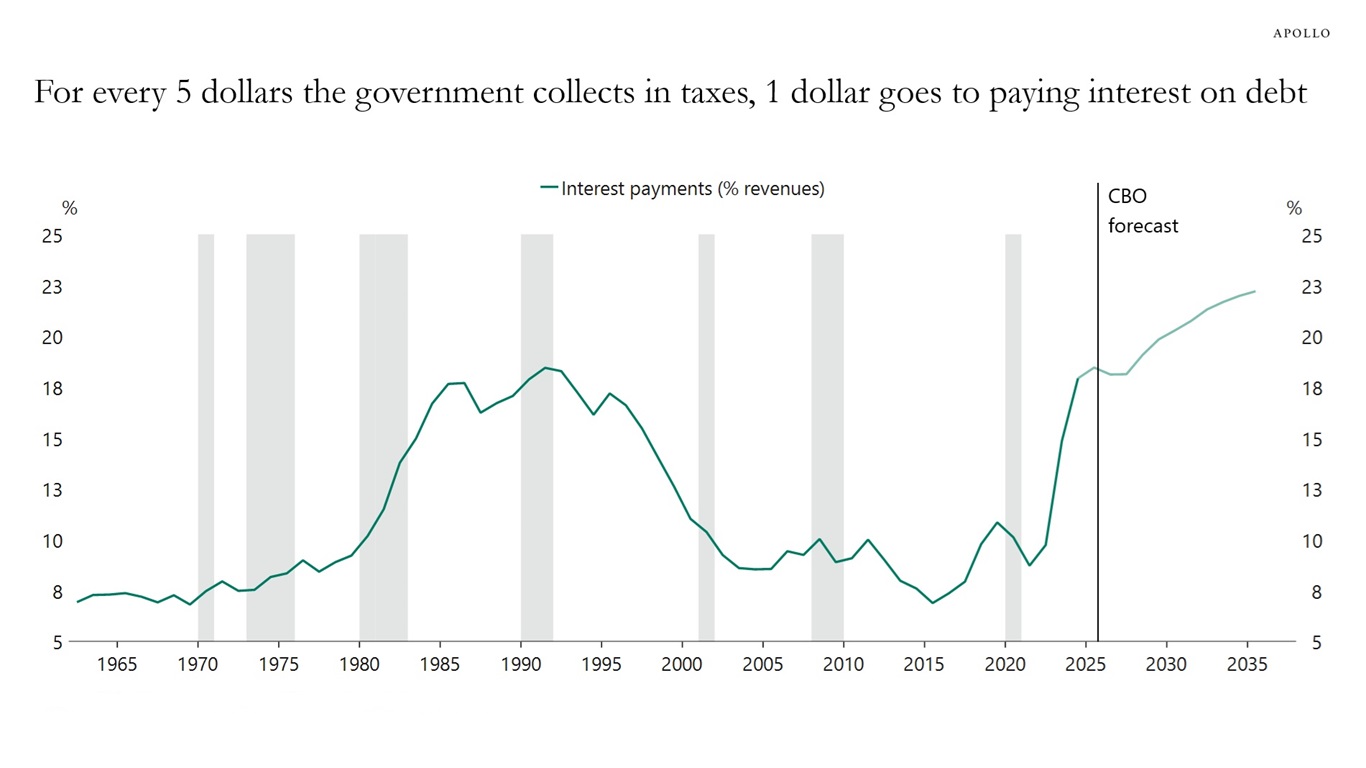

For every five dollars the government receives in tax revenue, one dollar is spent on servicing the national debt, see chart below.

Sources: US Congressional Budget Office (CBO), Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

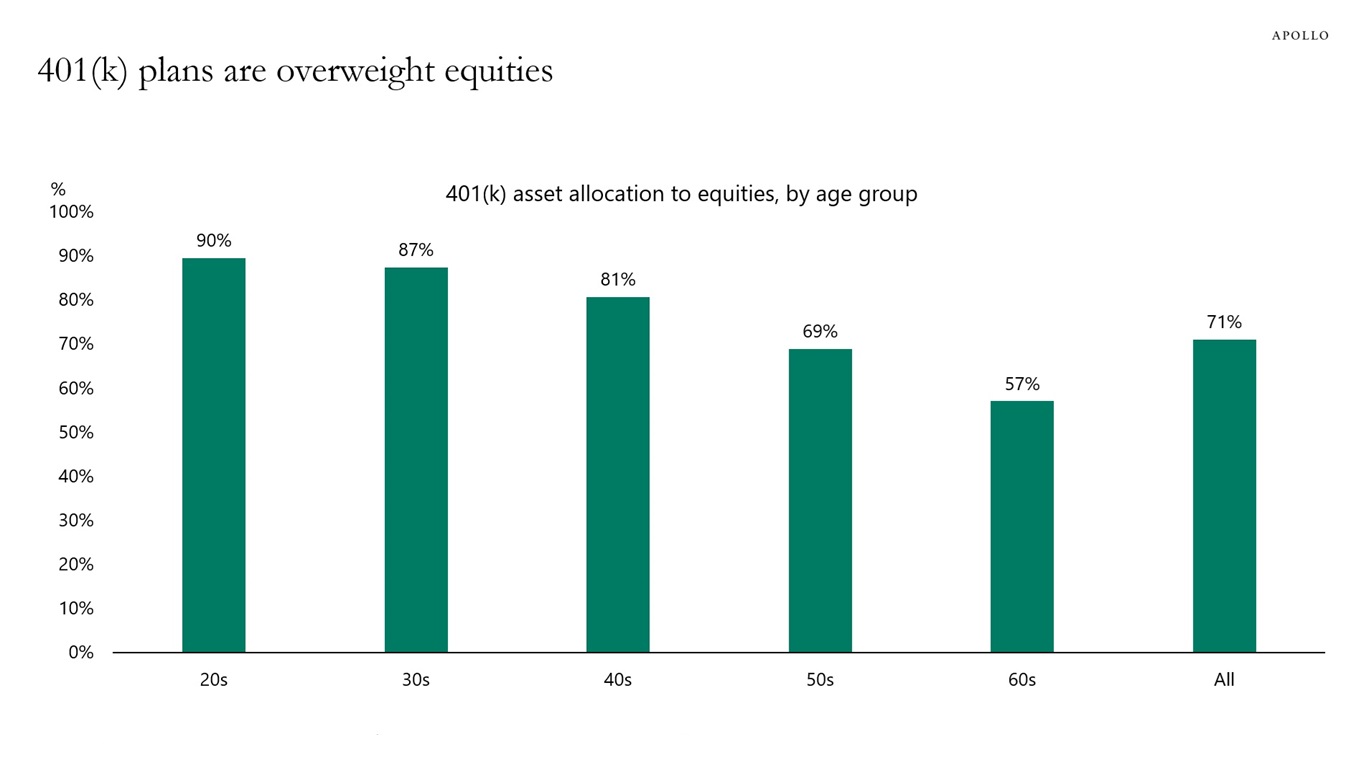

AI is driving returns in equity markets because of the growing size of tech in the S&P 500 index, and this is a problem for both institutional and individual investors, see chart below.

With hyperscalers issuing more debt, AI is increasingly also driving returns in bond markets.

And AI currently makes up 60% of investments in venture capital.

The bottom line is that there is one factor driving returns in portfolios, namely AI.

To avoid being overexposed to just one factor, asset allocation should deliberately increase exposure to sectors, regions and strategies whose fundamentals are less directly tied to AI.

Note: Equities include equity funds, company stock and the equity portion of balanced funds. Sources: EBRI, ICI, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

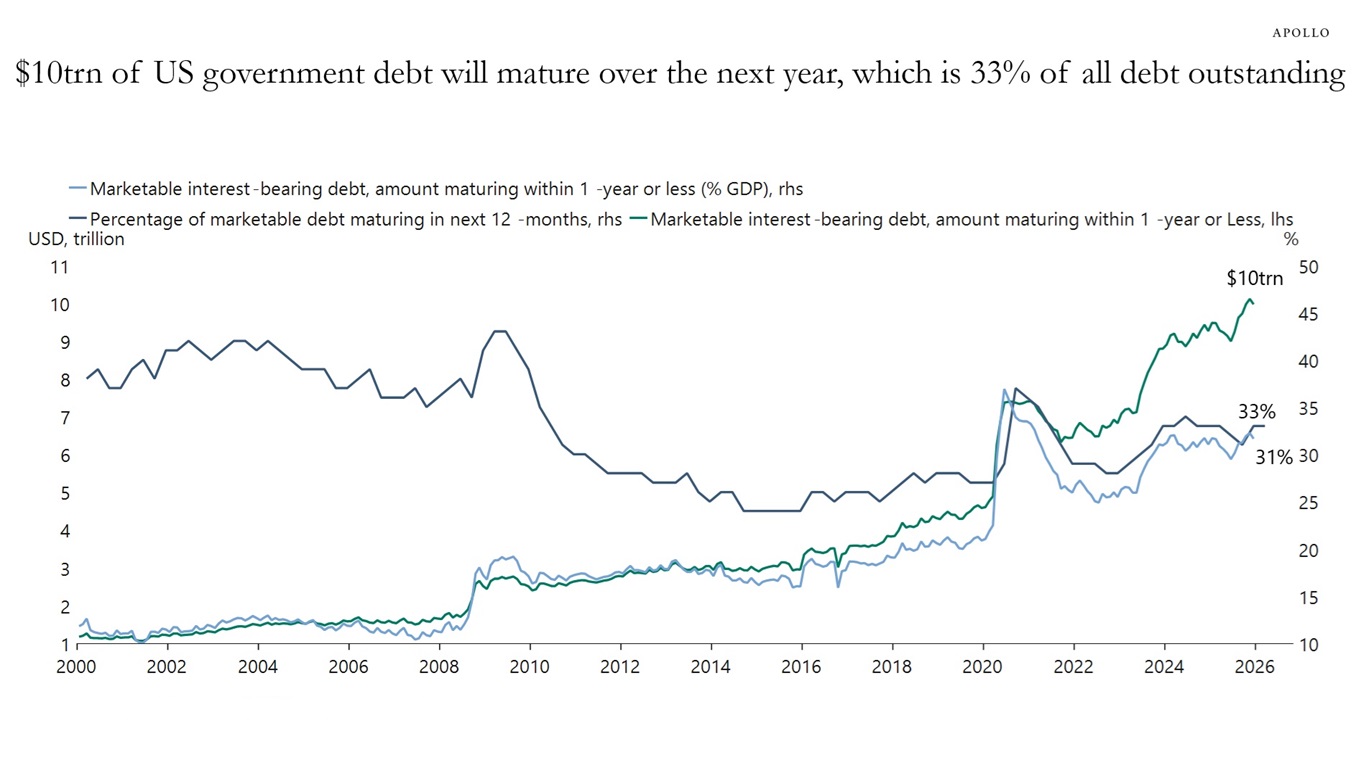

Ten trillion dollars in existing US government debt will need to be refinanced over the coming 12 months, see chart below.

The budget deficit this year is about $2 trillion.

Total gross corporate bond issuance in 2026 is likely to be around $2 trillion because of increased supply from hyperscalers.

Adding it all up, the total amount of investment grade supply coming to the market this year is around $14 trillion.

The bottom line is that the growing supply of investment grade fixed income product is putting upward pressure on rates and credit spreads.

Sources: US Department of Treasury, Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

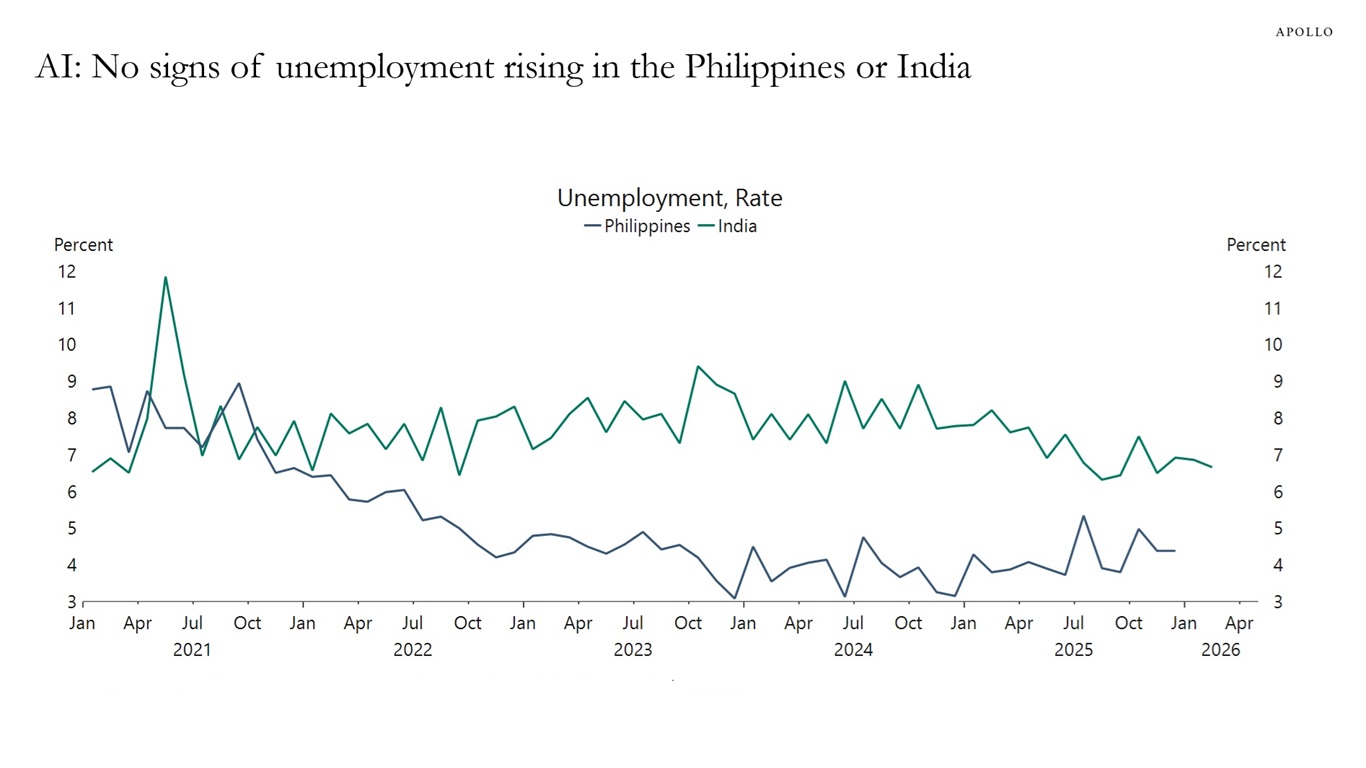

We are monitoring the unemployment rate in the Philippines and India for any signs that AI is reducing the need for outsourced workers in corporate America. So far, there are no signs of AI replacing offshore workers, see chart below.

Sources: Centre for Monitoring Indian Economy Pvt. Ltd. (CMIE), Philippine Statistics Authority, Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

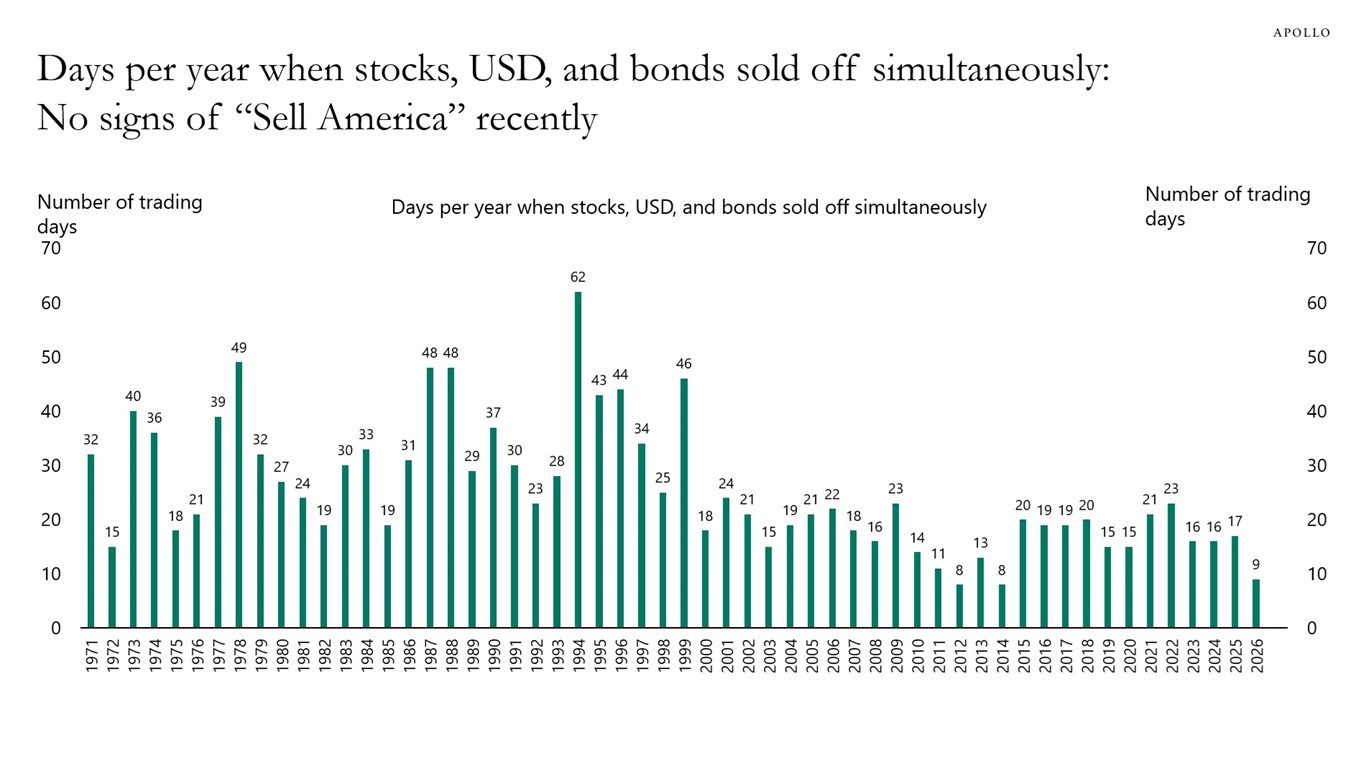

There are a lot of conversations in markets about the “Sell America” trade, i.e. the trade in which prices of US stocks, bonds and the dollar fall at the same time. But counting the number of days when this has happened shows no signs of 2025 and 2026 being anything special. In fact, the chart below shows that there has been no particular “Sell America” trade for the past 25 years.

The bottom line is that the US remains the most dynamic and innovative economy in the world, delivering the best and most steady returns for domestic and global investors.

Note: 2026 data is annualized. Sources: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

Markets are too focused on the near-term challenges from higher oil prices, see chart below. The real trade-off for investors is 4 to 6 weeks of instability, paying off 50 years of stability in oil markets, supply chains and geopolitics. The Gulf region will be more stable and even more closely integrated with the global economy. For the Fed, the rise in inflation because of higher oil prices is temporary, and once the conflict is over, Fed cuts will be priced in again and long rates will come down again.

Sources: Bloomberg, Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

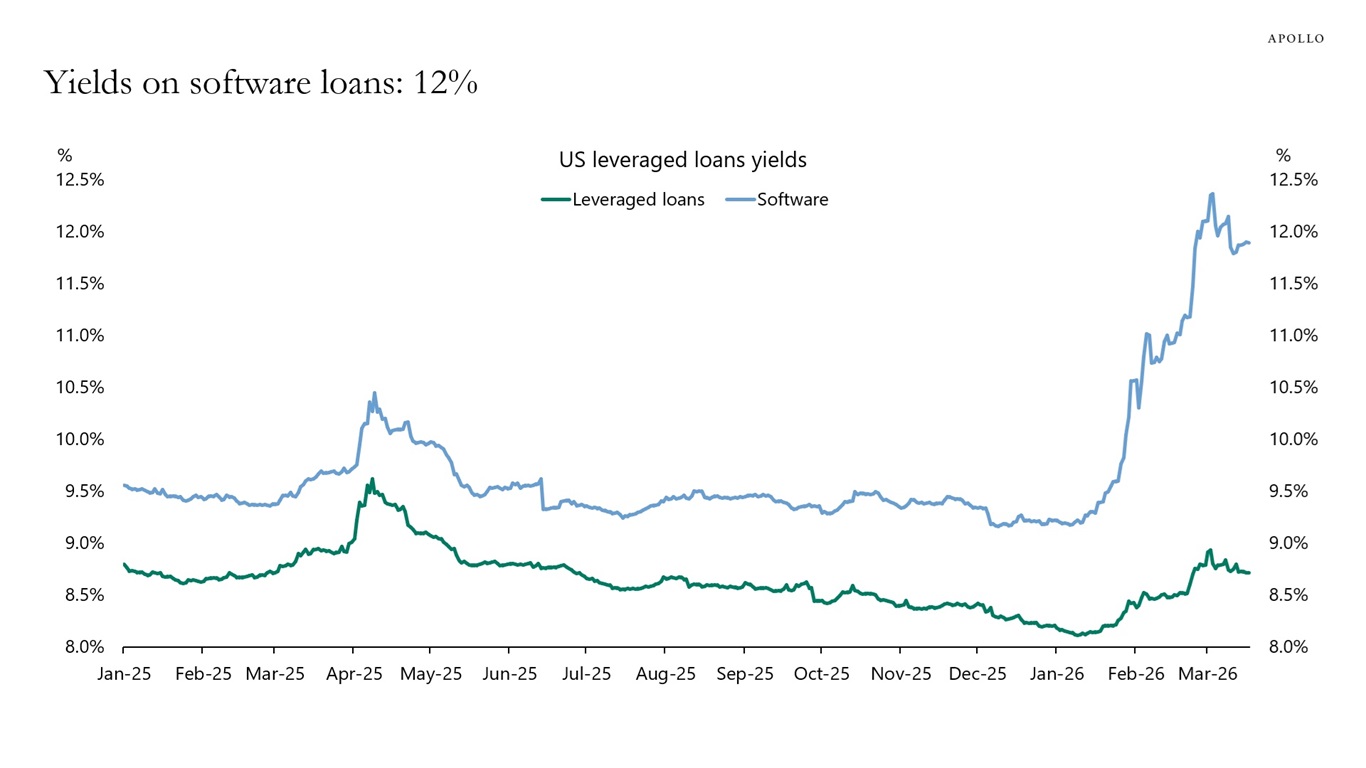

While the yield on software loans has increased significantly, yields on loans more generally have actually been going down, see chart below.

This suggests that the distress in software is largely idiosyncratic, rather than driven by a broad-based macro deterioration in credit conditions.

Sources: PitchBook, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

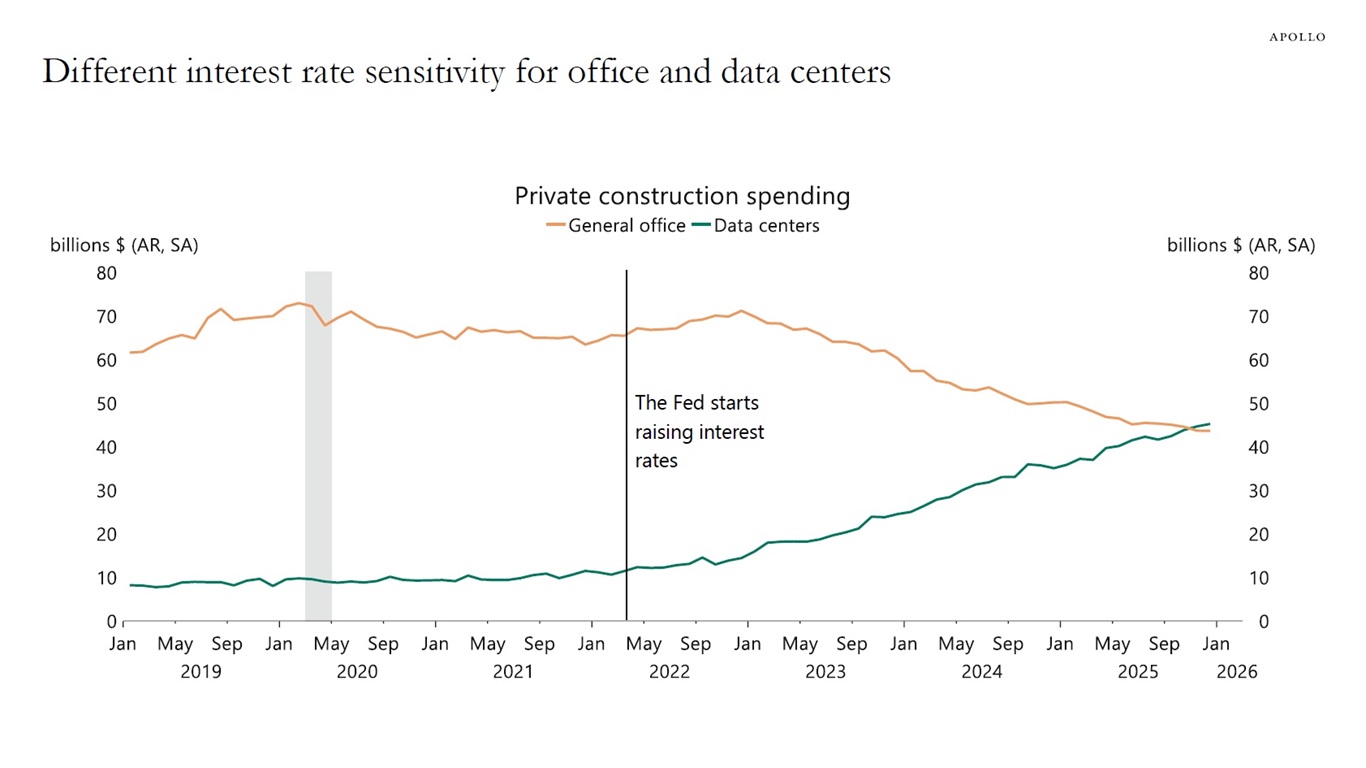

When the Fed began hiking in 2022, traditional rate-sensitive sectors like office construction rolled over quickly. But data center construction continued to surge, as investors and hyperscalers judged that AI-driven returns would exceed the higher cost of capital.

In effect, one of the traditional channels through which monetary tightening slows activity, a pullback in commercial construction, has been partially offset by structurally strong demand for digital infrastructure.

High expected returns and strategic capacity needs in data centers help explain why tighter monetary policy has cooled the economy less than in past cycles.

Combined with the positive growth impulse from the One Big Beautiful Bill, we expect economic growth to remain firm through 2026.

Sources: US Census Bureau, Macrobond, Apollo Chief Economist See important disclaimers at the bottom of the page.

-

There are no signs of a slowdown in corporate earnings expectations, see chart below.

Sources: Bloomberg, Apollo Chief Economist See important disclaimers at the bottom of the page.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.