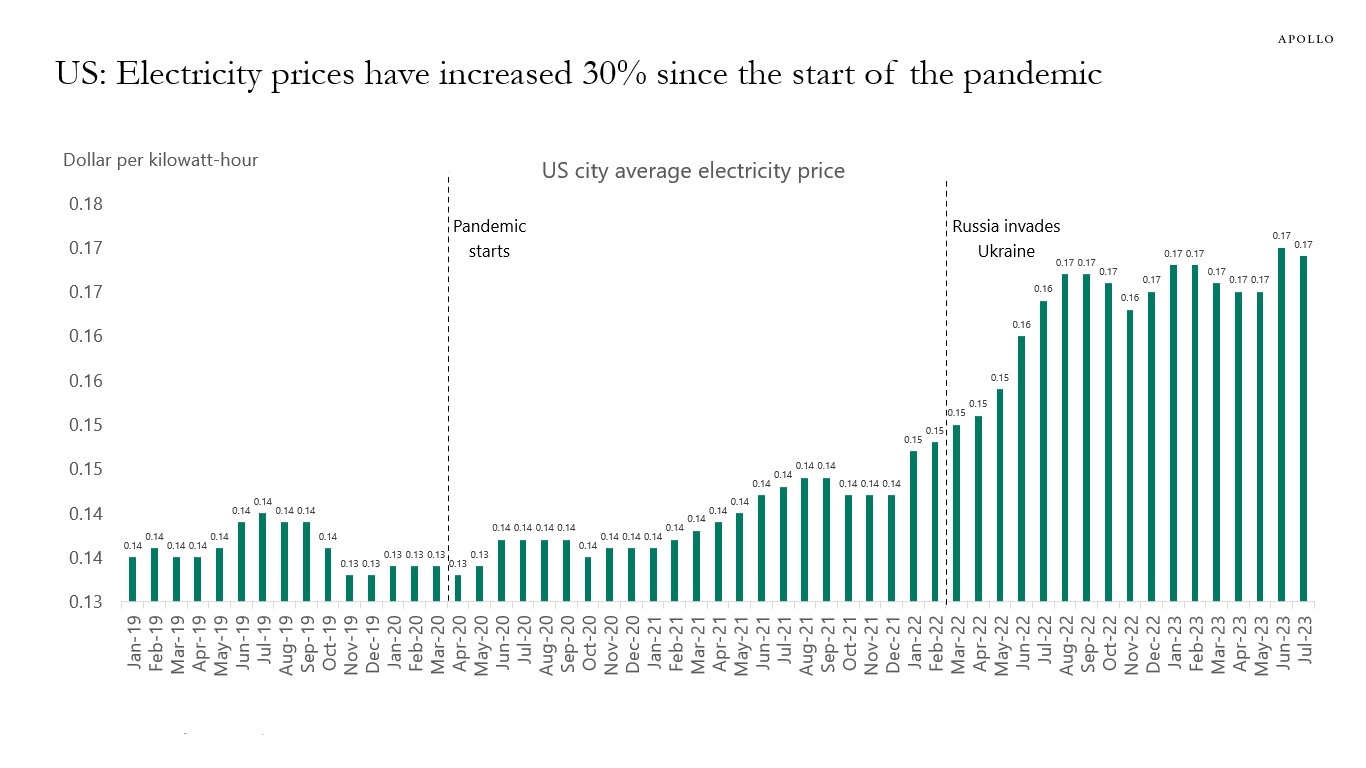

Electricity prices for households are up 30% since the pandemic started, see chart below.

Electricity prices for households are up 30% since the pandemic started, see chart below.

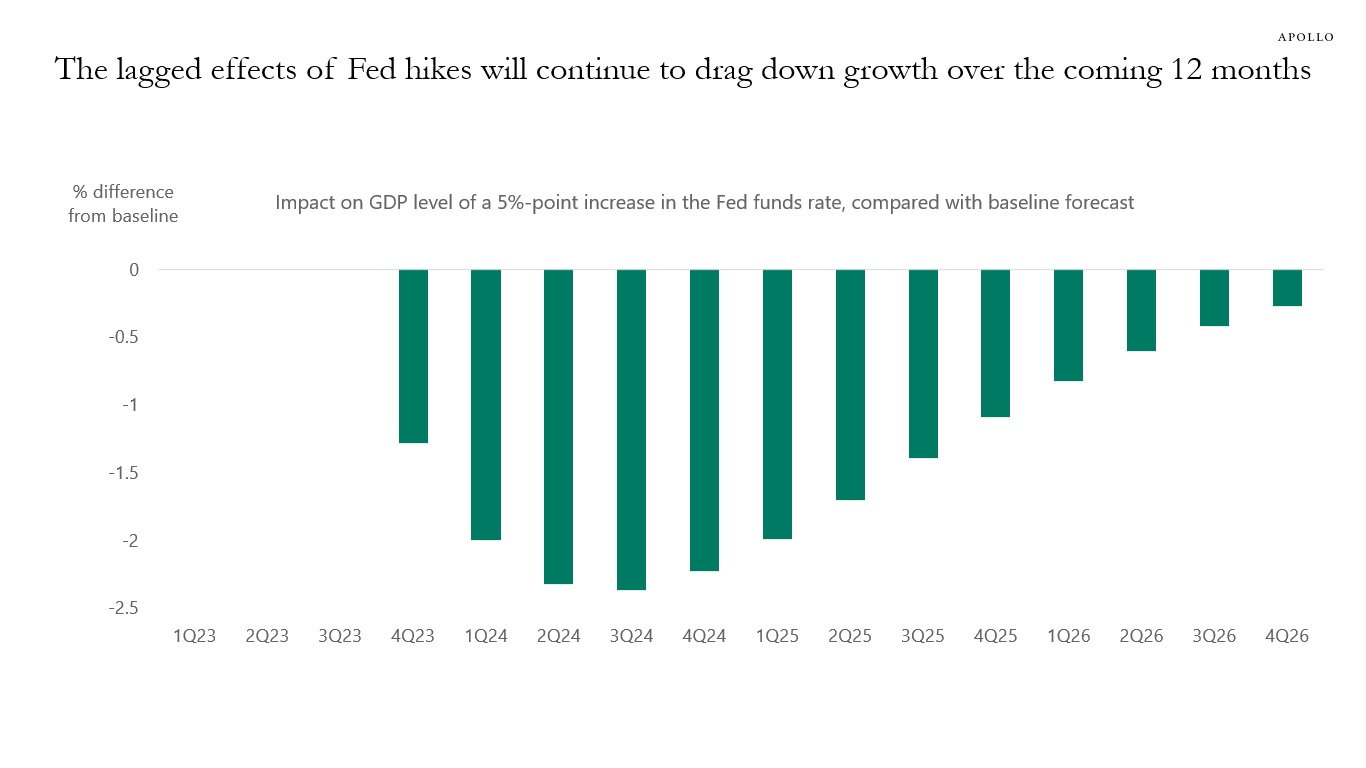

The FOMC started raising rates 16 months ago, and there are two different explanations for why Fed hikes have not yet slowed down the economy in a meaningful way:

1) The Fed has not raised interest rates enough.

2) The lagged effects of Fed hikes take longer than we think.

The Fed does not know if the continued strength in the economic data is because it has not raised rates enough or if the lagged effects of Fed hikes take longer than usual. As a result, the FOMC’s approach is to keep interest rates elevated until the economy starts slowing down. Against this backdrop, a soft landing is not an option because the Fed will keep interest rates high until they get the economic slowdown required for them to turn dovish.

Even if inflation comes down and growth is still strong, the Fed will continue to be hawkish because of worries about strong growth causing a re-acceleration in inflation. The implication for markets is that a recession is a pre-condition for the Fed to stop being hawkish.

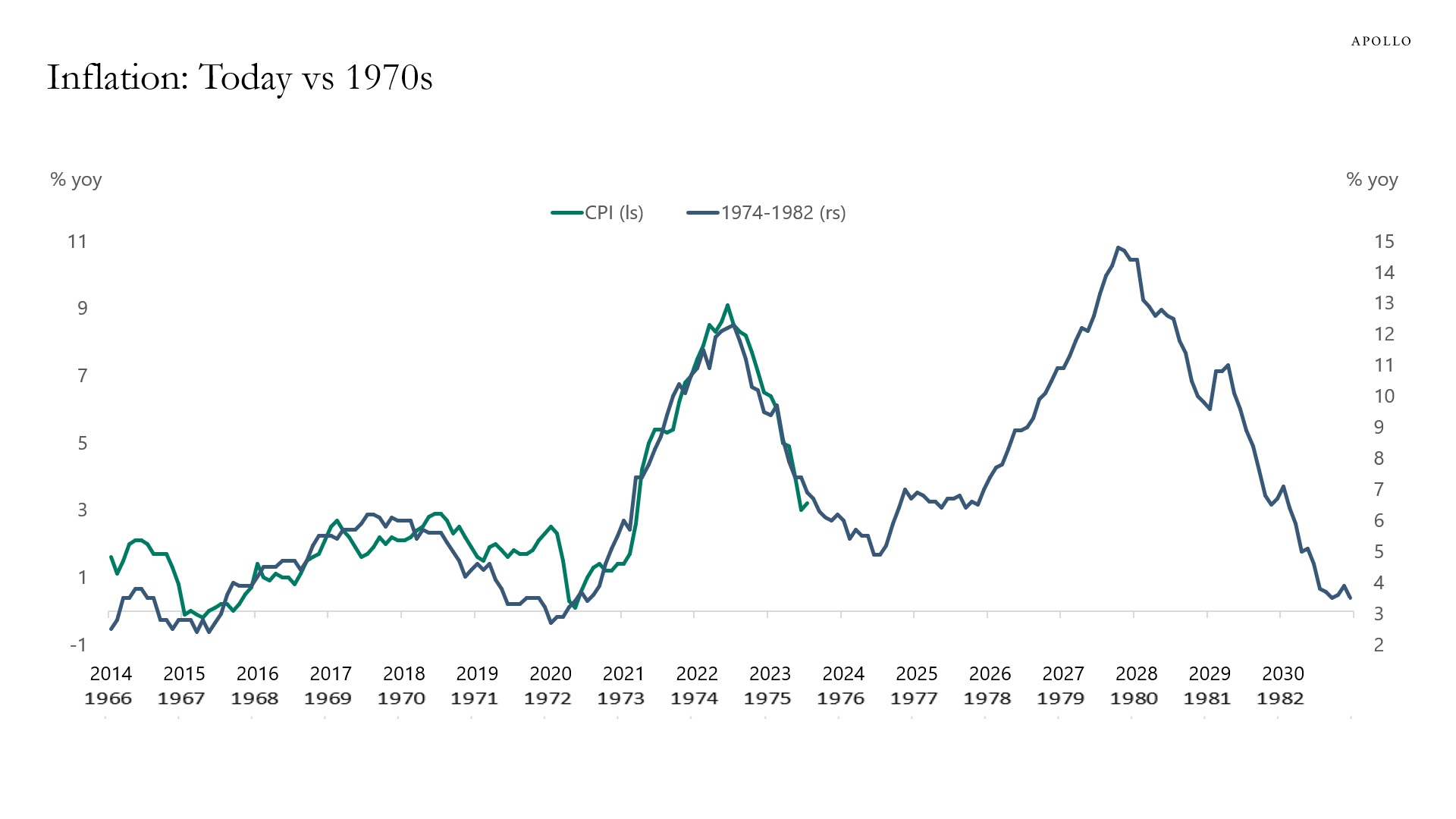

There are two lessons from the 1970s for the Fed today, see chart below.

First, if the Fed turns dovish too quickly, then inflation and inflation expectations will not settle at 2%.

Second, if the economy re-accelerates, the Fed will have to raise rates a lot more.

The implication for markets is that the Fed will be keeping the cost of capital higher for longer than the market is currently pricing to ensure that the FOMC doesn’t repeat the mistakes made in the 1970s.

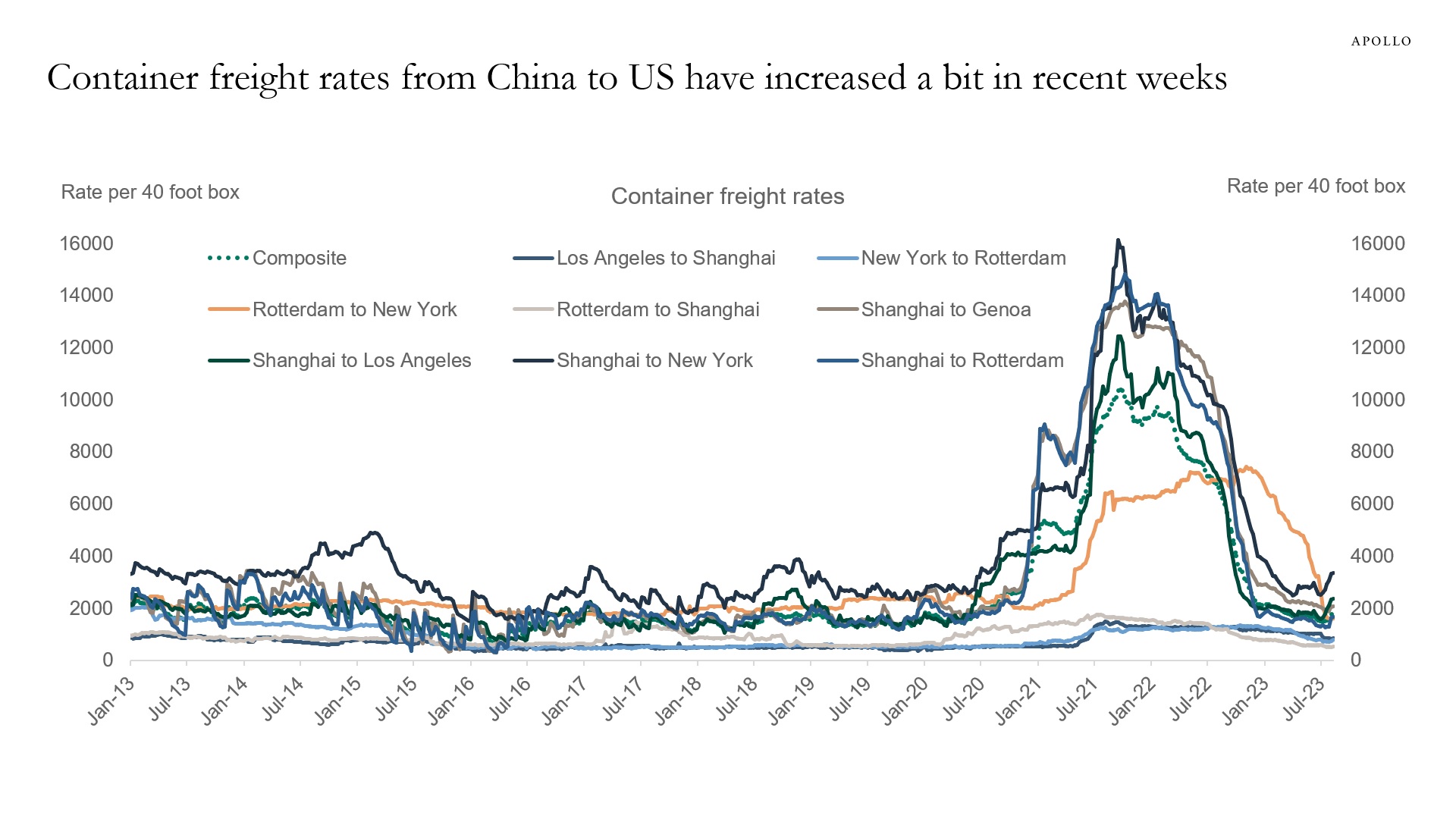

Supply chains are back to normal, but we are monitoring the rise in recent weeks in the price of transporting a container from China to the US. See chart below and this updated presentation.

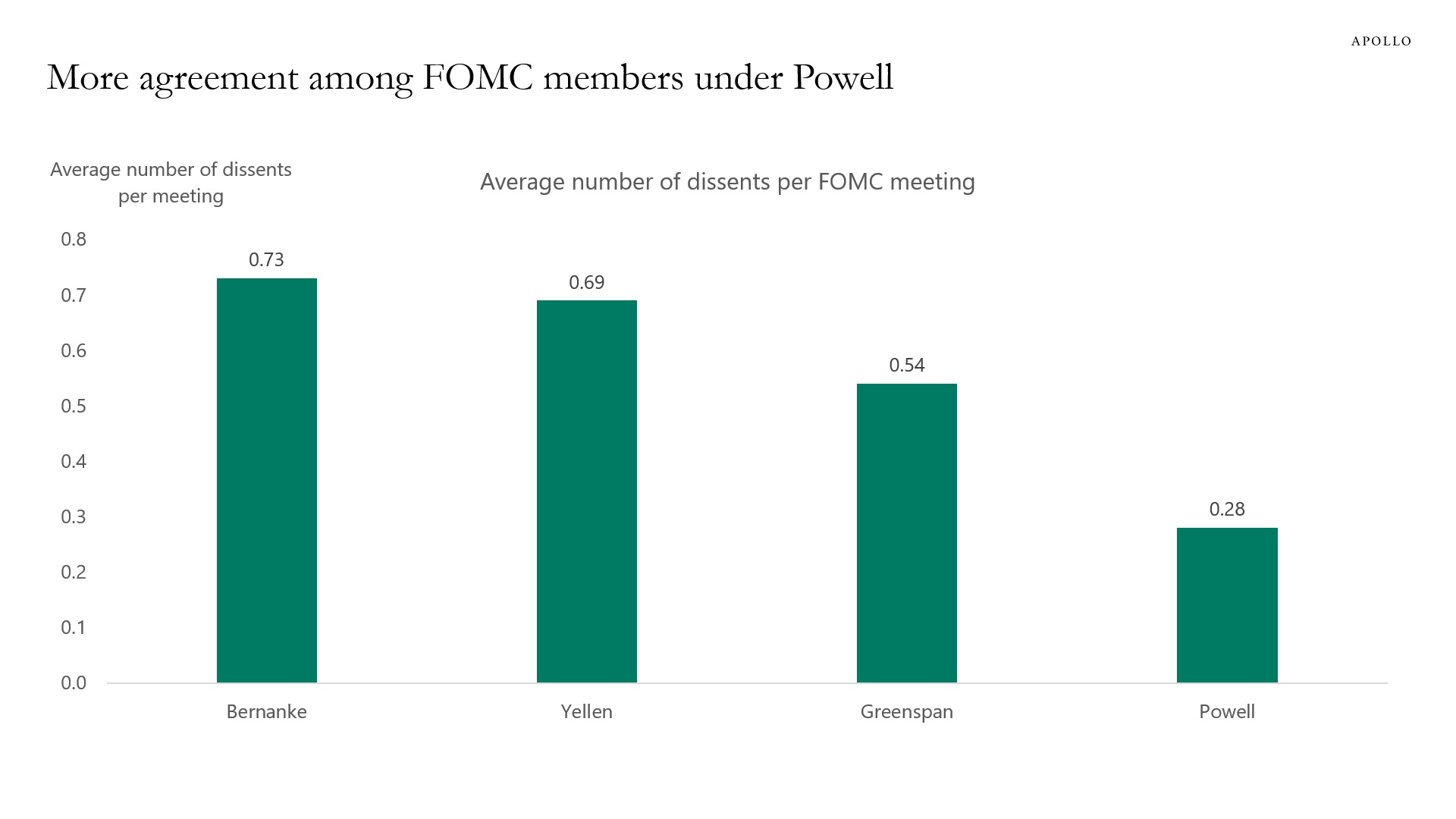

The average number of dissents per FOMC meeting has been lower under Powell, see chart below.

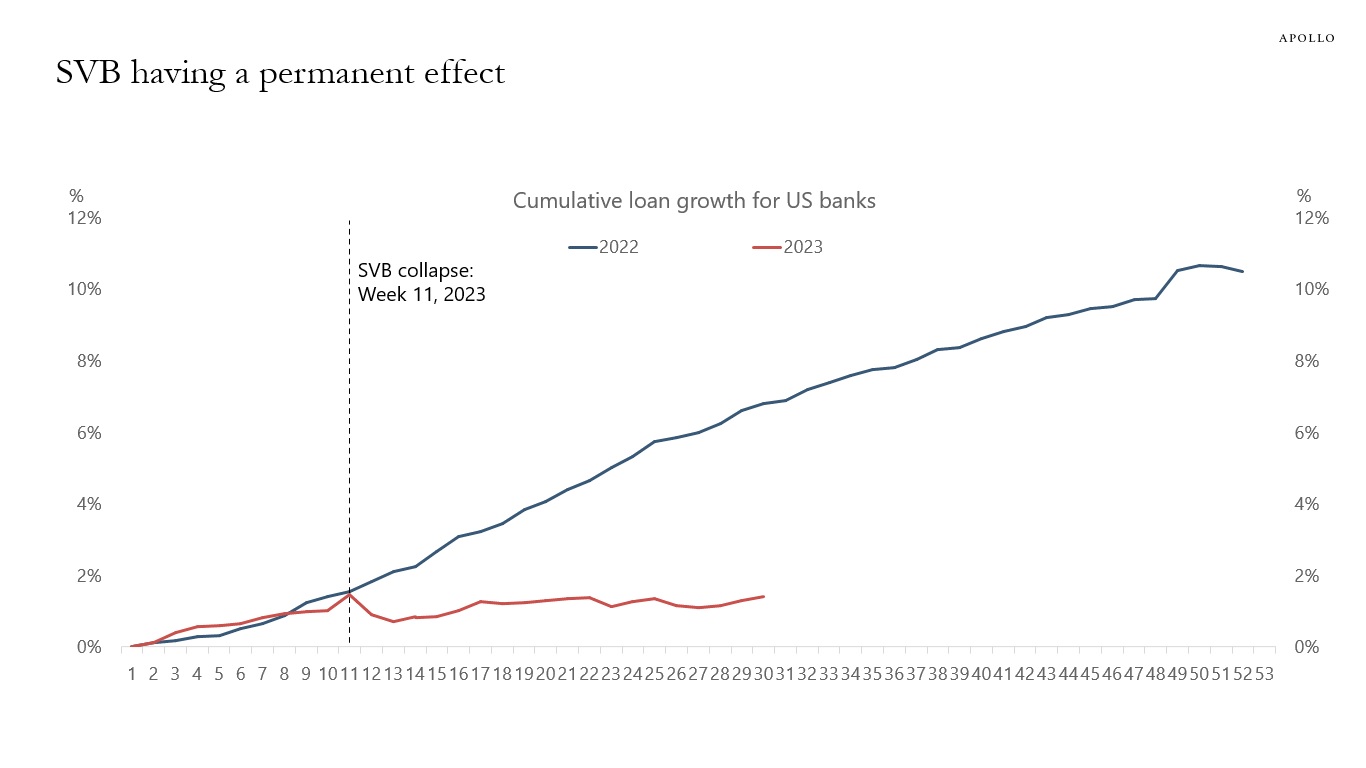

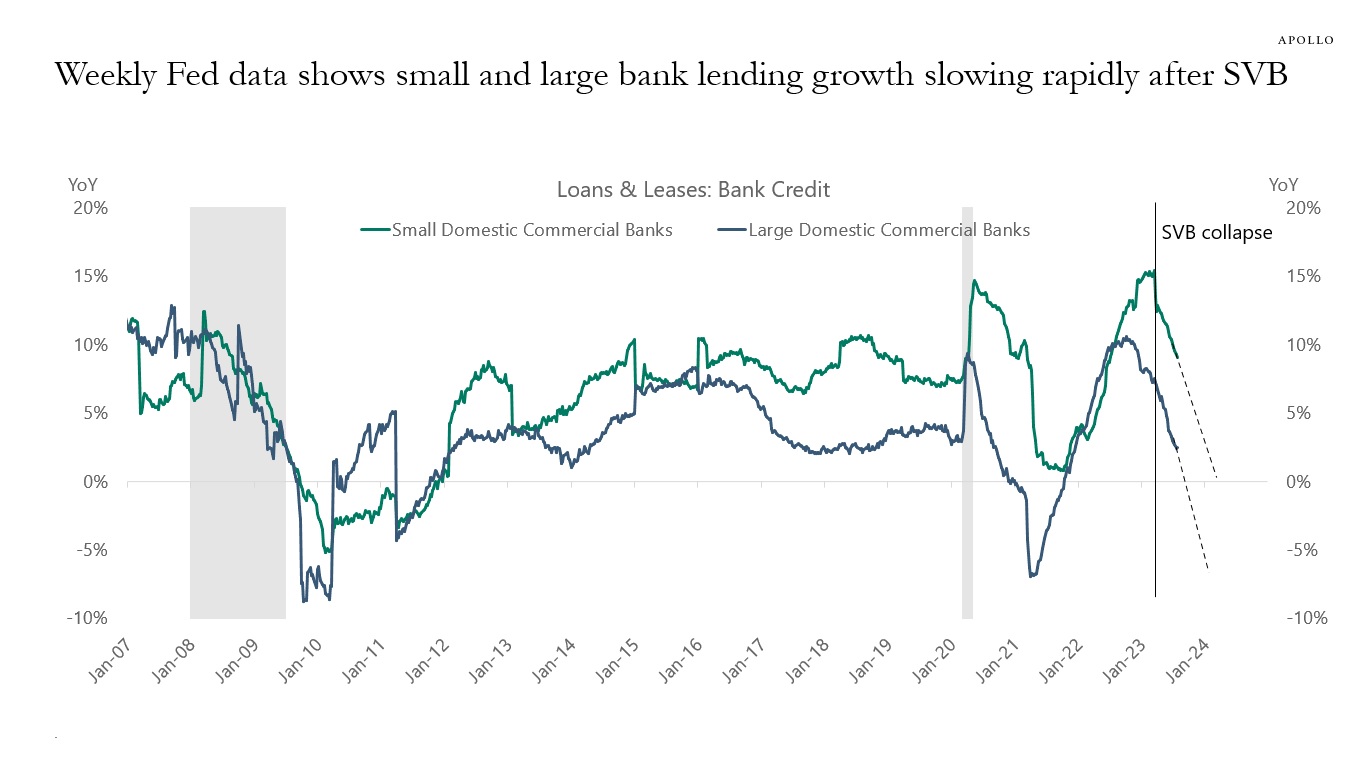

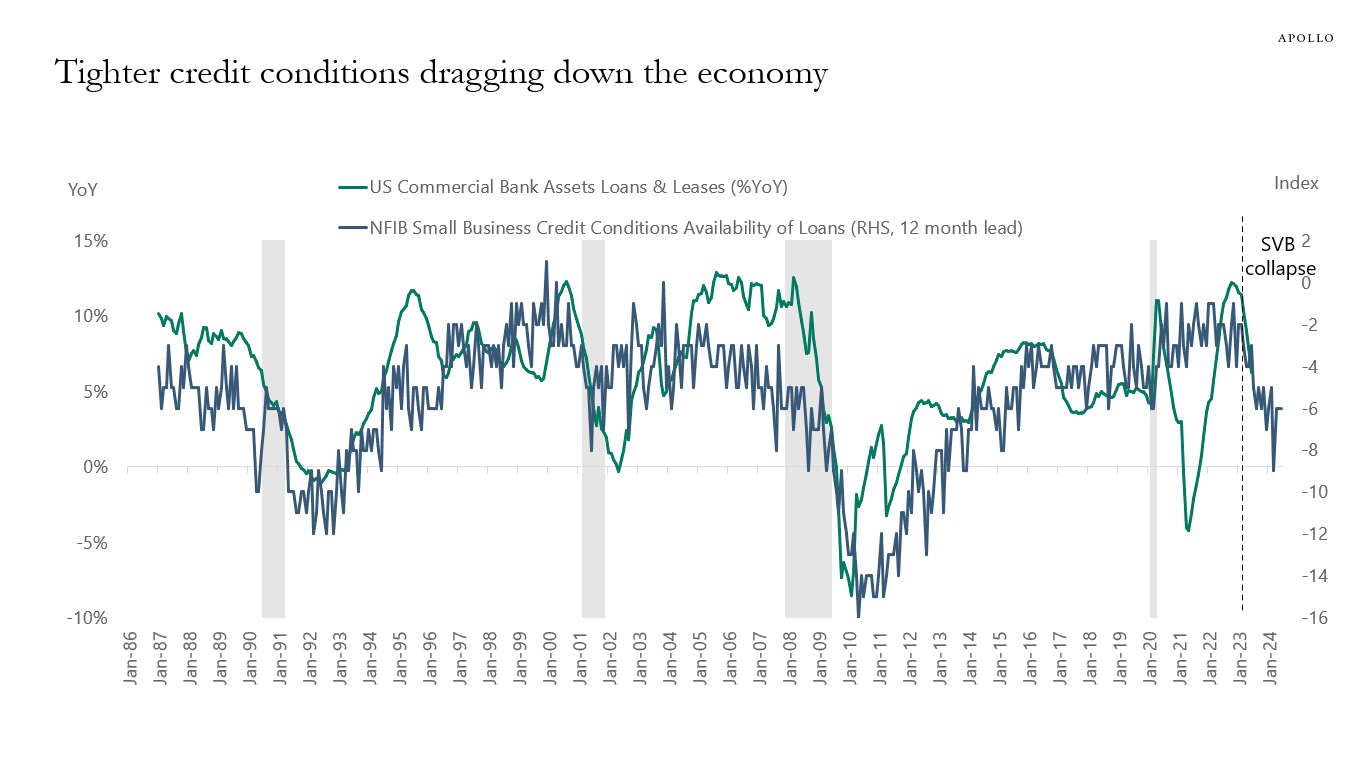

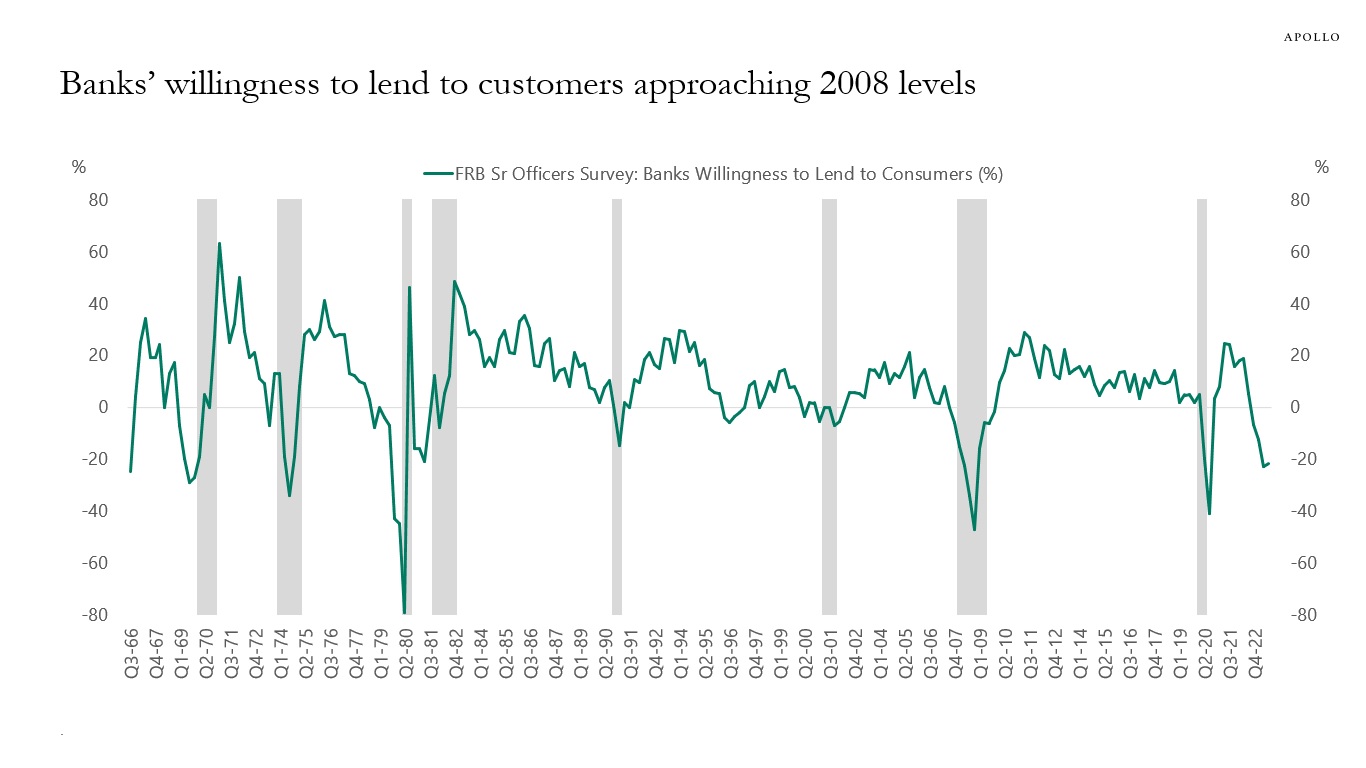

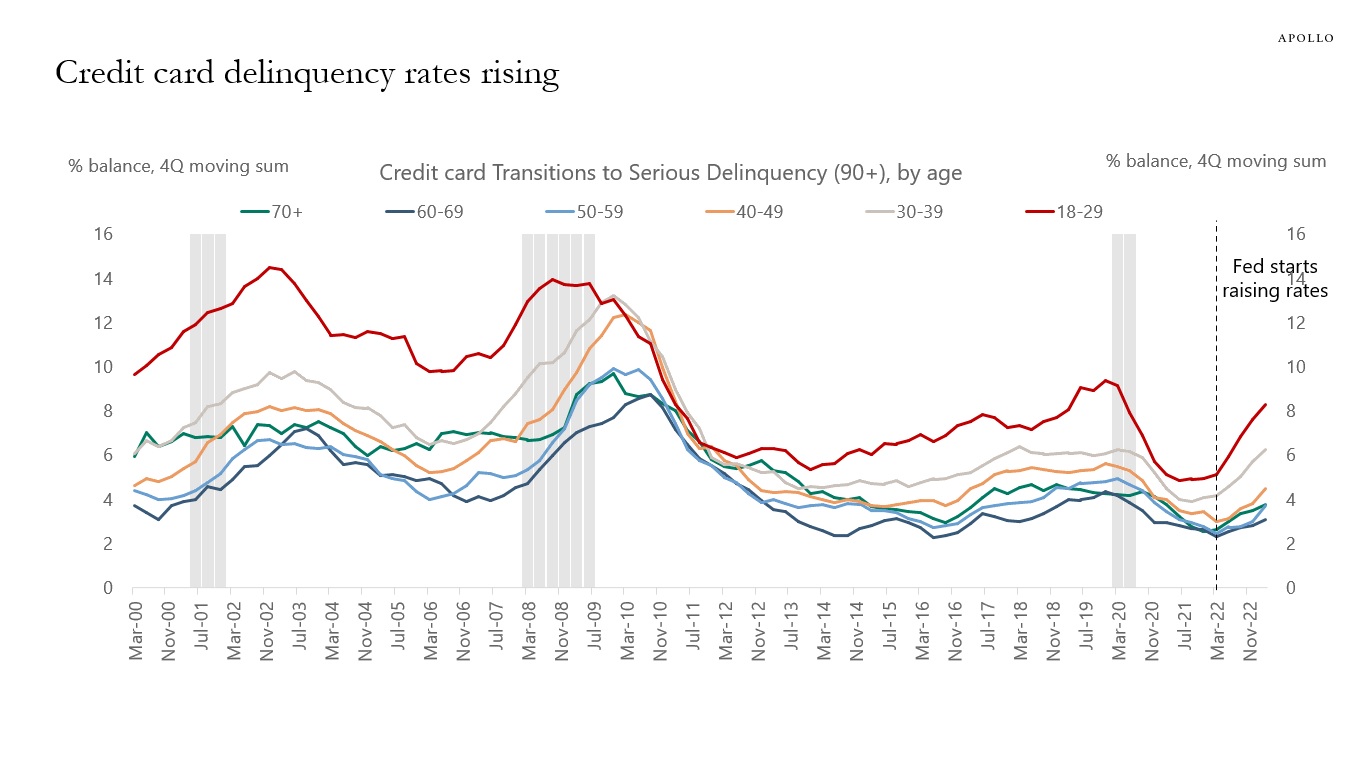

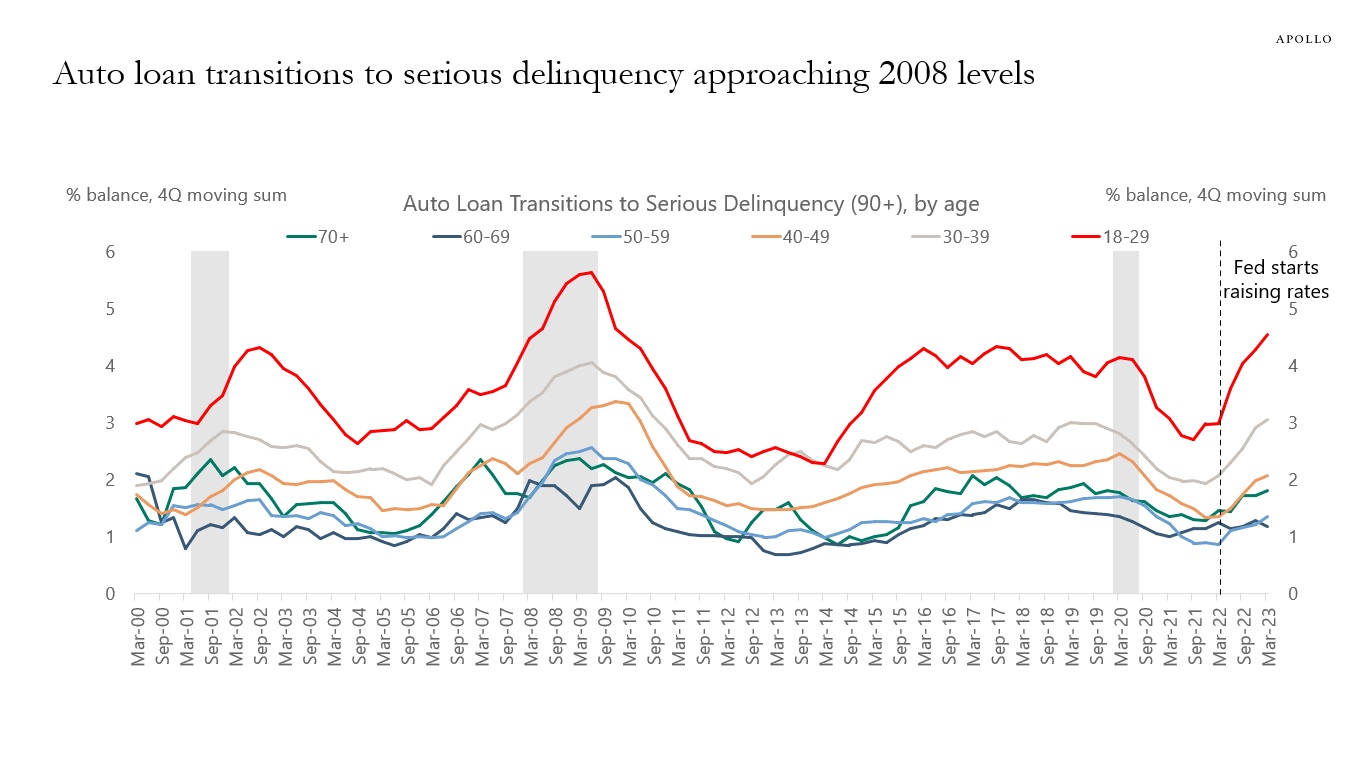

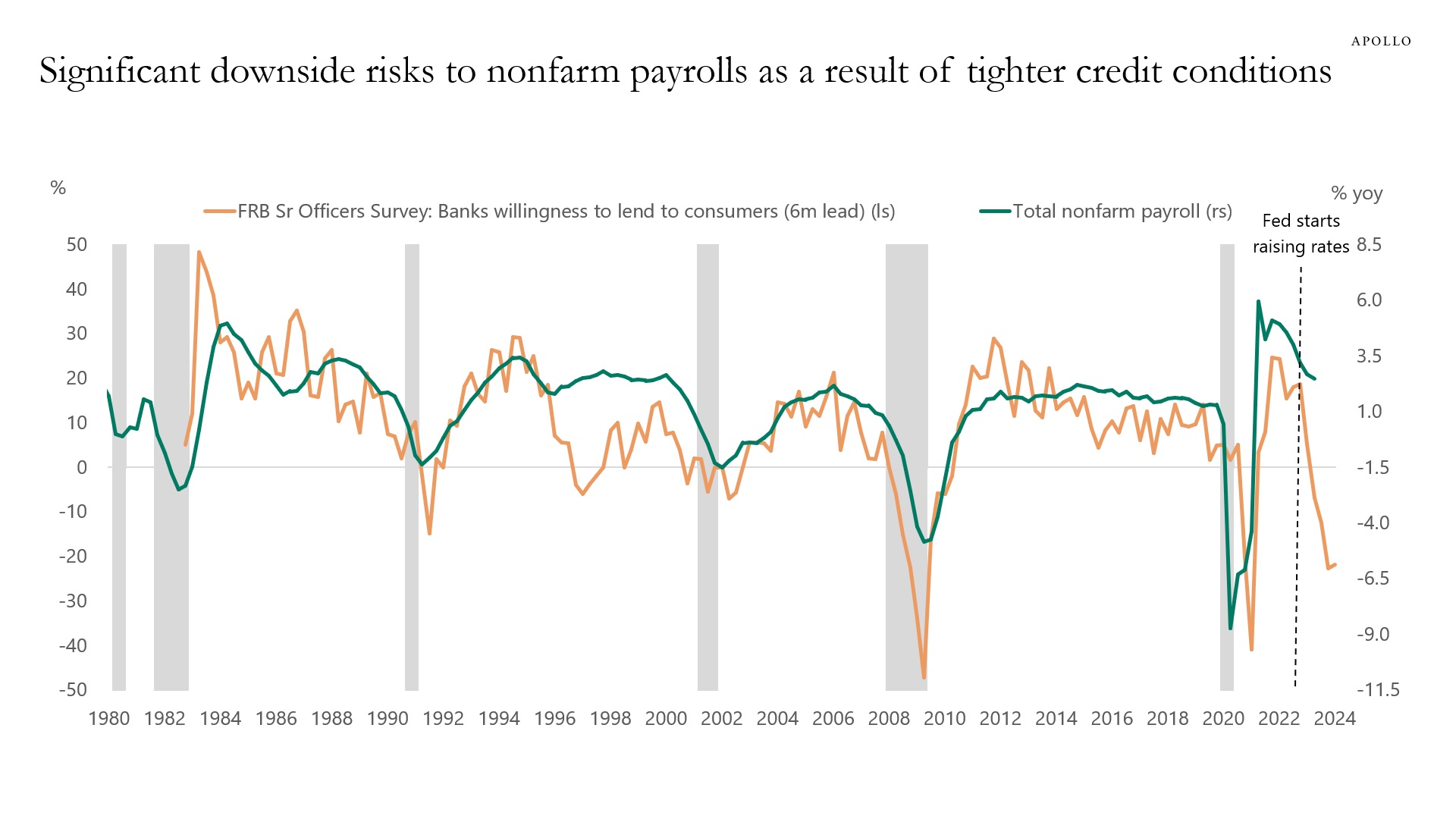

Since the Fed started raising rates, banks are much less willing to lend to consumers, and every day there are more and more consumers who have difficulties getting a credit card, auto loan, or mortgage, see the first chart below.

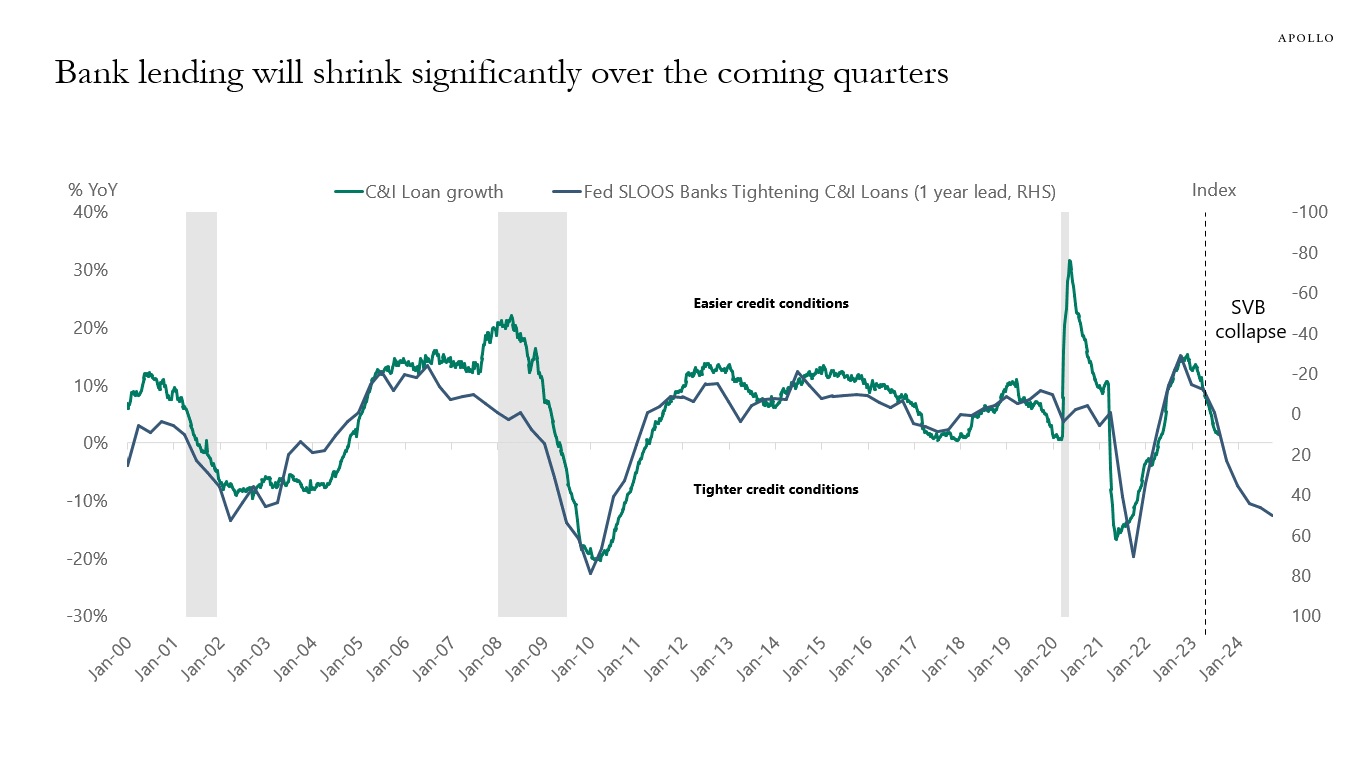

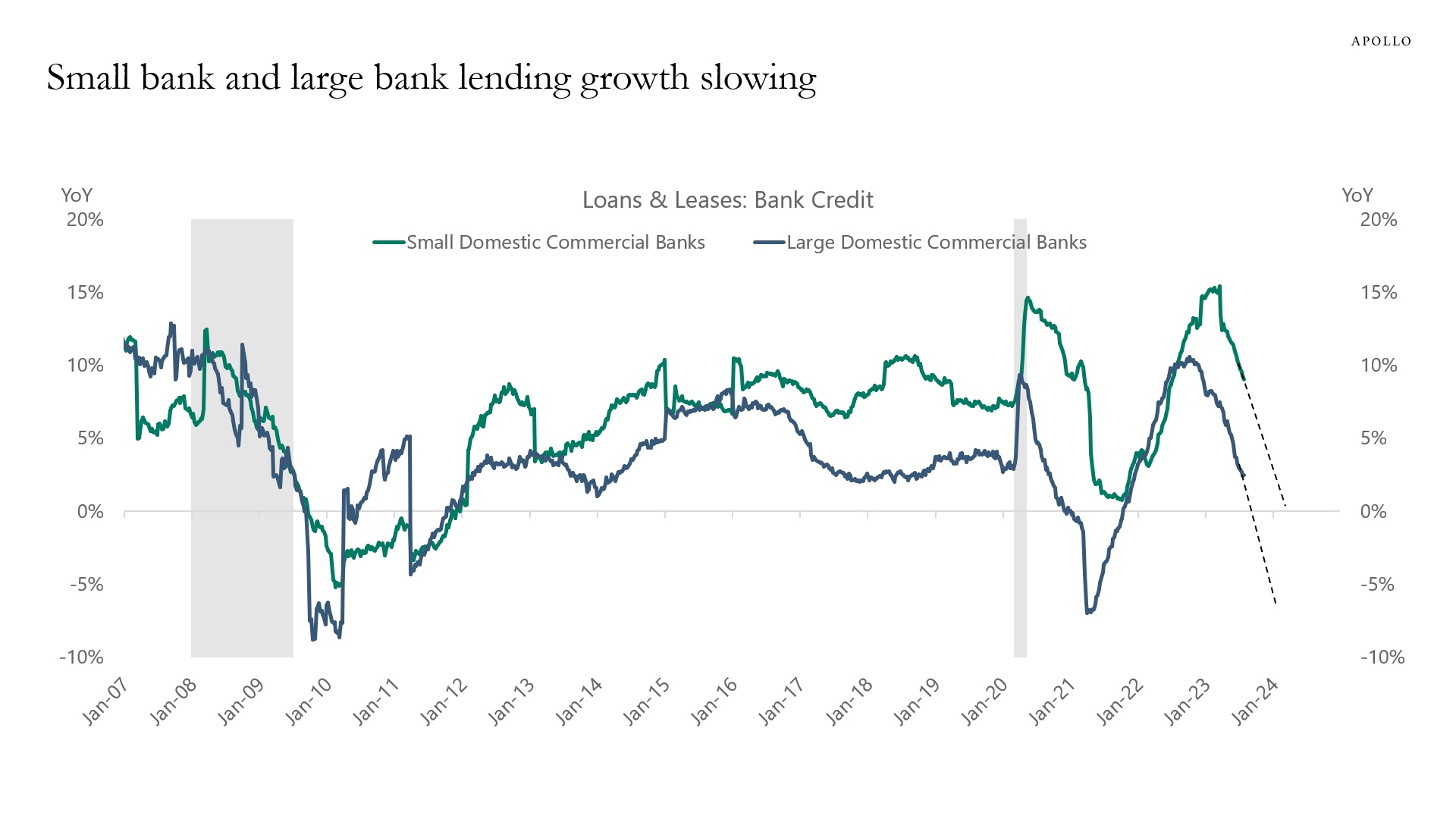

That is how monetary policy works. By raising interest rates, fewer households can borrow, which is why credit growth is slowing rapidly, see the second chart.

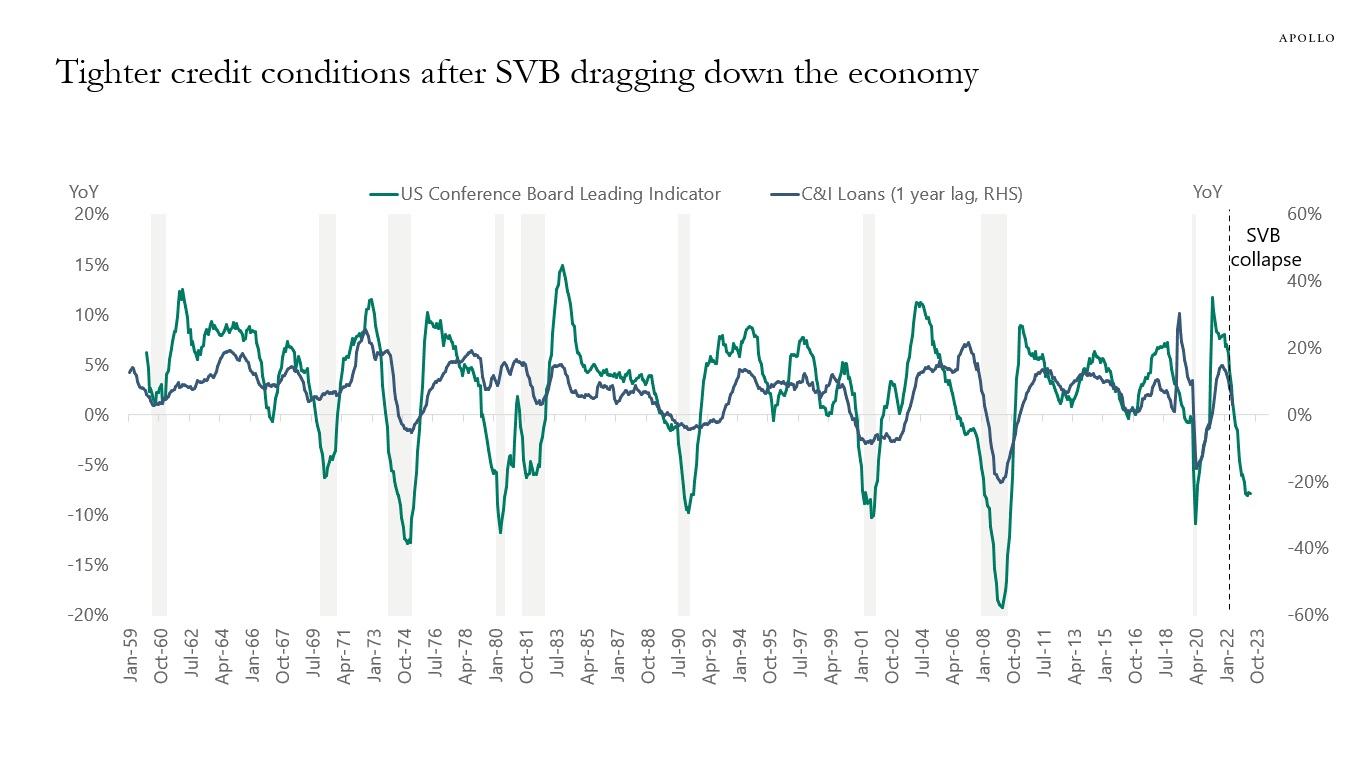

With consumers facing higher interest rates and tighter lending standards, the downside risk to nonfarm payrolls over the coming six months is significant, see again the first chart below.

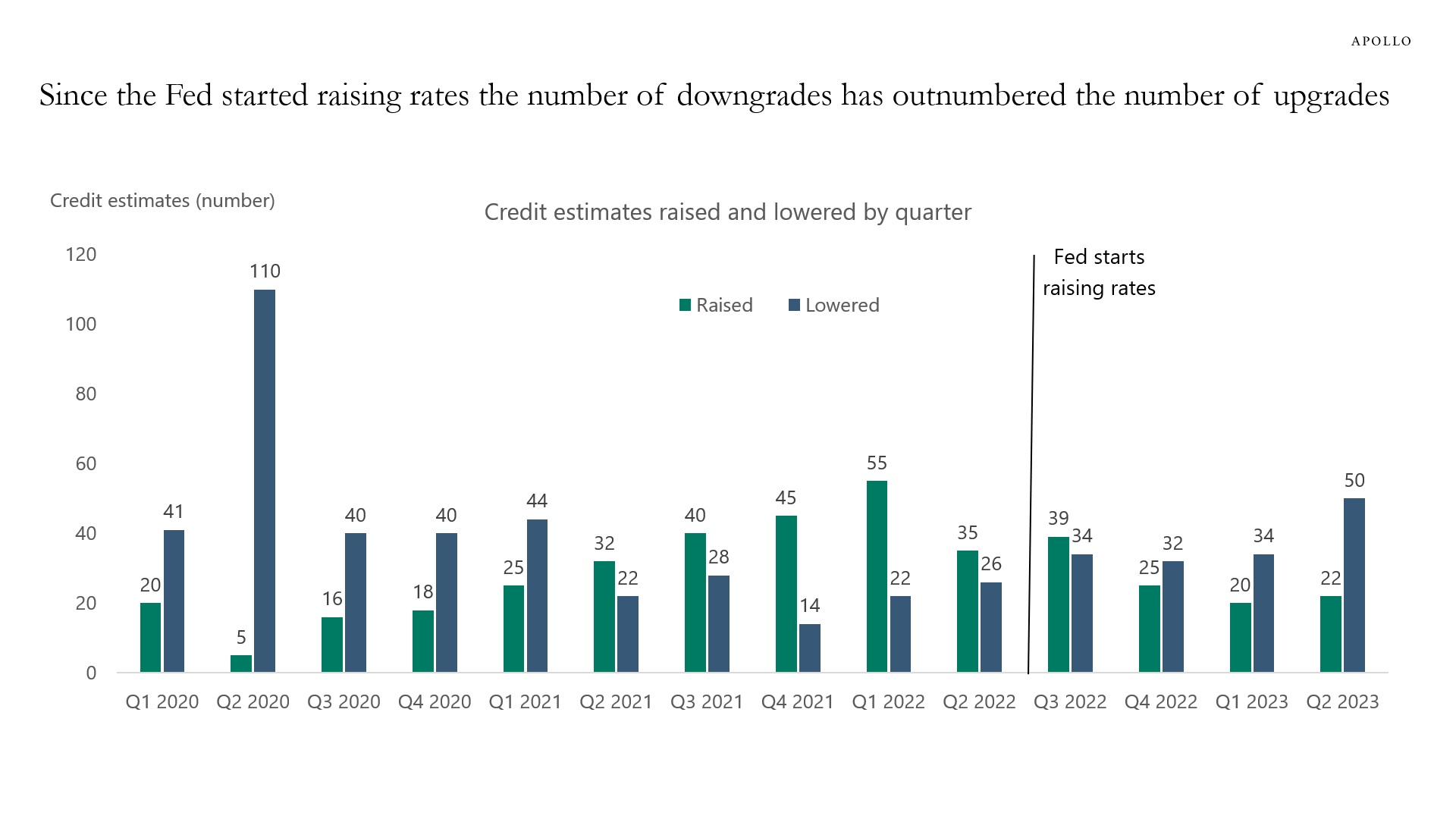

The Fed is trying to slow down the economy to slow down inflation. Specifically, the Fed is trying to slow down hiring, capex spending, and earnings growth.

The tool the FOMC has available is the cost of capital. By raising the cost of capital, the Fed makes it harder for firms to get new loans and to finance existing loans that are maturing.

This monetary policy transmission mechanism first hits companies with high leverage and little or no cash flow, e.g., tech, growth, and venture capital.

This is exactly what is happening at the moment. Companies with high debt and little cash flow are being downgraded, and there are now significantly more downgrades than upgrades, see chart below.

With the Fed funds rate staying at the current level for a couple of years, high cost of capital will continue to create problems for more and more companies characterized by high leverage and low earnings.

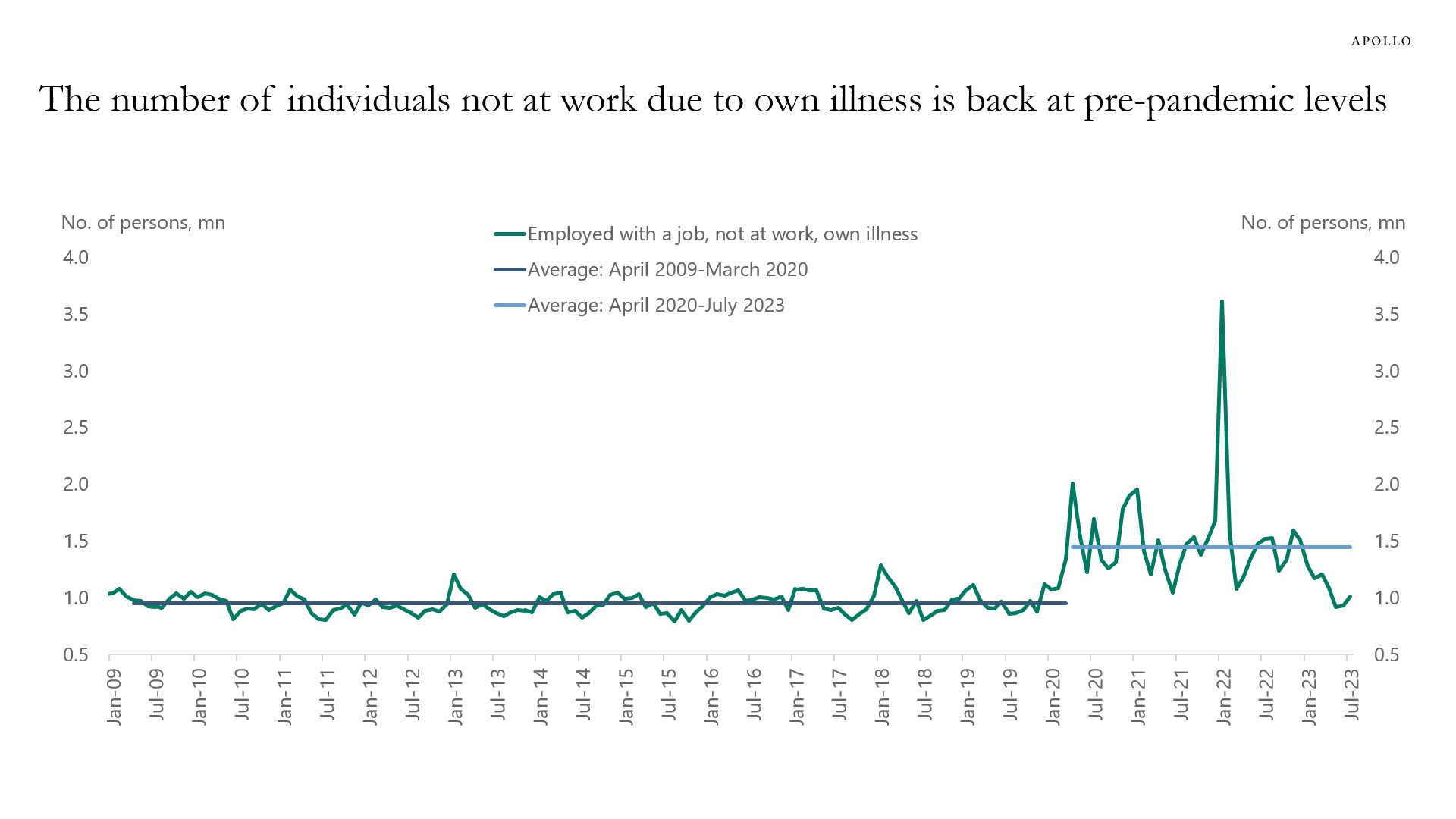

Before the pandemic, the number of workers not at work due to illness was around 1 million people every month. When the pandemic began, this number jumped to 1.5 million. But over the past six months, it has declined back to 1 million, see chart below.

Combined with the normalization in the participation rate and the employment-to-population ratio, the bottom line is that Covid is no longer holding back labor supply.

In other words, the source of strong wage growth has over the past six months shifted from the Covid-induced reduction in labor supply to labor demand. The implication for the Fed is that more demand destruction is needed to get wage inflation under control.

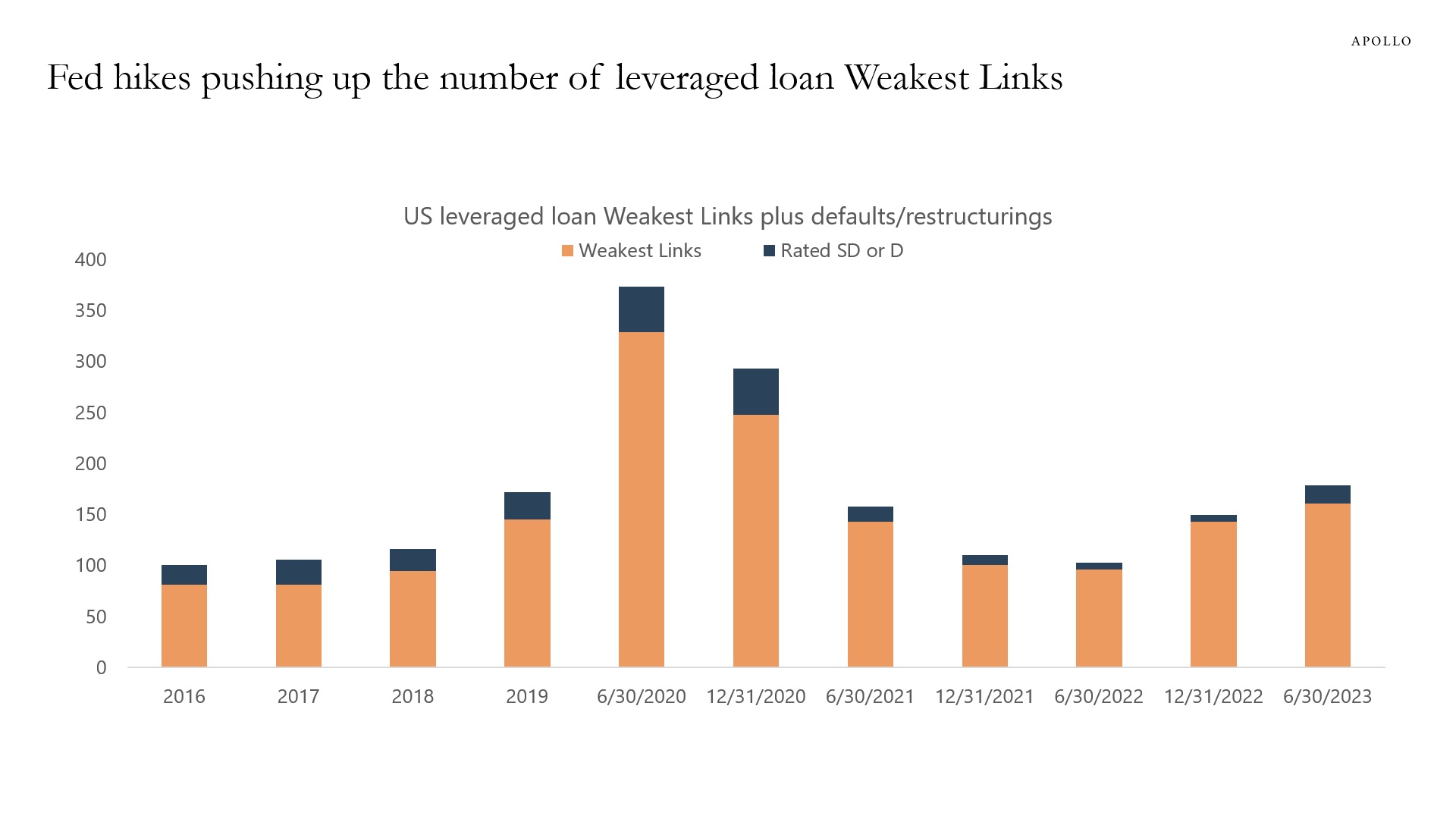

Weakest Links are loan issuers rated B-minus or lower with a negative outlook.

The number of US leveraged loan Weakest Links continues to increase, driven by higher costs of capital and costlier financing terms, see chart below.

This is how monetary policy works. Higher cost of capital makes it harder for more vulnerable companies to get financing.

The costs of capital have increased because of Fed hikes and tighter credit conditions. As a result, there are firms every day that cannot get a new loan or refinance their maturing loan.

This is how monetary policy works. Higher costs of capital slow down financings and, ultimately, growth and inflation.

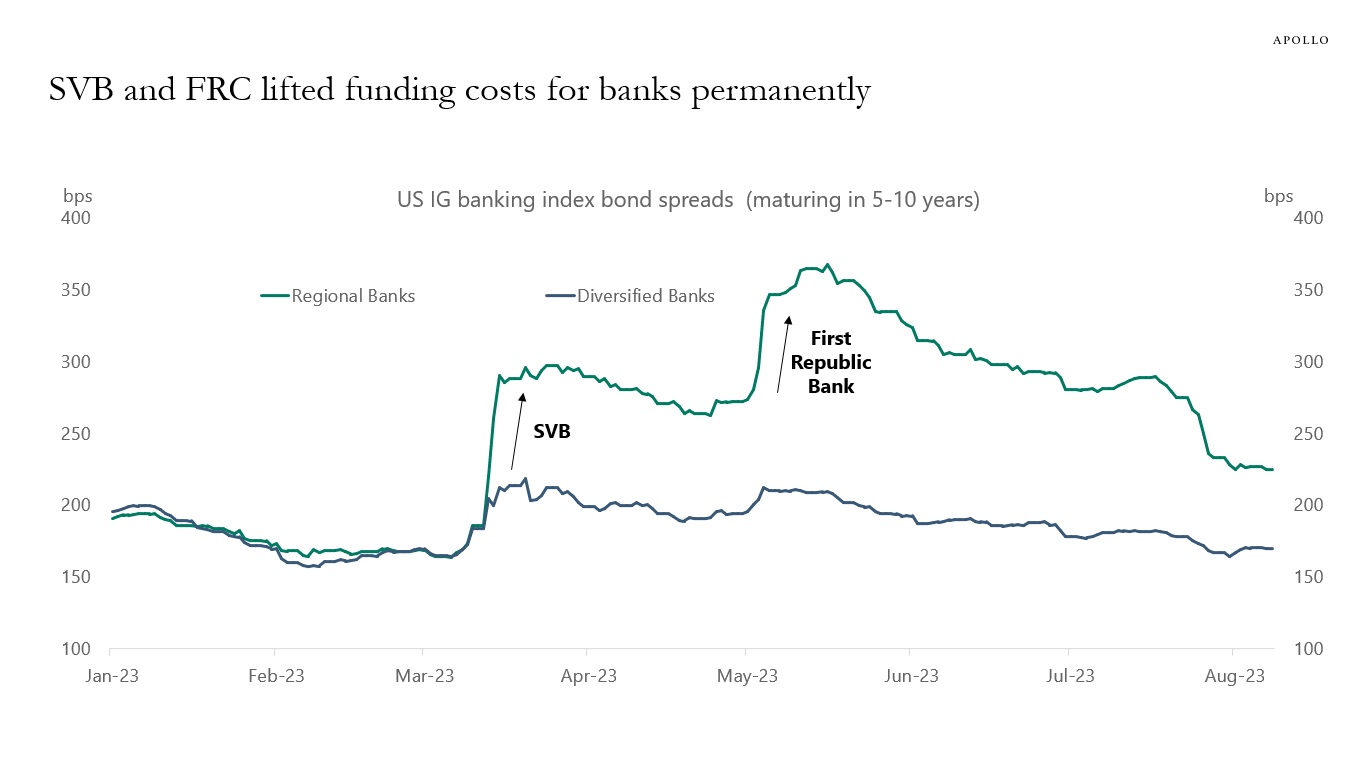

With the Fed saying that interest rates will stay high for “a couple of years,” this process will continue to slow down the economy. Our outlook for regional banks is available here and documents current trends in detail.