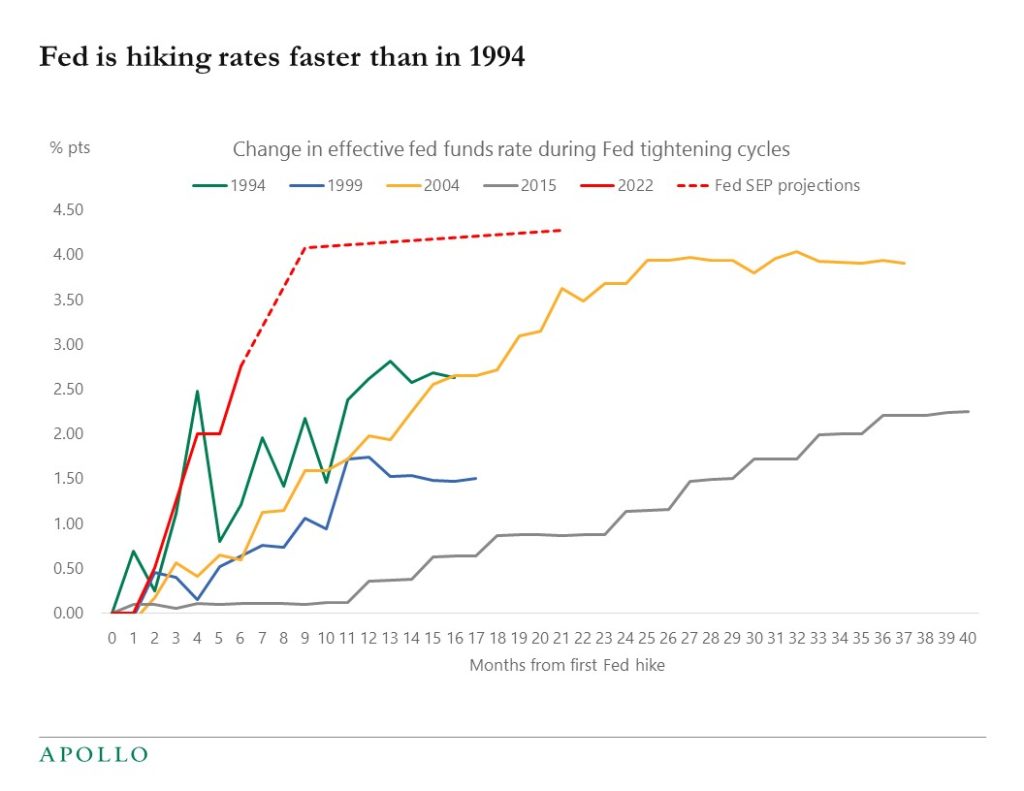

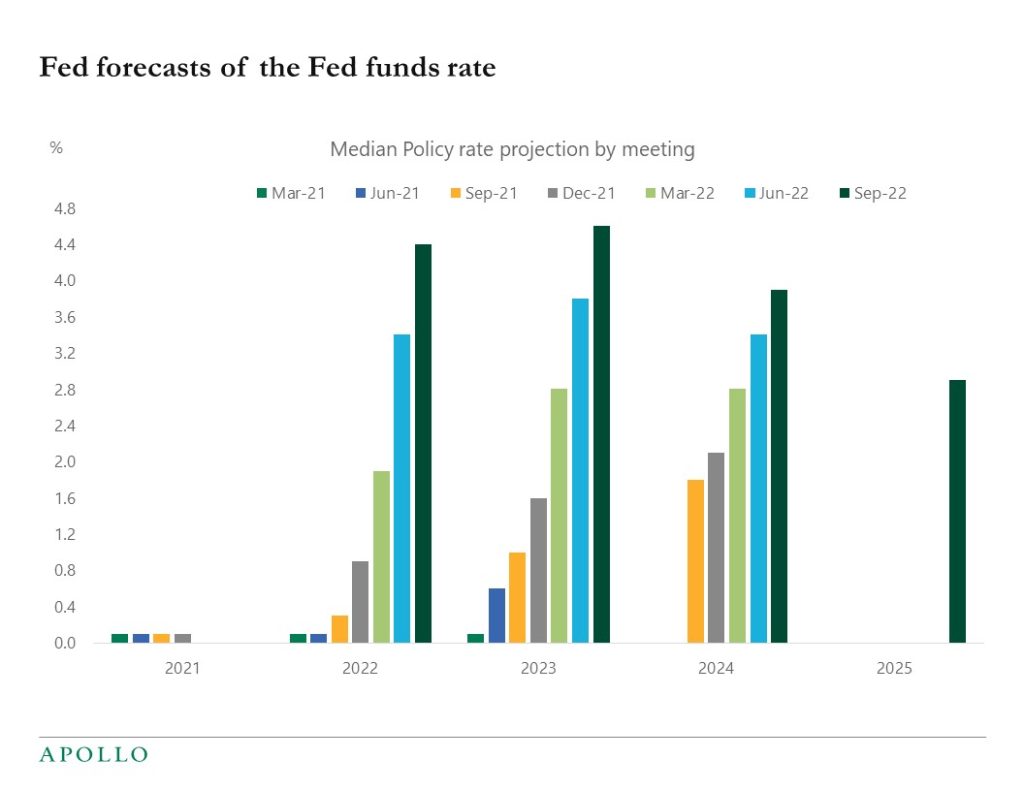

The 1994 Fed hiking cycle is often mentioned as a very unusual period, but in 2022 the FOMC has increased interest rates faster and more than during the 1994 episode, and the FOMC expects this to be the biggest percentage point increase in the Fed funds rate in recent history, see chart below. Inflation is 8.3% and the FOMC’s inflation target is 2%. The Fed is trying to cool down the economy by tightening financial conditions, i.e. by pushing rates higher, credit spreads wider, and stocks lower. Investors should be positioned accordingly.