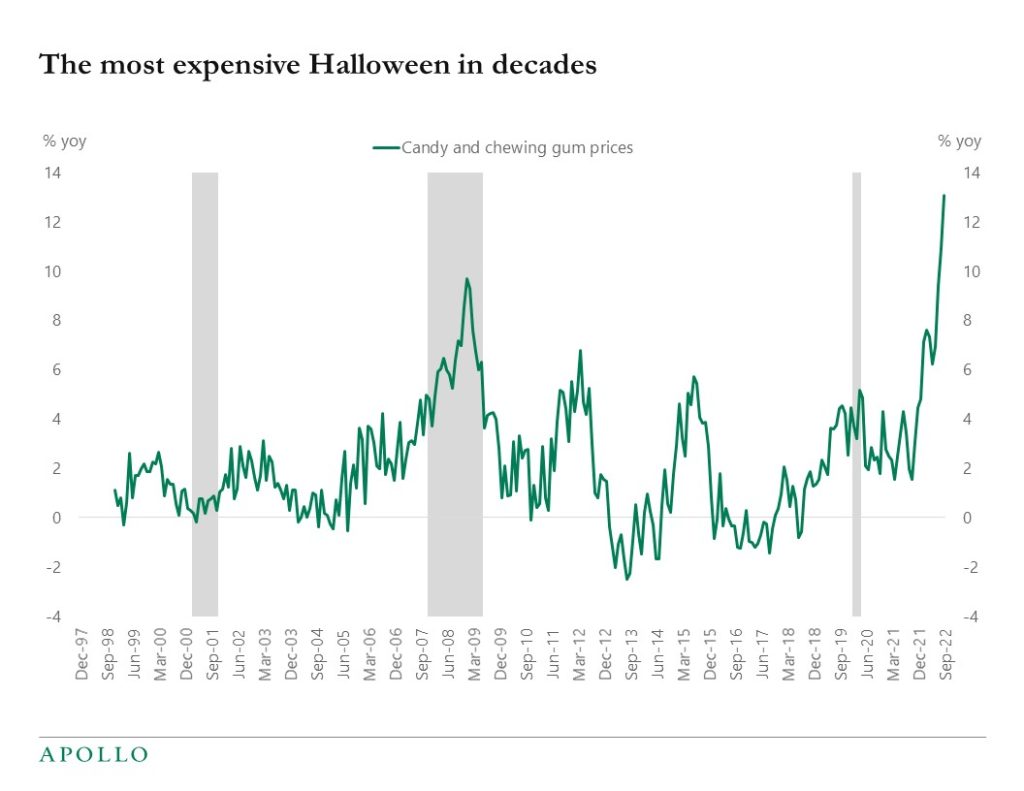

The price of candy and chewing gum has increased 13% over the past year, see chart below.

The price of candy and chewing gum has increased 13% over the past year, see chart below.

Last week PCE headline inflation came in at 6.2%, slightly better than expected but still much higher than the Federal Reserve’s 2% inflation target. In the week ahead we will be tracking data from the October employment report. The consensus expects non-farm payrolls to come in at 200,000 jobs (vs. 263,000 jobs in September) and for the unemployment rate to rise slightly to 3.6%. The goods sector—which encompasses housing, car sales, and durable goods (in other words: purchases that often require financing)—is showing signs of slowing down. However, it’s a completely different story in the services sector, which makes up about 80% of GDP. There, we are seeing solid growth across the board—from air travel and hotel bookings to the number of consumers eating in restaurants and going to Broadway shows. The bottom line is that the overall economy is still relatively strong and consumer services in particular continue to show robust growth. As such, we can expect to see more interest rate hikes from the central bank.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.

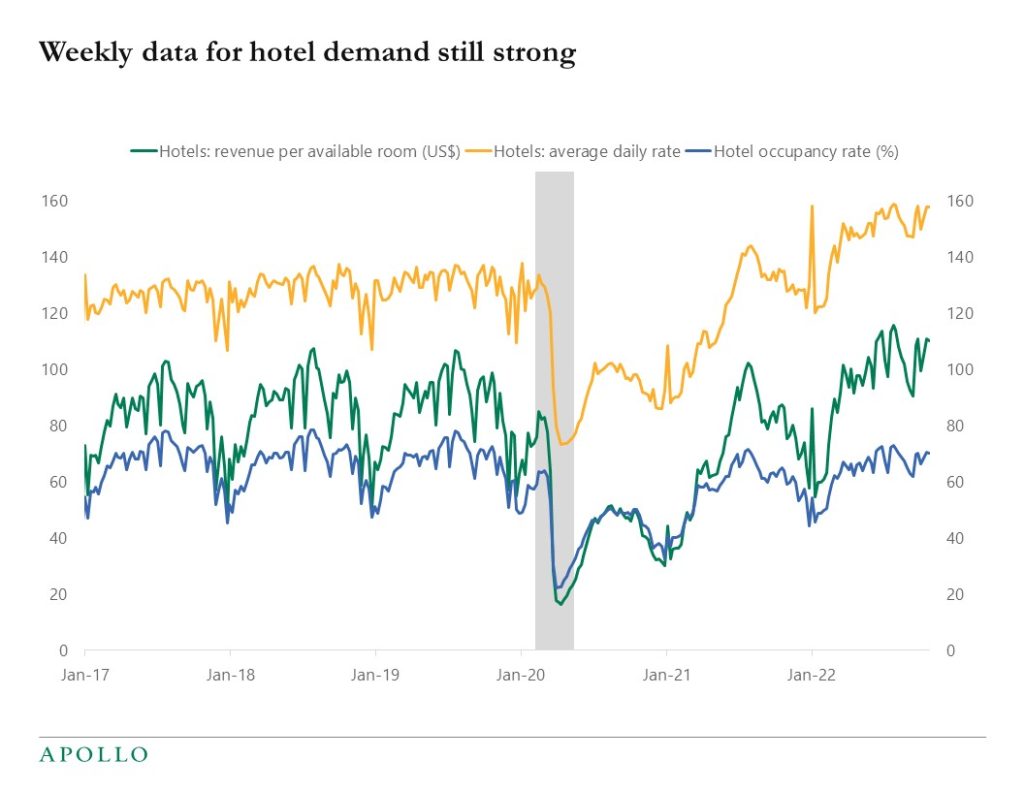

Weekly data shows that hotel demand is still very strong, see chart below. Our collection of daily and weekly indicators for the US economy is available here.

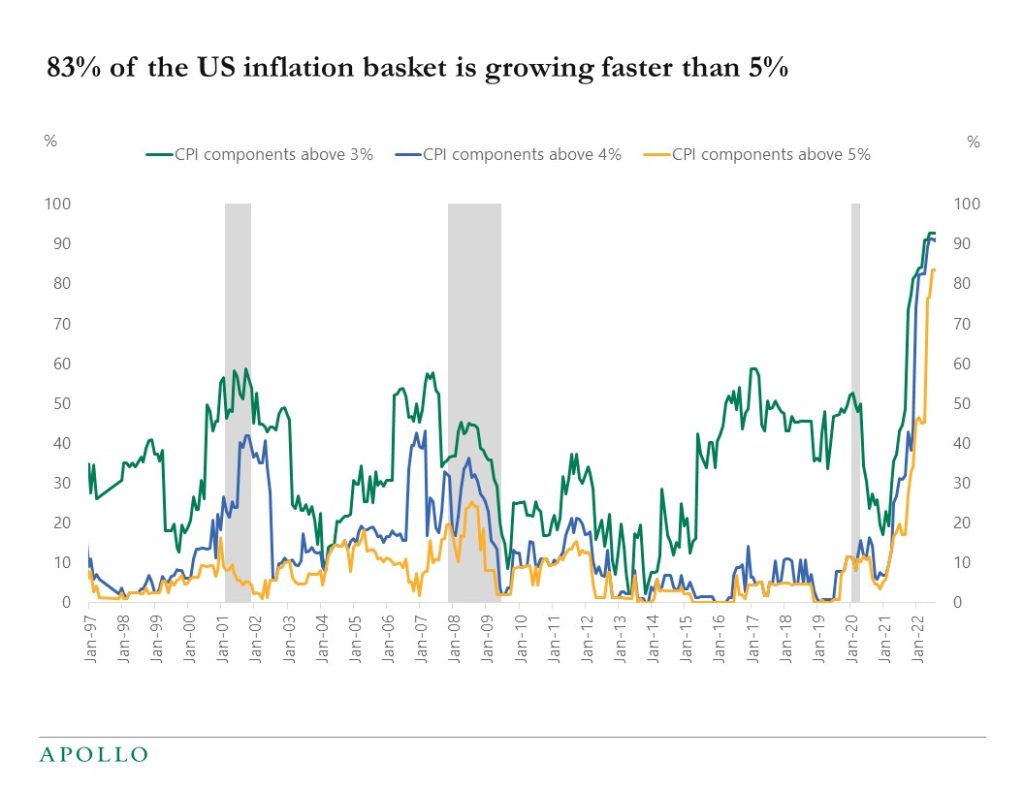

The FOMC’s inflation target is 2%, and 83% of the components in the CPI basket are growing faster than 5%. Inflation is, unfortunately very broad-based, see chart below.

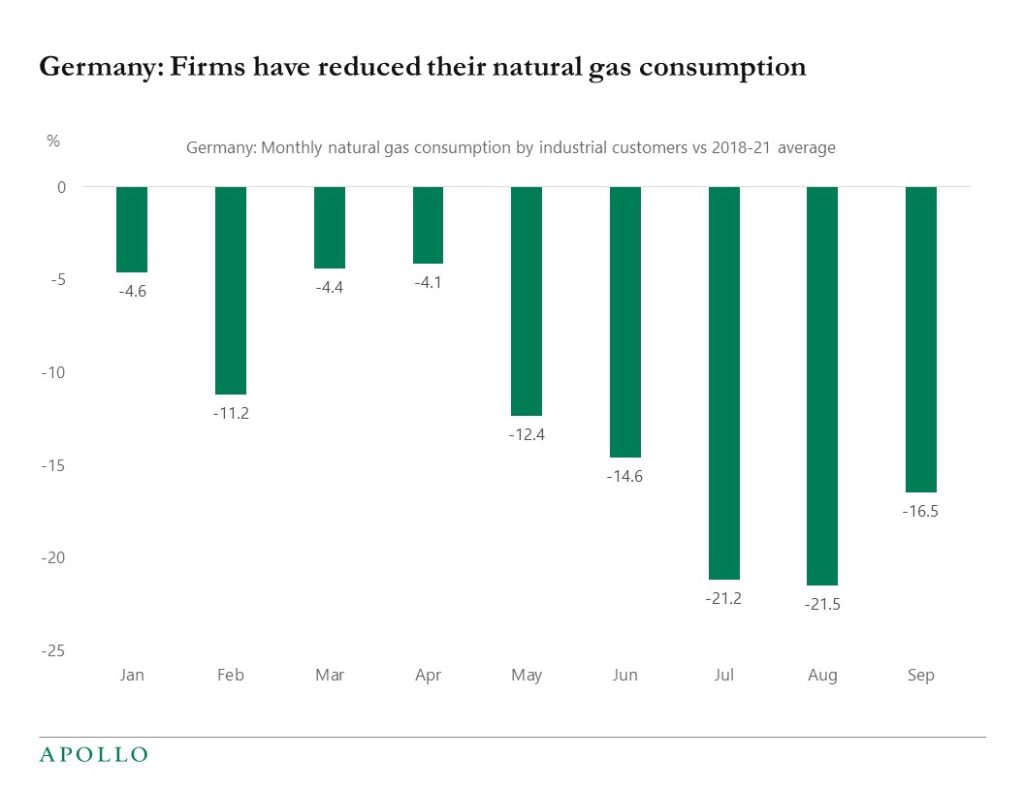

Firms in Germany are reducing their consumption of natural gas. The reduction is driven by slowing economic growth in Europe and substitution toward other sources of energy.

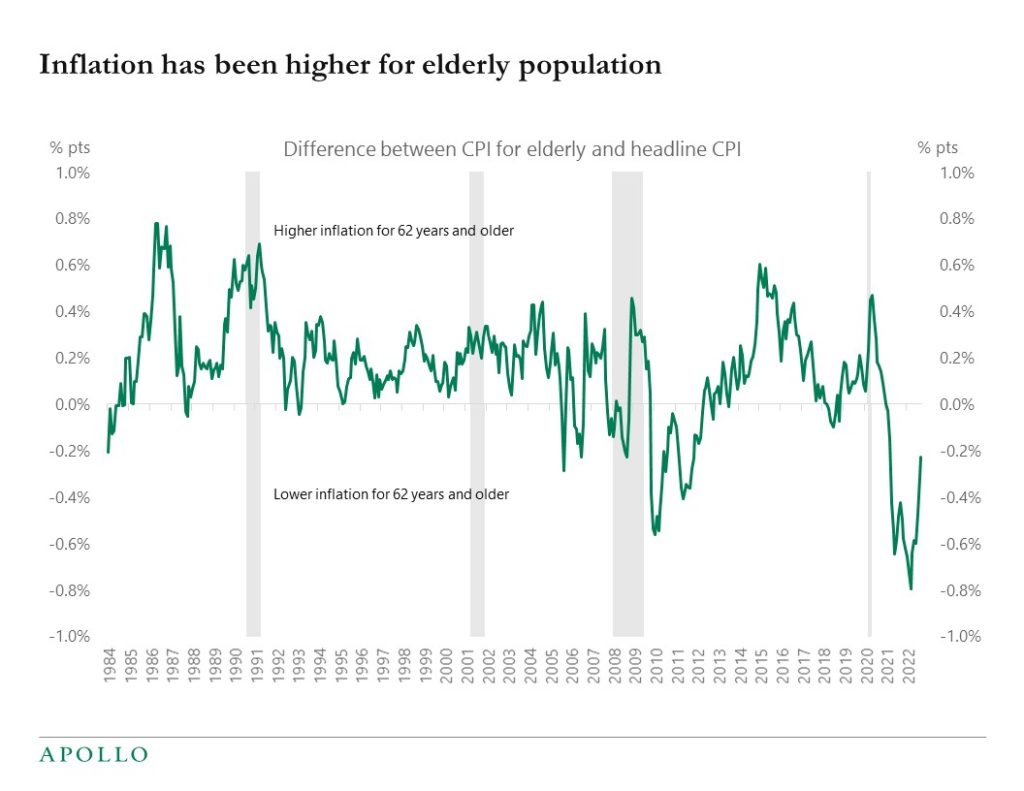

The CPI index used by the Fed and financial markets captures the spending habits of about 80 percent of the population of the United States. But spending patterns vary across different age groups. For example, older generations spend more on services such as housing and medical care, and less on goods including food, beverages, and apparel.

To better understand these differences in spending patterns, the BLS calculates a CPI index looking at inflation for people age 62 and above. It shows that for older generations, inflation has for decades been higher because of higher inflation in services. But during the pandemic, when inflation on goods was very high, inflation for people age 62 and above has been relatively lower. With goods inflation coming down and service sector inflation still rising, we should expect more convergence between the two inflation measures going forward, a process which has already started in the chart below.

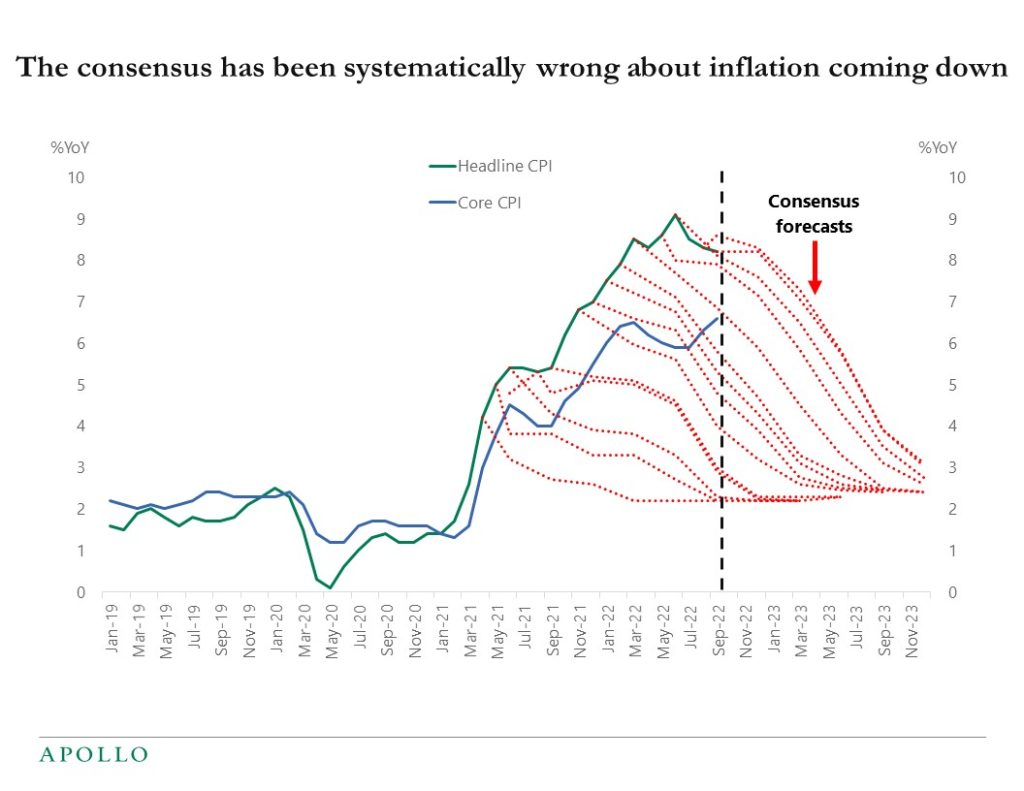

Inflation will be coming down over the coming quarters. This is what the Fed is predicting, that is what the consensus is expecting, and that is what we are predicting. The problem is that this has been the forecast ever since inflation started going up in April 2021, see chart below. Given how systematically wrong inflation forecasts have been over the past 18 months, there are good reasons to be cautious about the current forecast.

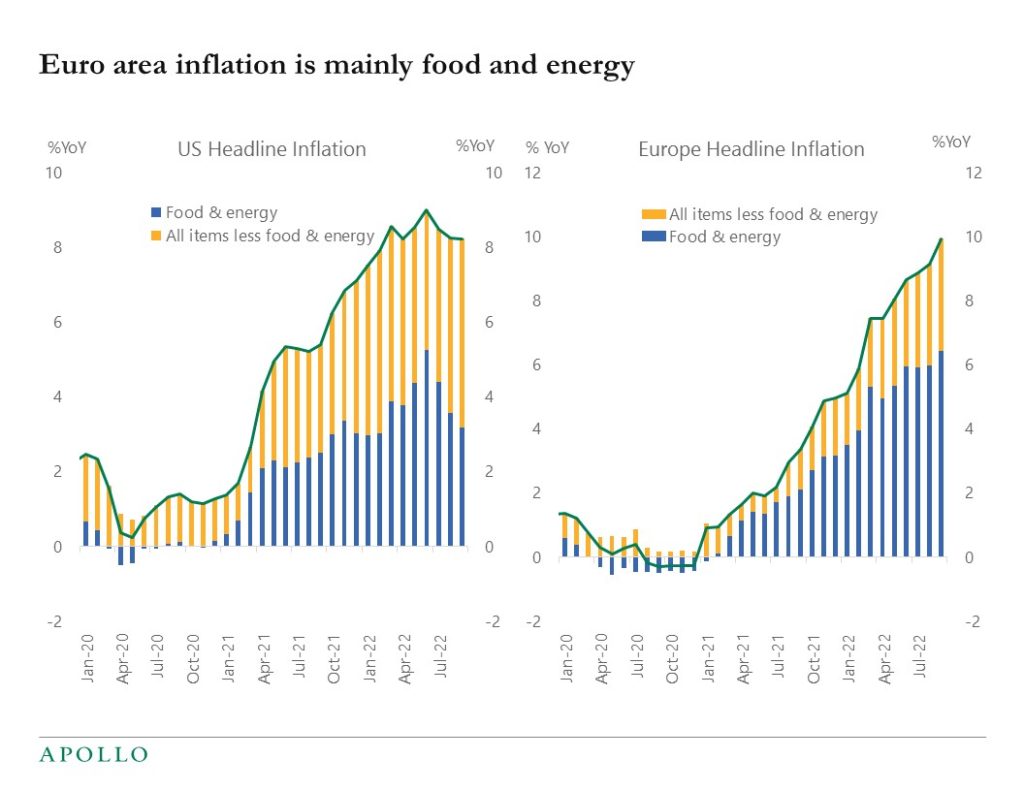

The Fed will remain hawkish for longer than the ECB because European inflation is mainly driven by food and energy, see chart below. This is in contrast to US inflation, which is driven primarily by higher core inflation, see again the chart below.

Each Thursday, new jobless claims are released and last week’s report saw a drop in the number of people applying for unemployment benefits. This is consistent with the picture we’ve seen in the labor market over the last several months. Although job openings have slightly declined, there still remains a substantial amount of job openings per unemployed individuals. This week, we will be tracking the release of PCE inflation data, which is expected to show slight increases both at the core and headline levels. The bottom line from a markets perspective is the economy is still quite strong, and the labor market remains tight—leaving the Fed with no choice but to continue with aggressive interest rate hikes. The timing for when inflation will begin to fall remains uncertain, and consensus projections have consistently underestimated the duration of elevated inflation.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.