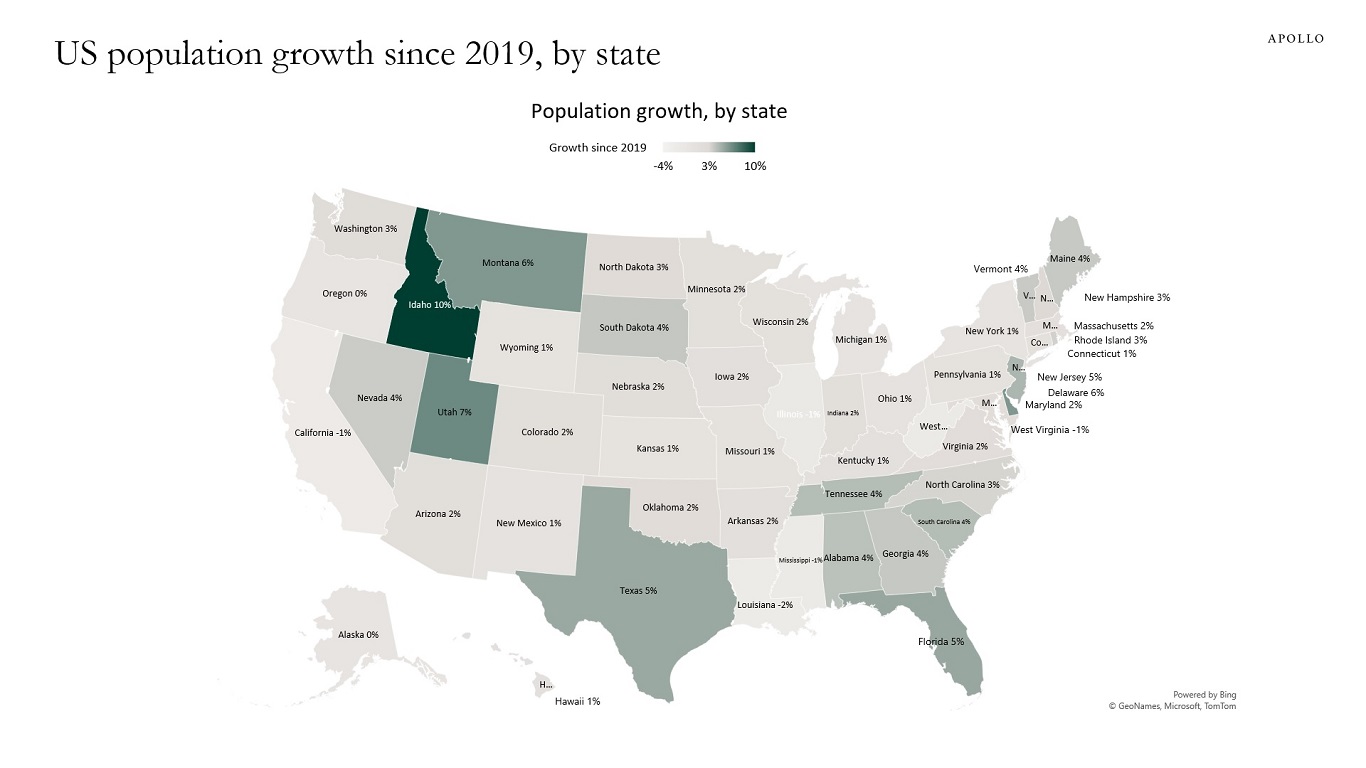

During the post-Covid period, US population growth has been the fastest in Idaho, Utah, Montana, Texas, Florida, and New Jersey, see map below.

During the post-Covid period, US population growth has been the fastest in Idaho, Utah, Montana, Texas, Florida, and New Jersey, see map below.

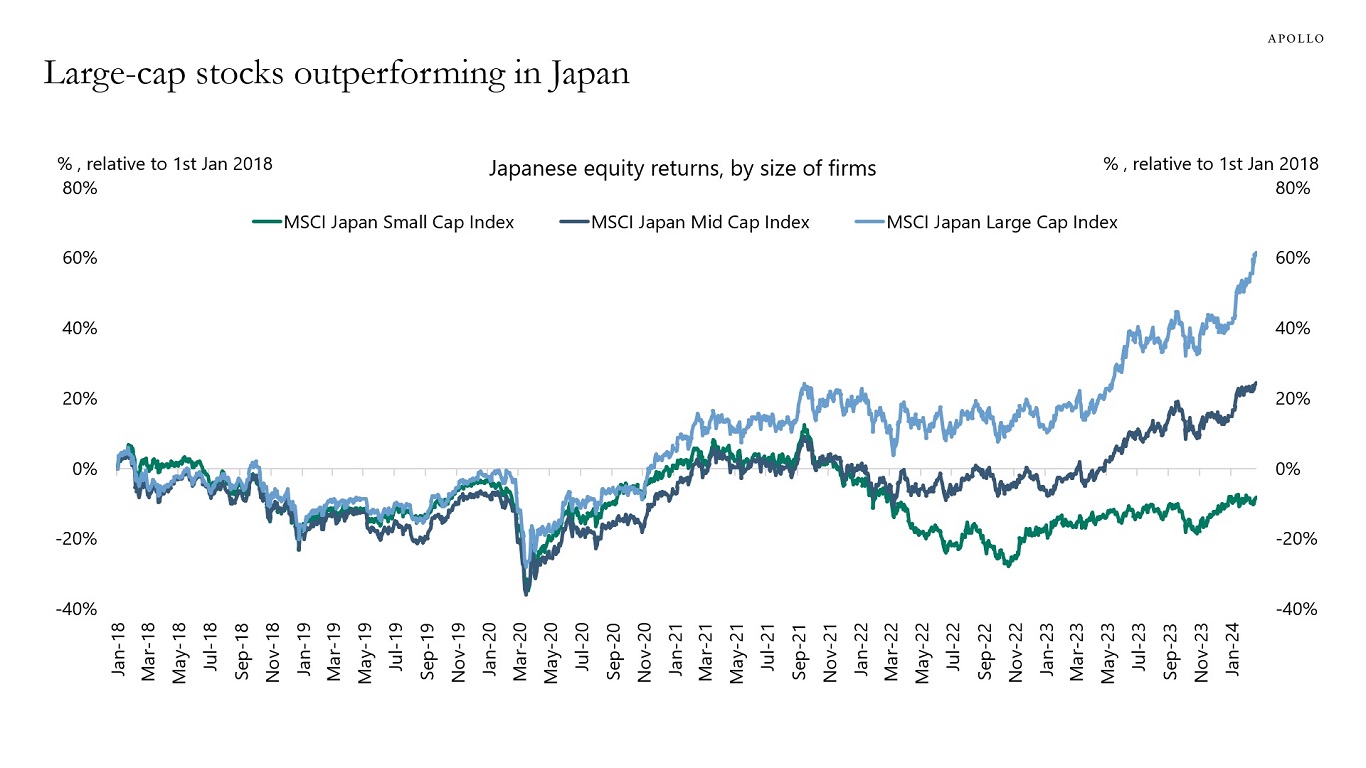

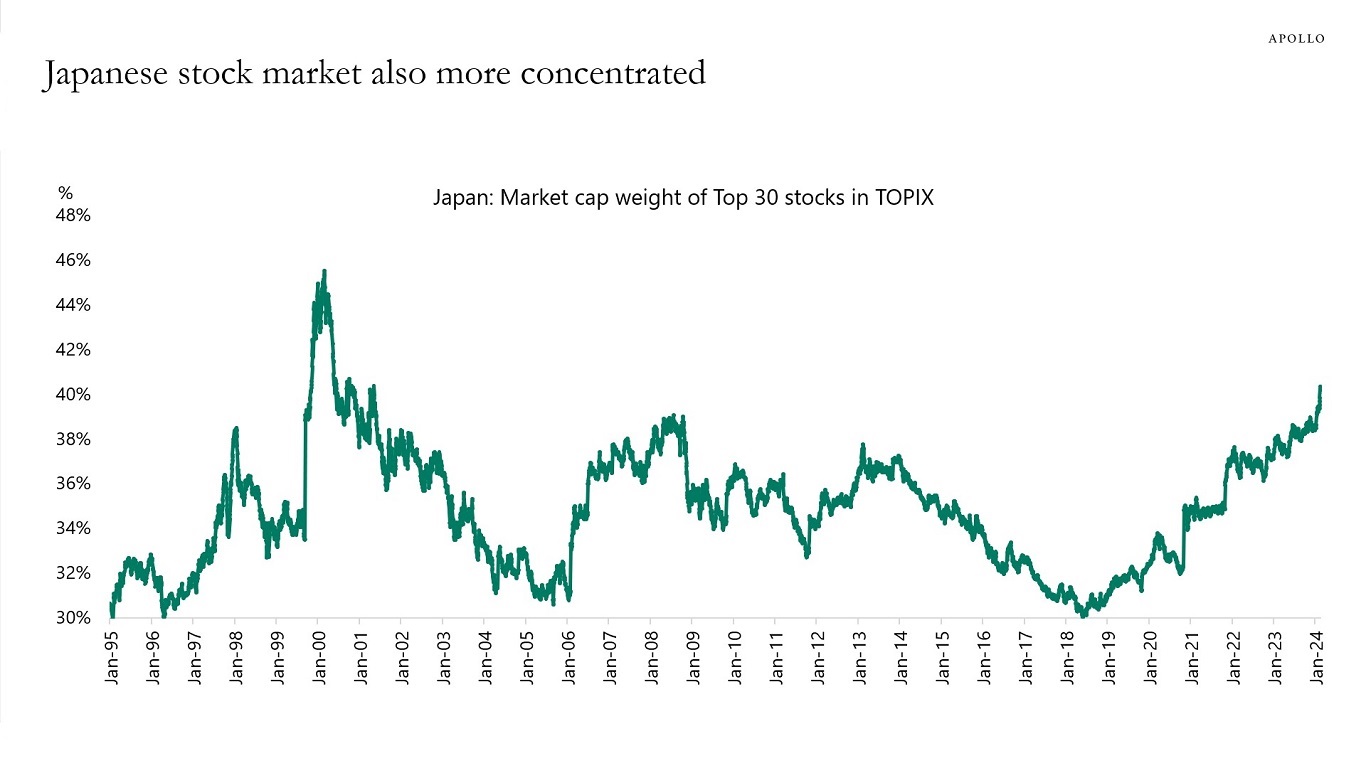

The global rise in stock prices is driven mainly by large-cap firms, not only in the US and Europe but also in Japan, see charts below.

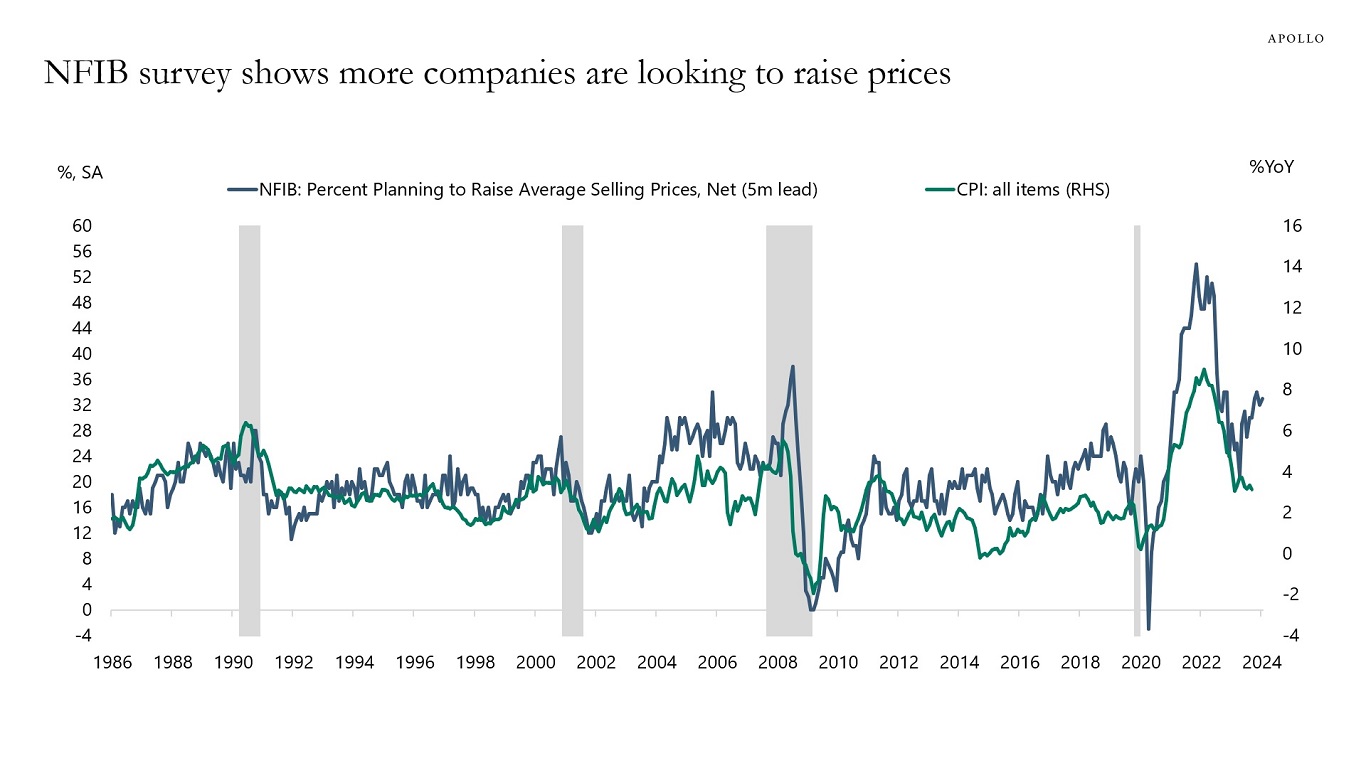

The NFIB survey of small businesses asks 10,000 firms if they plan to increase selling prices over the next three months. The recent acceleration in the share of firms saying yes suggests that CPI inflation could increase over the coming months, see chart below.

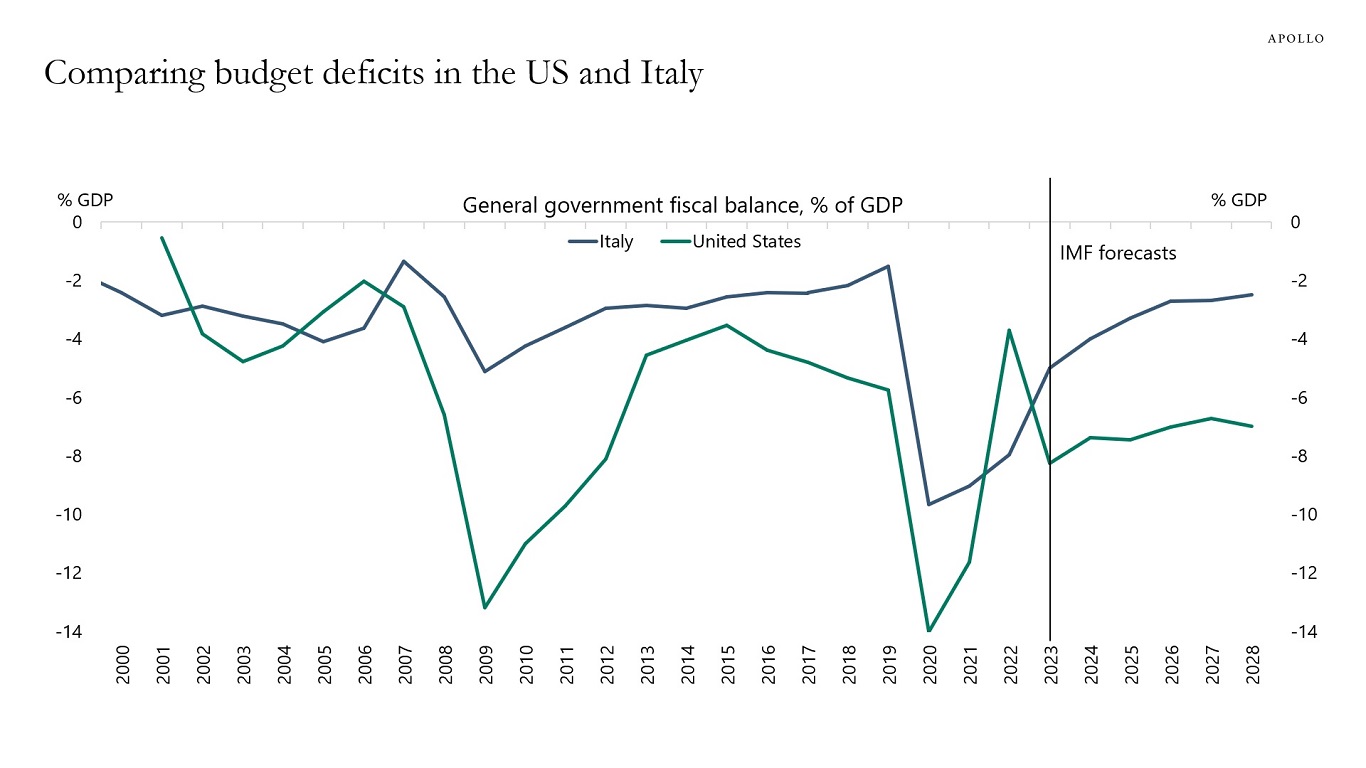

The government budget deficit is bigger in the US than in Italy, see the first chart.

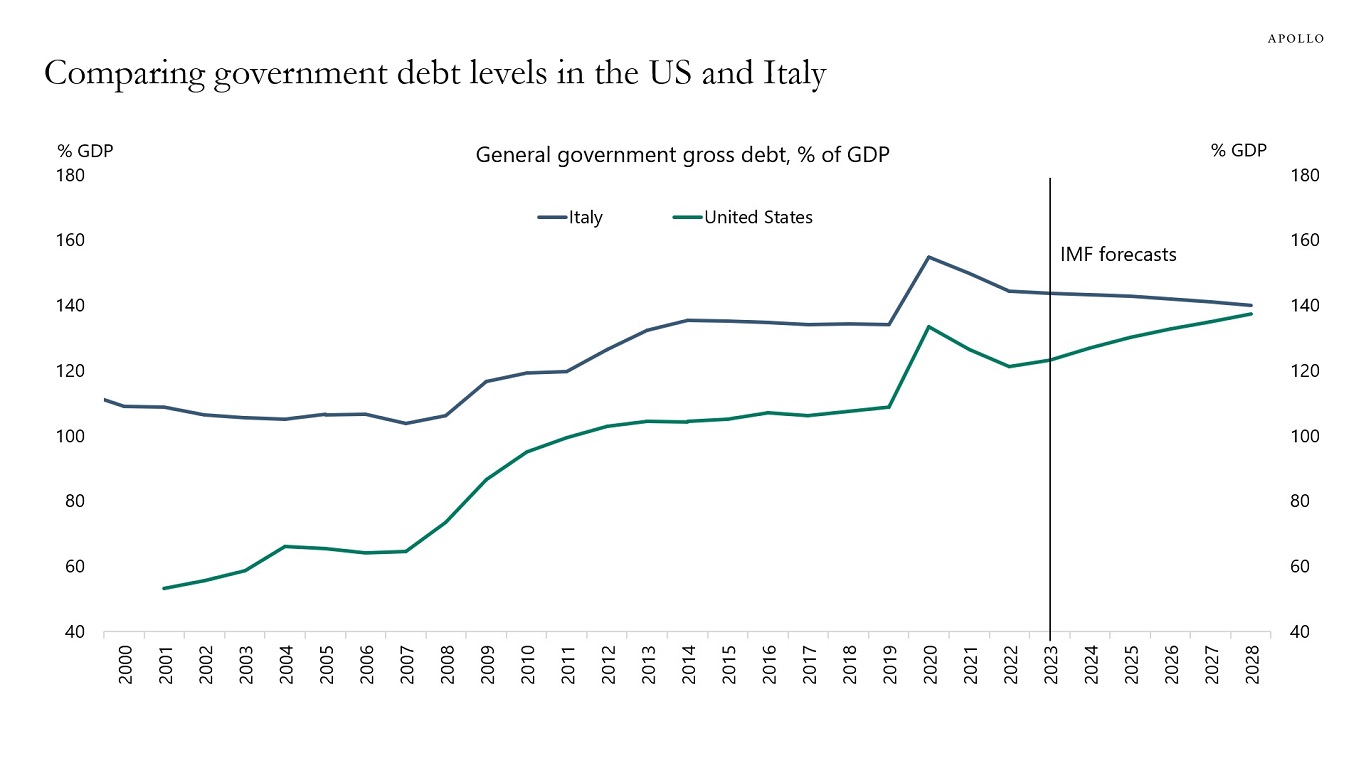

Government debt levels are currently higher in Italy than in the US, but according to IMF forecasts, they are converging over the coming years, see the second chart.

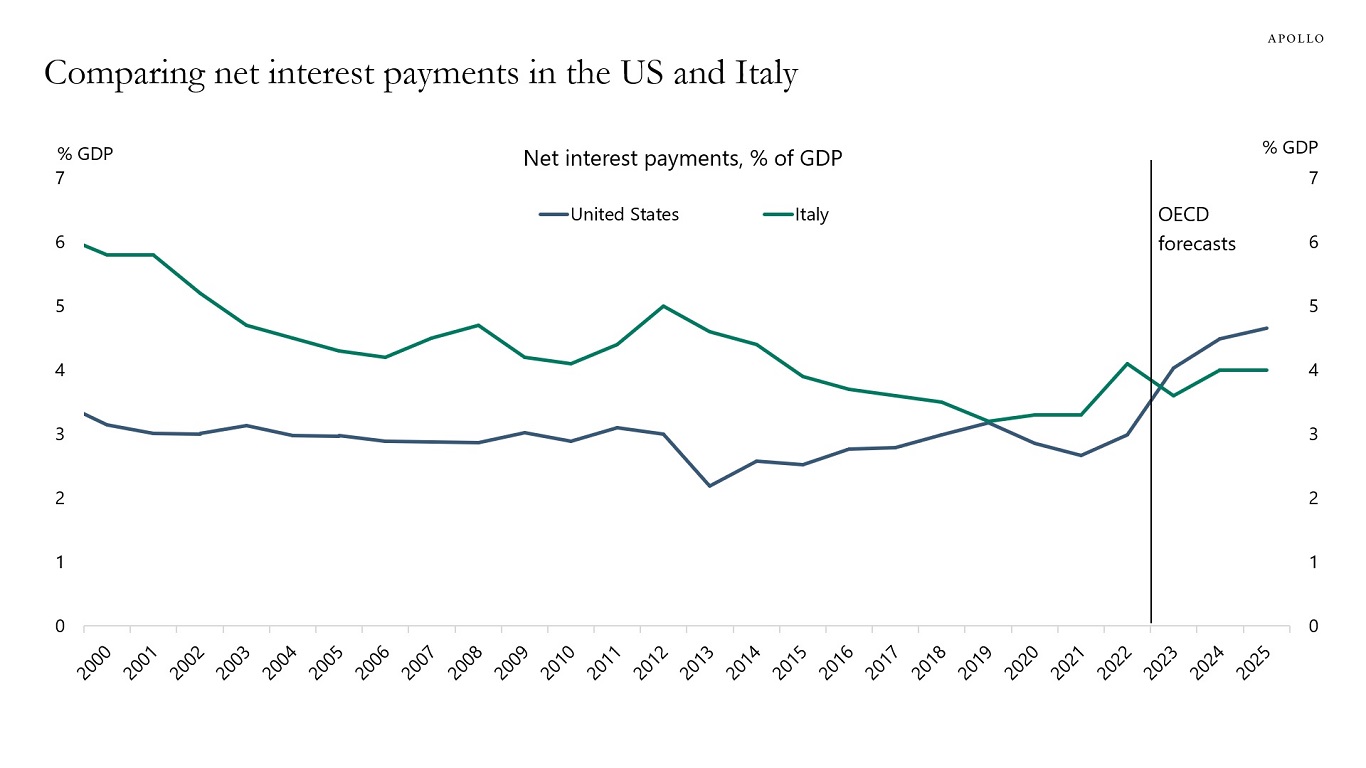

Government net interest payments are similar in the US and Italy, see the third chart.

Despite these similarities, Italy has a BBB rating, and the US has a AAA rating.

If the US continues on the fiscal trajectory forecasted by the CBO, the risks are rising that the US will be downgraded later this year.

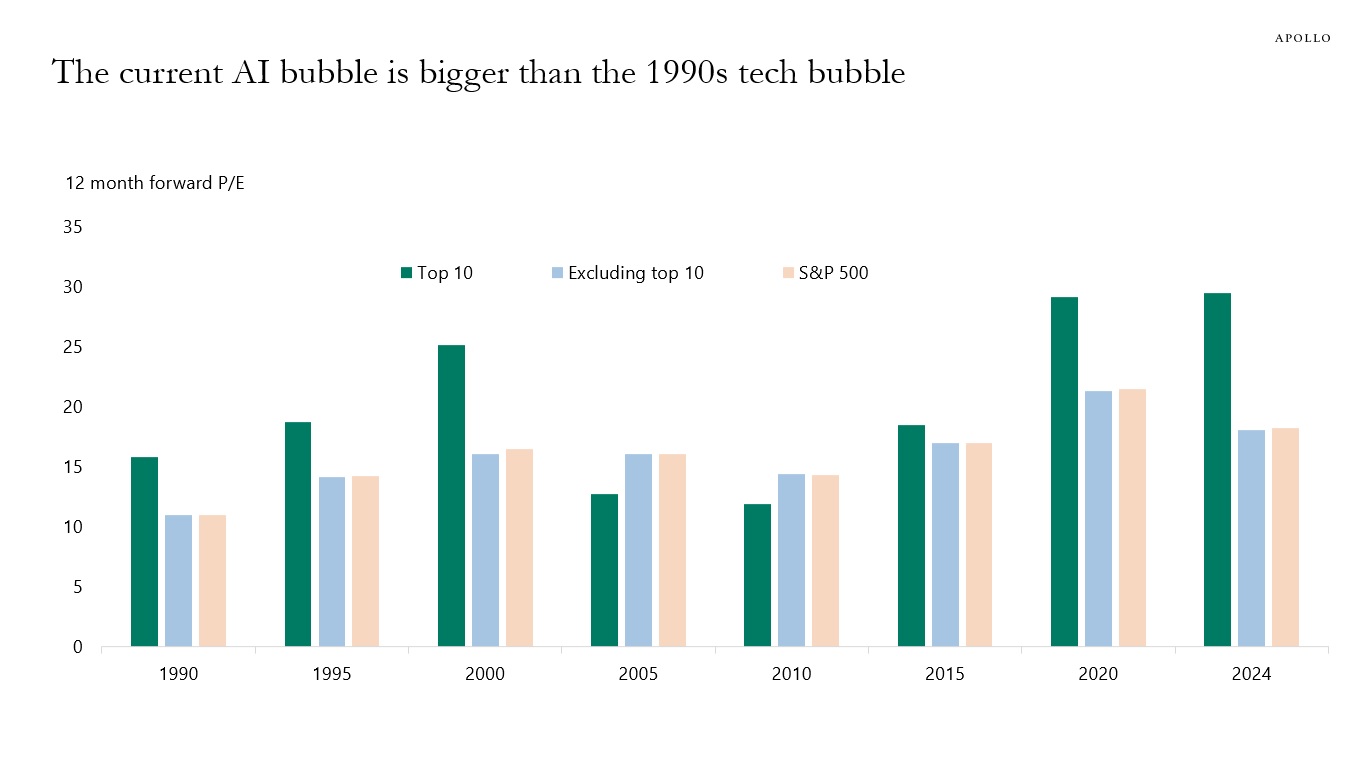

The top 10 companies in the S&P 500 today are more overvalued than the top 10 companies were during the tech bubble in the mid-1990s, see chart below.

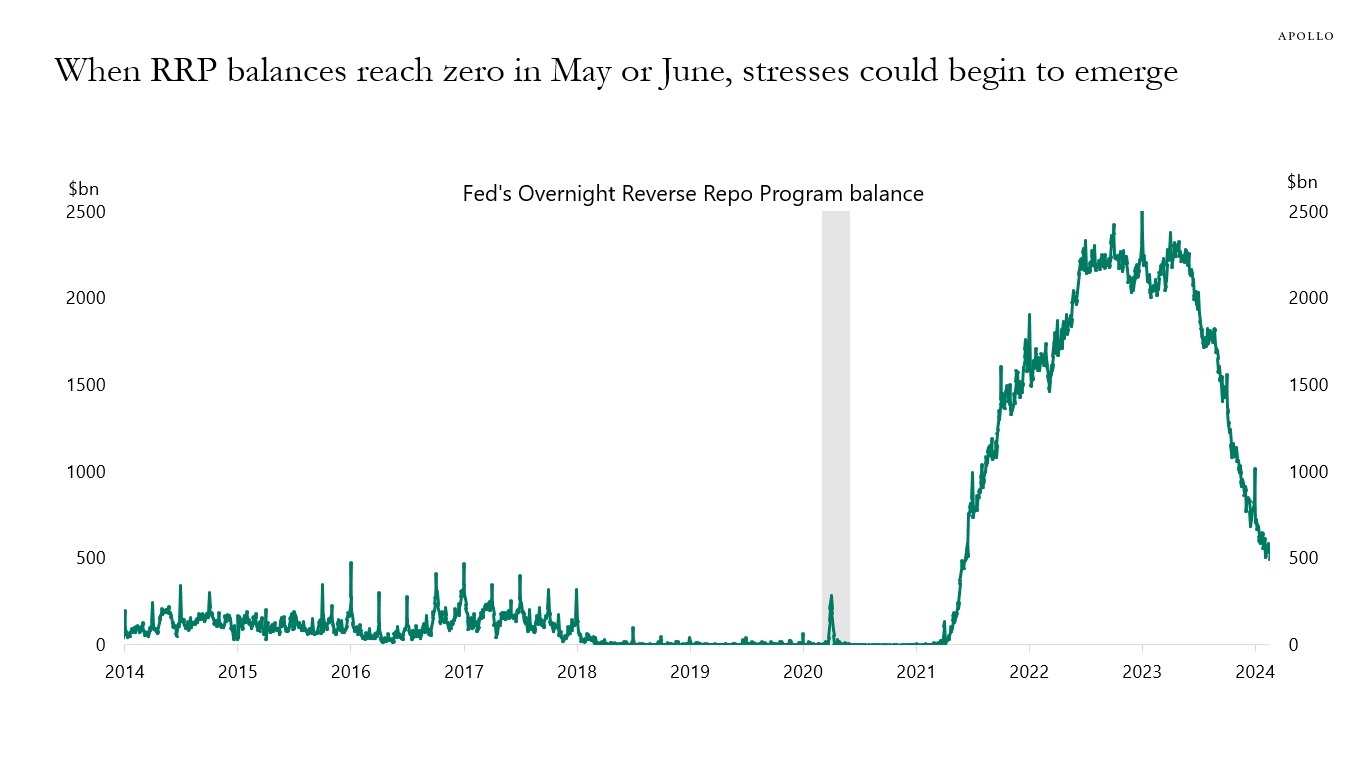

The Fed’s Reverse Repo Program (RRP) is a measure of excess reserves in the banking sector. If banks have excess cash, RRP balances go up and vice versa.

With Fed cuts on the horizon, there is an emerging debate about what will happen once RRP balances reach zero, in particular if QT continues, see chart below.

The worry is that once there are no longer abundant reserves in the banking sector, then reserves will be scarce, and the consequences could be less support for T-bills, duration, and credit markets, or stresses in money markets similar to what we saw in September 2019.

The bottom line is that credit investors should keep an eye on RRP balances because as they are depleted, we will find out if reserves in the banking sector are scarce, abundant, or ample.

In short, once RRP reaches zero in May or June, there may no longer be abundant reserves in the banking sector, which increases the probability of an accident somewhere in the plumbing of the financial system.

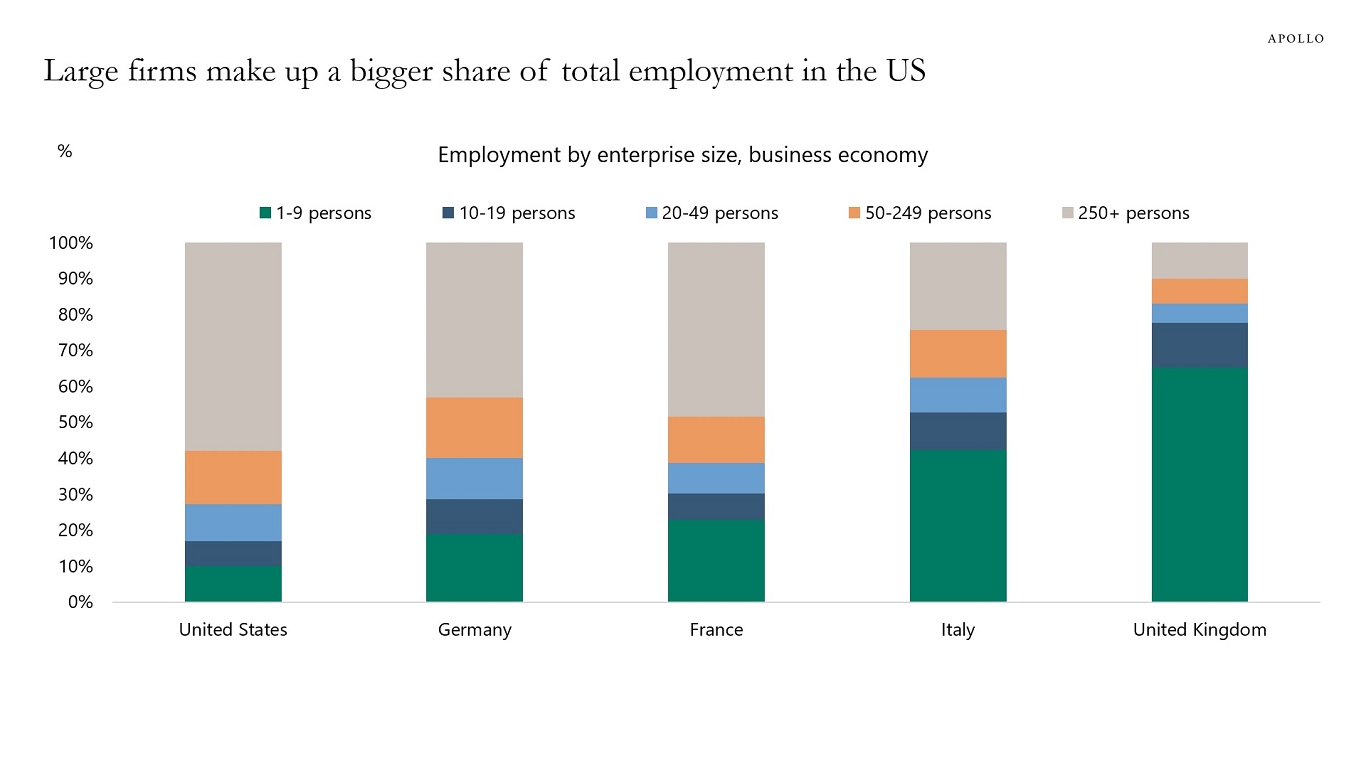

The share of total employment in large firms with more than 250 employees is bigger in the US than in Europe, see chart below.

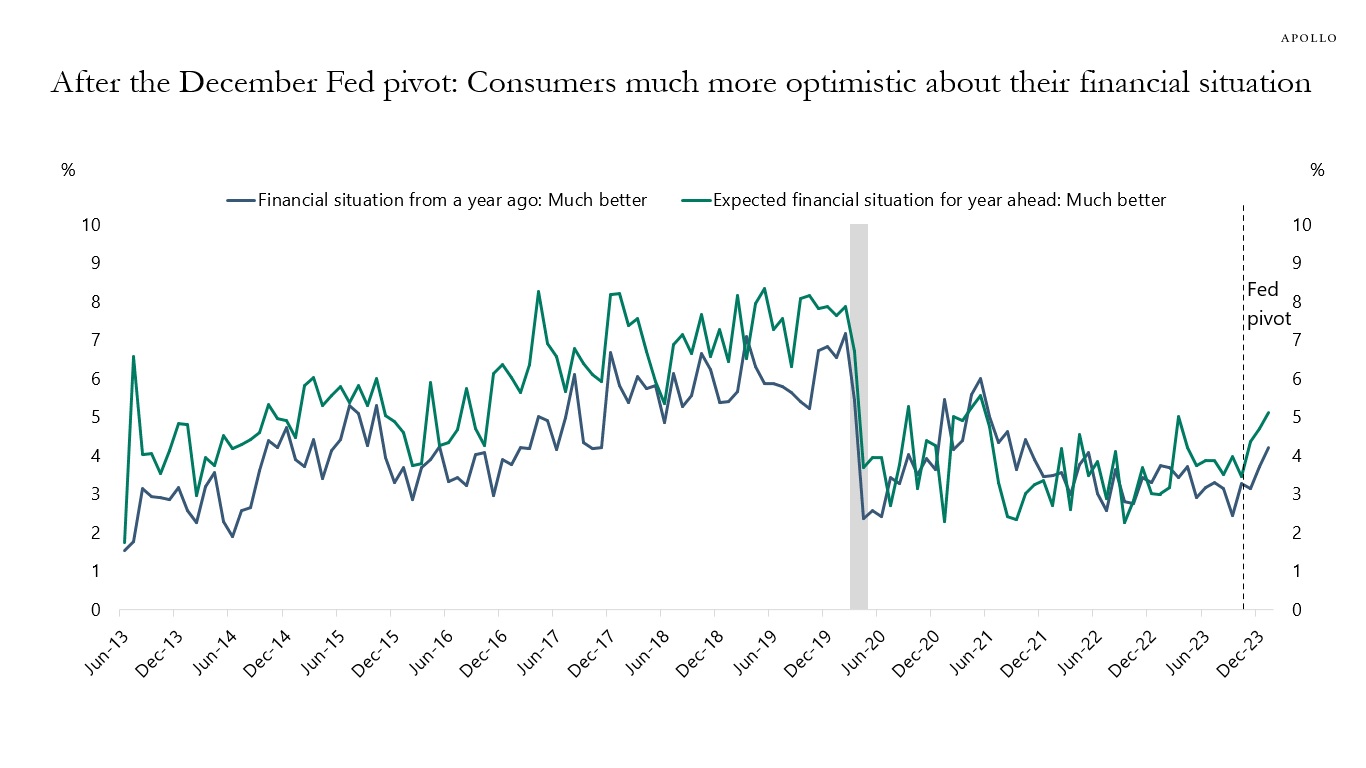

Since the Fed pivot on December 13, consumers have become much more optimistic about the economic outlook, see chart below. Combined with record-high IG issuance, high HY issuance, and more IPO and M&A activity since December, it is not surprising that employment and inflation rebounded in January and jobless claims remain low.

The last mile is harder not because of some structural feature in the economy, but because of the Fed turning dovish too soon, triggering a reacceleration in growth and inflation. That is why the Fed will keep rates higher for longer than markets expect.

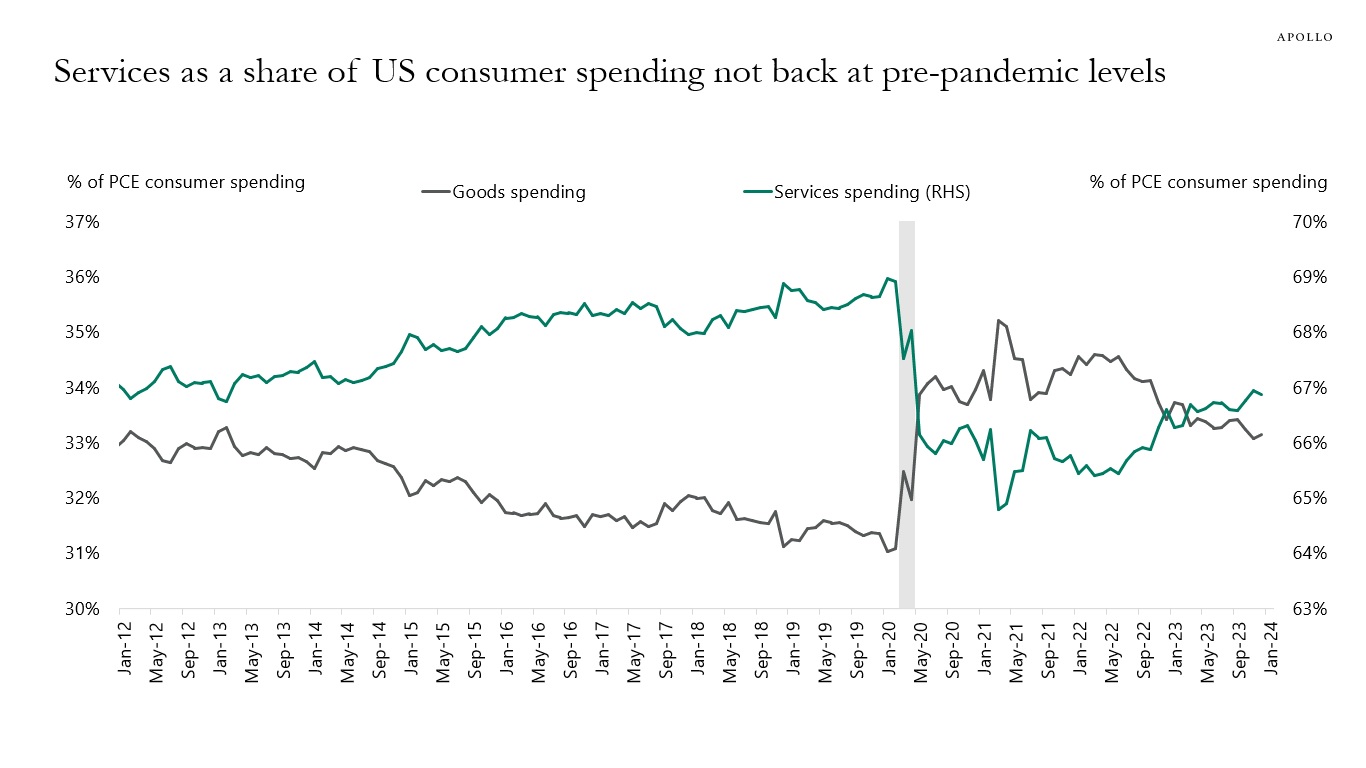

The share of private consumption spent on services is still 2 percentage points below its pre-pandemic level, see chart below.

The implication for markets is that there is still more upside for growth in consumer services, i.e., spending on airlines, hotels, restaurants, concerts, sporting events, etc.

With inflation still not fully tamed, stock valuations high, and bond spreads tight, what’s an investor seeking diversification to do? In his latest paper, Apollo Partner & Global Wealth Strategist Alexander Wright argues that private markets—both equity and debt—might offer solutions amid expected continued volatility.

The information herein is provided for educational purposes only and should not be construed as financial or investment advice, nor should any information in this document be relied on when making an investment decision. Opinions and views expressed reflect the current opinions and views of the authors and Apollo Analysts as of the date hereof and are subject to change. Please see the end of this document for important disclosure information.

Important Disclosure Information

This presentation is for educational purposes only and should not be treated as research. This presentation may not be distributed, transmitted or otherwise communicated to others, in whole or in part, without the express written consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

The views and opinions expressed in this presentation are the views and opinions of the author(s) of the White Paper. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Further, Apollo and its affiliates may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this presentation. There can be no assurance that an investment strategy will be successful. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. Target allocations contained herein are subject to change. There is no assurance that the target allocations will be achieved, and actual allocations may be significantly different than that shown here. This presentation does not constitute an offer of any service or product of Apollo. It is not an invitation by or on behalf of Apollo to any person to buy or sell any security or to adopt any investment strategy, and shall not form the basis of, nor may it accompany nor form part of, any right or contract to buy or sell any security or to adopt any investment strategy. Nothing herein should be taken as investment advice or a recommendation to enter into any transaction.

Hyperlinks to third-party websites in this presentation are provided for reader convenience only. There can be no assurance that any trends discussed herein will continue. Unless otherwise noted, information included herein is presented as of the dates indicated. This presentation is not complete and the information contained herein may change at any time without notice. Apollo does not have any responsibility to update the presentation to account for such changes. Apollo has not made any representation or warranty, expressed or implied, with respect to fairness, correctness, accuracy, reasonableness, or completeness of any of the information contained herein, and expressly disclaims any responsibility or liability therefore. The information contained herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Investors should make an independent investigation of the information contained herein, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients.

Certain information contained herein may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such information. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.

The Standard & Poor’s 500 (“S&P 500”) Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies by market value.

Additional information may be available upon request.