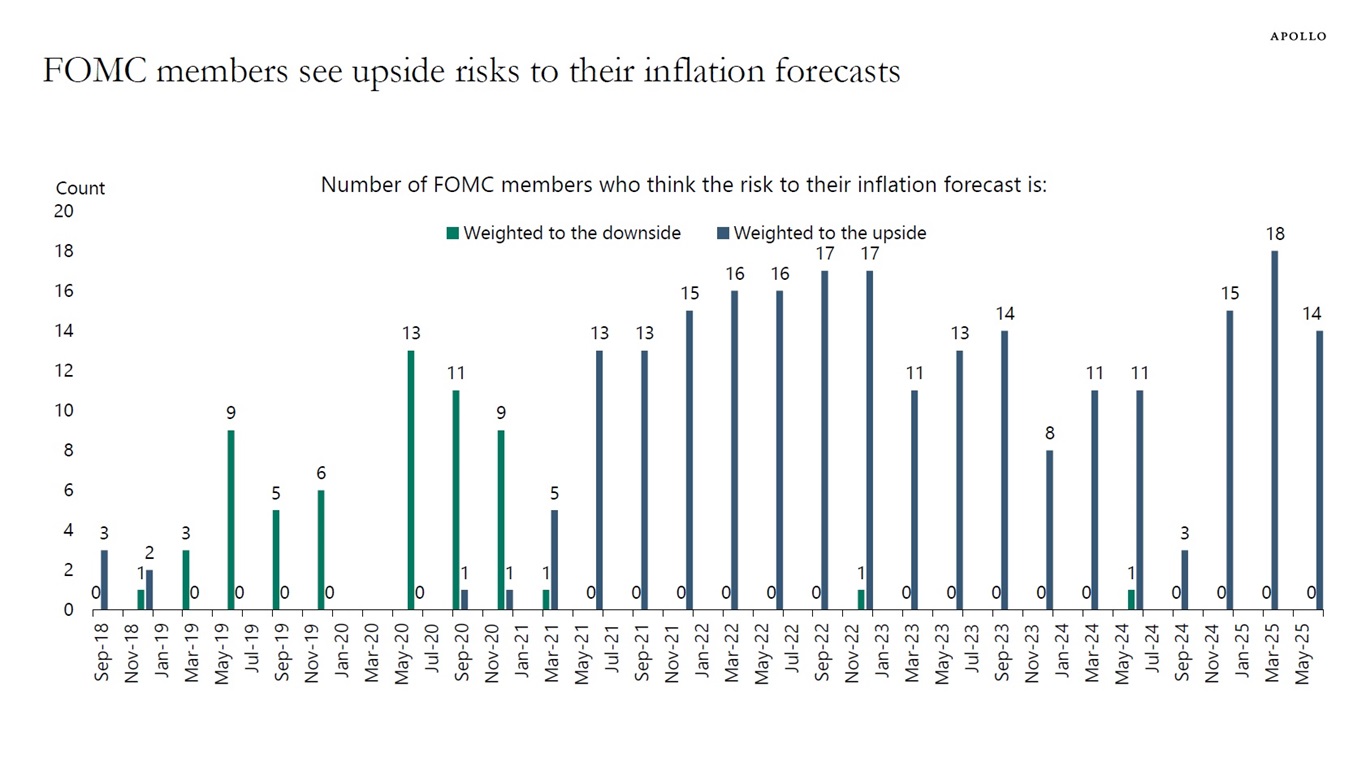

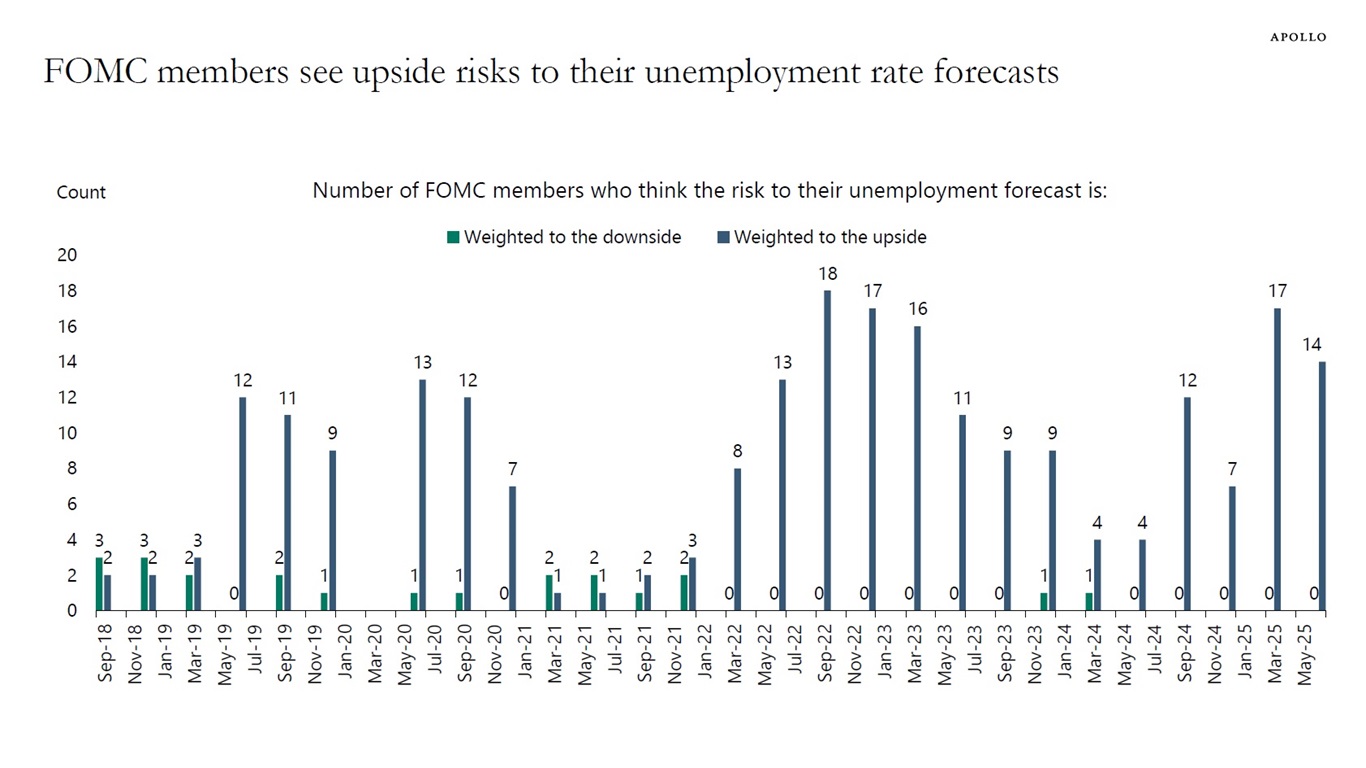

When FOMC members produce their forecasts ahead of Fed meetings, they are also asked how they view the risks to inflation and unemployment.

Currently, there are no FOMC members who foresee downside risks to the unemployment rate or inflation, see charts below.

In other words, the Fed continues to forecast stagflation and is concerned that we may experience rising inflation and rising unemployment at the same time.

These worries are likely driven by higher oil prices, tariffs, and immigration restrictions, all of which are putting upward pressure on inflation and unemployment simultaneously.