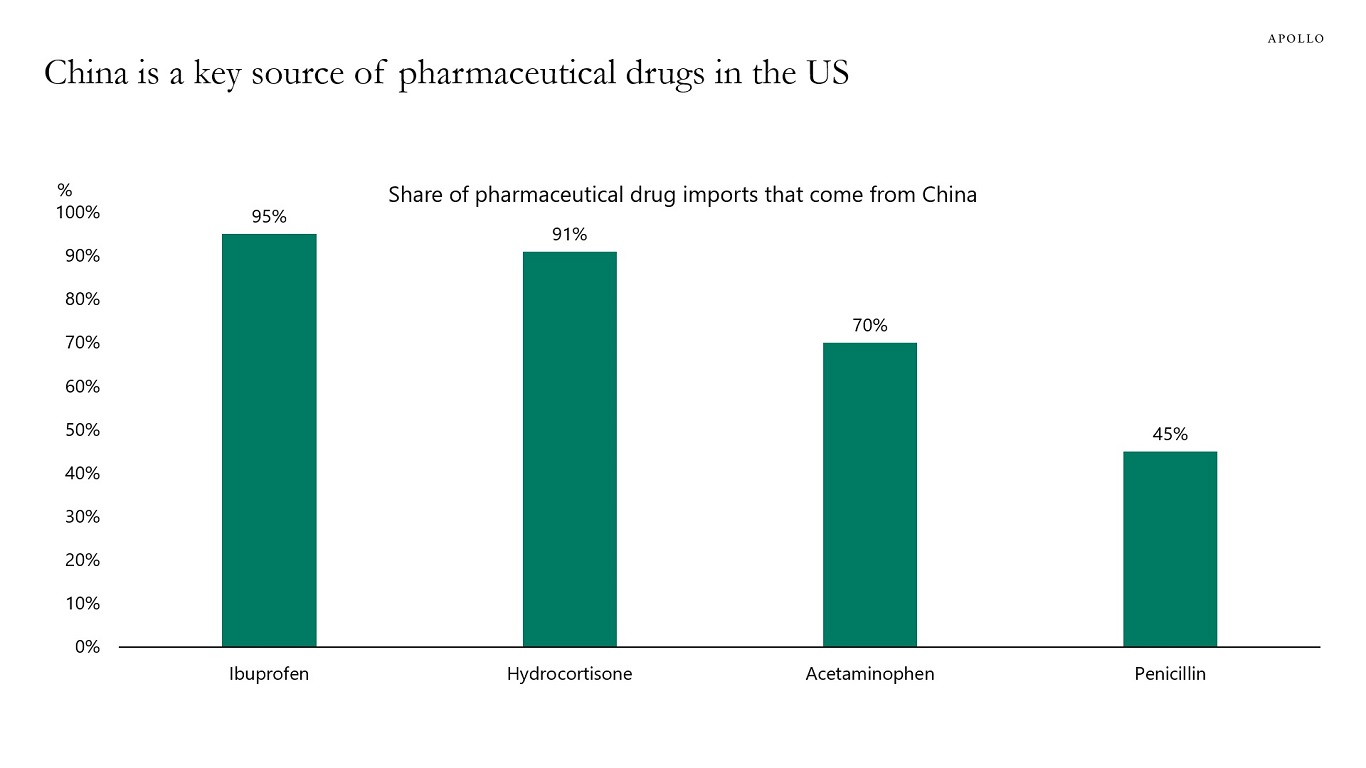

Estimates show that 90% of the inputs in prescription drugs consumed in the US are imported, and the chart below shows the product groups where the US has a high dependency on China.

Estimates show that 90% of the inputs in prescription drugs consumed in the US are imported, and the chart below shows the product groups where the US has a high dependency on China.

The employment report for April will come out on Friday, May 2, and some leading indicators suggest we could see a dramatic weakening in the labor market over the coming months.

Importantly, the survey week for the employment report was the week after Liberation Day tariffs were announced. In other words, the establishment survey and the household survey were carried out during a week with extreme levels of uncertainty for businesses.

The consensus expects 130K jobs created in April. There are significant risks the number is going to be lower, perhaps even negative, see chart below.

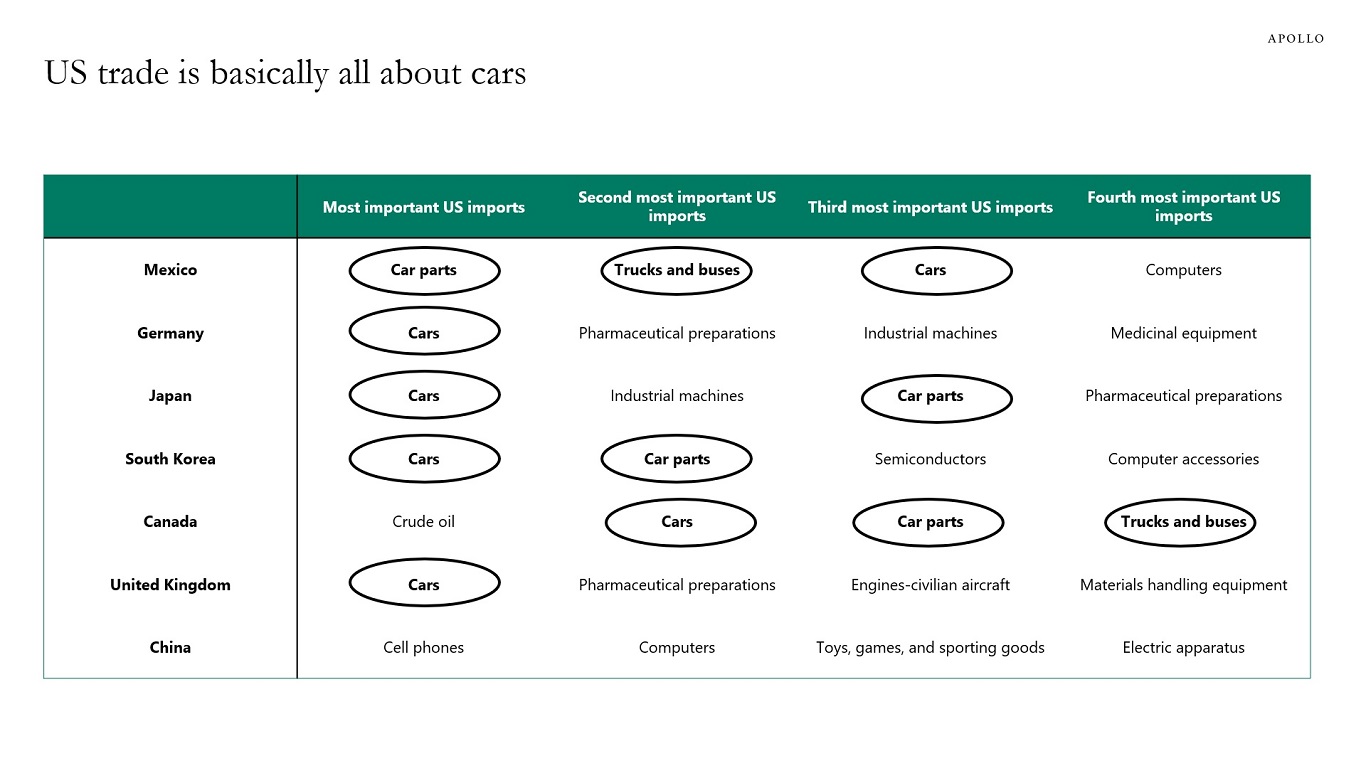

The chart below shows that cars and car parts play a key role in most trade negotiations.

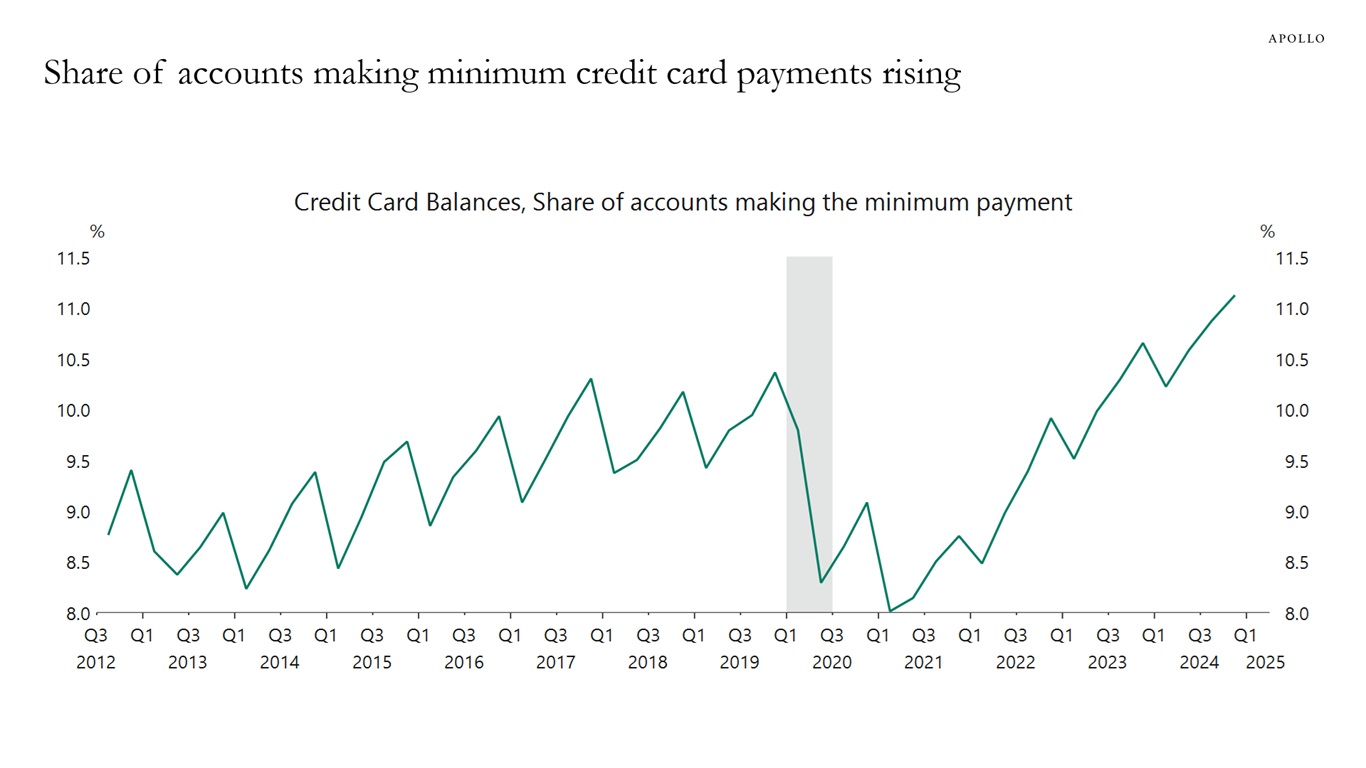

Data from the Fed shows that a record-high share of households are only making the minimum payment on their credit cards, see chart below.

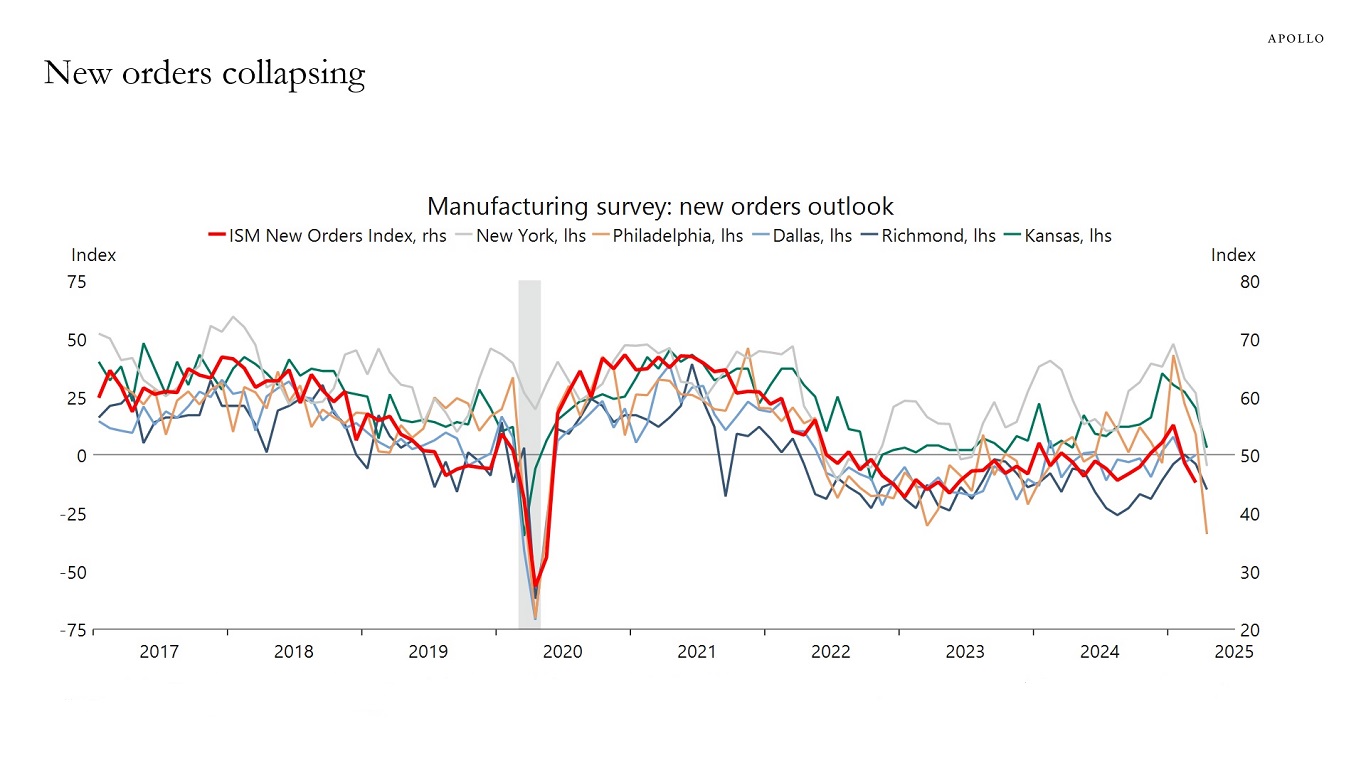

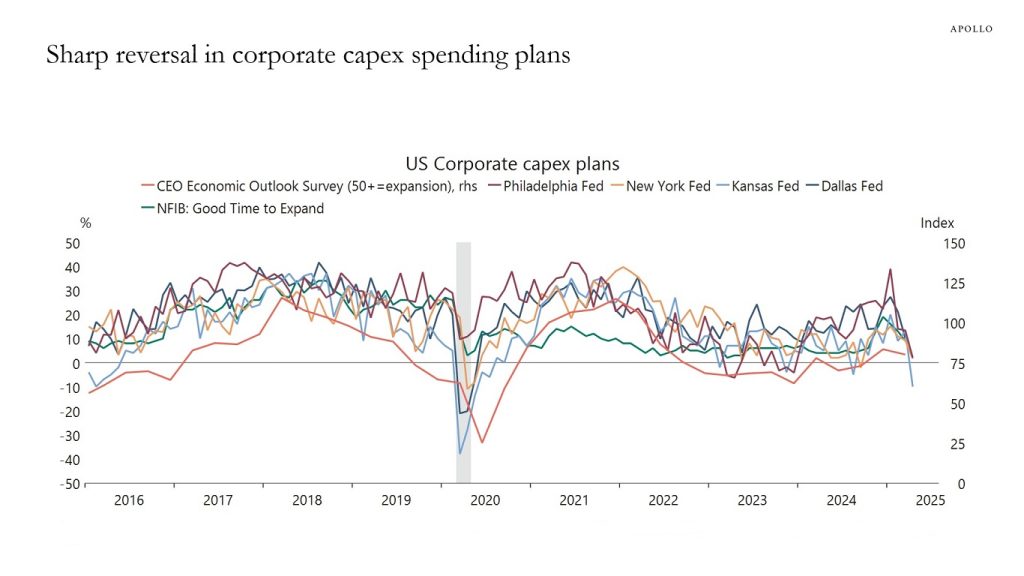

The chart book available here looks at how US consumers and firms are responding to tariffs.

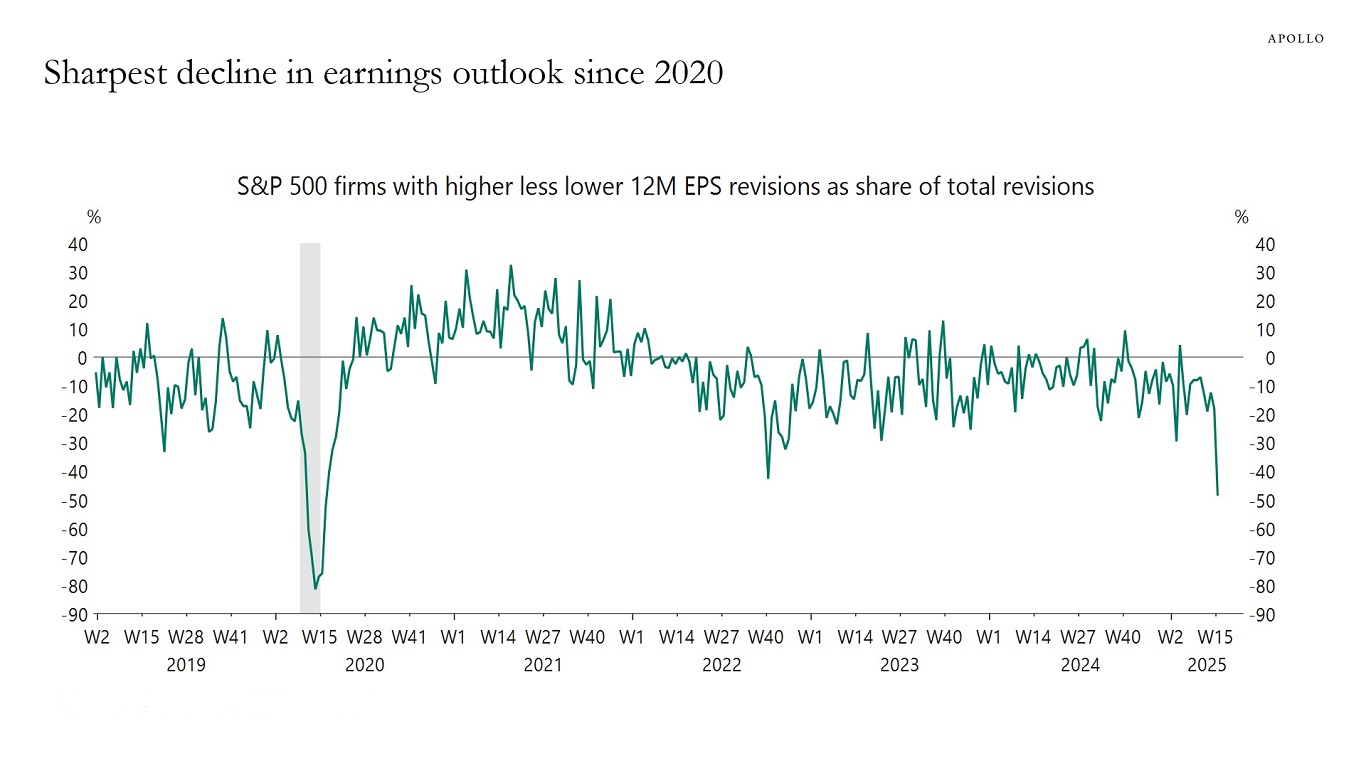

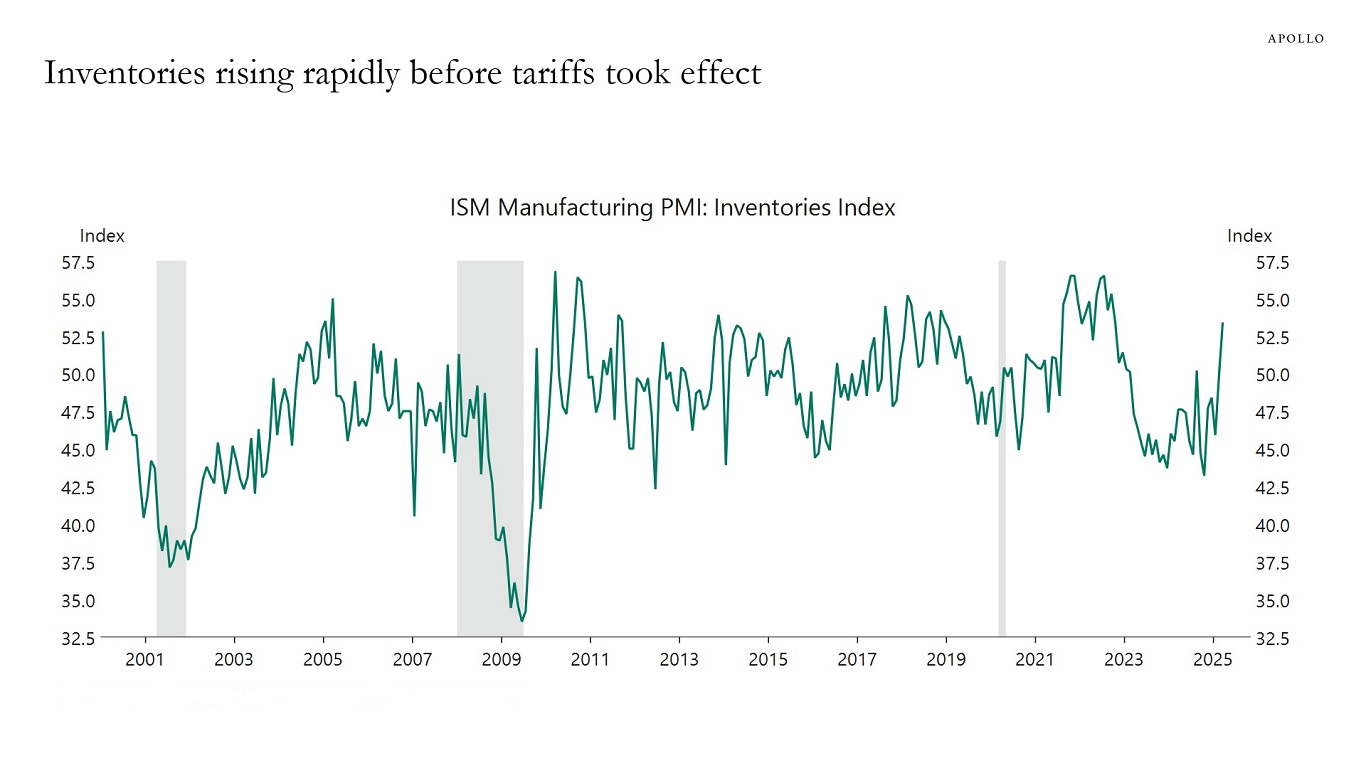

For companies, new orders are falling, capex plans are declining, inventories were rising before tariffs took effect, and firms are revising down earnings expectations.

For households, consumer confidence is at record-low levels, consumers were front-loading purchases before tariffs began, and tourism is slowing, in particular international travel.

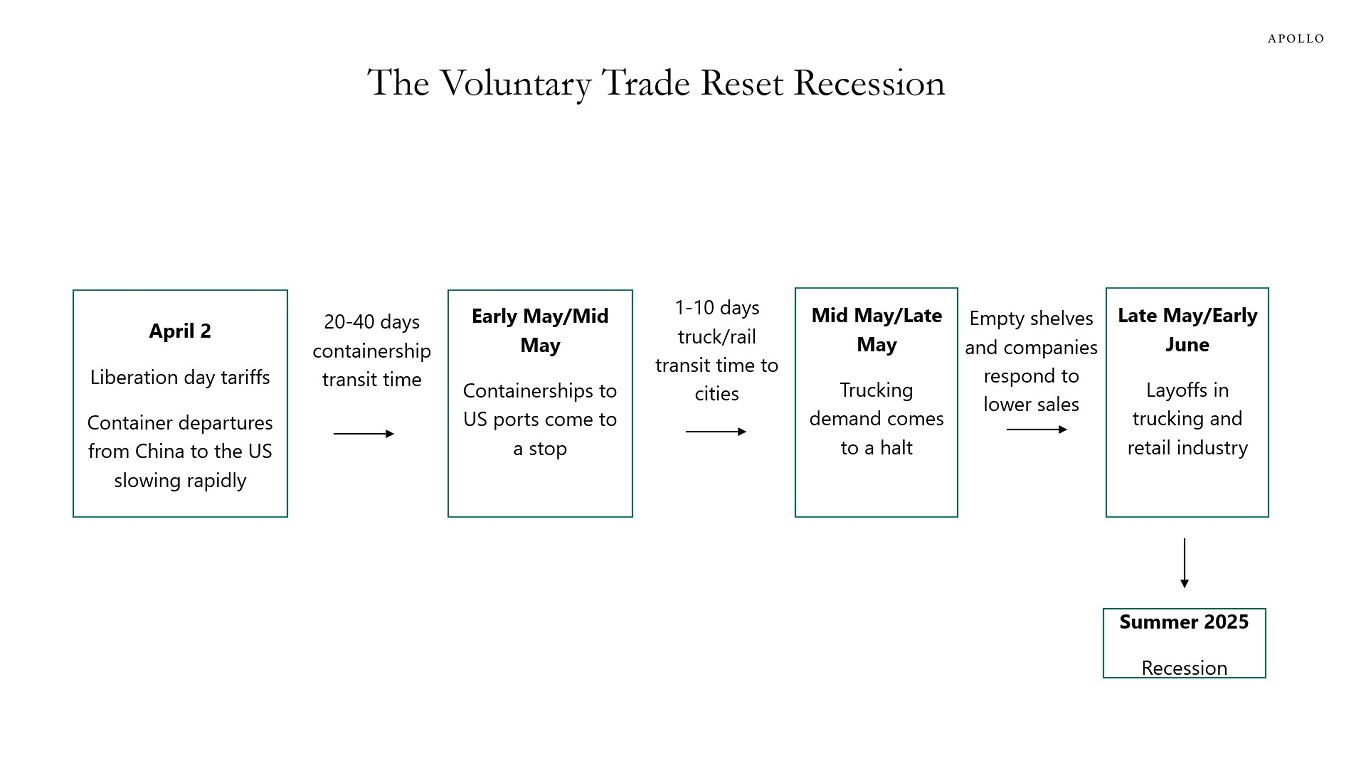

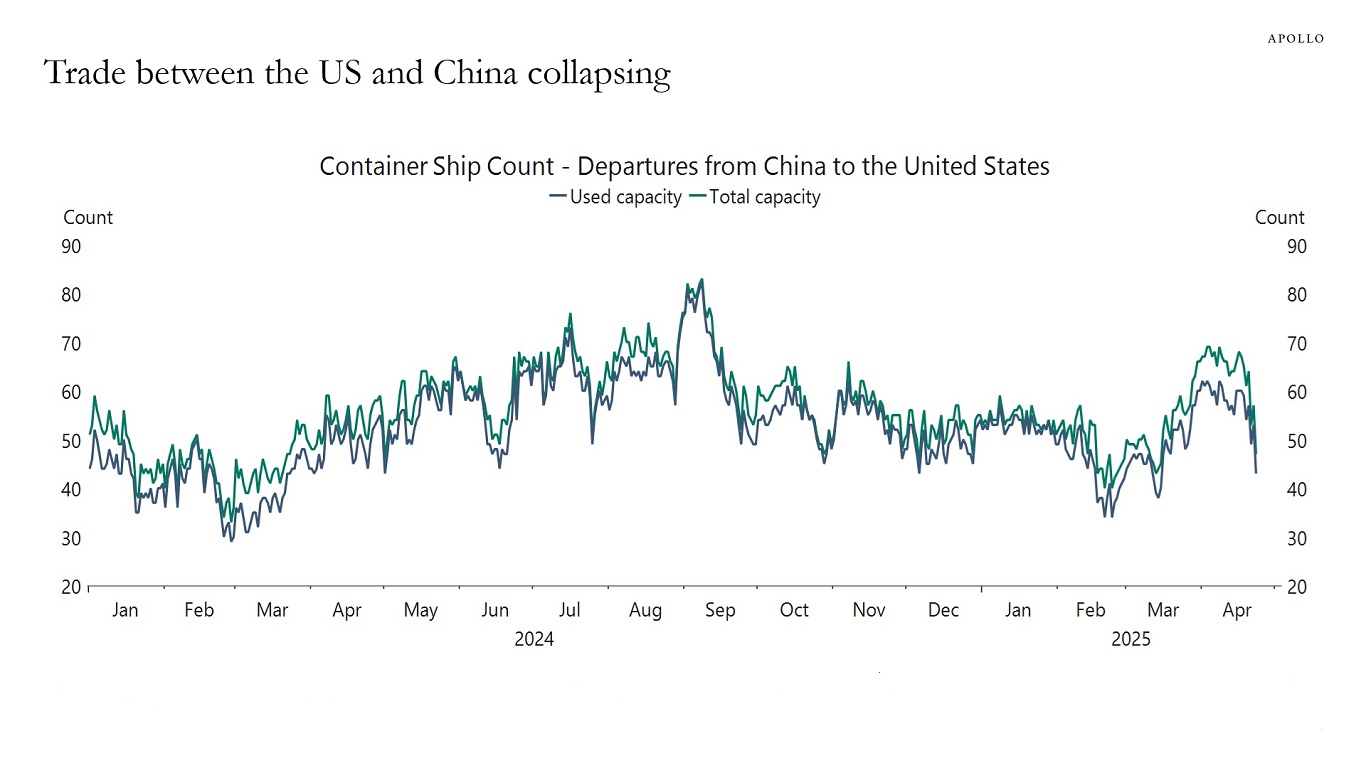

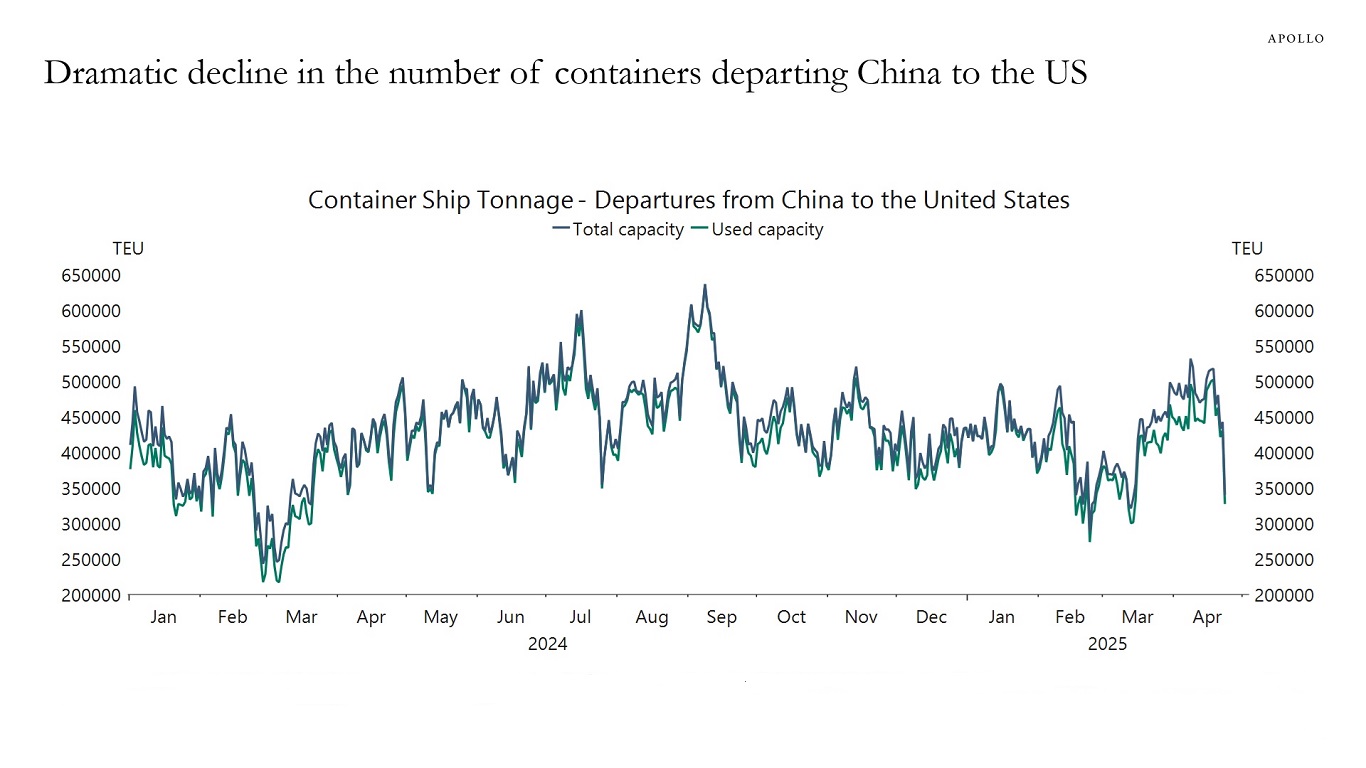

Daily data for container traffic from China to the US is collapsing, see charts below.

The consequence will be empty shelves in US stores in a few weeks and Covid-like shortages for consumers and for firms using Chinese products as intermediate goods.

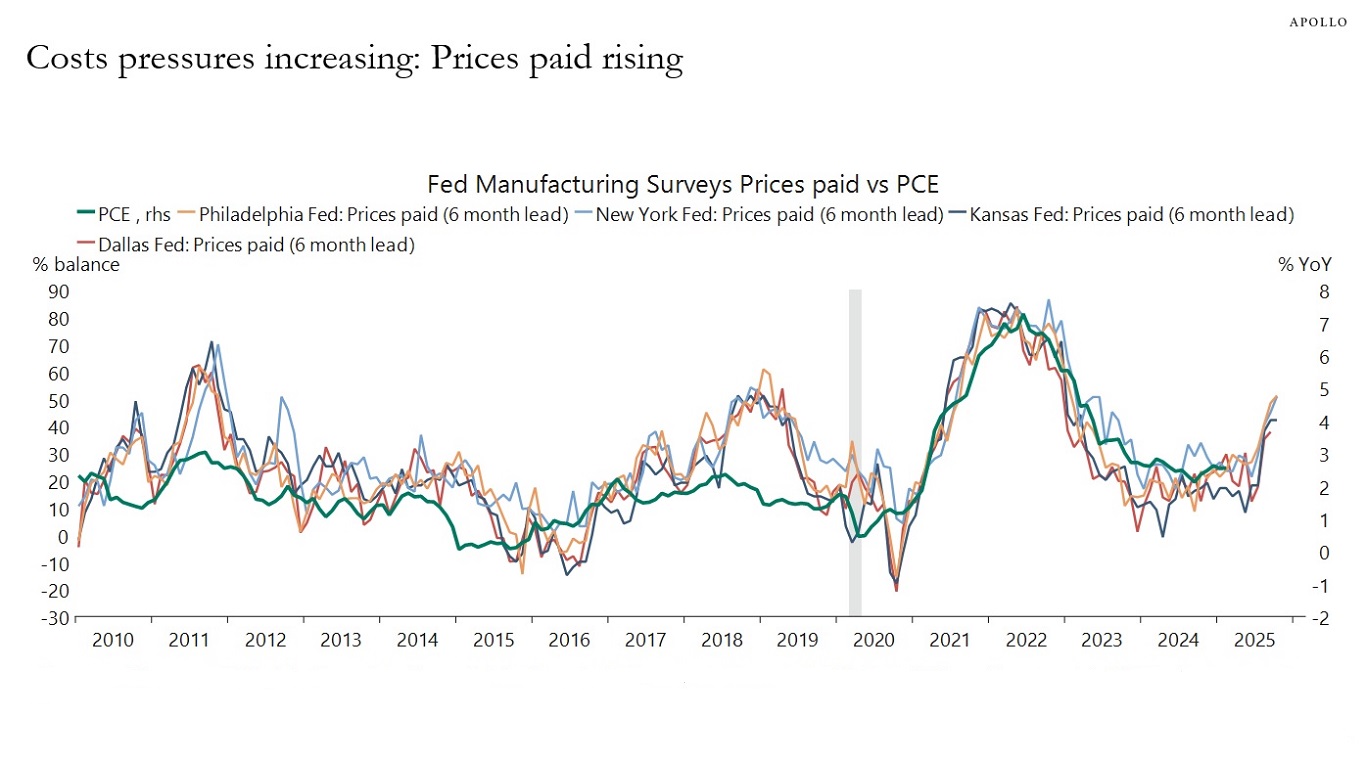

In addition, we will soon begin to see higher inflation because there are a significant number of product categories where China is the main provider of certain goods into the US market.

In May, we will begin to see significant layoffs in trucking, logistics, and retail—particularly in small businesses such as your independent toy store, your independent hardware store, and your independent men’s clothing store. With 9 million people working in trucking-related jobs and 16 million people working in the retail sector, the downside risks to the economy are significant.

The manufacturing sector in the US has been in steady decline for the past 80 years, and manufacturing jobs today only make up 8% of total US employment. See chart below.

There are three reasons why manufacturing is playing a smaller role: automation, global trade, and significant growth in services, such as the technology sector.

If the dollar falls in value, US exports become cheaper, which encourages foreigners to buy more US manufacturing goods.

But another reason why the rest of the world buys US products is because US products are superior relative to products from other countries, particularly in the services sector, where the US is market-leading with Microsoft, Meta, AWS, Netflix, large language models, etc.

By depreciating the dollar and starting a trade war about goods, which make up less than 10% of US GDP, the US is risking that the rest of the world will slow their imports of the 80% of the US economy that is services, such as iPhones, Windows, Facebook, and large language models.

In addition, a depreciating dollar puts upward pressure on inflation and the term premium, which can create new macroeconomic challenges.

The bottom line is that depreciating the dollar comes with some risks. There is no free lunch in macroeconomics.

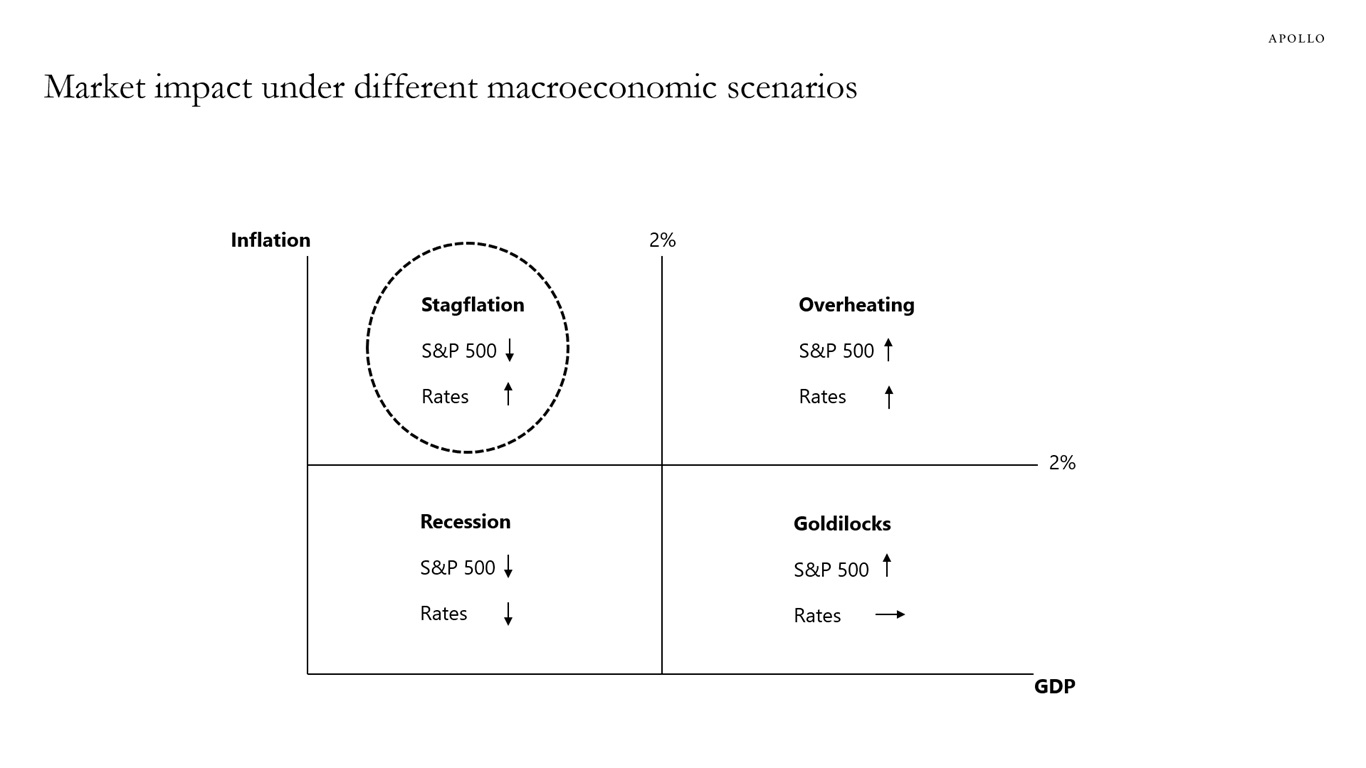

The economics textbook would say that a trade war is a stagflation shock. Tariffs increase consumer prices, and earnings are lower because companies either have to pay some of the tariffs or raise prices for consumers and experience lower demand.

With higher inflation and lower earnings, investors should expect interest rates to stay higher for longer, and investors should expect downward pressure on the stock market as a result of downward pressure on corporate profits, see chart below.

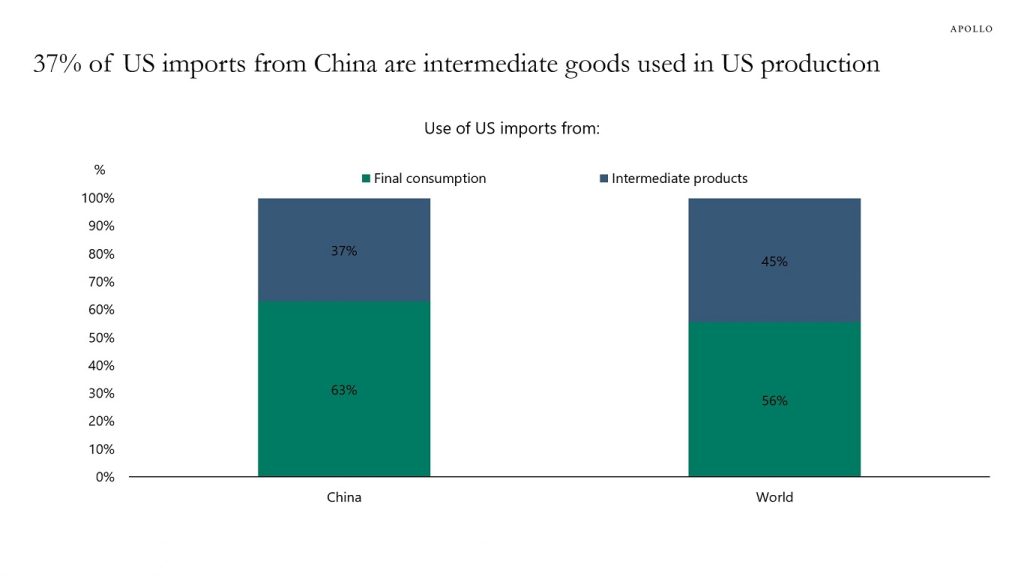

Thirty-seven percent of US imports from China are intermediate goods that are used in US production—such as in the machinery, tool, and auto industries—see chart below. In addition, small and medium-sized enterprises account for 41% of imports from China.

The bottom line is that imports from China are not only t-shirts, shoes, and TV monitors purchased by US consumers. Almost 40% of imports from China are intermediate goods used in US production.

As a result, a dramatic increase in tariffs on China will also increase US companies’ costs of production.

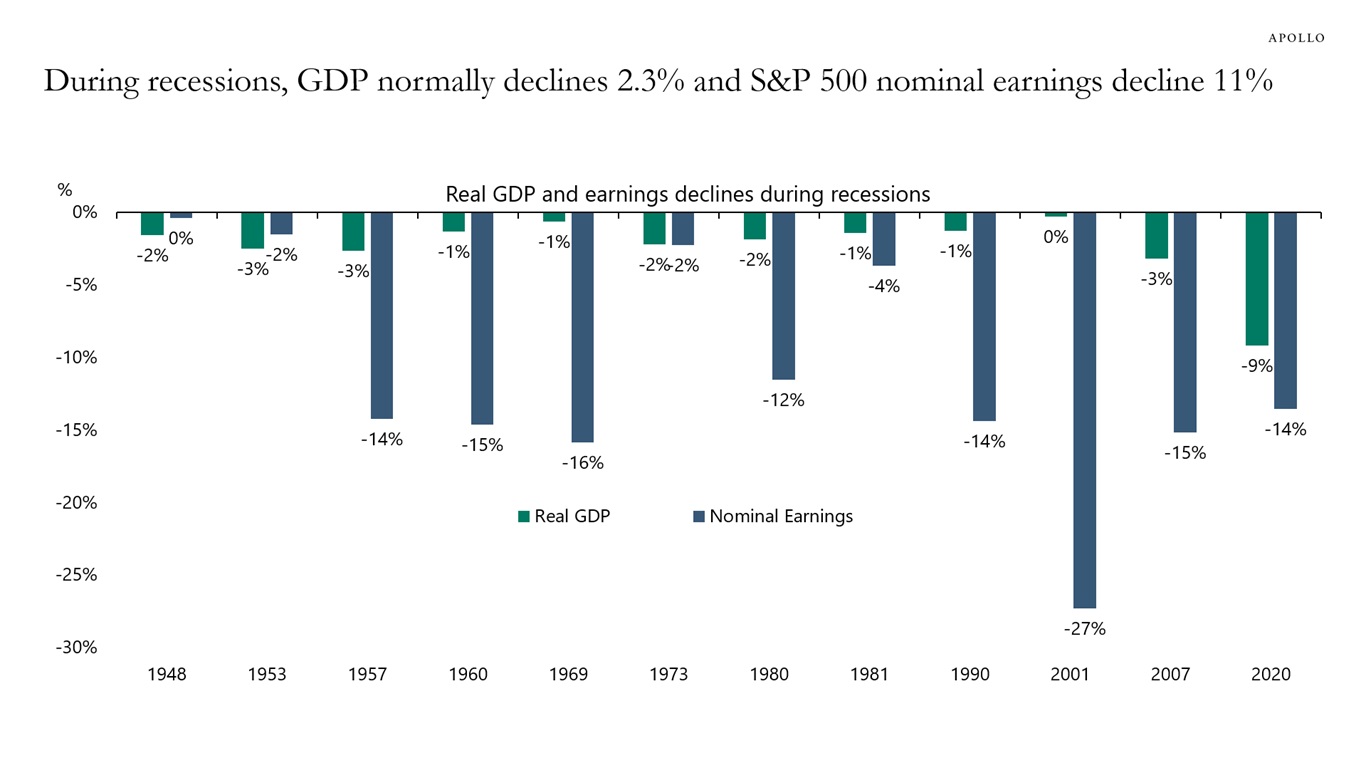

Looking back at all recessions since World War II shows that GDP on average declines 2.3% and S&P 500 earnings on average decline 11%, see chart below.