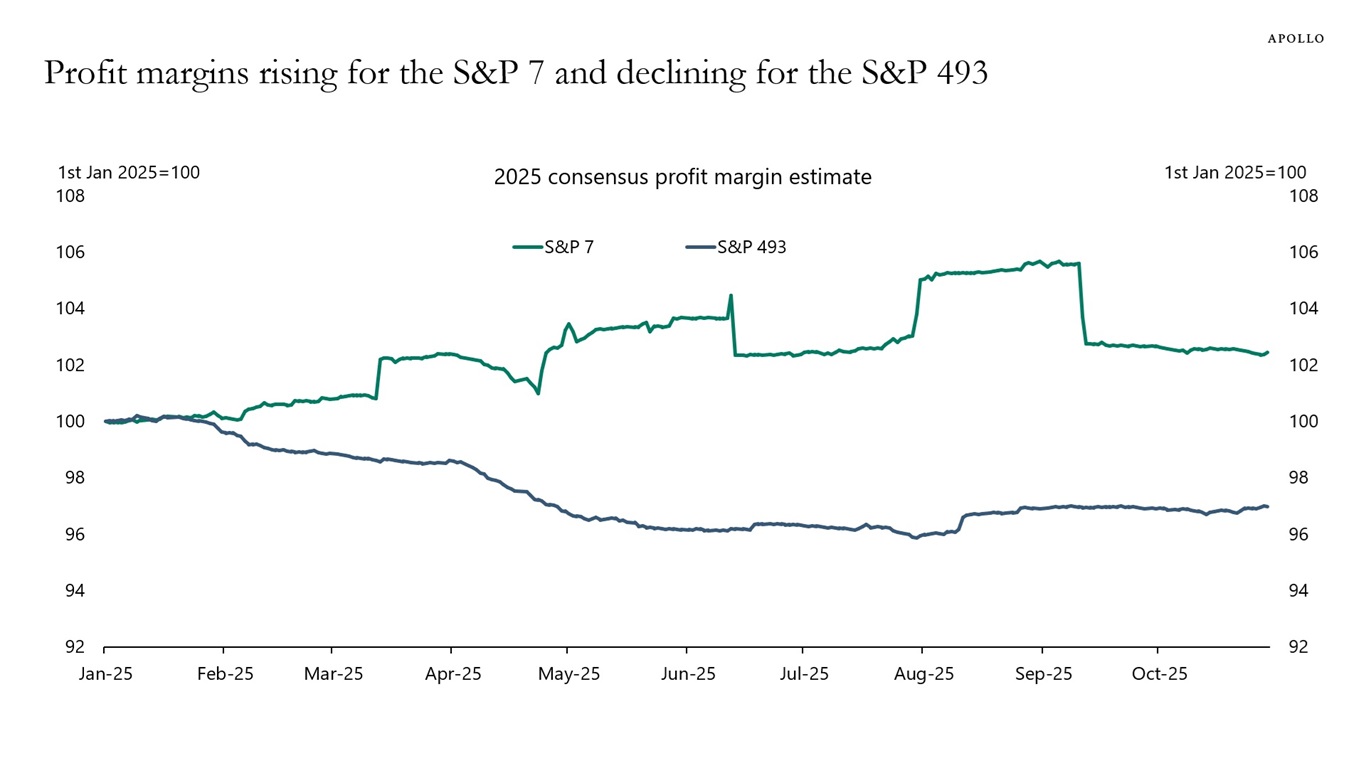

Since the beginning of the year, profit margins have increased for the Magnificent Seven and declined for everyone else, see chart below.

Since the beginning of the year, profit margins have increased for the Magnificent Seven and declined for everyone else, see chart below.

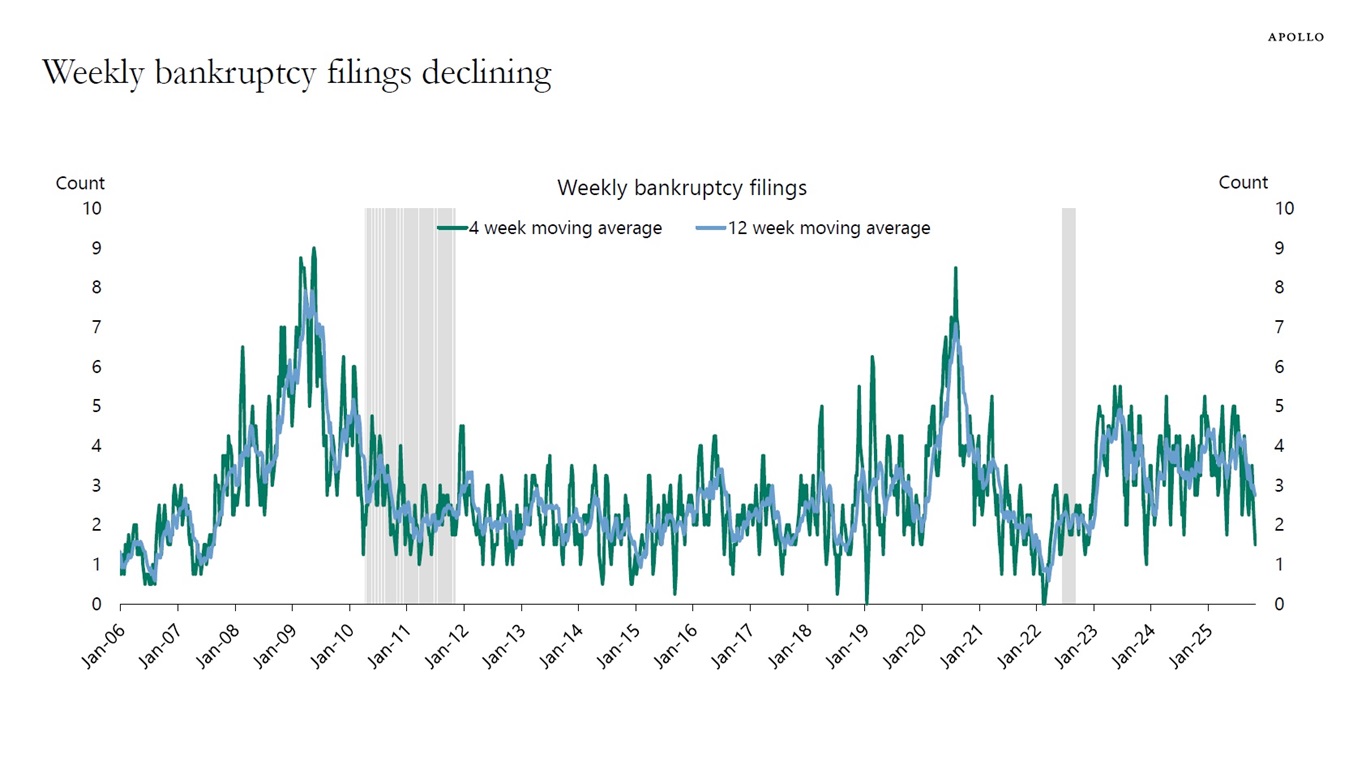

The weekly data for bankruptcy filings shows a clear downtrend in recent months, see chart below.

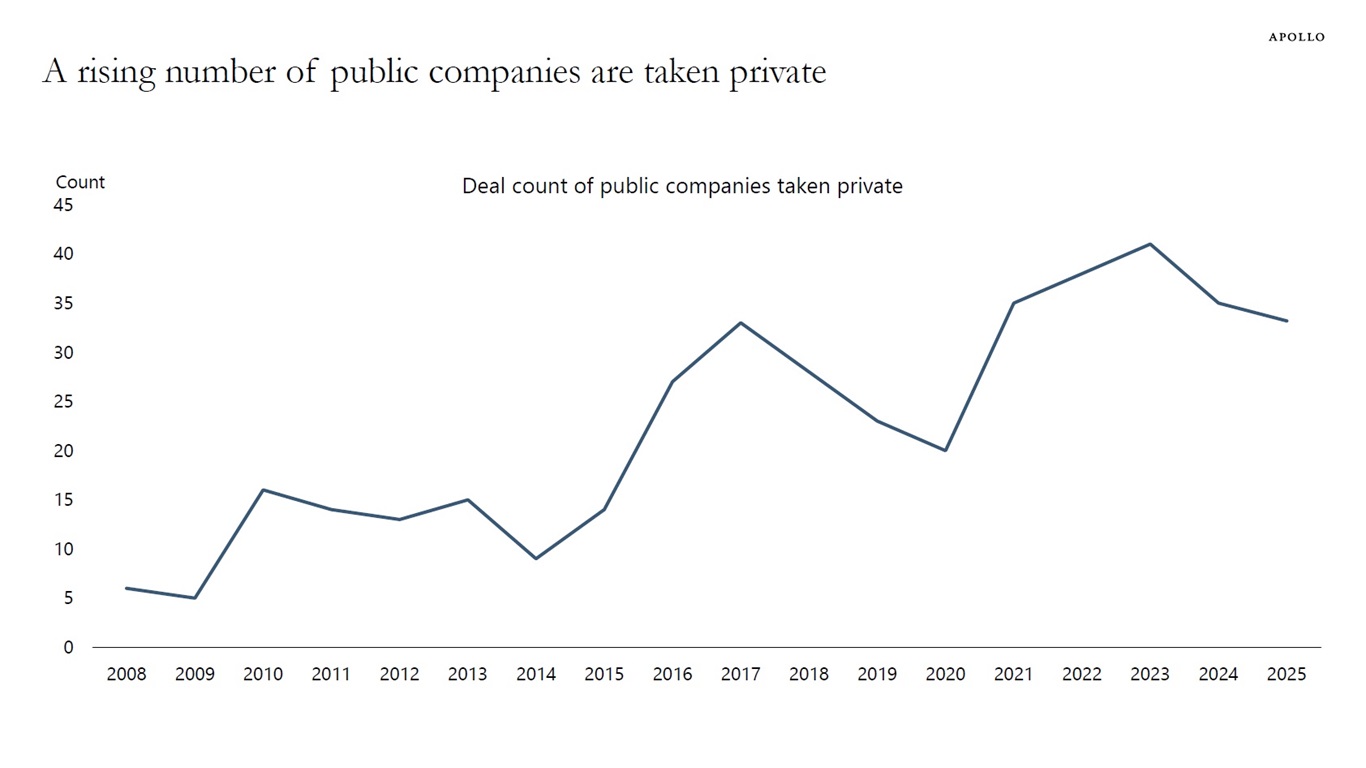

The number of publicly listed companies has declined by 50% since the mid-1990s, and there is a rising trend in the number of public companies that are taken private, see chart below.

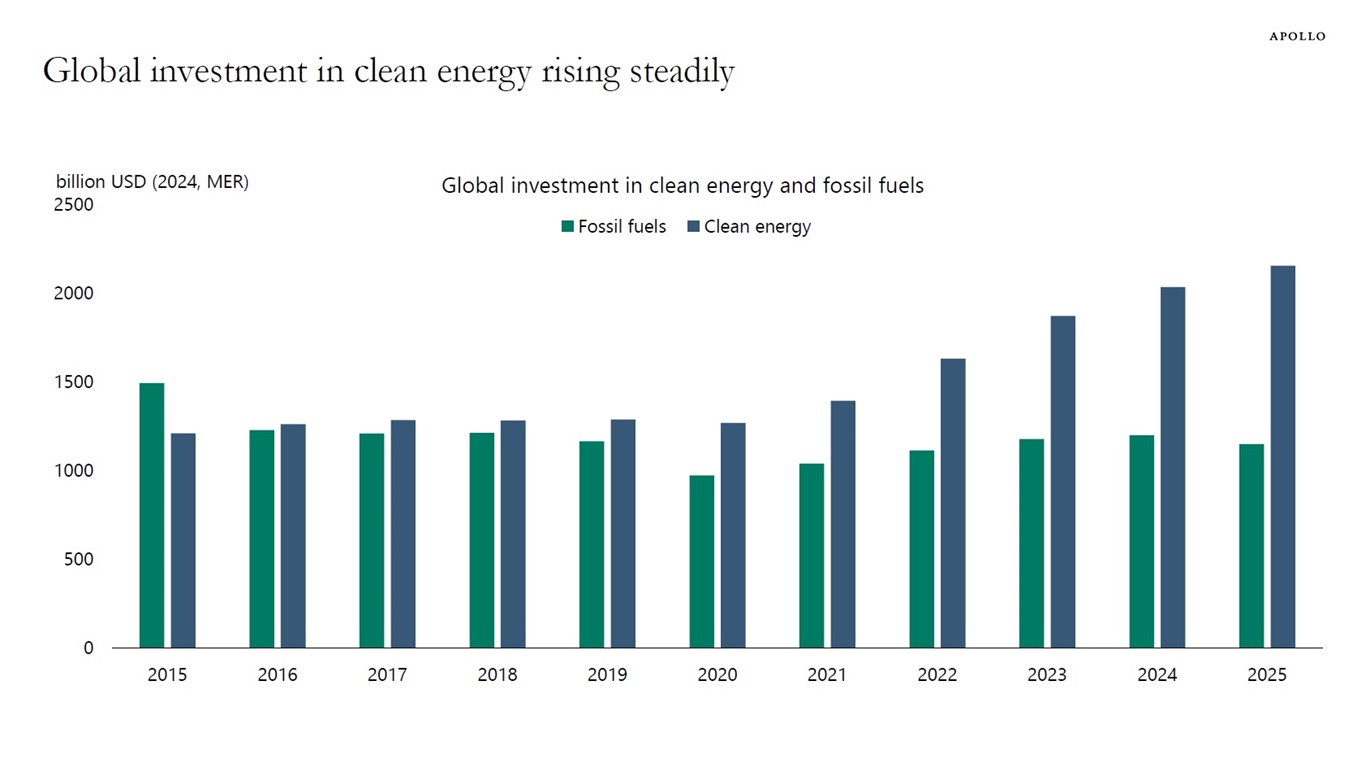

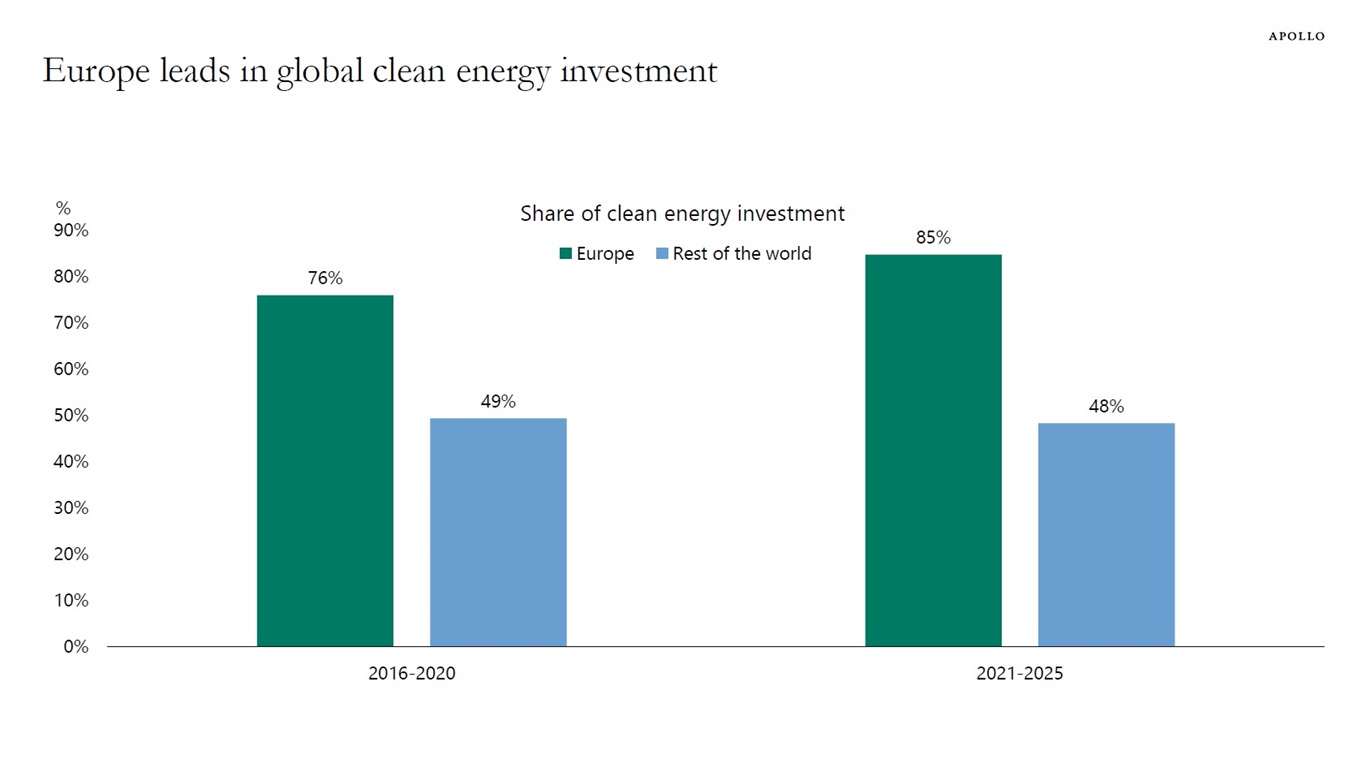

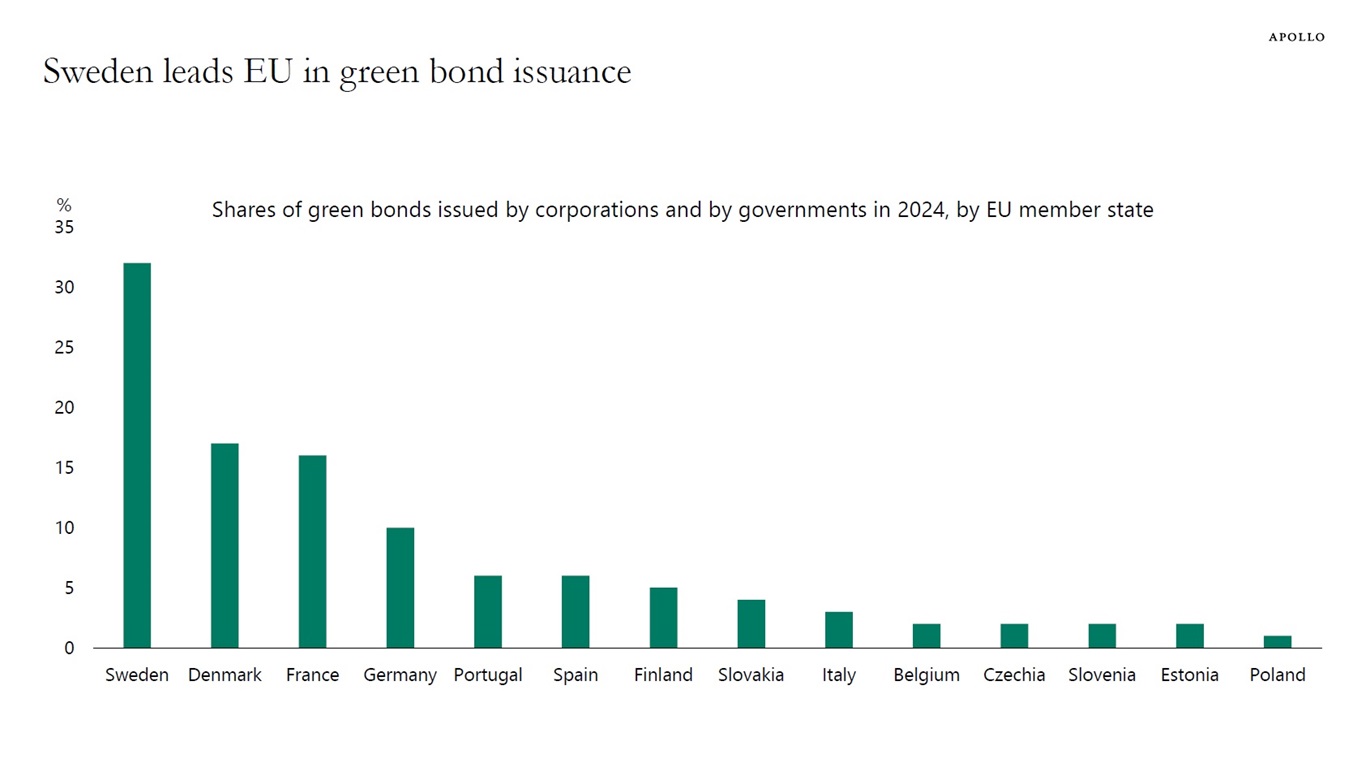

Global investment in clean energy is rising, and Europe is accounting for the biggest share, see charts below.

Private credit is taking on a larger, more important role in capital markets, opening the door for investors to evolve their strategic asset allocations. Combining the collateral-backed security of asset-backed finance with the capital structure seniority and control of direct lending can enhance diversification and give investors a broader, more resilient opportunity set.

Key Takeaways

The information herein is provided for educational purposes only and should not be construed as financial or investment advice, nor should any information in this document be relied on when making an investment decision. Opinions and views expressed reflect the current opinions and views of the authors and Apollo Analysts as of the date hereof and are subject to change. Please see the end of this document for important disclosure information.

Important Disclosure Information

This presentation is for educational purposes only and should not be treated as research. This presentation may not be distributed, transmitted or otherwise communicated to others, in whole or in part, without the express written consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

The views and opinions expressed in this presentation are the views and opinions of the author(s) of the White Paper. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Further, Apollo and its affiliates may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this presentation. There can be no assurance that an investment strategy will be successful. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. Target allocations contained herein are subject to change. There is no assurance that the target allocations will be achieved, and actual allocations may be significantly different than that shown here. This presentation does not constitute an offer of any service or product of Apollo. It is not an invitation by or on behalf of Apollo to any person to buy or sell any security or to adopt any investment strategy, and shall not form the basis of, nor may it accompany nor form part of, any right or contract to buy or sell any security or to adopt any investment strategy. Nothing herein should be taken as investment advice or a recommendation to enter into any transaction.

Hyperlinks to third-party websites in this presentation are provided for reader convenience only. There can be no assurance that any trends discussed herein will continue. Unless otherwise noted, information included herein is presented as of the dates indicated. This presentation is not complete and the information contained herein may change at any time without notice. Apollo does not have any responsibility to update the presentation to account for such changes. Apollo has not made any representation or warranty, expressed or implied, with respect to fairness, correctness, accuracy, reasonableness, or completeness of any of the information contained herein, and expressly disclaims any responsibility or liability therefore. The information contained herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Investors should make an independent investigation of the information contained herein, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients.

Certain information contained herein may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such information. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.

The Standard & Poor’s 500 (“S&P 500”) Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies by market value.

Additional information may be available upon request.

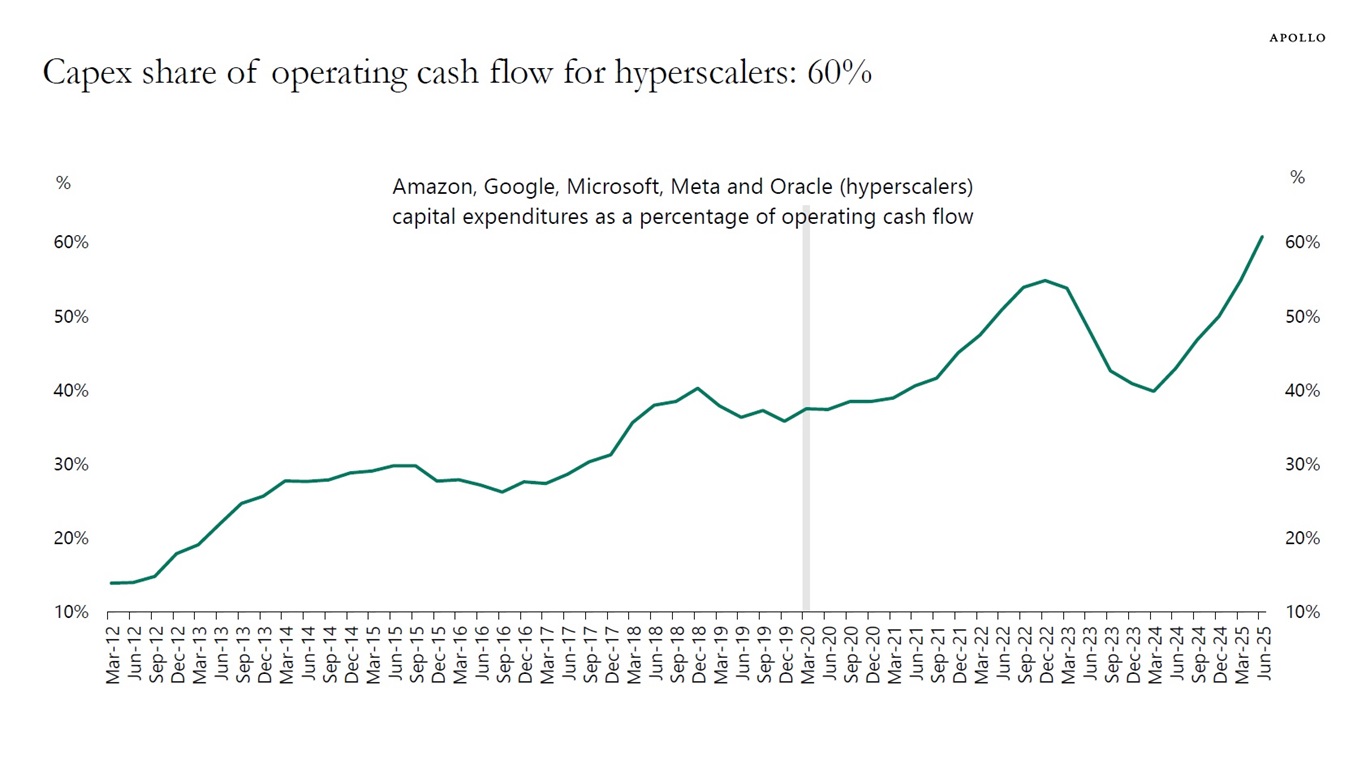

Hyperscalers are currently spending a record high 60% of their operating cash flow on capex, see chart below.

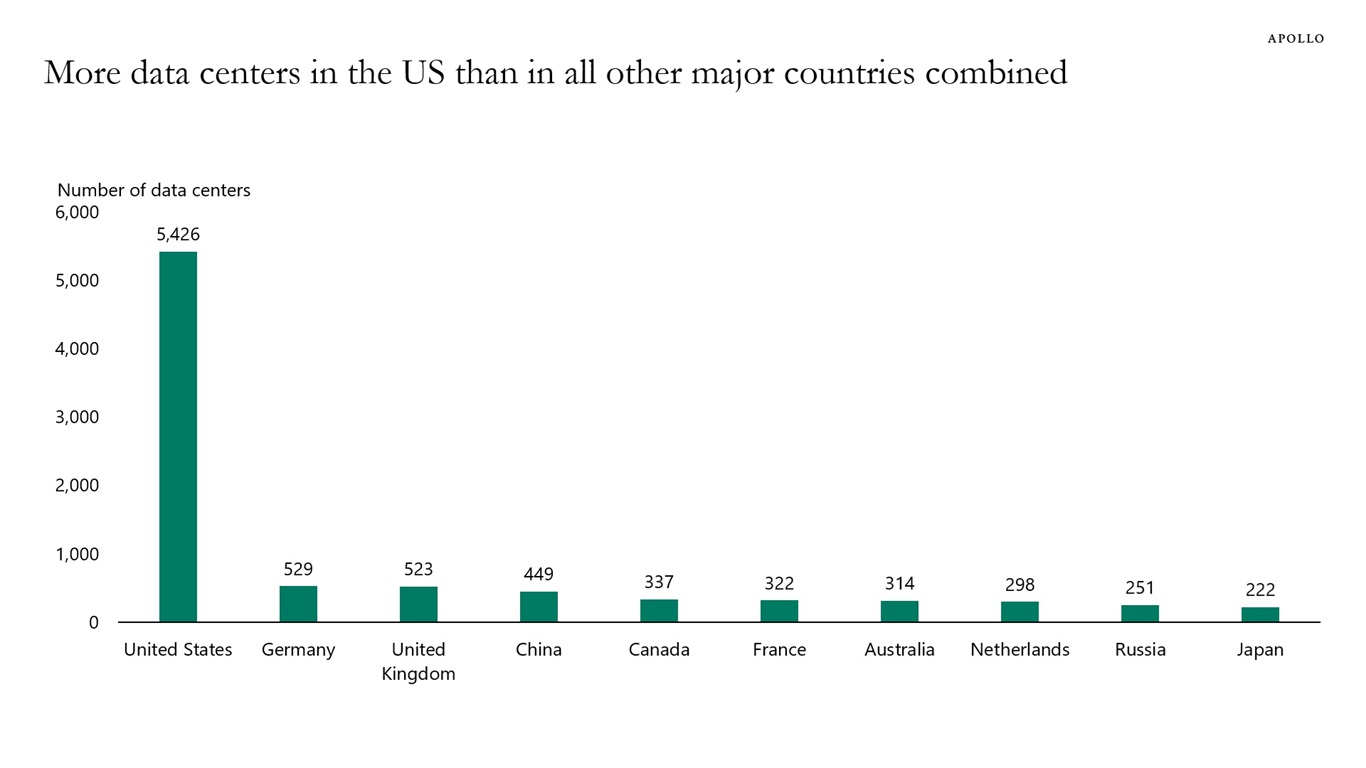

There are about 5,500 data centers in the US, and in Germany there are 529, see chart below. The bottom line is that the rest of the world is far behind the US when it comes to AI.

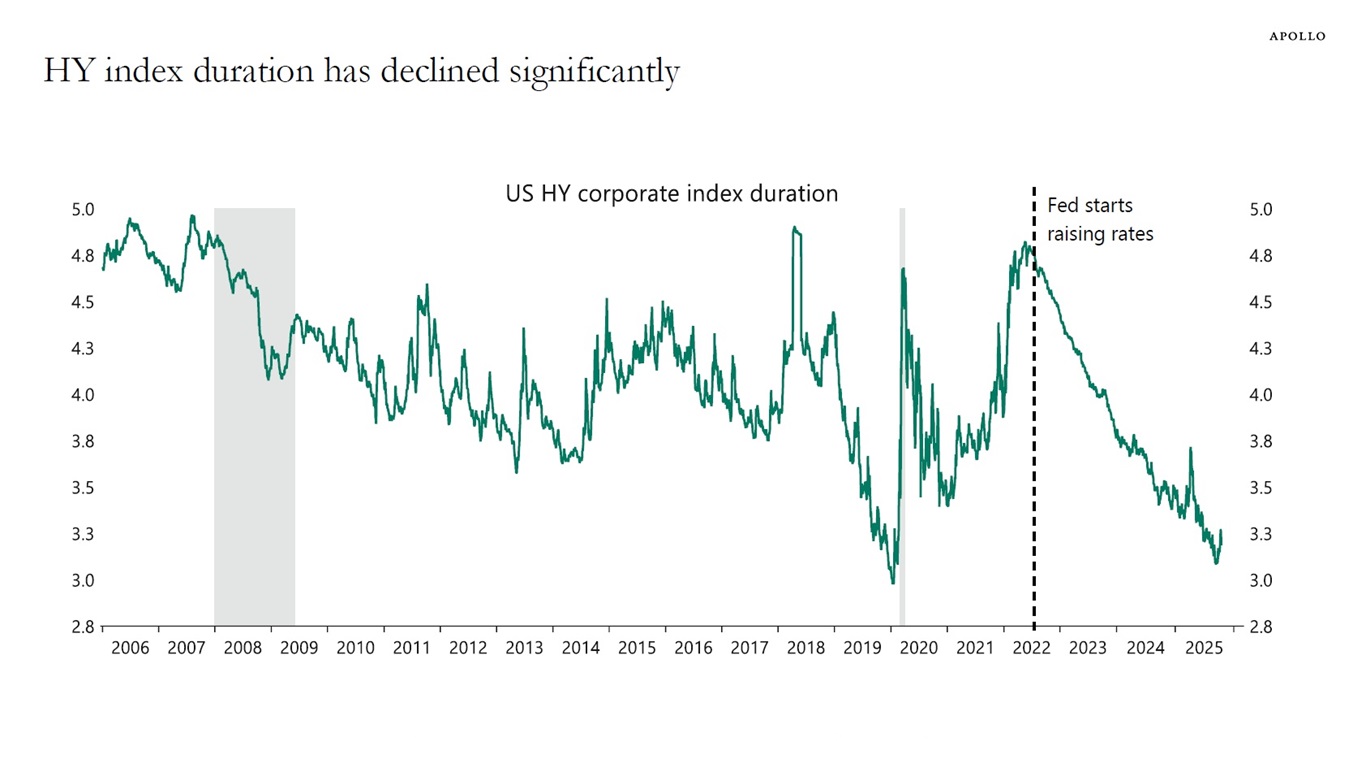

High yield index duration has declined significantly for three reasons:

1) After the Fed raised rates in 2022, and the entire yield curve shifted higher, issuers became reluctant to lock in high coupons for extended periods, instead opting for three- to five-year maturities.

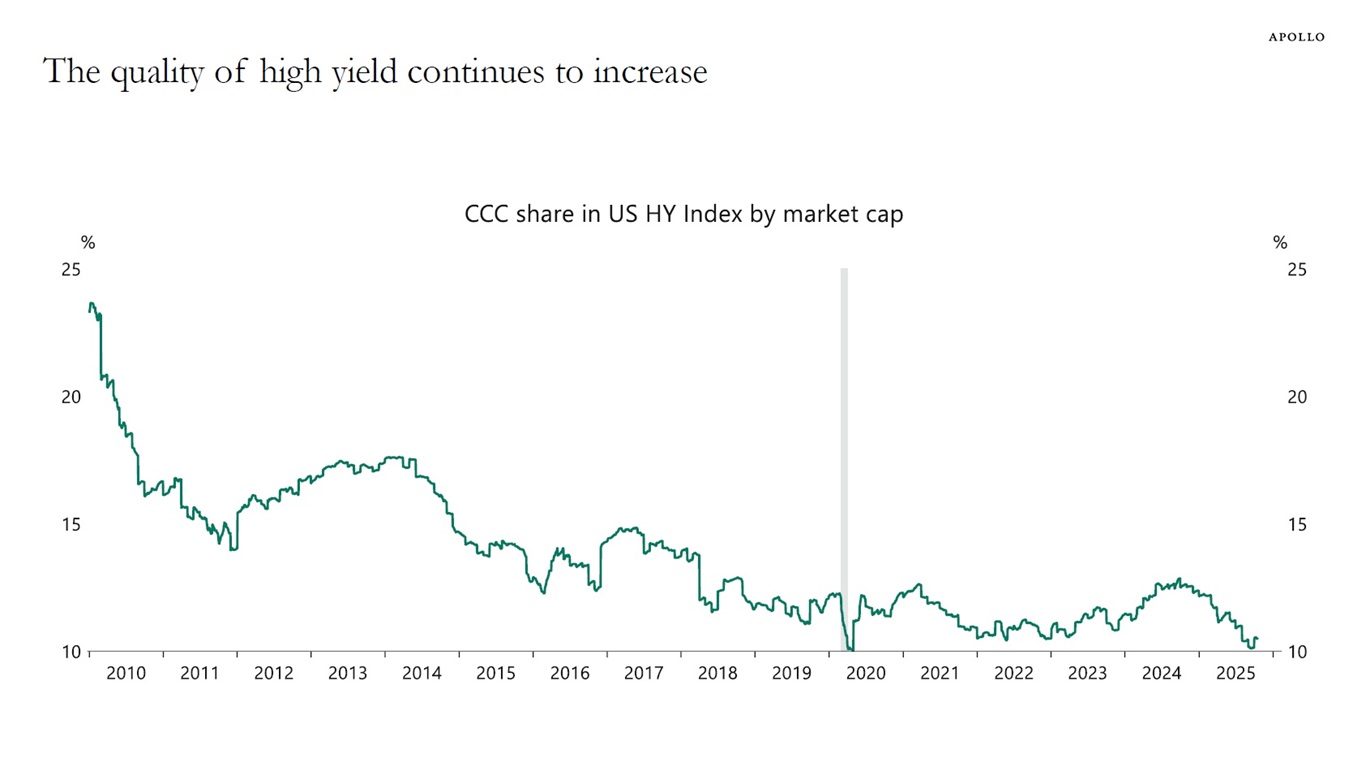

2) Stronger balance sheets and upgrades have raised the average credit rating for high yield, indirectly reducing duration because higher-quality issuers usually issue shorter-term paper, see the second chart.

3) Higher yield levels compress duration mathematically, and a bond’s modified duration declines as its coupon rises, even if the maturity structure is constant.

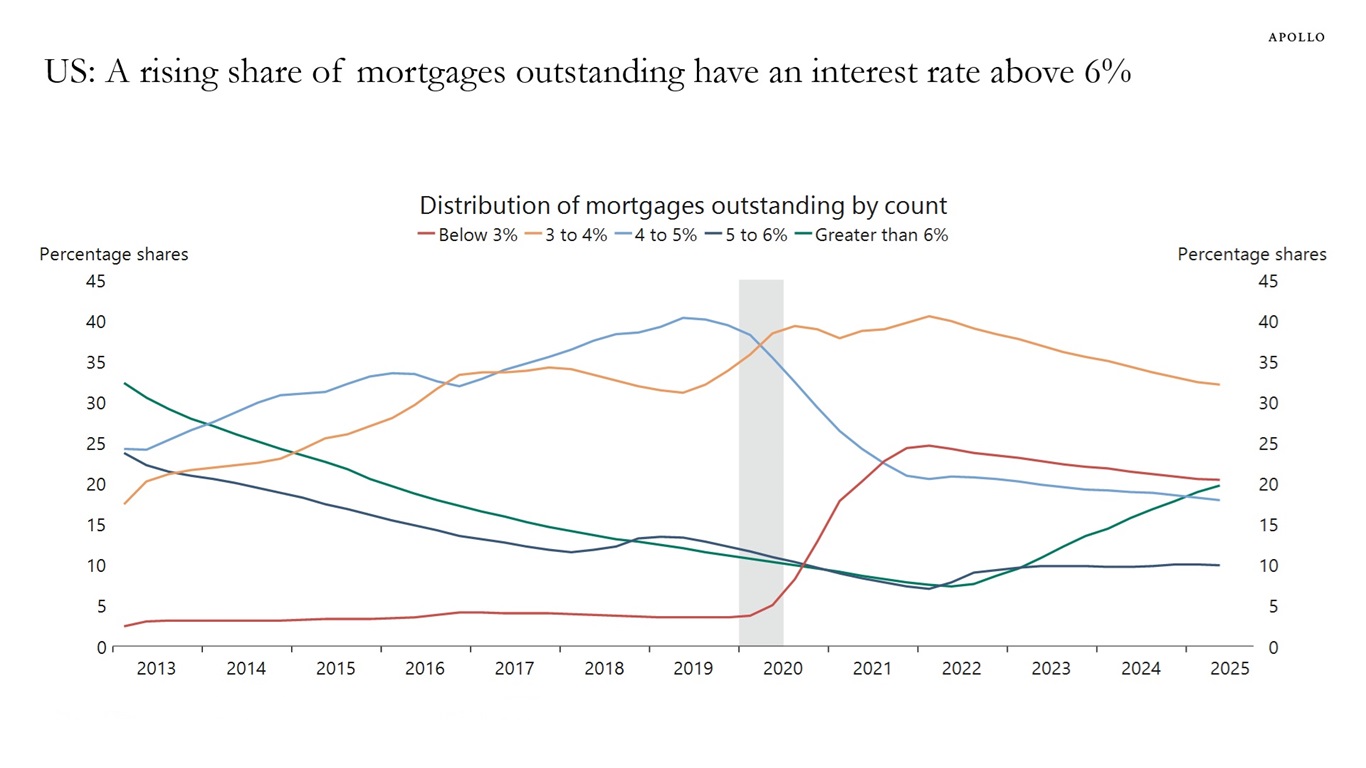

Twenty percent of mortgages outstanding have an interest rate above 6%, see chart below.

In this episode of The View From Apollo, Apollo Global Head of Product Akila Grewal breaks down why private credit’s growth reflects fundamentals, not froth, and how investors are evolving their portfolios to balance liquidity, yield, and long-term opportunity across private markets.