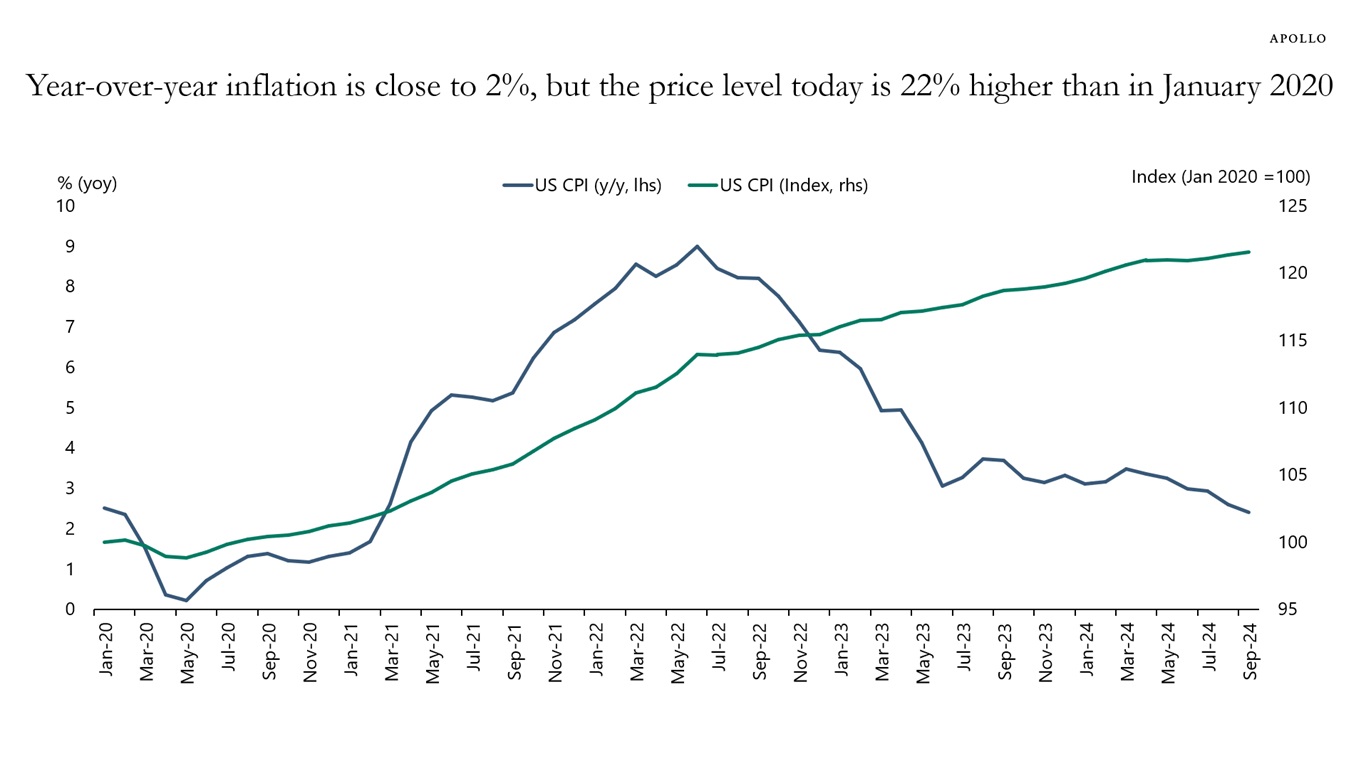

The Consumer Price Index is 22% higher than in January 2020, see chart below.

This means that the prices of all goods and services that consumers spend money on are up, on average, 22%.

For example, since January 2020, the price of cereal is 30% higher, household electricity is 32% higher, and car insurance is 52% higher.

The bottom line is that the Fed’s preferred measure of inflation, namely year-over-year inflation, may be back near 2%, but the living costs for households are still dramatically higher than four years ago.