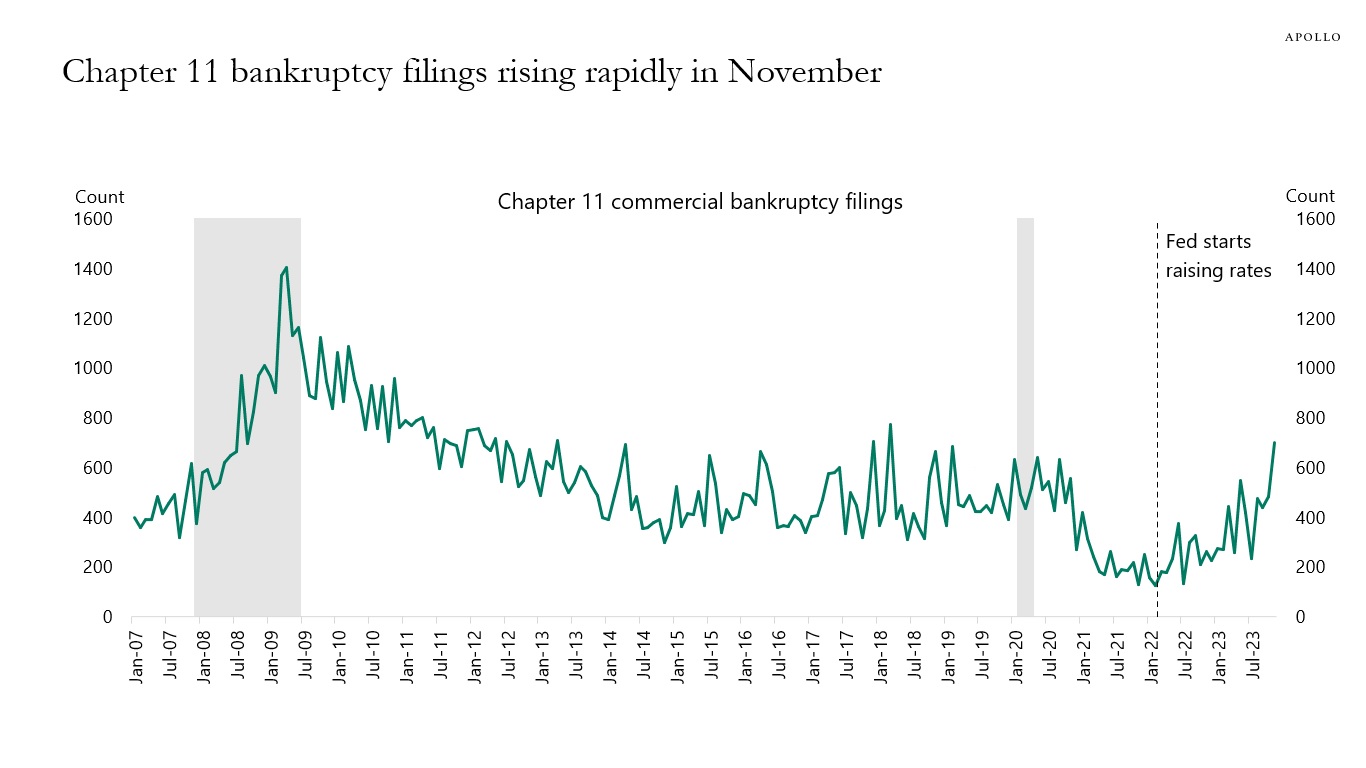

Data for November shows that Chapter 11 bankruptcy filings are trending higher, and Fed hikes continue to bite harder and harder on highly leveraged firms with little or no cash flows in tech, growth, and venture capital, see chart below.

Data for November shows that Chapter 11 bankruptcy filings are trending higher, and Fed hikes continue to bite harder and harder on highly leveraged firms with little or no cash flows in tech, growth, and venture capital, see chart below.

This chart book looks at recent developments in private equity, PE deal activity, private credit, real assets, secondaries, middle markets, and venture capital.

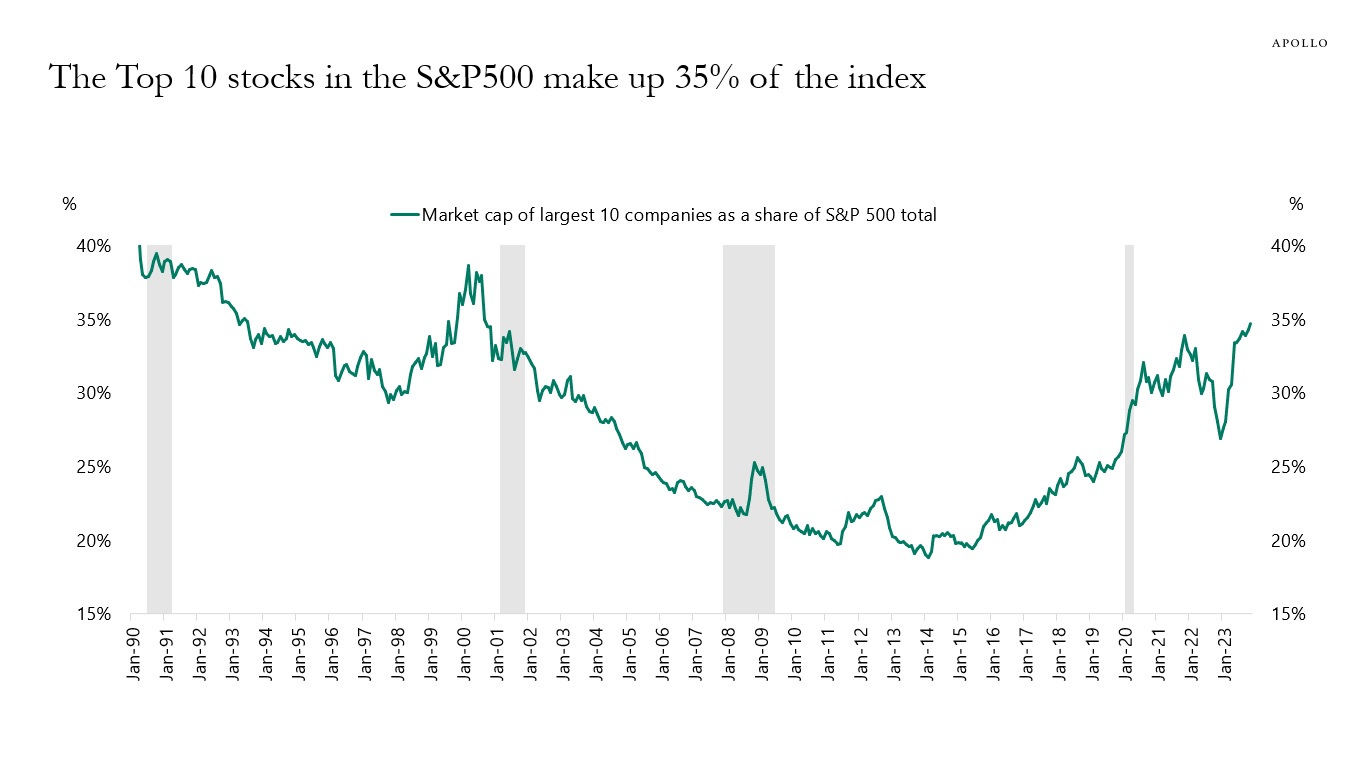

The concentration in the S&P500 continues to increase, and the ten largest stocks now make up 35% of the index, the highest level since the last tech bubble in 2000, see chart below.

With long rates falling in recent weeks, Treasury supply has seemingly become less important as a driver of long rates.

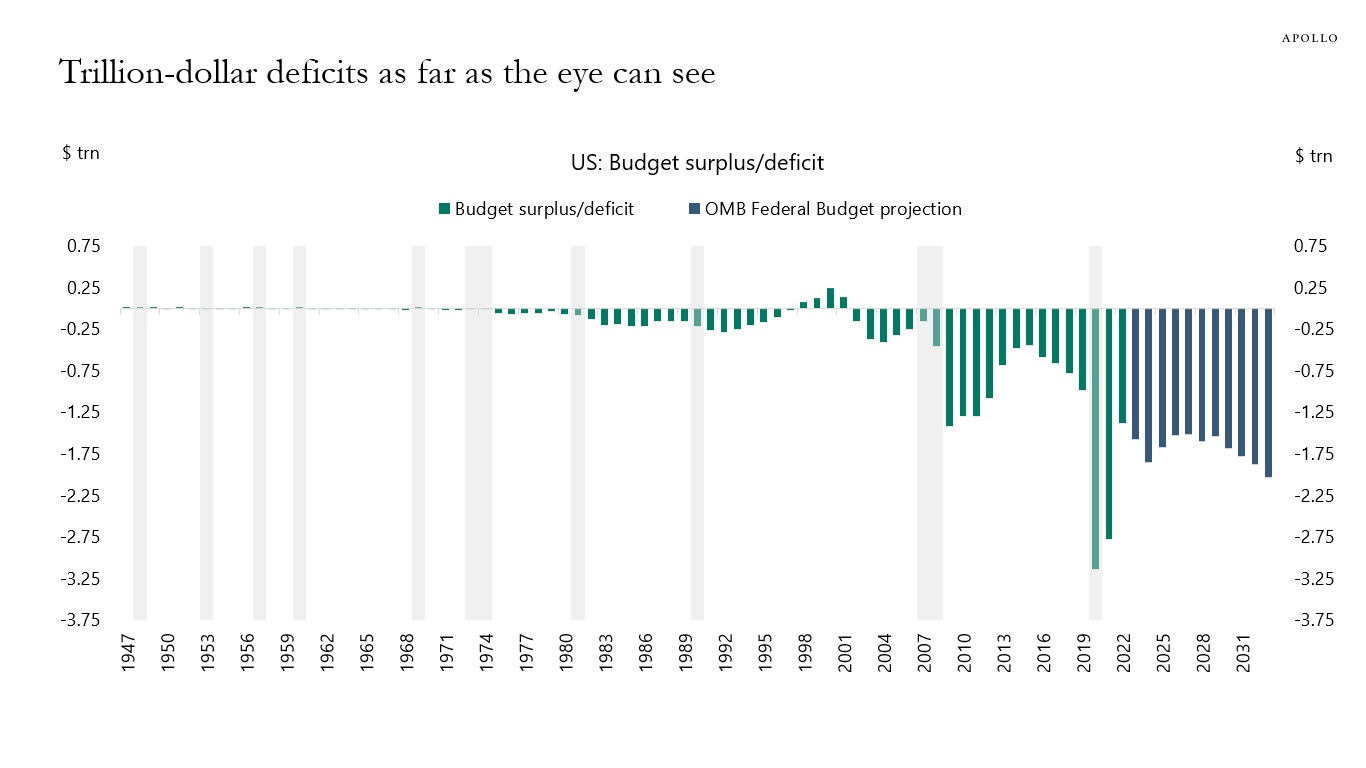

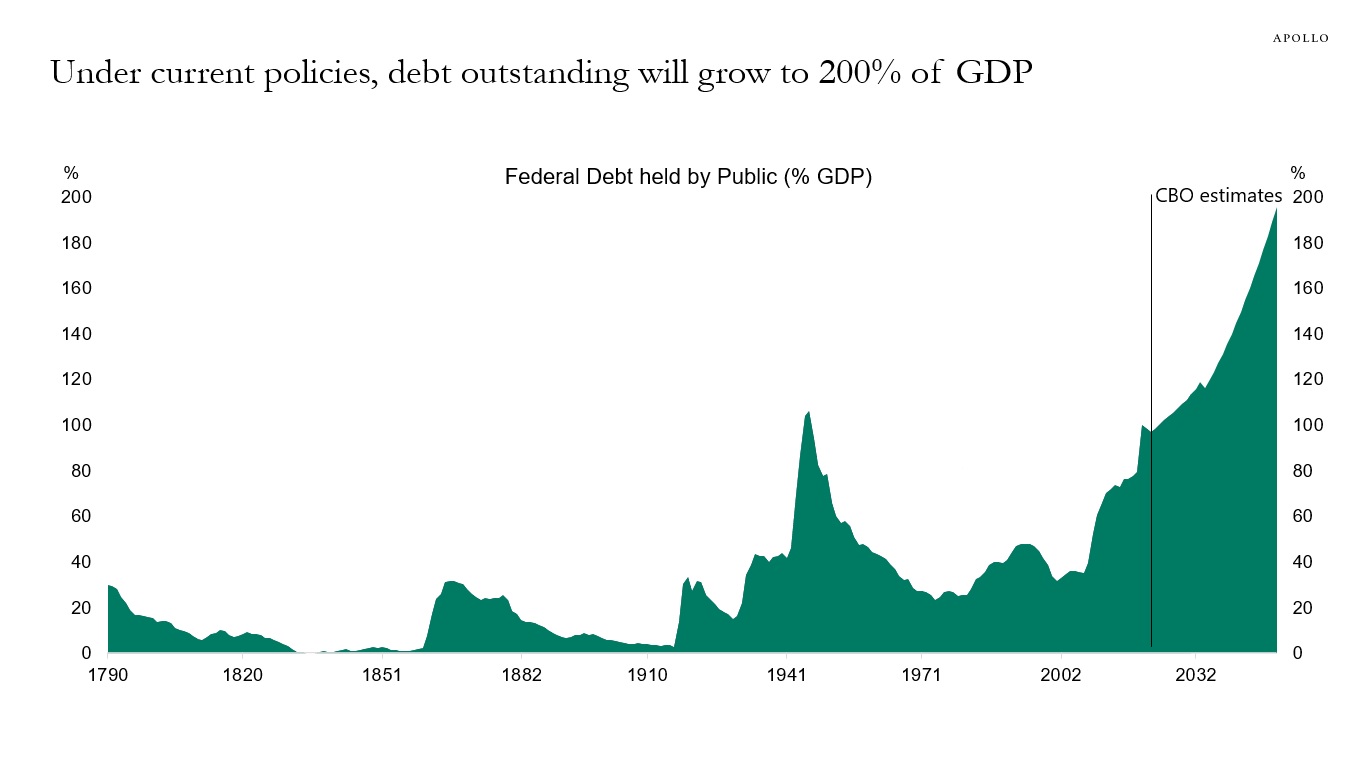

But the fiscal challenges have not disappeared.

Next week, we have a 10-year auction on Monday and a 30-year auction on Tuesday. And looking into 2024, Treasury auction sizes will be, on average, 23% higher than in 2023.

Because of the constant rise in government debt levels, investors need to monitor not only Treasury auctions but also rating agencies and the term premium.

In this short presentation is a collection of relevant data for thinking about the US fiscal situation and the likely transmission channels to financial markets.

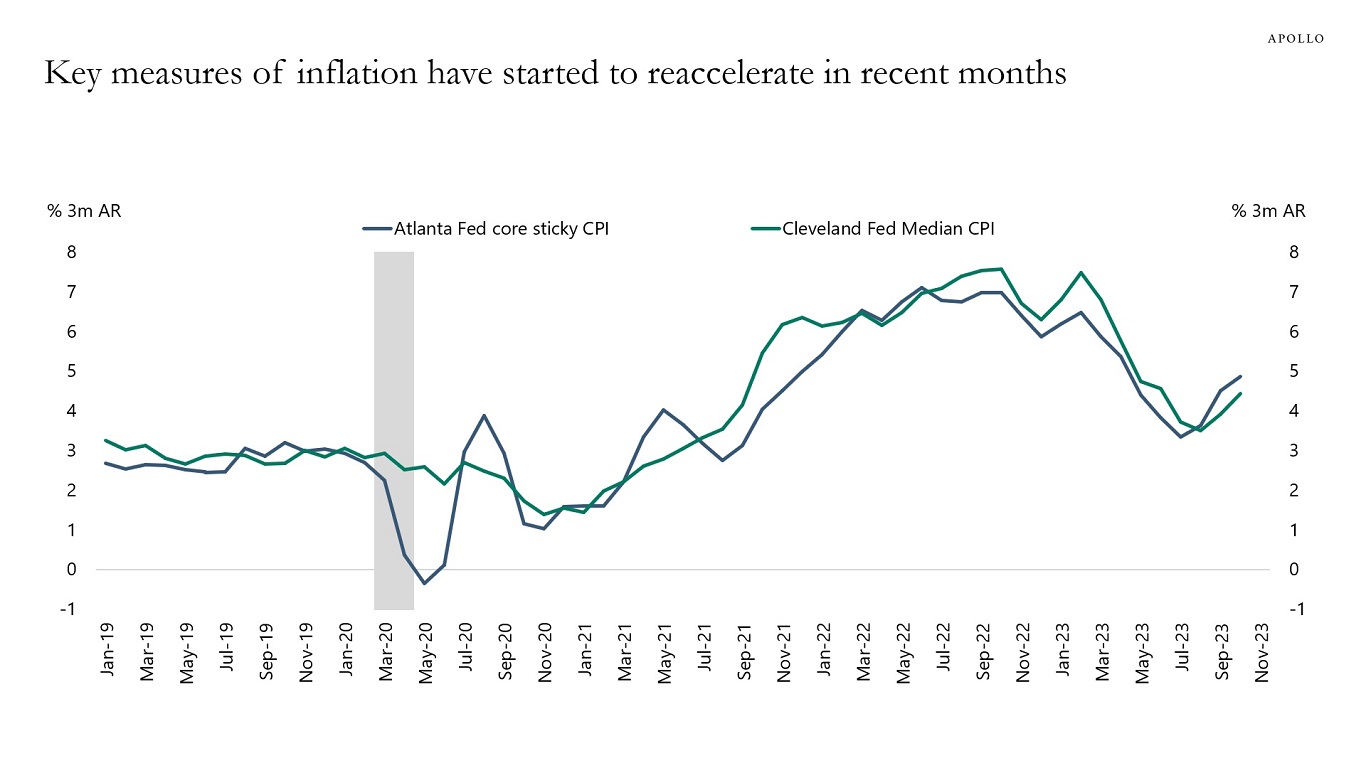

Measures of underlying inflation have started to reaccelerate in recent months, and this is a problem for the Fed, see chart below.

The Fed cannot and will not turn dovish as long as inflation remains significantly above the FOMC’s 2% inflation target, particularly when underlying inflation is trending higher.

The consequences are that delinquency rates on credit cards and auto loans will continue to increase, corporate default rates will continue to move higher, and bank lending will continue to trend lower.

In other words, we are entering a period with weaker economic data where the Fed will stay on hold.

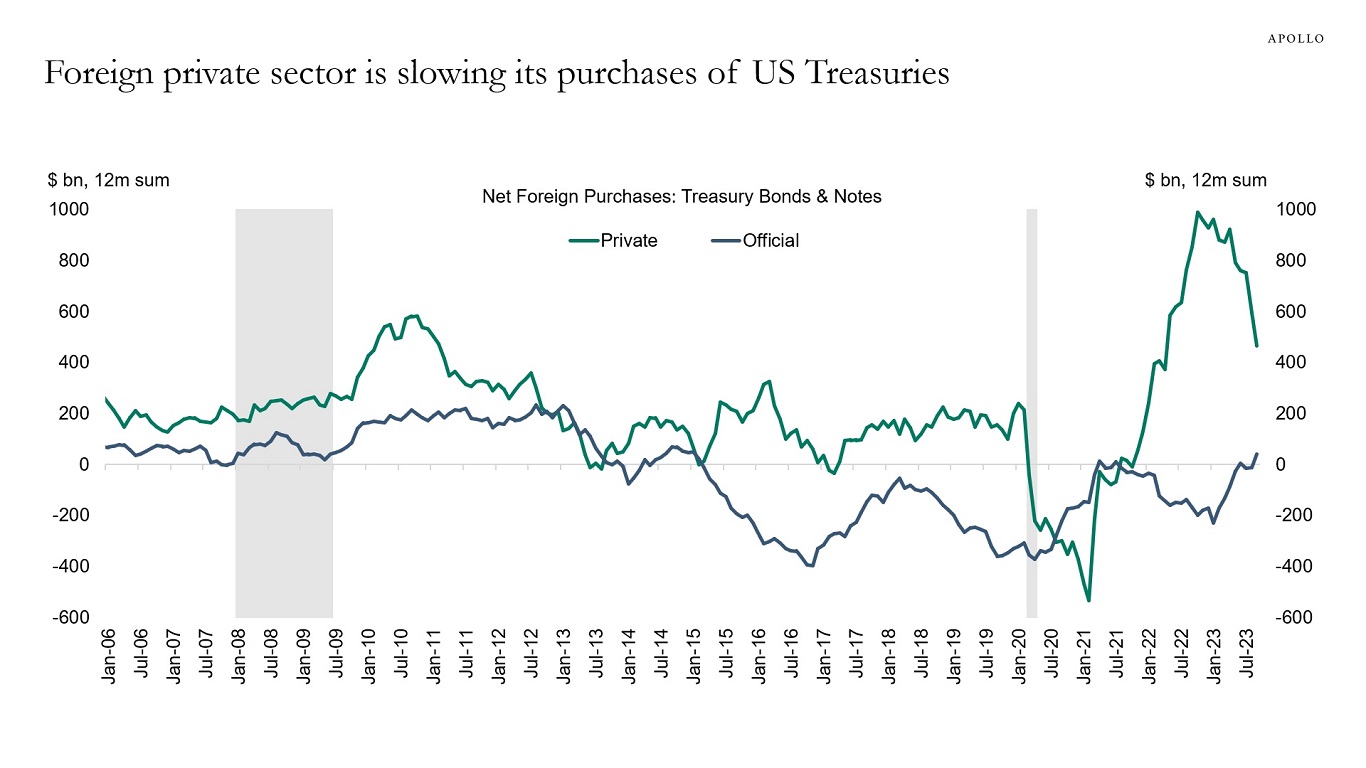

Since the Fed started raising rates, the biggest foreign buyer of US Treasury bonds has been the yield-sensitive private sector, see the first chart below.

But with rates peaking, the foreign private sector has been slowing purchases, see chart below.

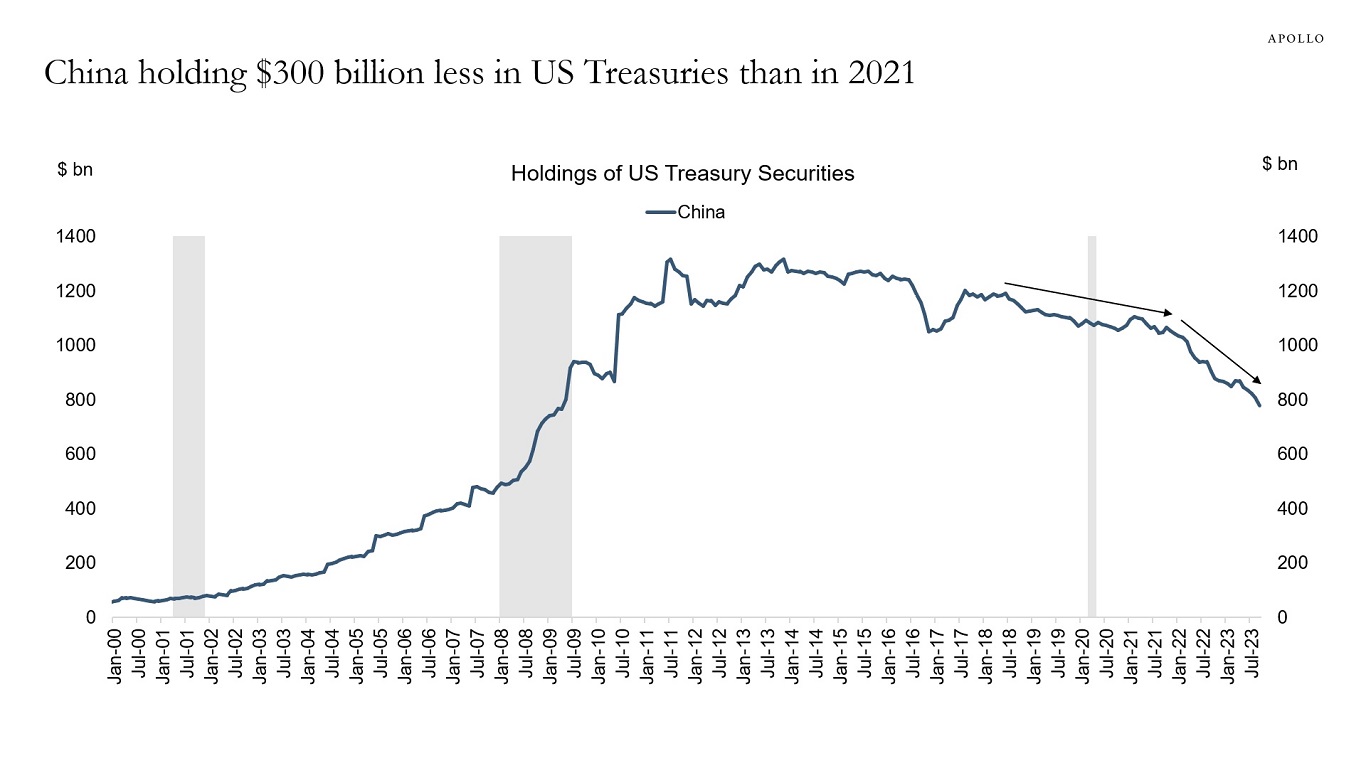

The foreign official sector has been a net seller during this rate cycle. This is also the case for China, where holdings of US Treasuries have declined by $300 billion since 2021, see the second chart below.

With growth slowing in China due to demographic headwinds, slowing exports, and a deflating housing market, demand for US Treasuries from the foreign official sector will likely remain weak.

Our 2024 outlook for China is available here.

Looking across the wage distribution shows that wage inflation remains sticky between 4% and 5%, see chart below.

The FOMC would likely look at this chart and conclude that a higher unemployment rate is needed to get wage inflation down to levels consistent with the Fed’s 2% inflation target.

Listen to Apollo Chief Economist Torsten Slok and Vice Chairman of Global Real Estate Philip Mintz discuss where they see opportunities amid a still-volatile macroeconomic environment. They cover a lot: credit, equity, and real estate relative valuations; real-estate investments in the sunbelt and other “non-gateway” cities; what portfolio allocations might look like in 2024, and much more.

The consensus expects nonfarm payrolls on Friday to come in at 180,000 jobs added in November. This bullish consensus estimate is likely based on one single indicator, namely jobless claims.

But other indicators are showing ongoing signs of weakness in labor demand, which would point to a weaker employment report for November:

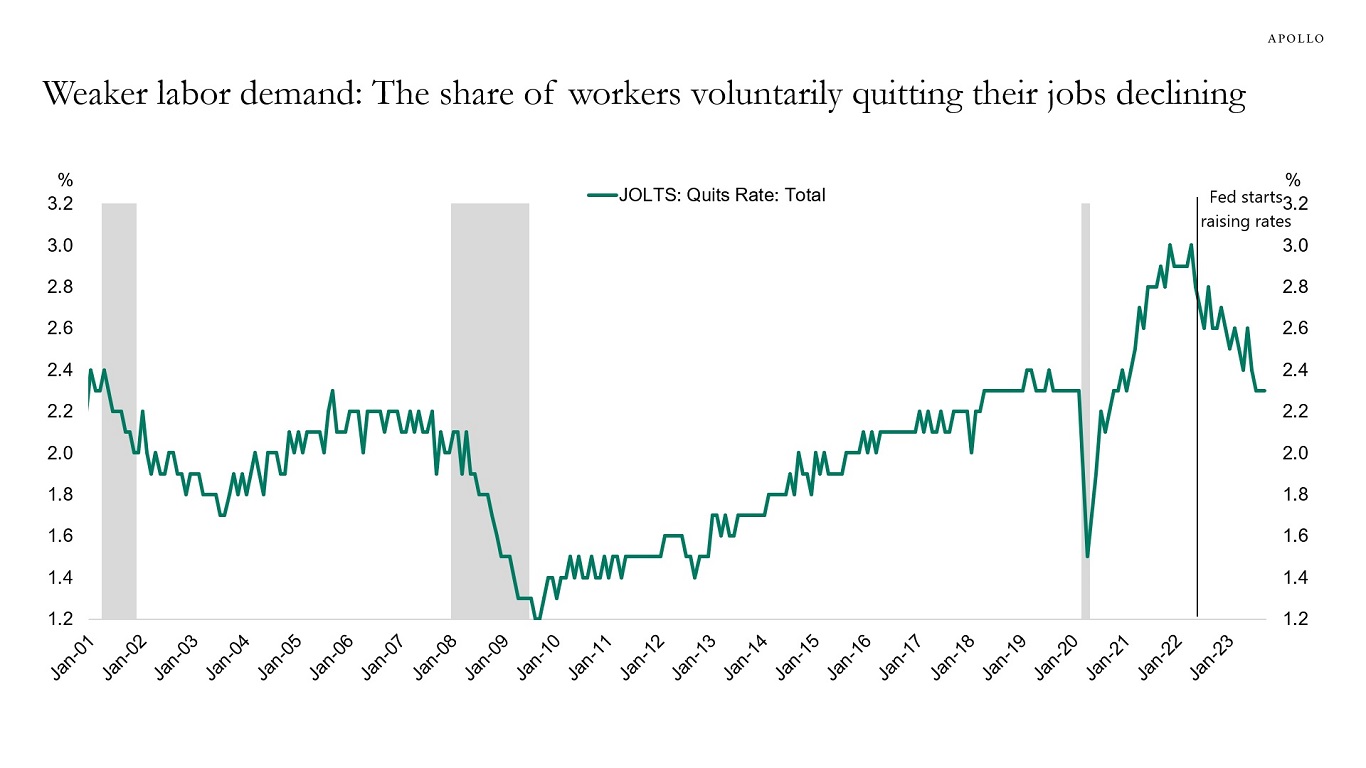

1) The quits rate, i.e., the share of workers voluntarily quitting their jobs every month, continues to trend lower, see the first chart below.

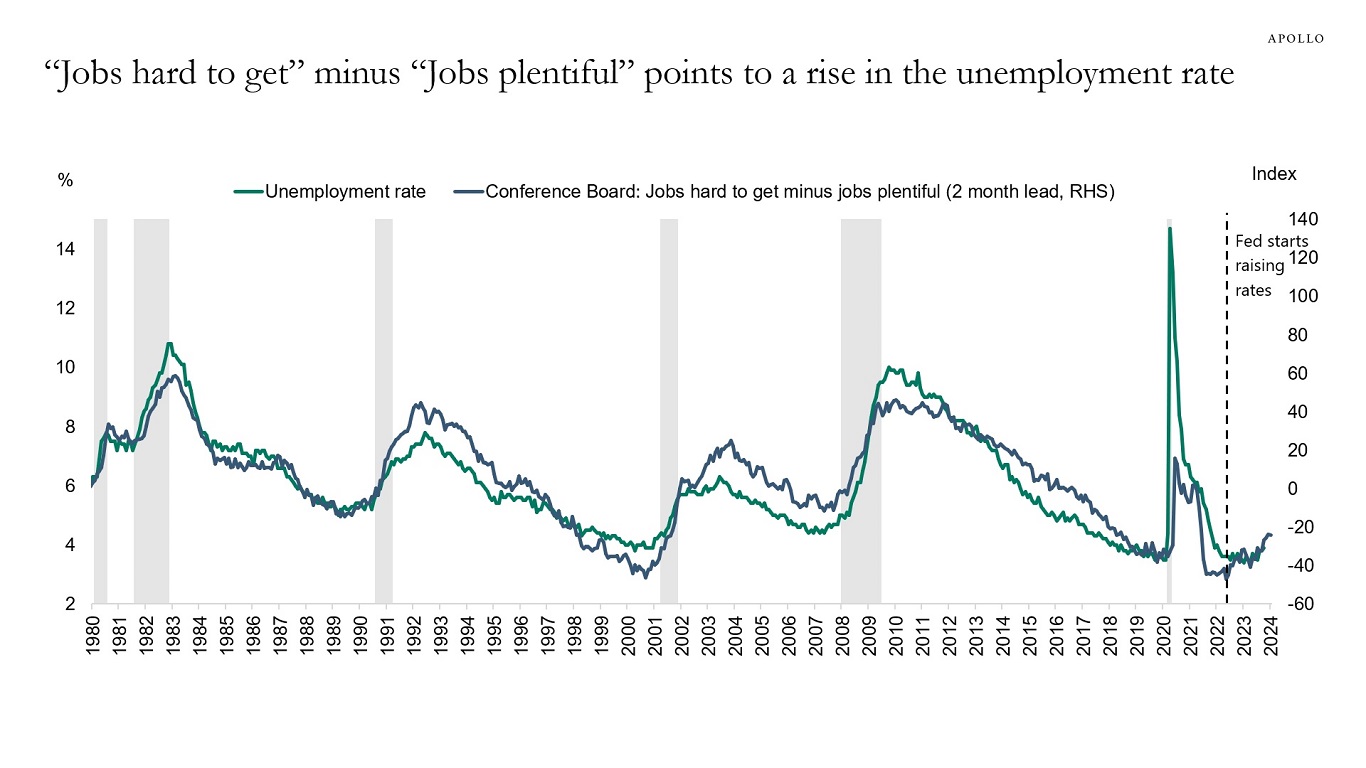

2) More consumers are starting to say that it is harder to find a job, see the second chart below.

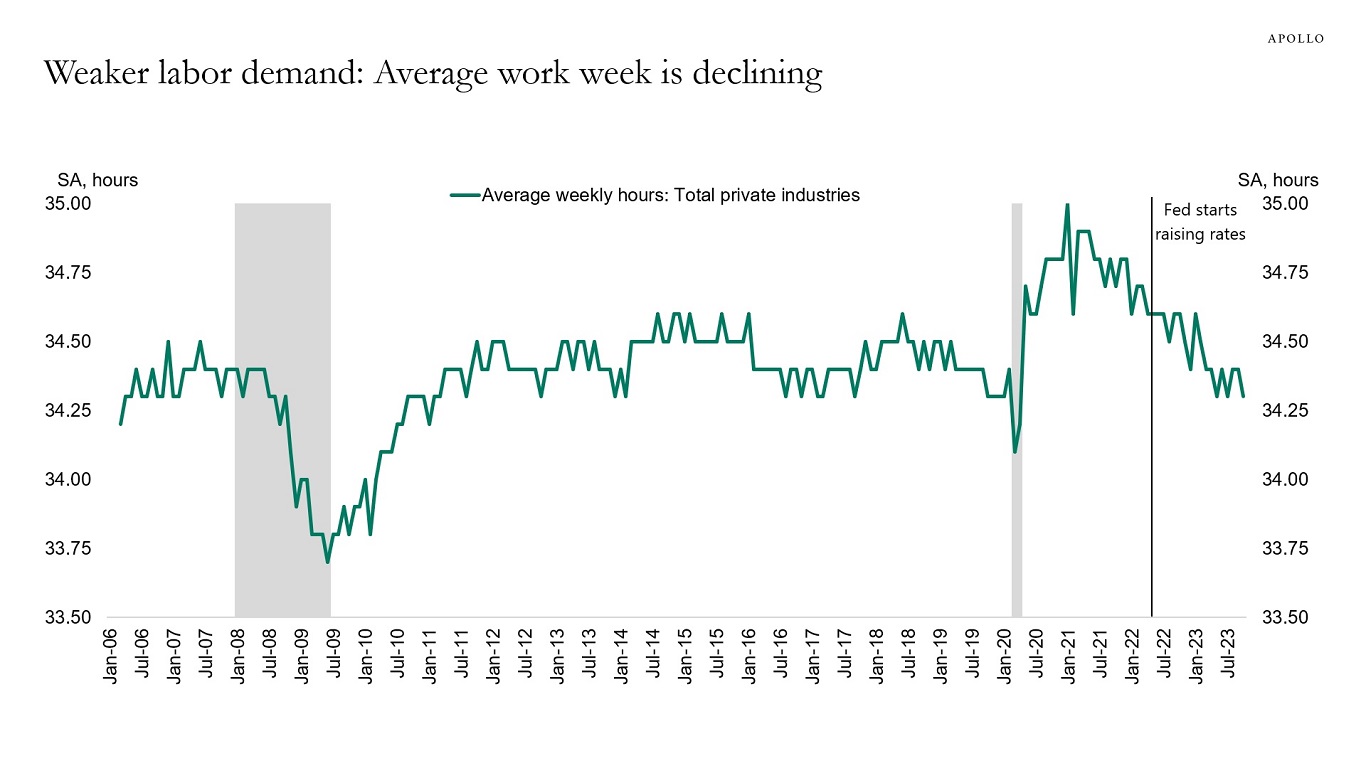

3) The work week for private sector workers has been declining, suggesting labor demand is weaker, see the third chart.

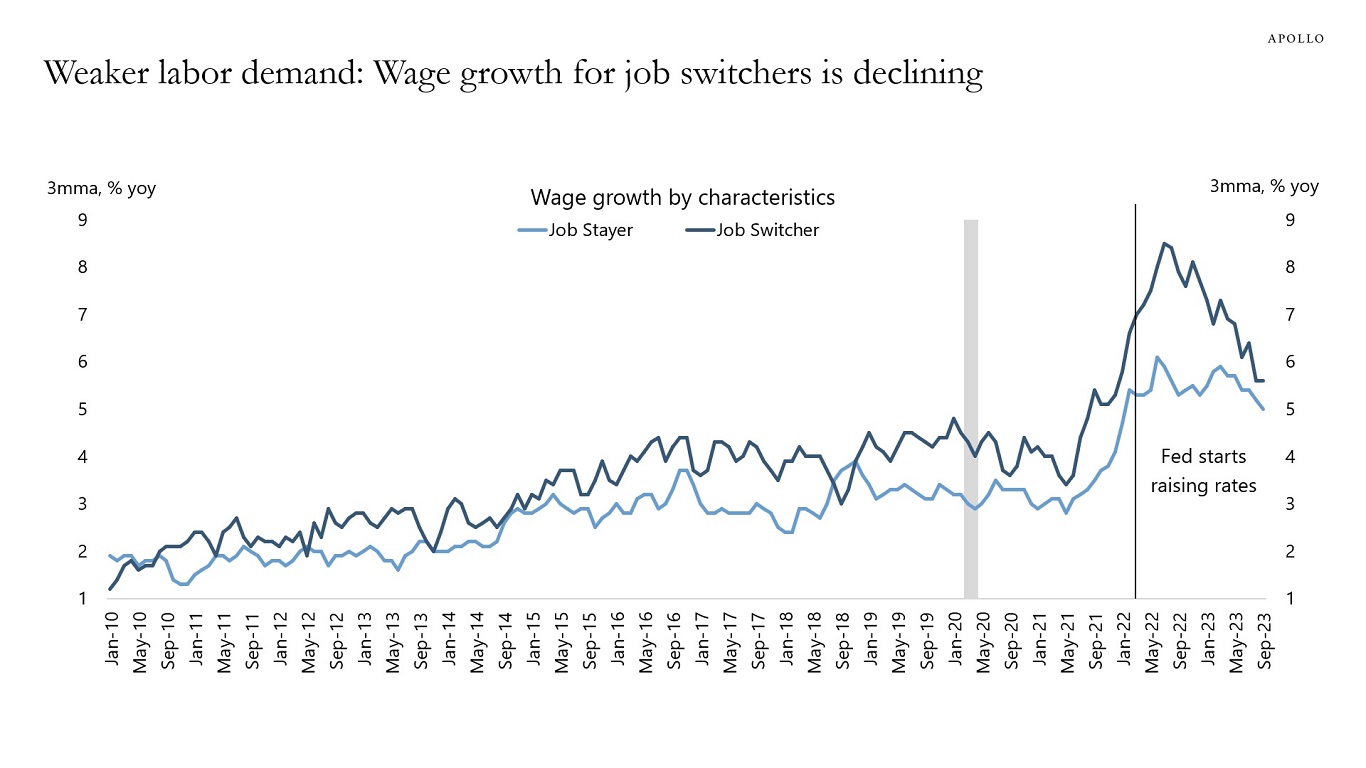

4) There is now very little difference between wage growth of job switchers and job stayers, suggesting that job switchers are no longer able to get big pay increases, see the fourth chart.

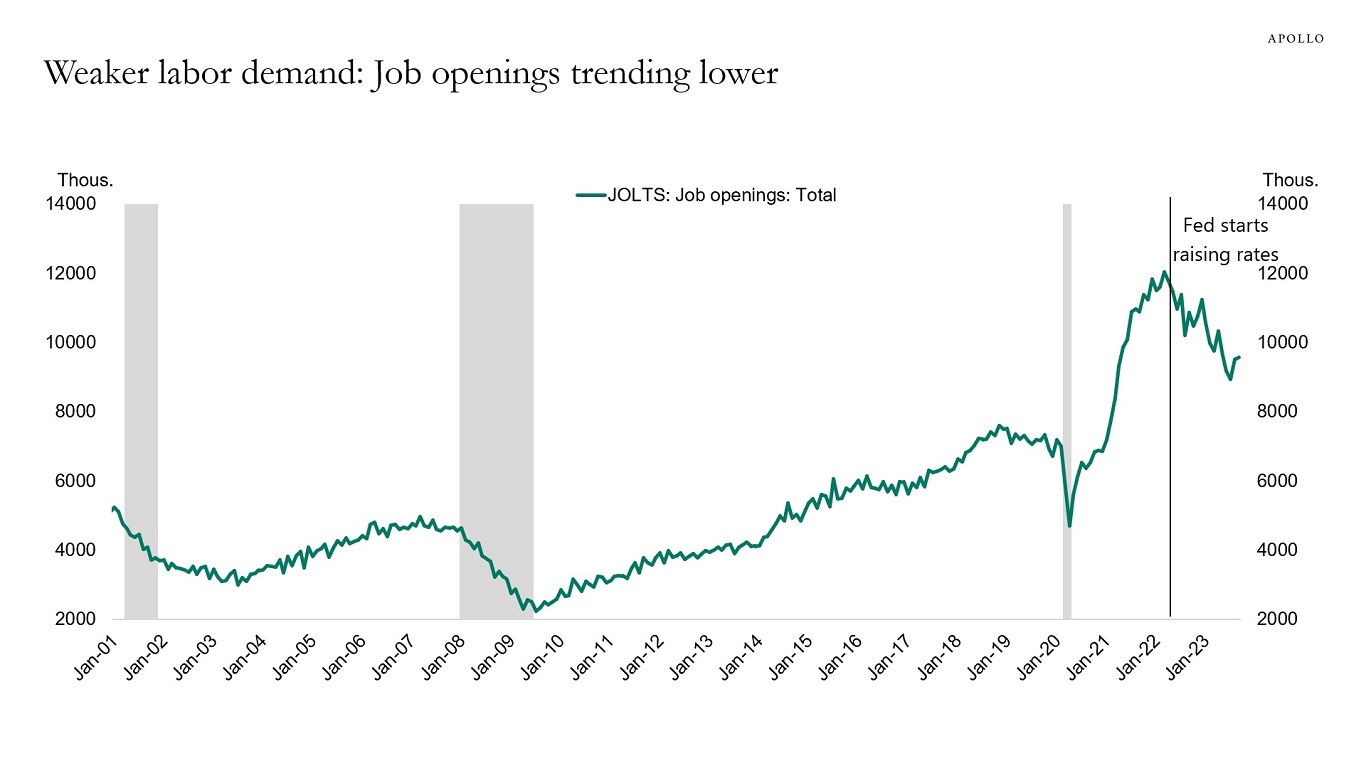

5) The number of job openings has decreased since the Fed started raising interest rates, see the fifth chart.

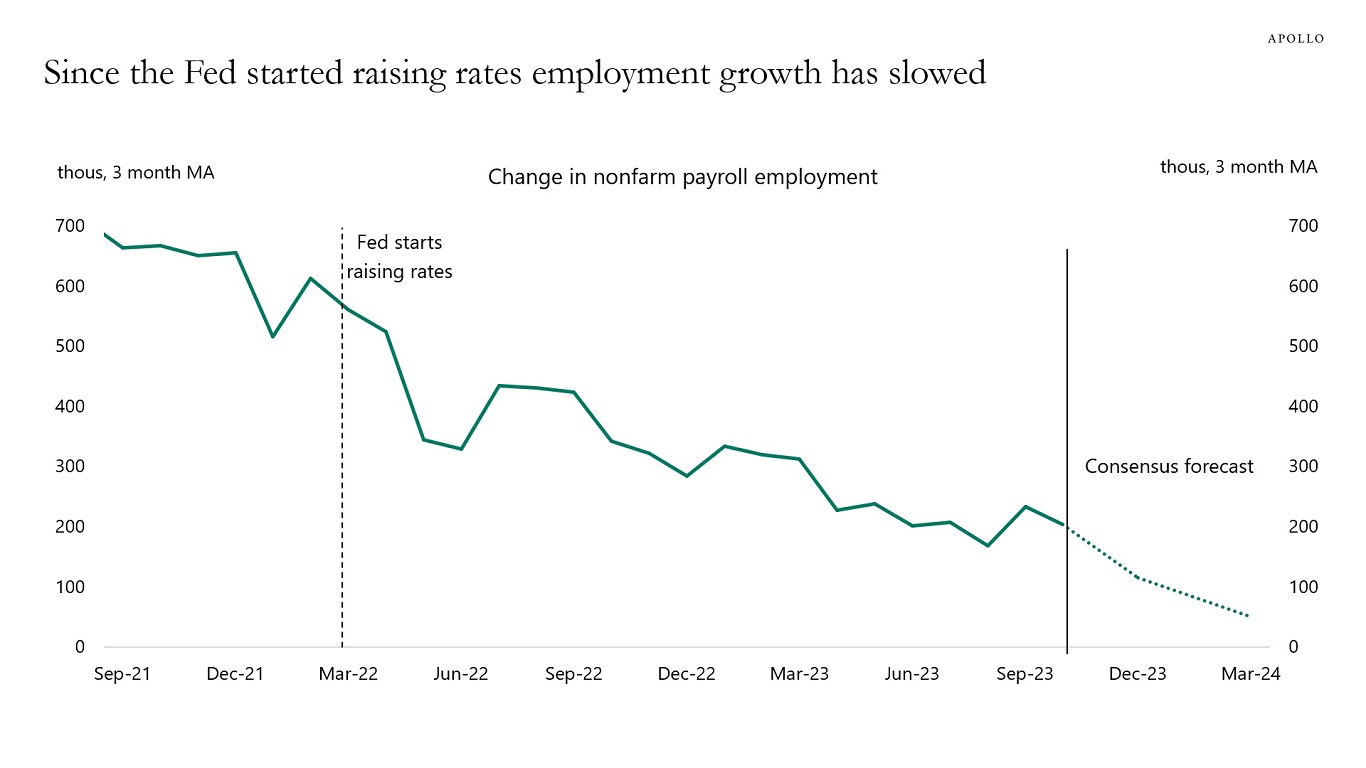

6) The pace of job growth has declined as the Fed has raised interest rates, and with the Fed on hold well into 2024, this trend will likely continue, see the sixth chart.

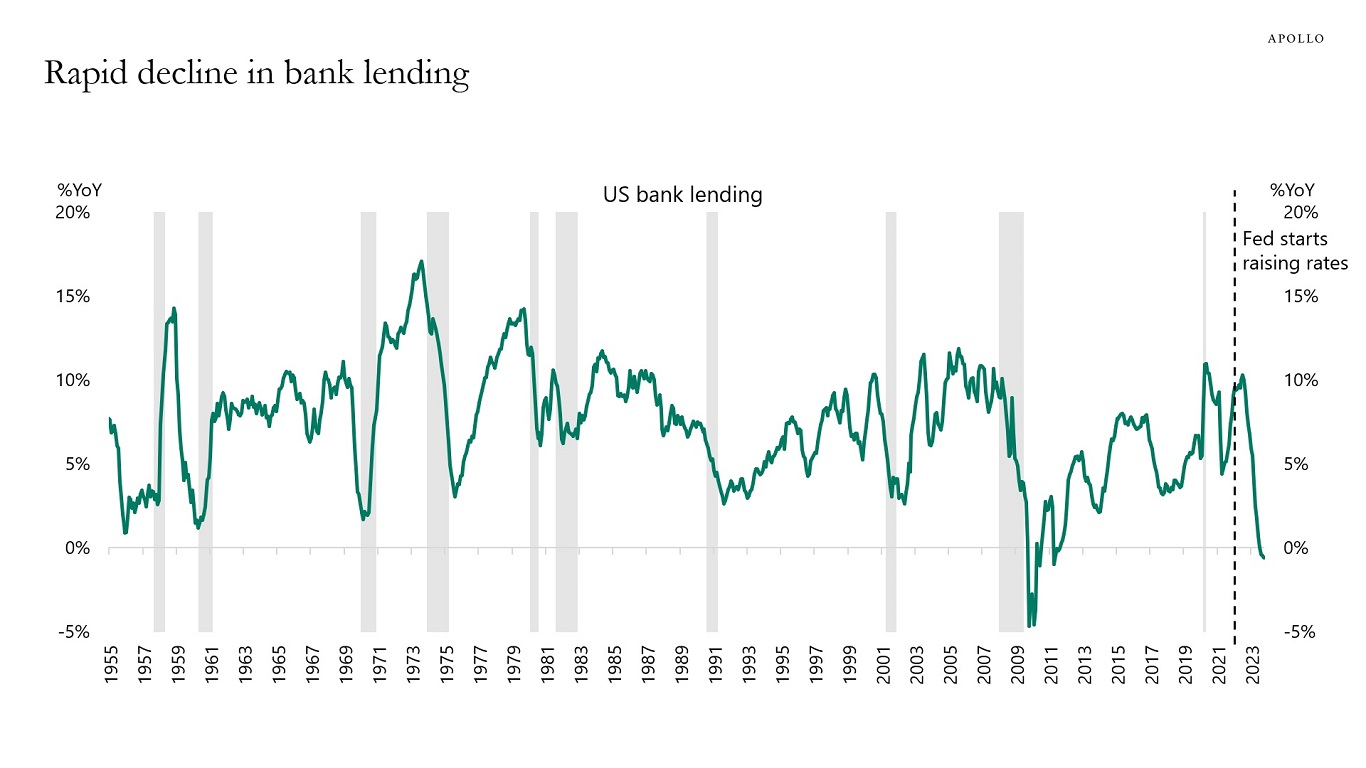

Since the Fed started raising rates, lending growth has slowed, see chart below. This is not surprising. The idea with raising interest rates is to make it more expensive for firms and households to borrow. Our latest outlook for the banking sector is available here.