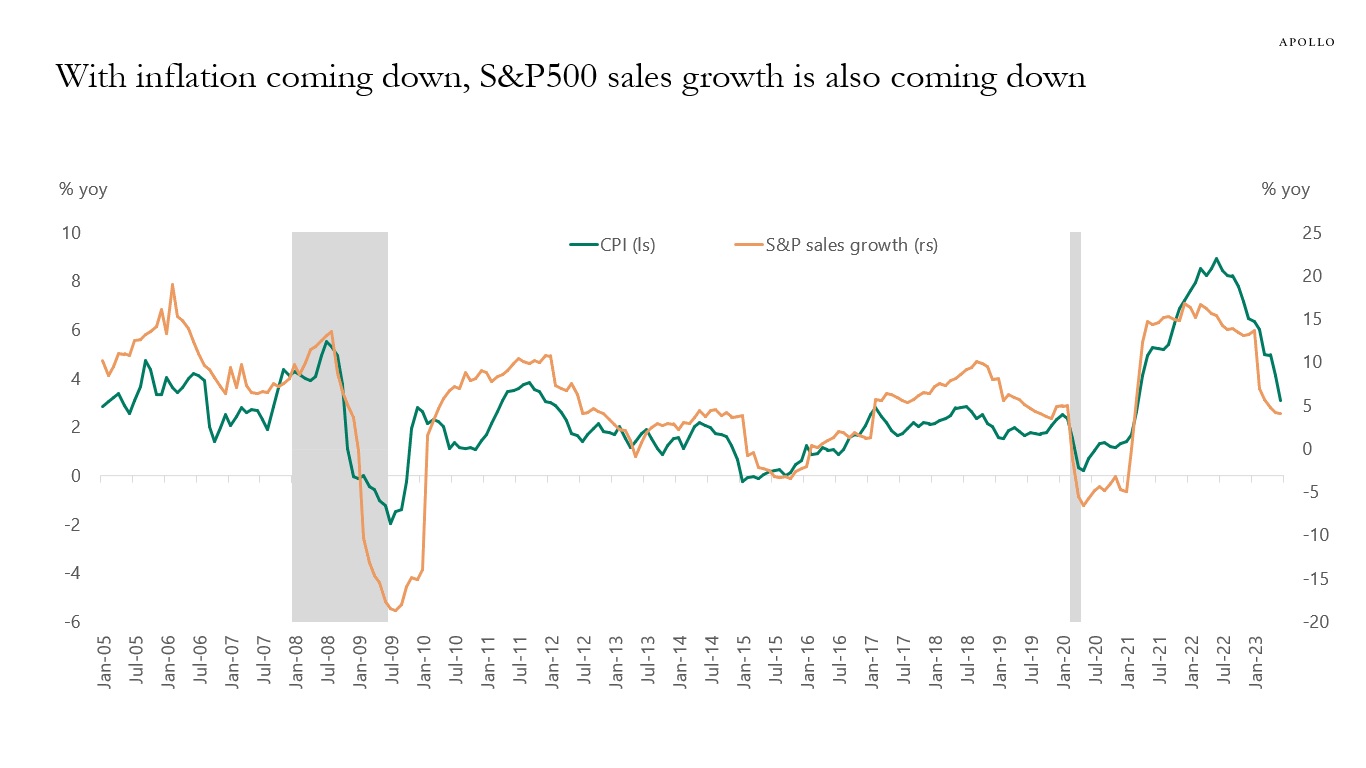

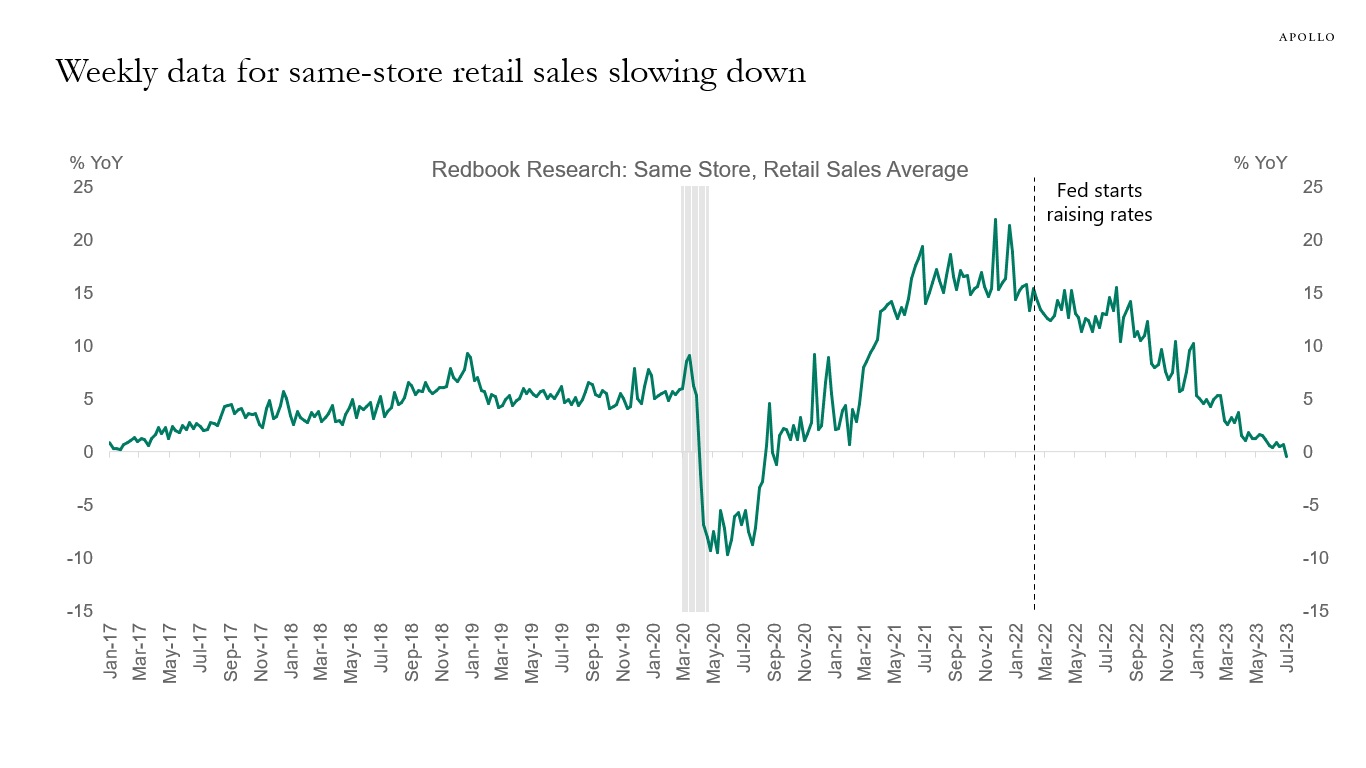

What matters for bond markets and the Fed are real variables, including unemployment, real GDP growth, and real consumer spending.

What matters for the stock market is nominal variables, including earnings growth, sales growth, and output prices.

The chart below shows that with inflation coming down, we should also expect to see a slowdown in nominal sales growth and nominal earnings growth.