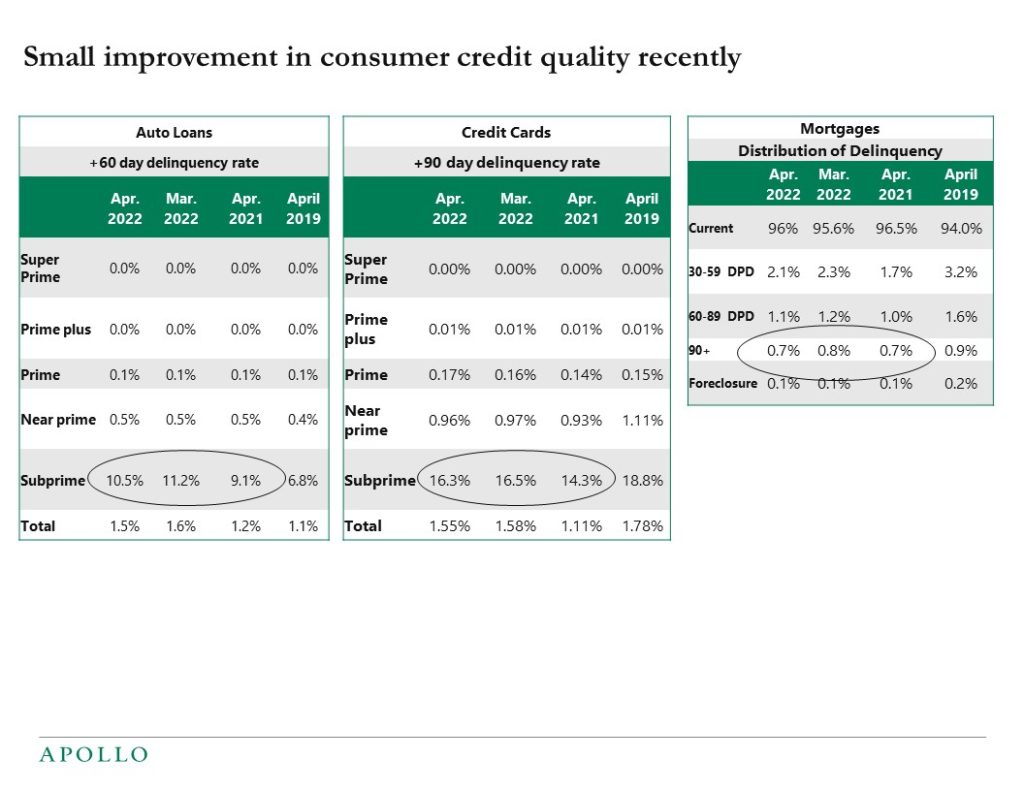

The latest data for delinquency rates for auto loans, credit cards, and mortgages show that consumer credit quality is still good, including for lower FICO scores, see table below.

With the Fed hiking rates and financial conditions tightening, and the economy slowing, we will, over the coming quarters, likely begin to see more broad-based signs of weakness.