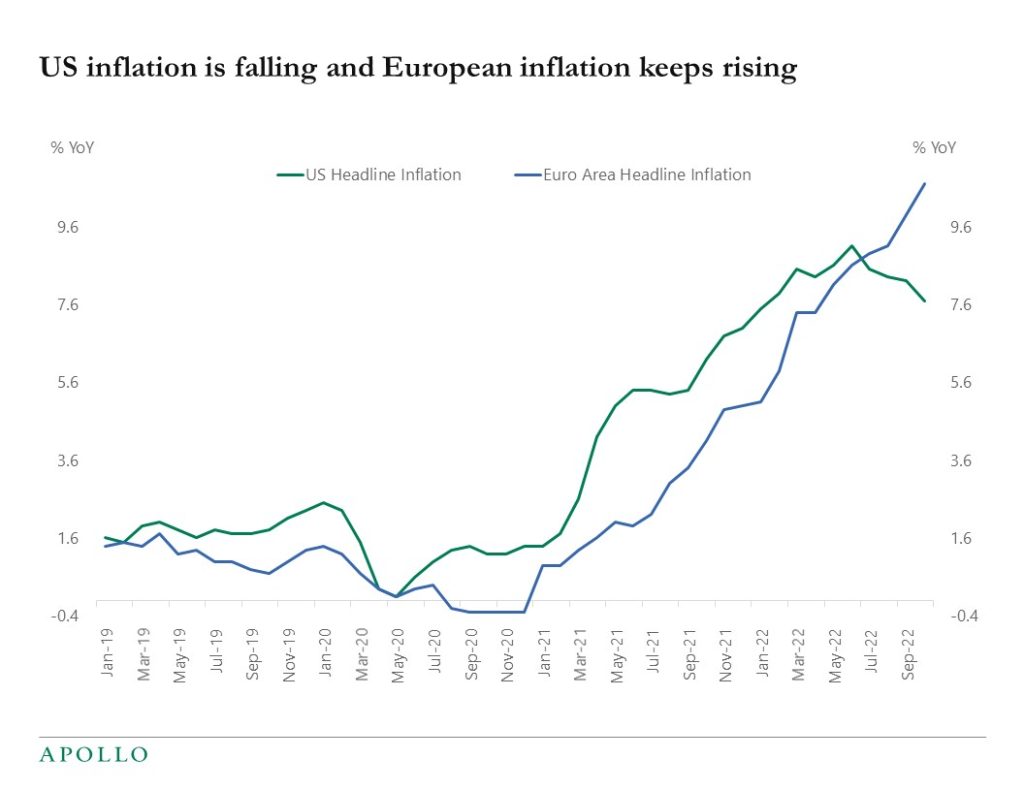

The difference between inflation in the US and Europe is noteworthy, see chart below.

Europe is experiencing stagflation with high inflation and the economy in a recession.

The US is seeing falling inflation and still solid growth.

Our set of daily and weekly indicators is available here.