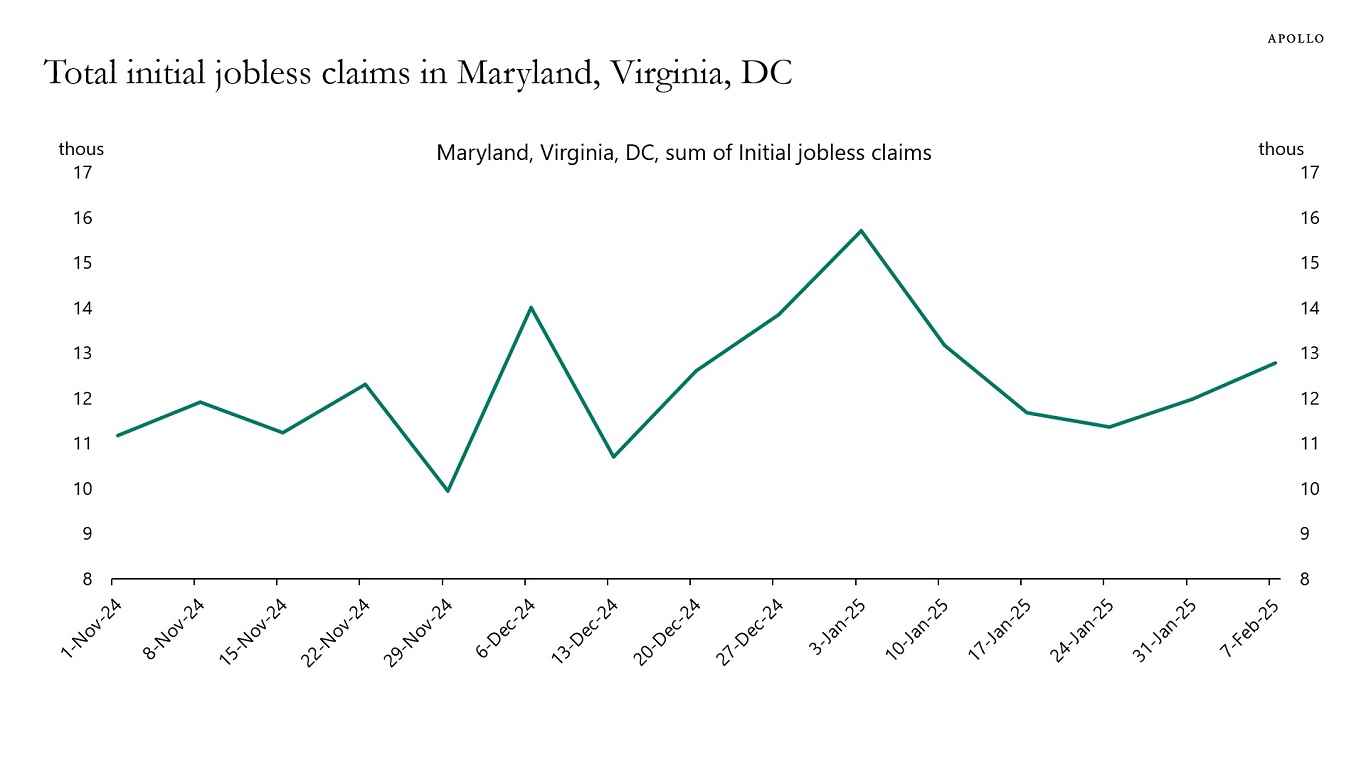

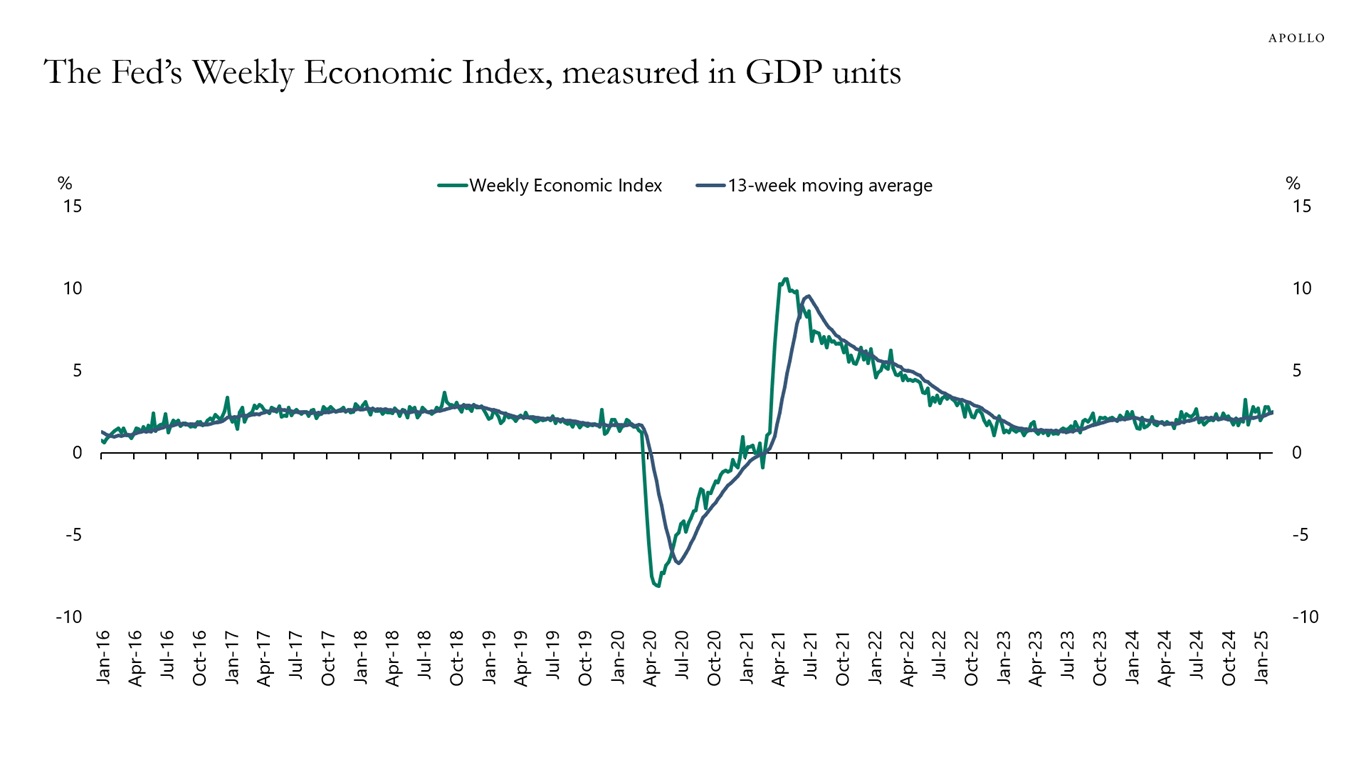

We are watching the weekly data for the number of people who file for unemployment benefits in Washington DC, Maryland, and Virginia, and any impact federal government layoffs may have on nationwide jobless claims, see chart below. This data comes out every Thursday at 8:30 a.m. ET.