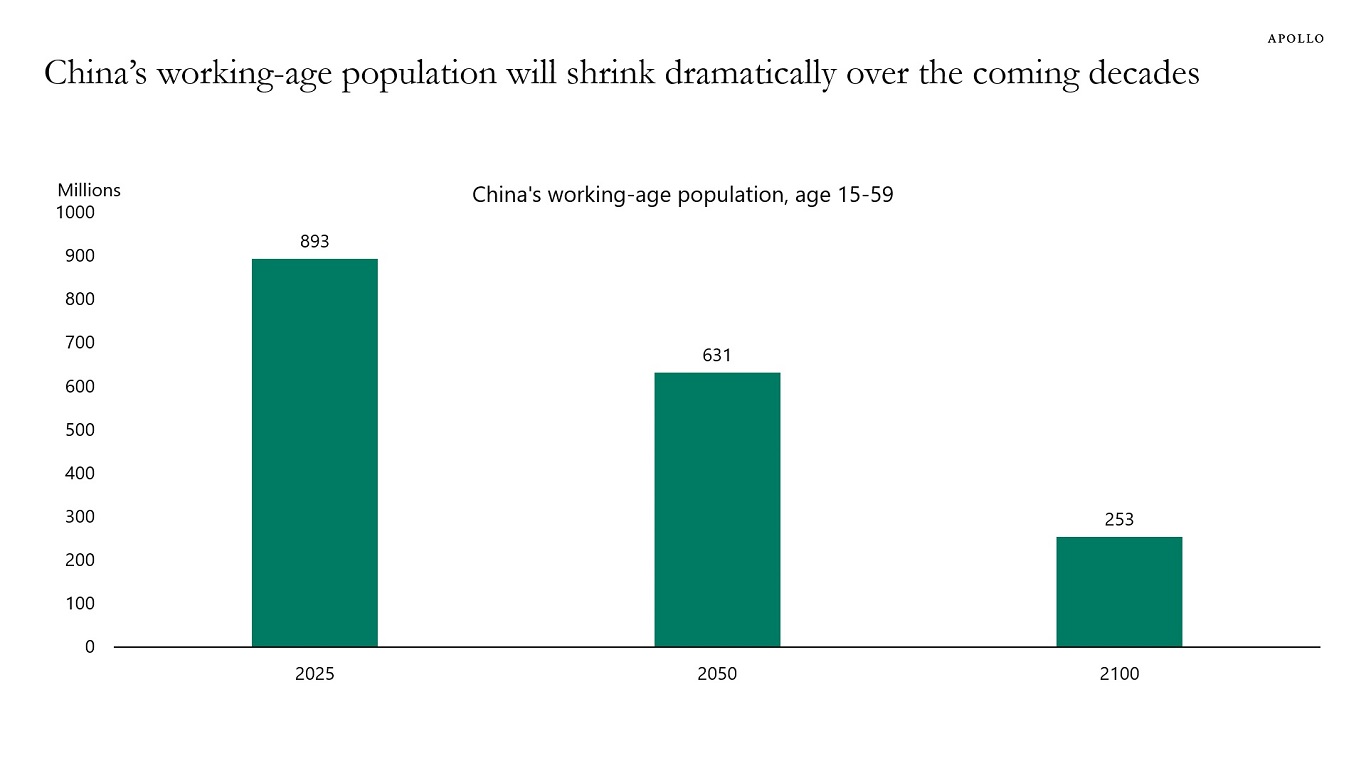

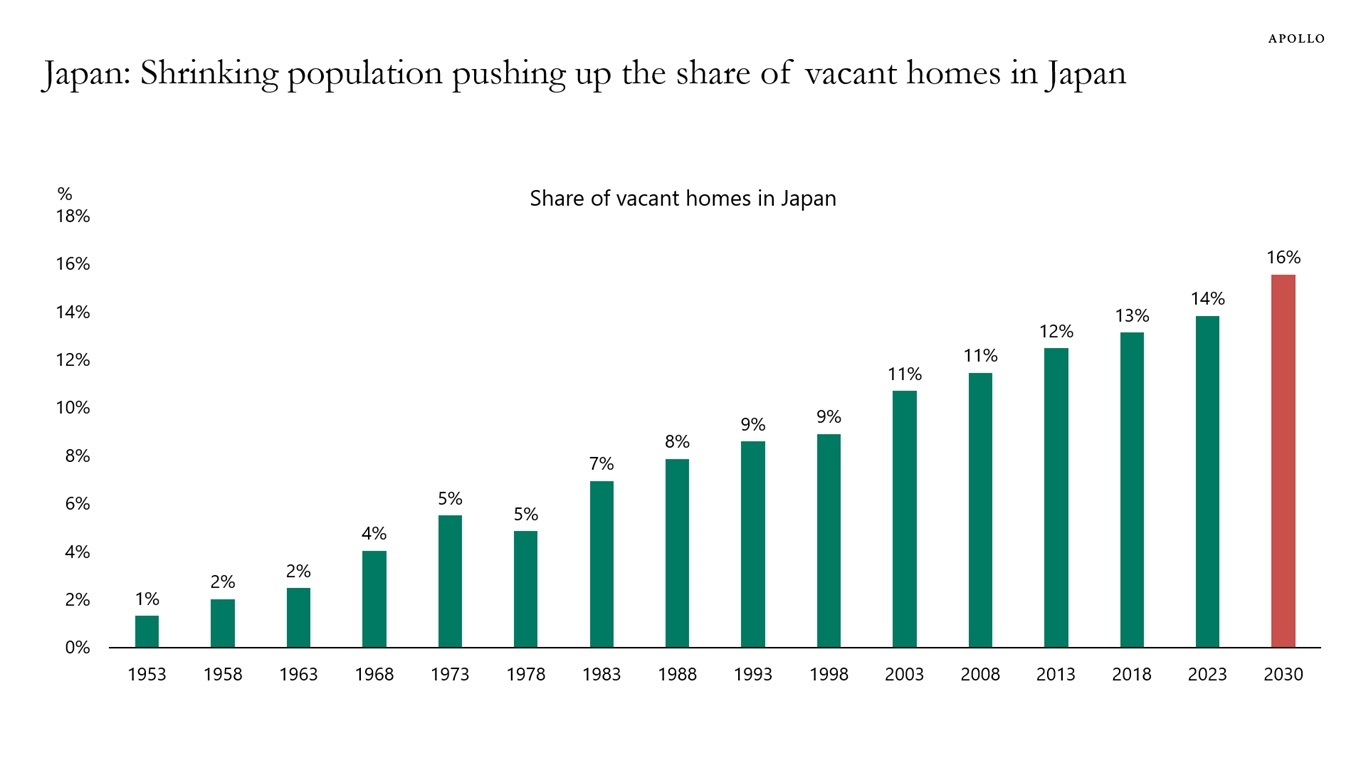

China’s working-age population will shrink dramatically over the coming decades, driven by the lagged effects of the one-child policy, an aging population, and a significant decline in fertility rates—which currently stand at 1.09 births per woman, far below the 2.1 needed to maintain population size.

This decline in the working-age population will have significant implications for economic growth, the fiscal outlook due to an aging population, and investment and productivity growth.

These risks to China’s long-term outlook are, in many ways, similar to those we have seen in Japan in recent decades.