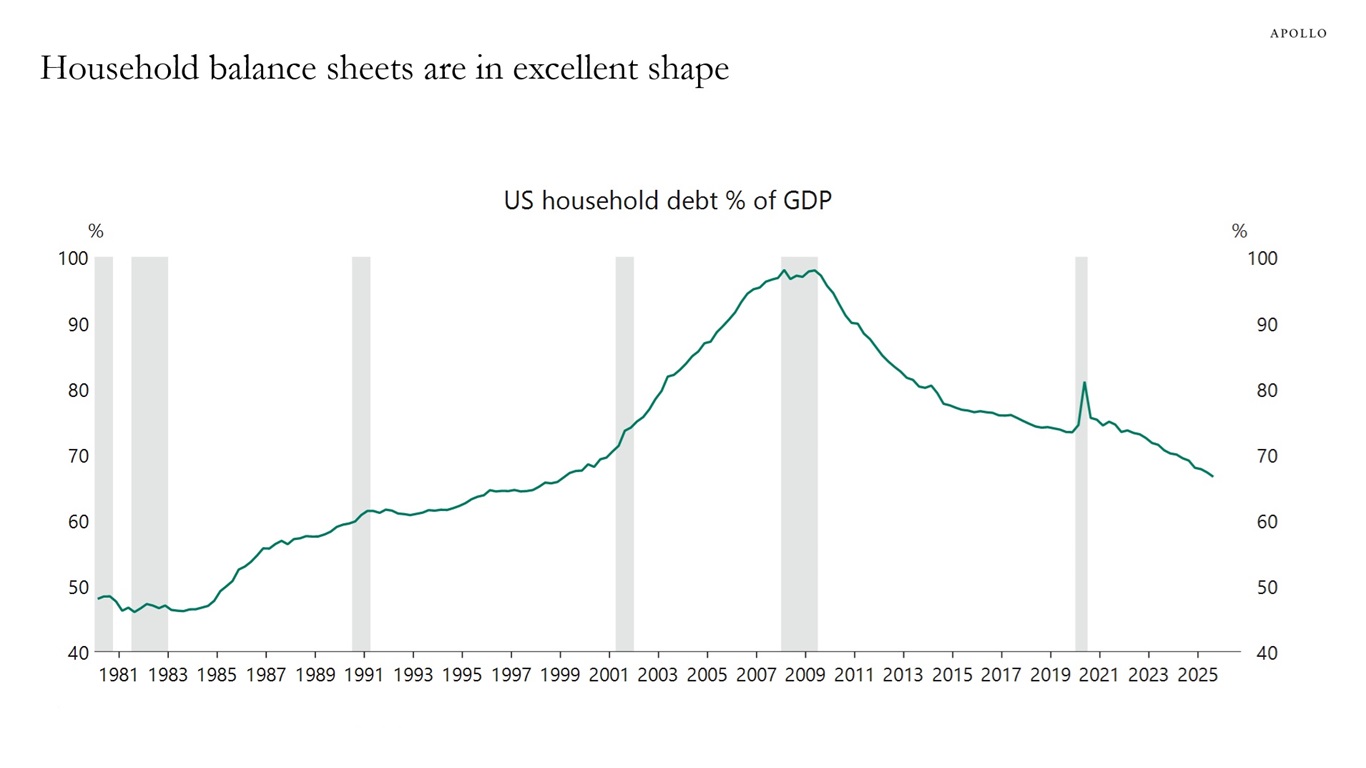

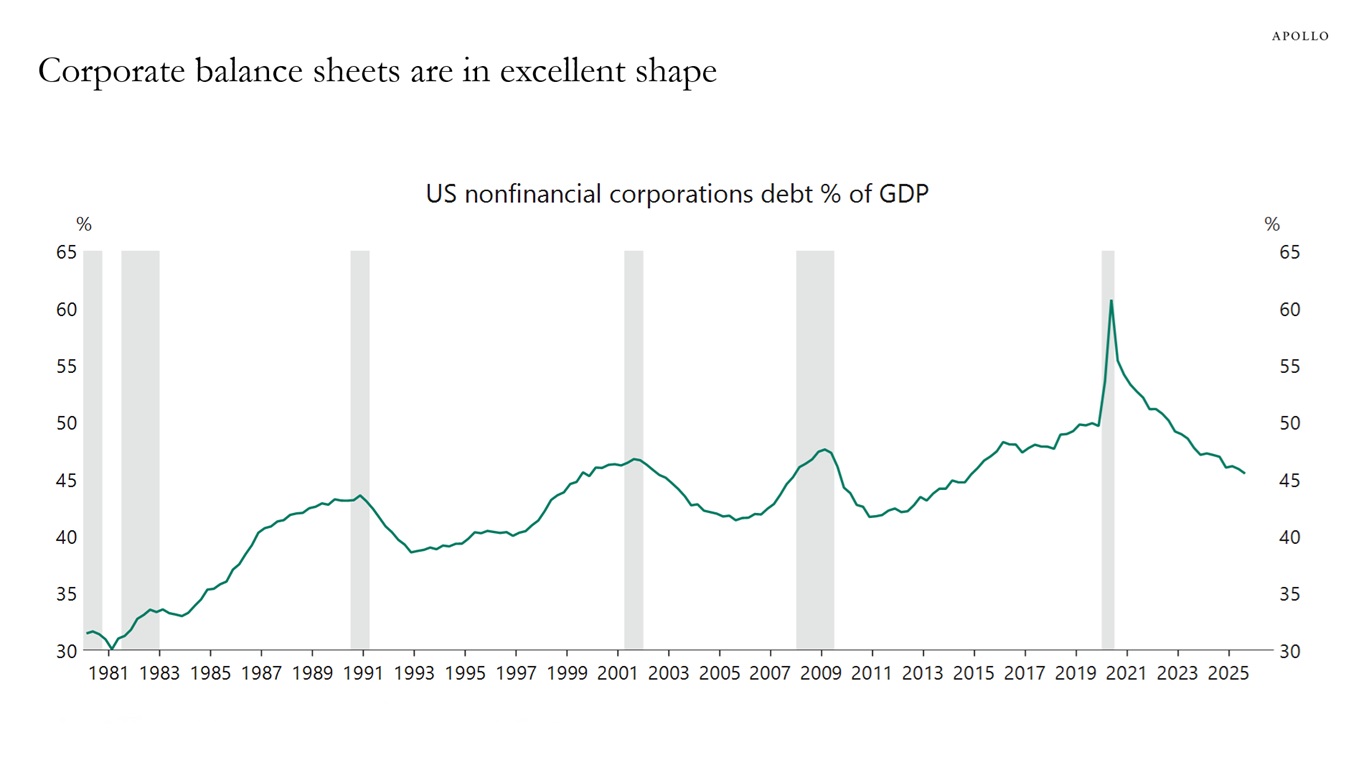

The private sector in the US is in really good shape. Households have been deleveraging since the 2008 financial crisis, see the first chart. The corporate sector has been deleveraging since COVID, see the second chart.

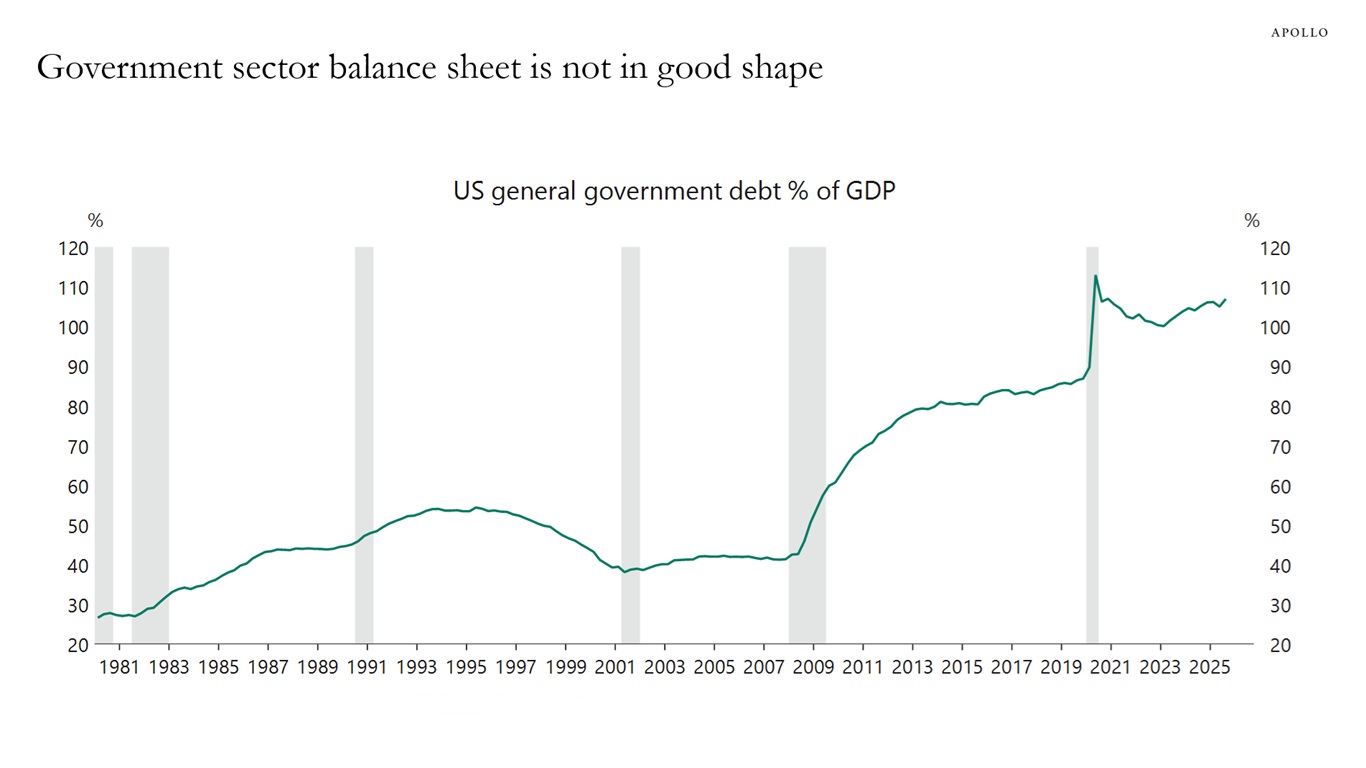

Unfortunately, the government balance sheet is not in good shape. Government debt to GDP has increased steadily from 40% of GDP in 2007 to more than 100% today, see the third chart.