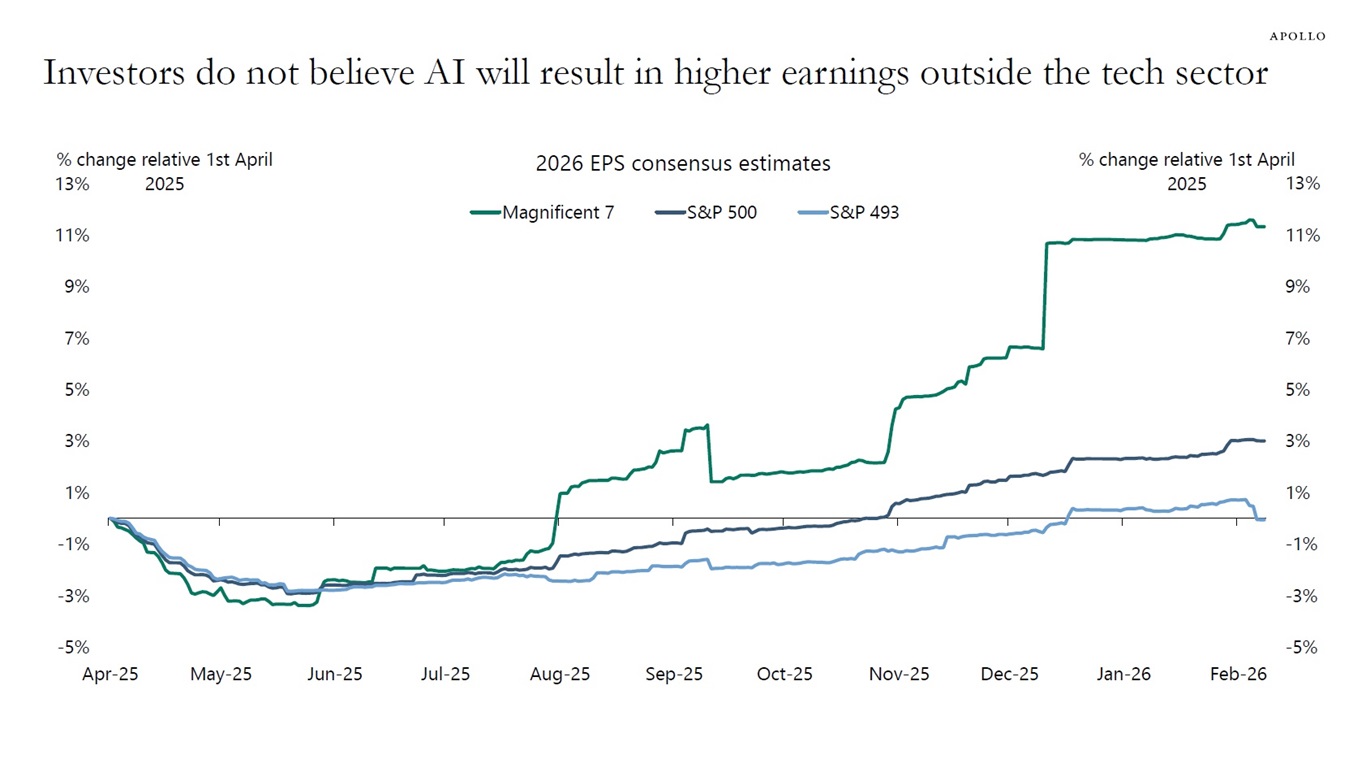

The chart below shows consensus expectations for earnings for the Magnificent Seven and the S&P 493 since Liberation Day.

Earnings expectations for the Magnificent Seven have increased significantly. But expectations for earnings for the S&P 493 are basically unchanged.

The bottom line is that the consensus does not expect AI to improve profitability for corporate America outside the tech sector.