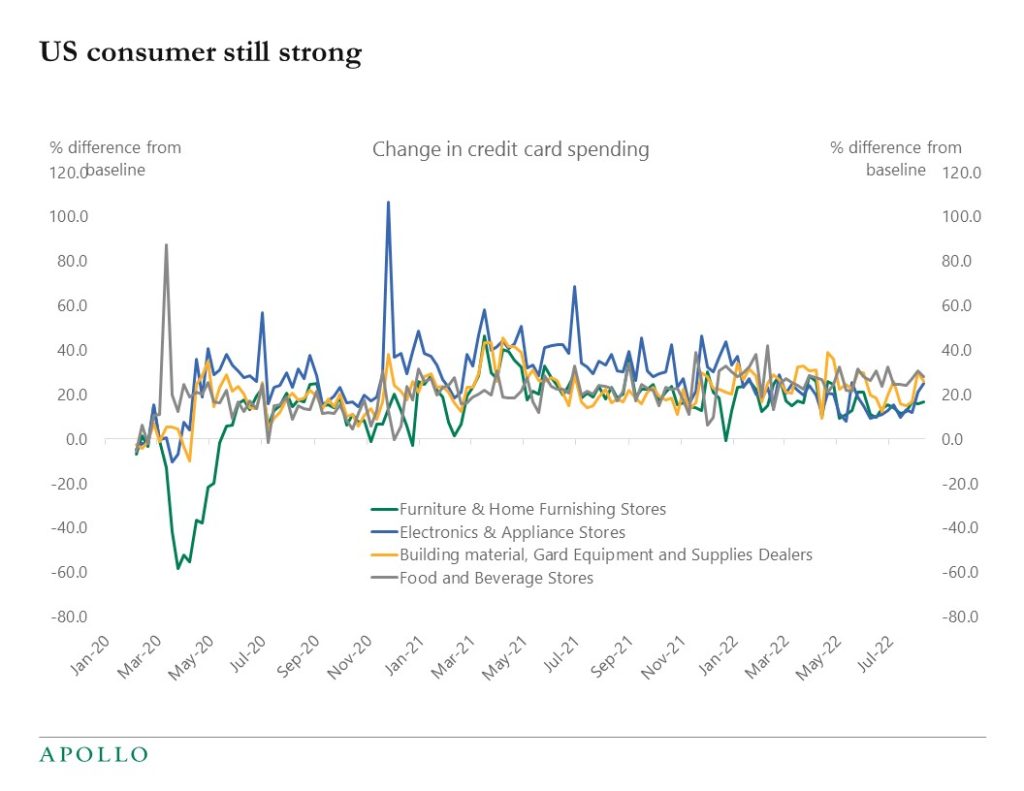

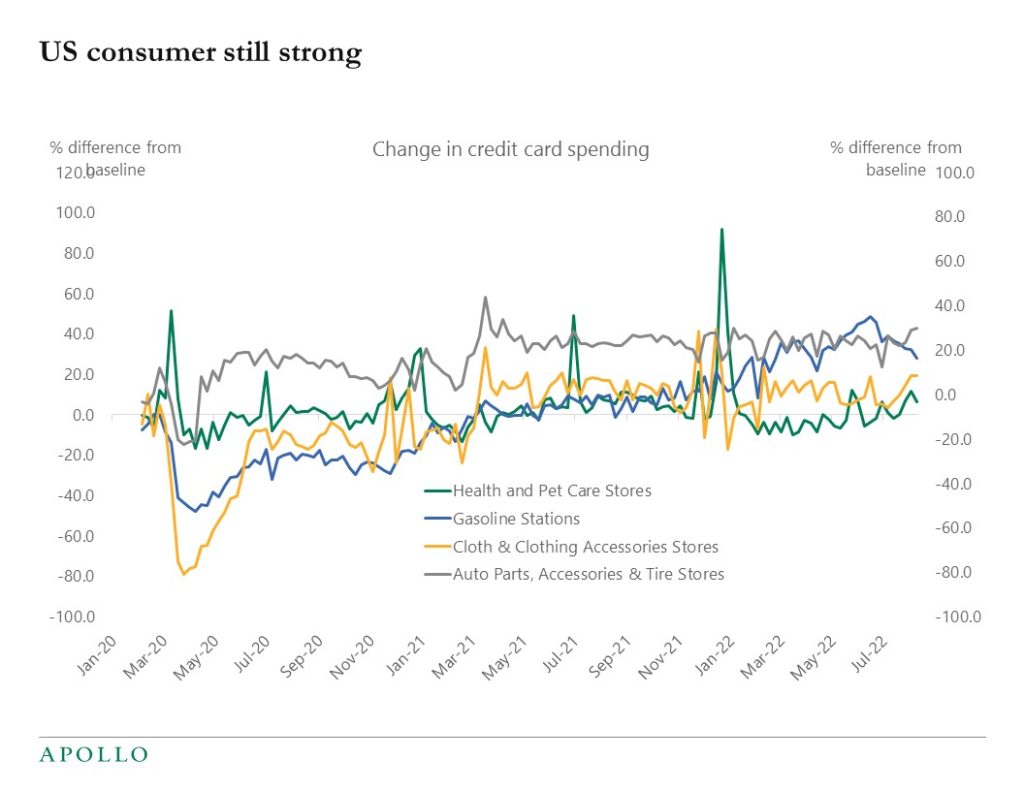

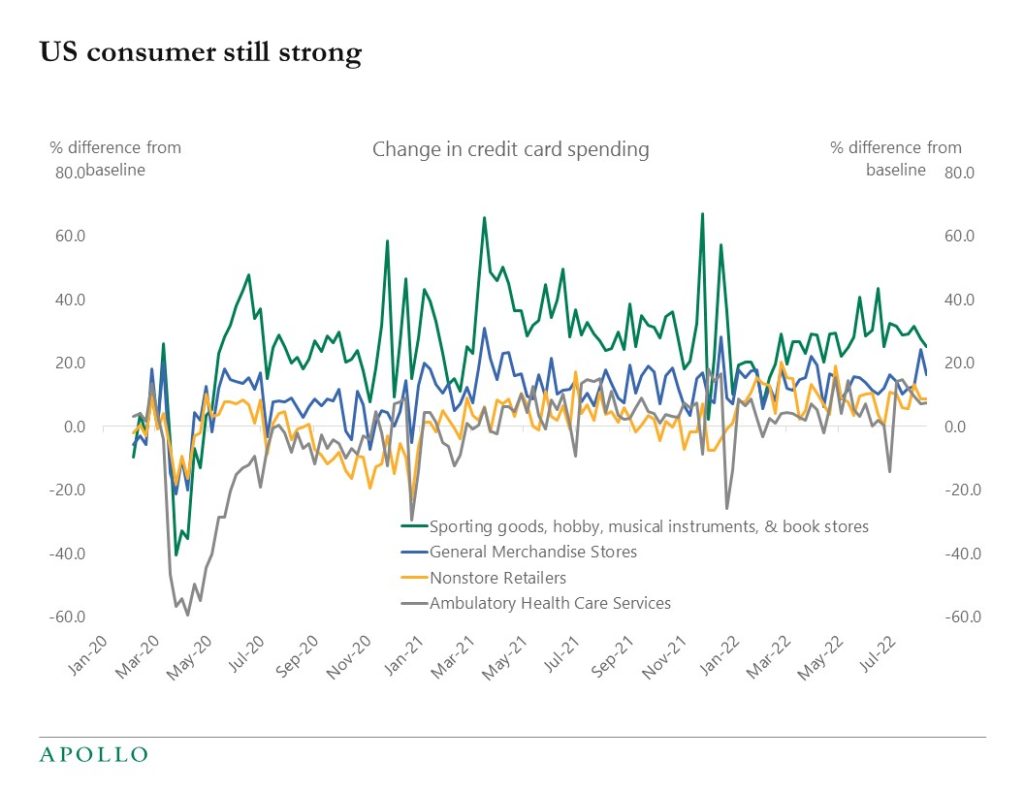

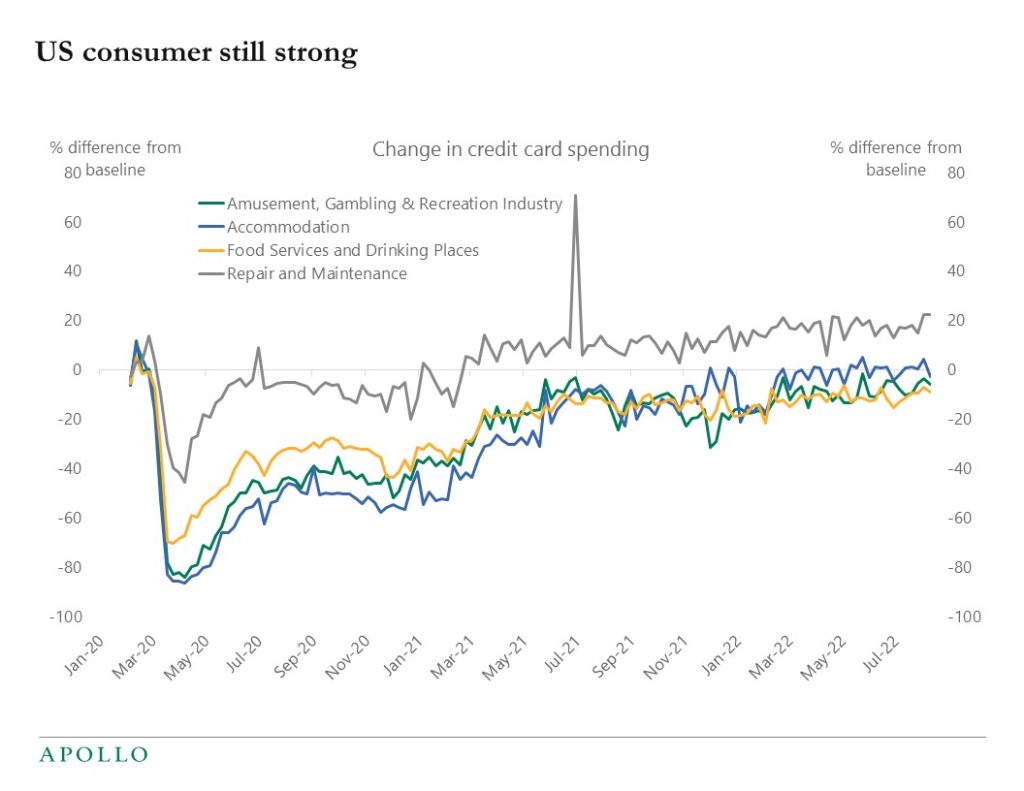

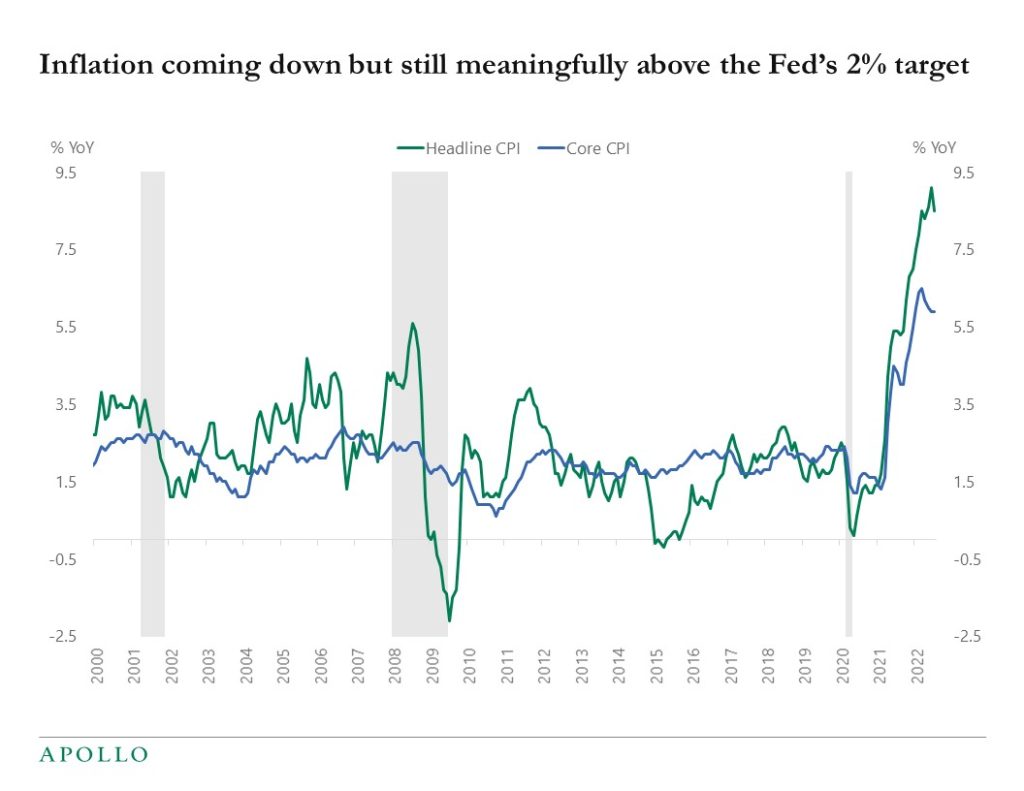

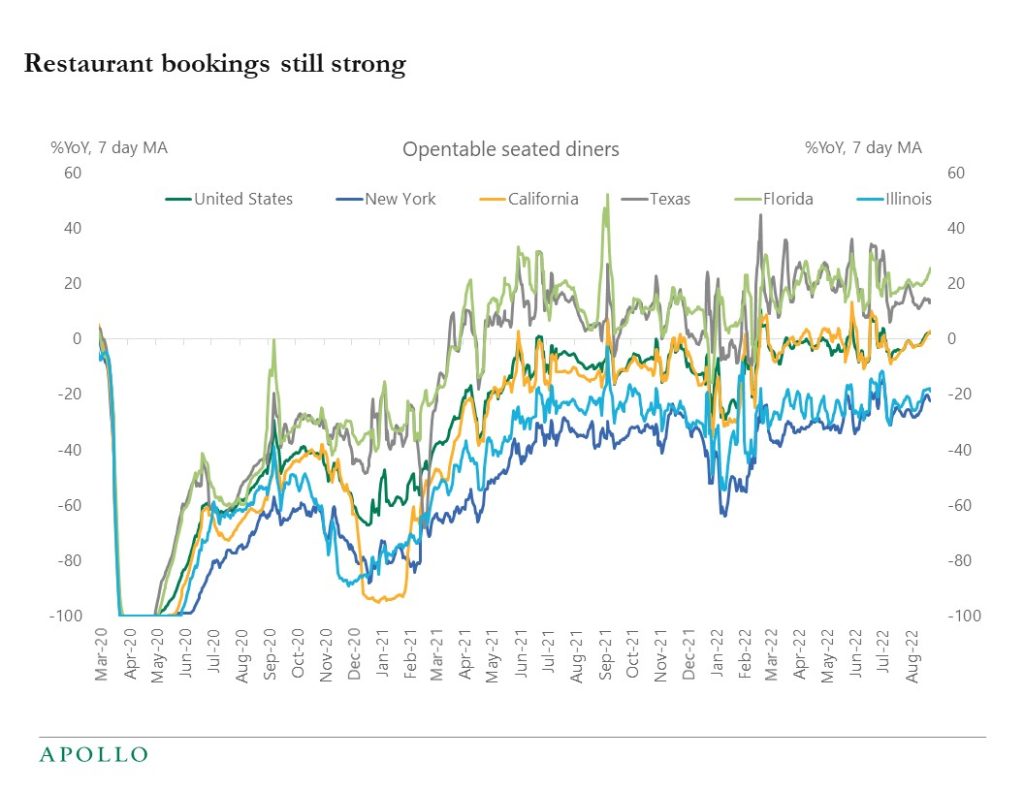

The FOMC minutes from last week gave us more information about the Federal Reserve’s thinking behind raising interest rates 75 basis points at their most recent meeting. From this release, we learned that the Fed still thinks inflation is too high and that they are focused on cooling the economy down. Markets zeroed in on a few sentences in the minutes that discussed the possibility of slowing the pace of rate hikes, interpreting that as a dovish sentiment. We will be watching what Fed Chairman Jay Powell says about that this Friday at the annual global central banking conference in Jackson Hole. We believe that Powell and other FOMC members will attempt to draw a more hawkish line this week, considering that inflation remains so far above their 2% target. Despite the central bank’s efforts, the economy is still showing signs of strength. For example, US consumer credit card spending remains strong across all areas—from clothing, sporting goods, and amusement parks to hotels, restaurants, and more. The bottom line is that the US consumer is simply not slowing down, which means that the Fed still has more work to do to cool the economy off to help lower inflation. It’s against this backdrop that we expect more rate hikes ahead, and therefore continued uncertainty in equity and credit markets.

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.