This new academic paper finds that about 7% of US adults, or around 19 million people, still suffer from long covid. And of those with long covid, 25%, or about 5 million people, report that their day-to-day activities are impacted ‘a lot’.

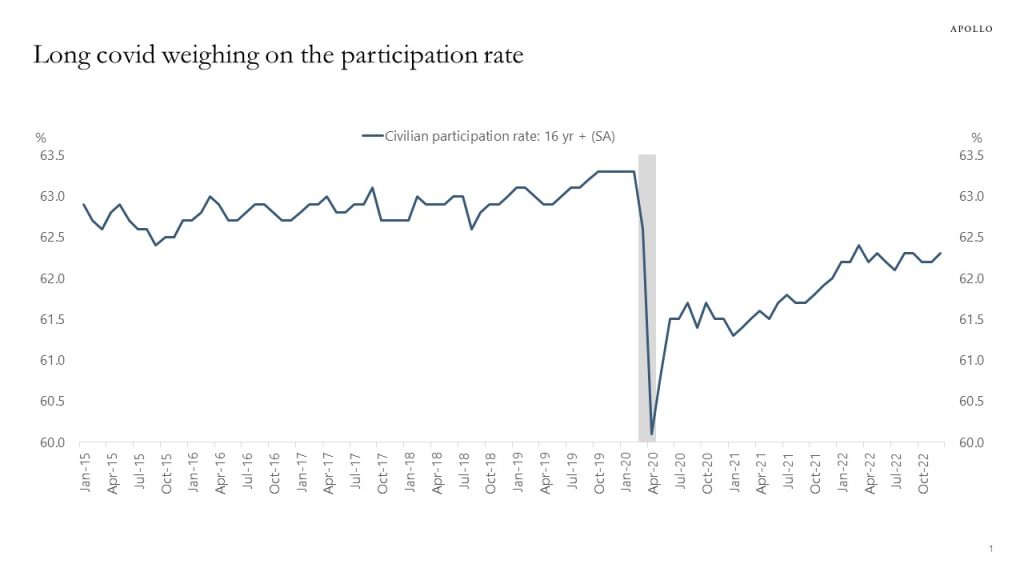

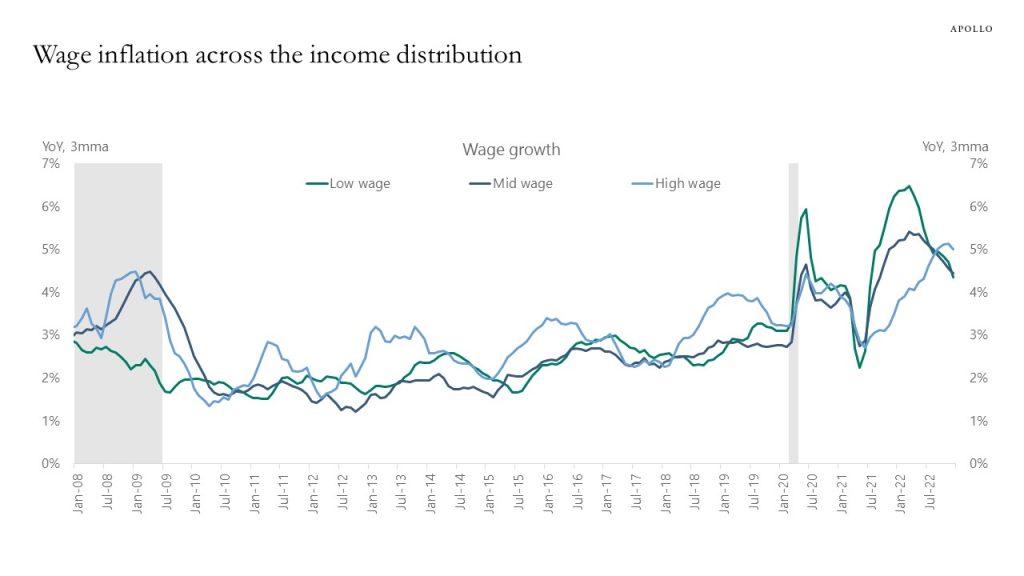

The bottom line is that long covid is why the labor force participation rate has not recovered to pre-pandemic levels, even in a situation with solid wage growth, see chart below. In other words, people are staying outside the labor market for health reasons and are unlikely to come back in the near term.

These “missing” workers are why companies continue to report labor shortages and why wage inflation remains so high. This continues to be a challenge for the Fed as the FOMC tries to get inflation quickly back to the Fed’s 2% inflation target. Immigration is starting to increase, but ultimately long covid is a key reason why the Fed will have to keep the Fed funds rate elevated for an extended period.