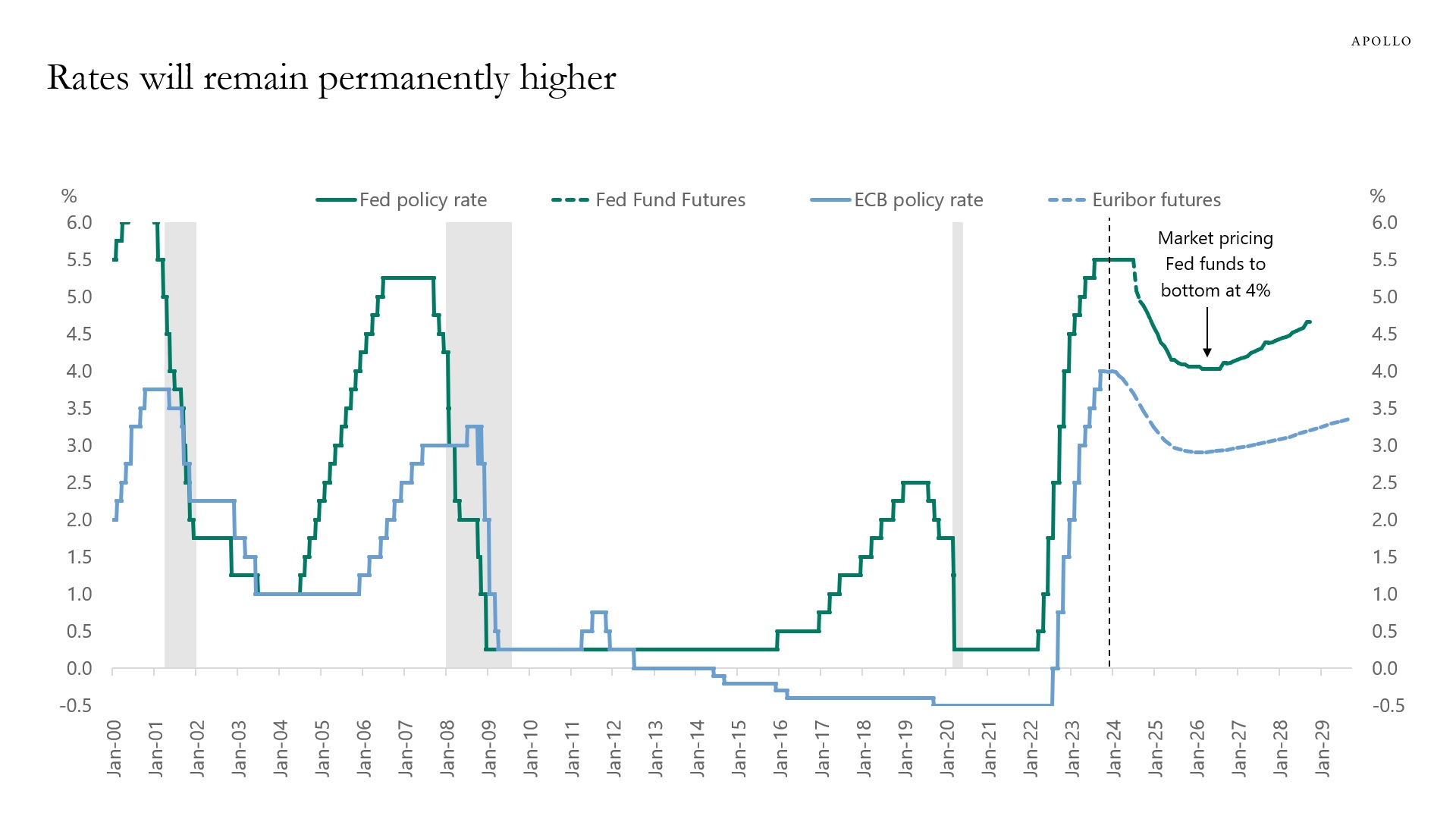

Markets are pricing that the Fed funds rate will bottom at 4% in 2025 and then start rising again, see chart below.

The same profile can be seen for the ECB, where rates will bottom at 3% and then start rising again.

The conclusion is that long-term investors should plan on rates being permanently higher than they were from 2008 to 2020.

In other words, rates are not going back to zero.