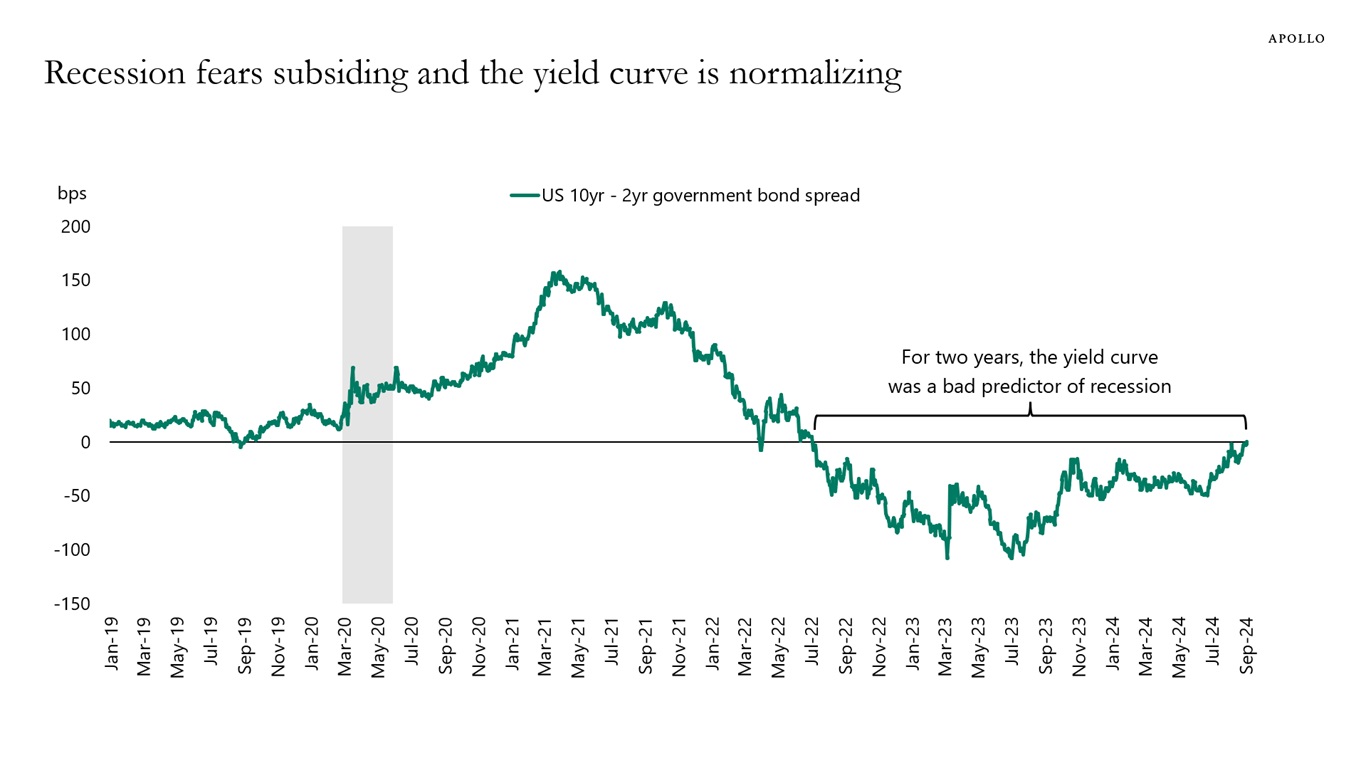

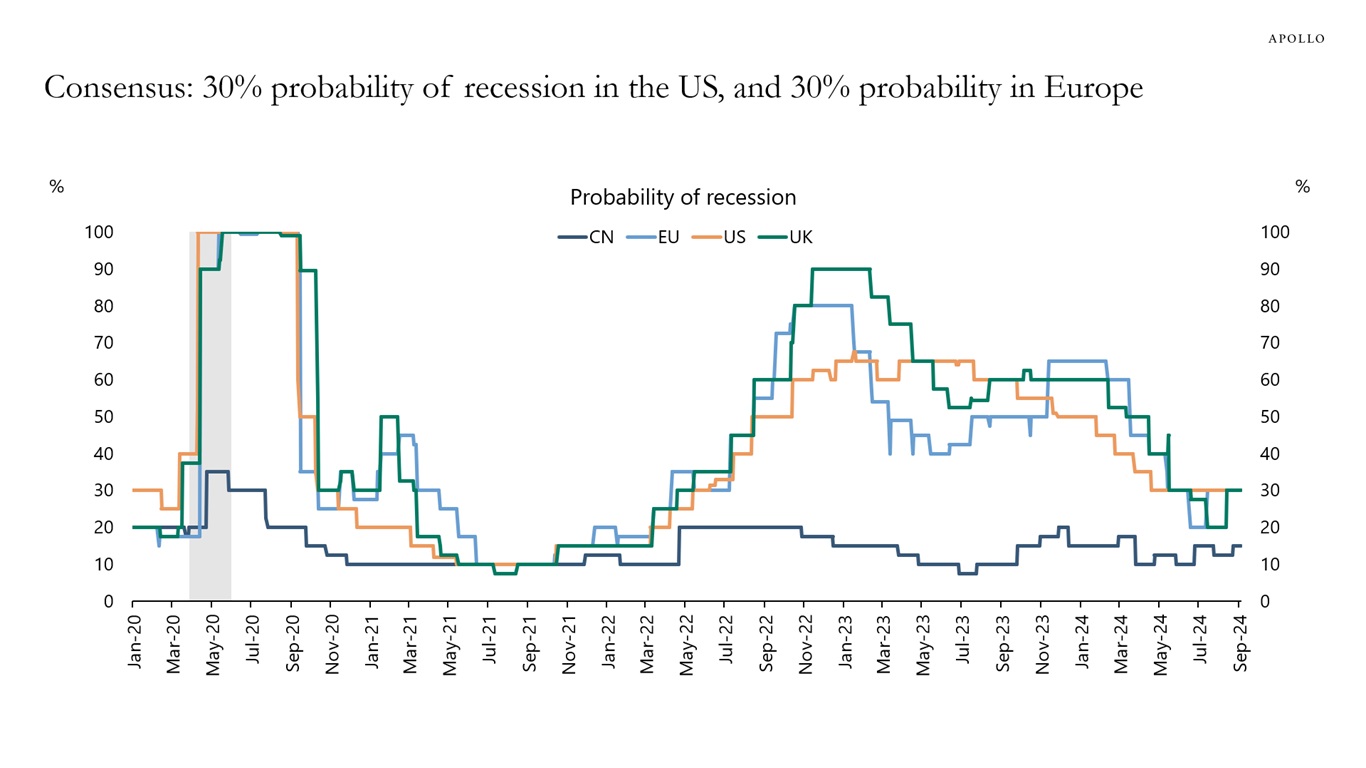

The yield curve is no longer inverted, and the recession probability is declining, see charts below.

To understand if a recession is coming, it is a better idea to look at the incoming data than to look at the yield curve because long rates are not only a reflection of the business cycle but also foreign demand, fiscal policy, and the term premium. And the incoming data continues to look just fine, see also here.