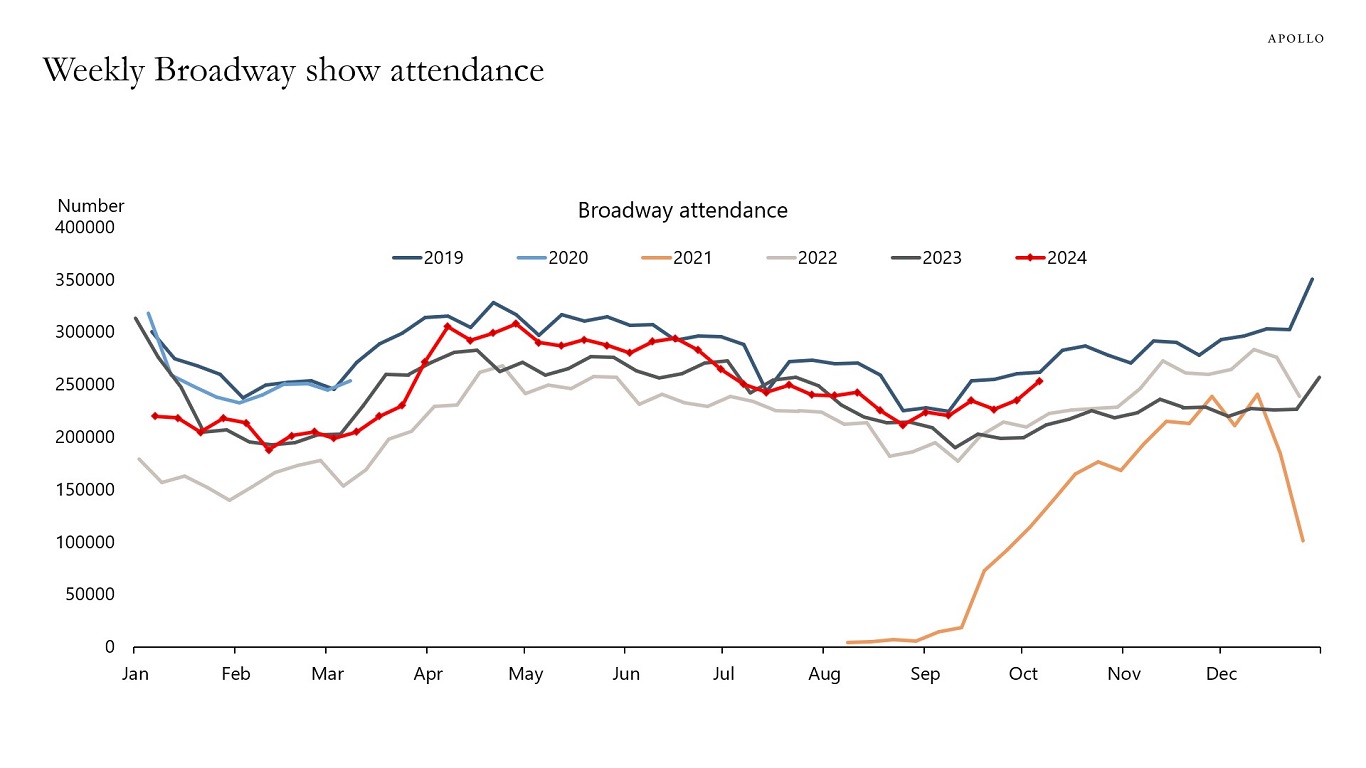

Going to a Broadway show can cost up to $200, and the latest weekly data shows that consumers are still happy to pay this discretionary expense, see the first chart below.

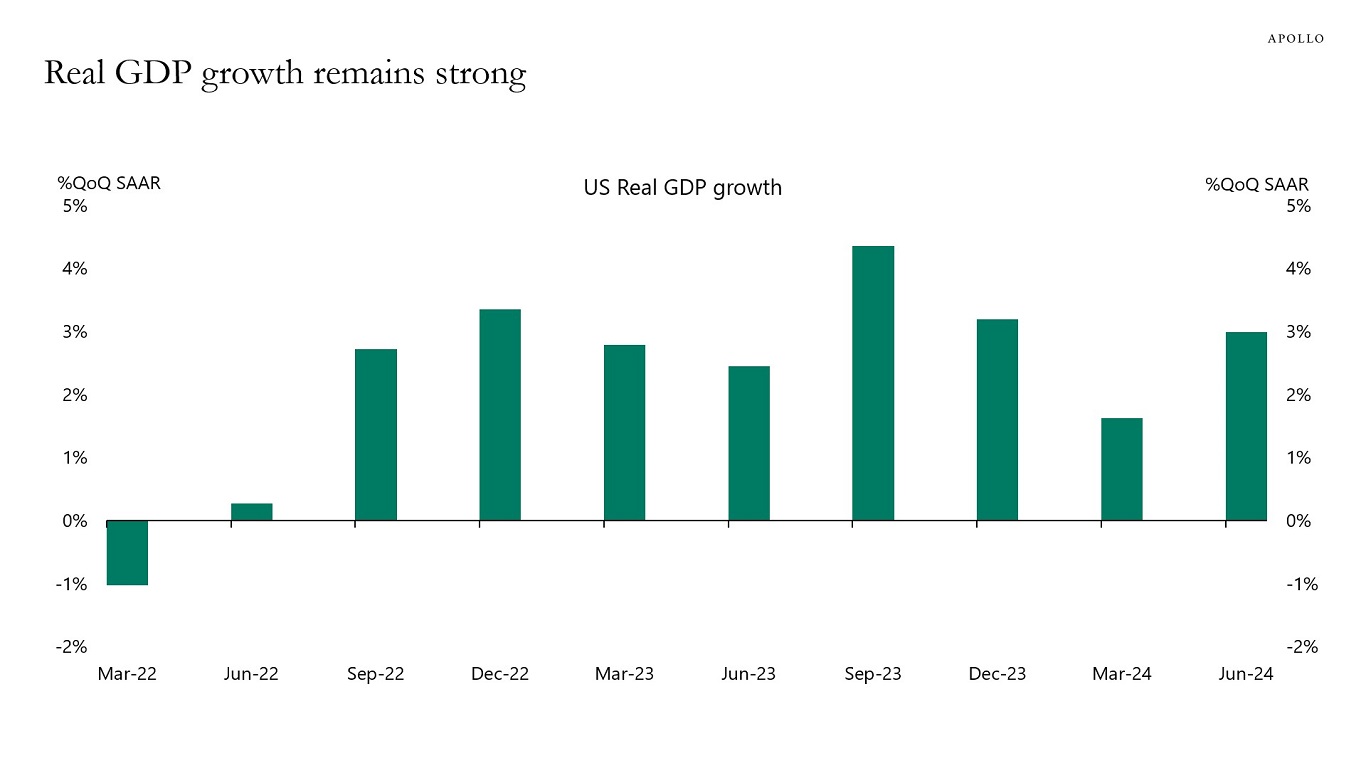

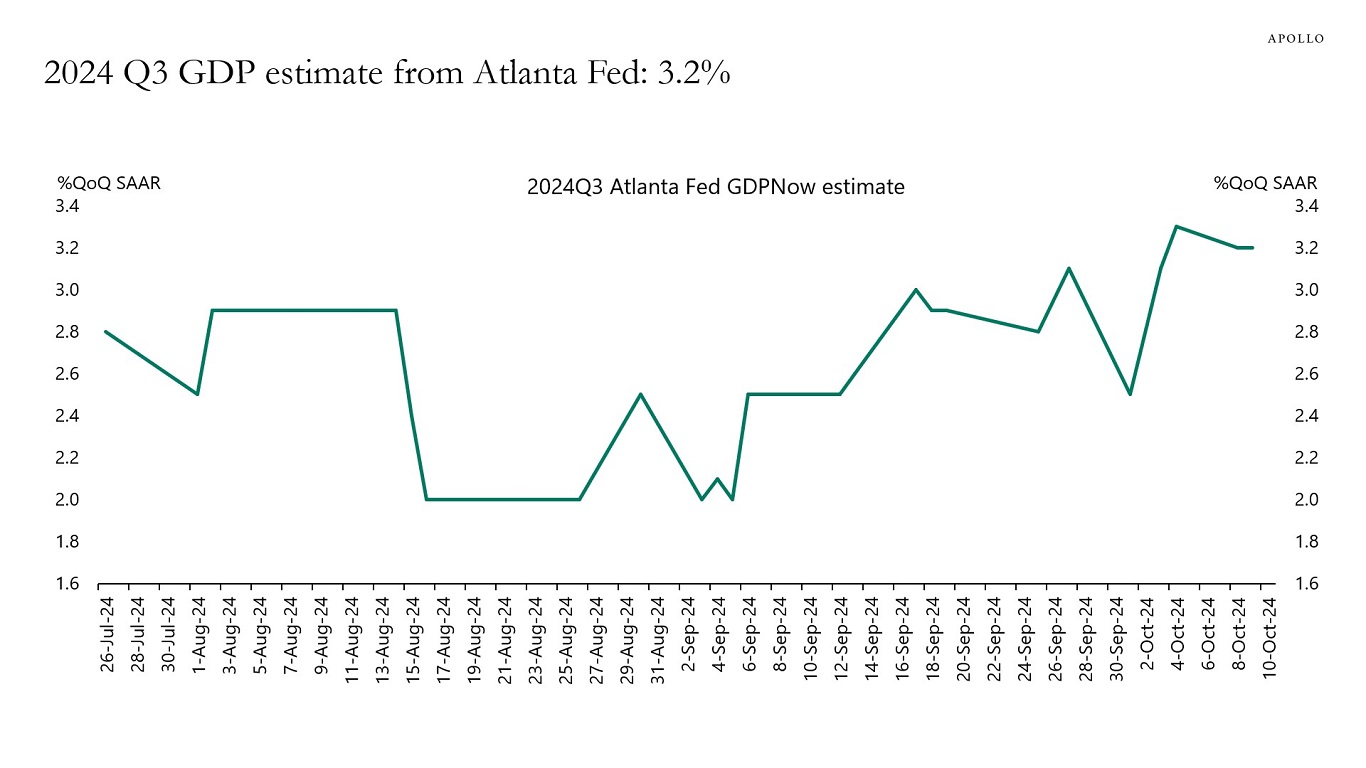

More broadly, GDP growth in the second quarter was 3.0%, and the Atlanta Fed GDP estimate for the third quarter is 3.2%, see the second and third chart.

Why is the economy so strong? Because of lower interest rate sensitivity for households and firms because of locked-in low interest rates, strong AI spending, and strong fiscal spending driven by the CHIPS Act, the IRA, and the Infrastructure Act. Combined with high stock prices and tight credit spreads, these forces are offsetting the long and variable lags of monetary policy.

See our chart book with daily and weekly indicators.