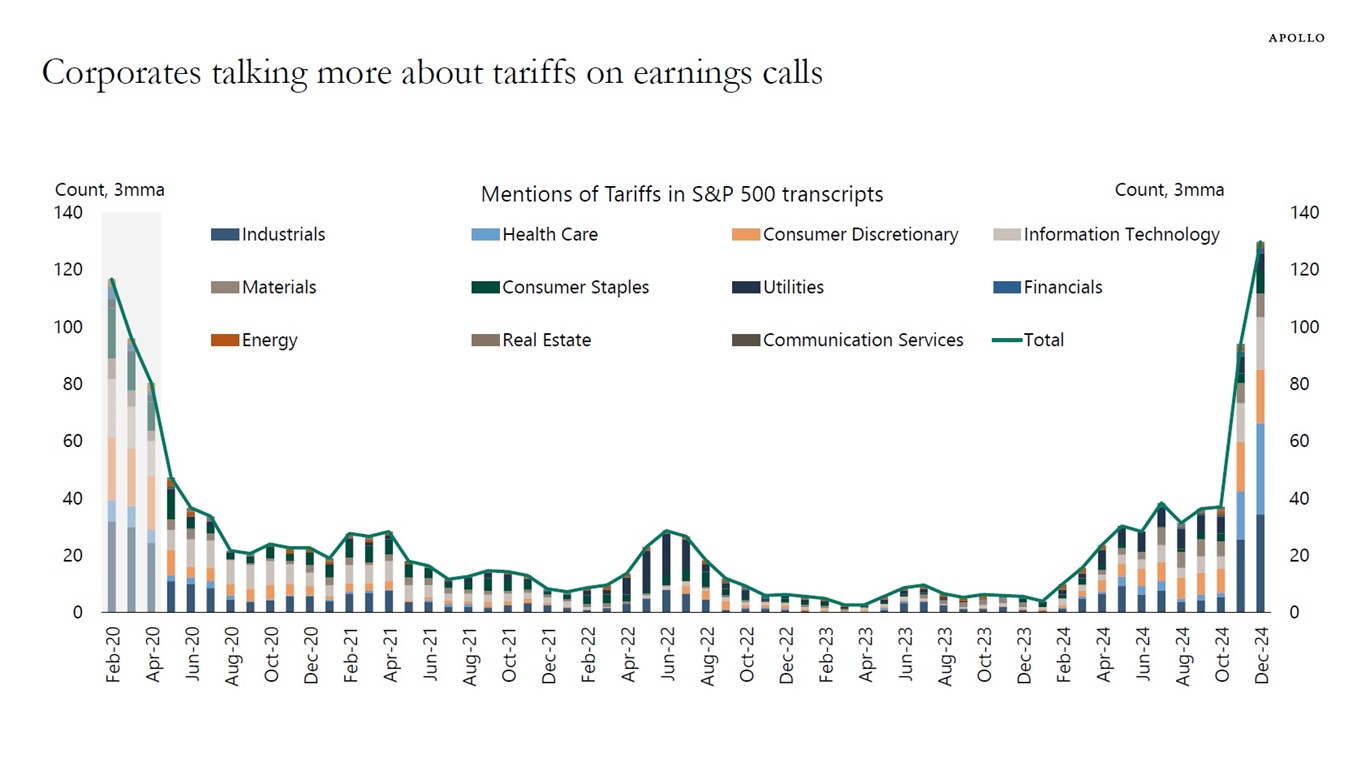

Looking at transcripts of earnings calls shows that there is more talk about tariffs among firms in the industrial, health care, consumer discretionary, and IT sectors, see chart below.

Looking at transcripts of earnings calls shows that there is more talk about tariffs among firms in the industrial, health care, consumer discretionary, and IT sectors, see chart below.

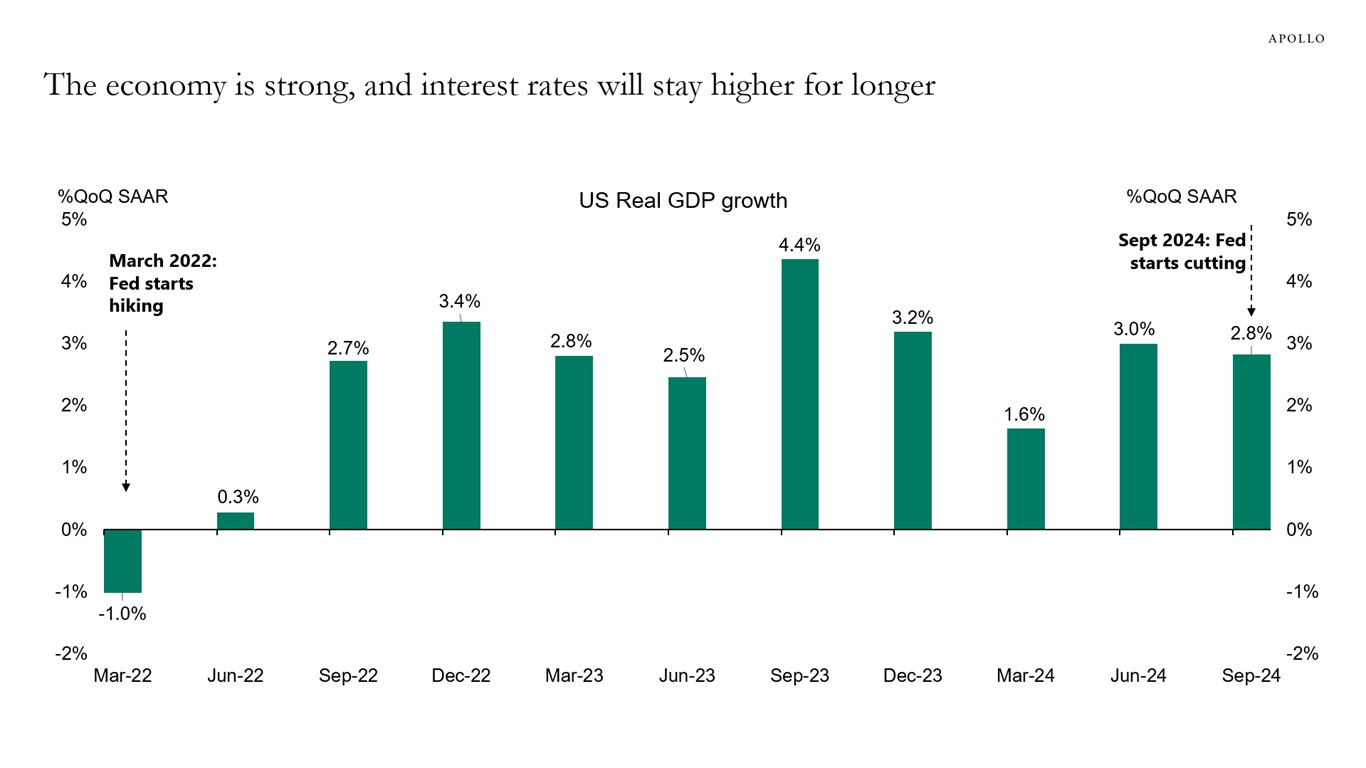

The Fed has now cut interest rates 100 bps this year. In a strong economy where growth over the past two quarters has been 3.0% and 2.8%, see chart below, the Atlanta Fed expects GDP growth in the fourth quarter to be 3.2%, well above the CBO’s 2% estimate of long-run US growth.

The strong economy, combined with the potential for lower taxes, higher tariffs, and restrictions on immigration, has increased the risk that the Fed will have to hike rates in 2025. We see a 40% probability that the Fed will raise interest rates in 2025.

For investors, it is starting to look similar to 2022—too high inflation, rising interest rates, and falling stock prices.

The bottom line is that there are significant downside risks to the 60/40 portfolio as we enter 2025.

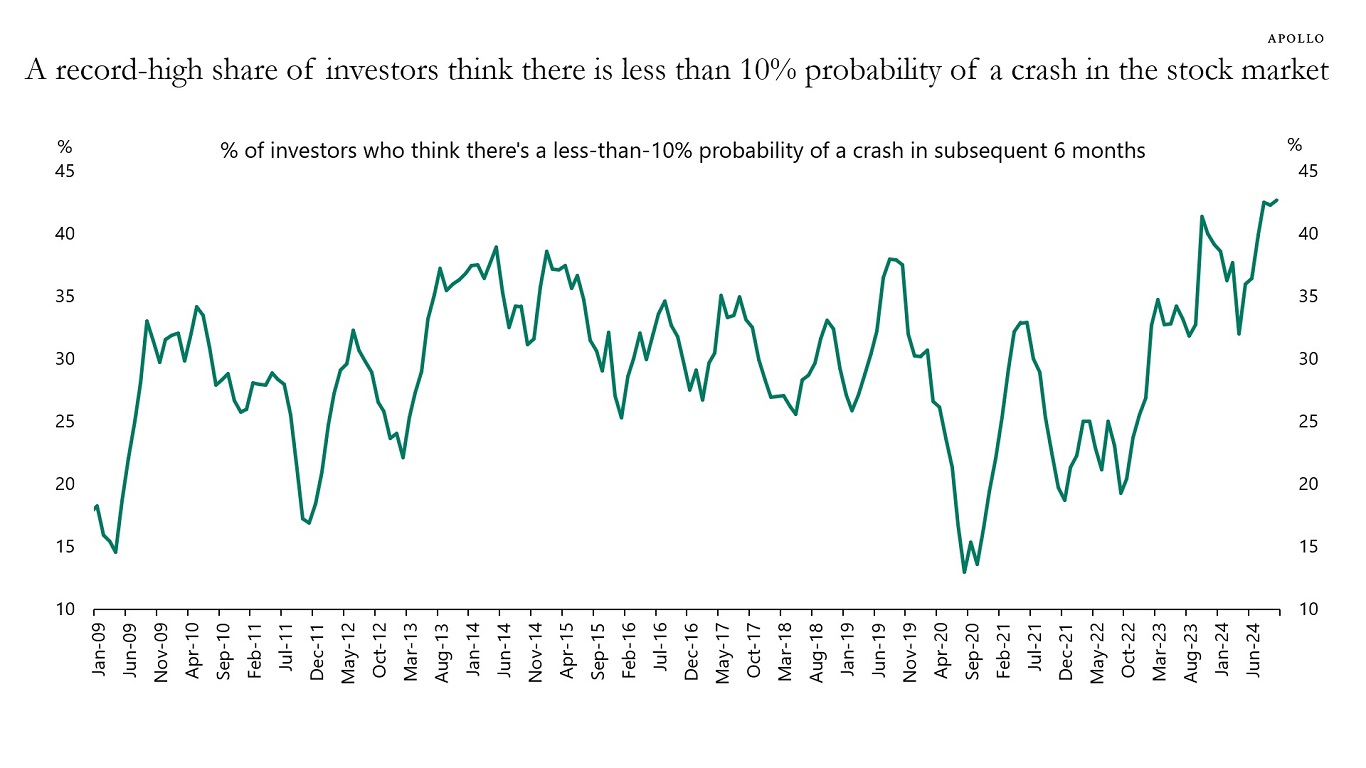

Investors are extremely bullish on the stock market, and a record-high share think that there is less than 10% probability of a crash over the coming six months, see chart below.

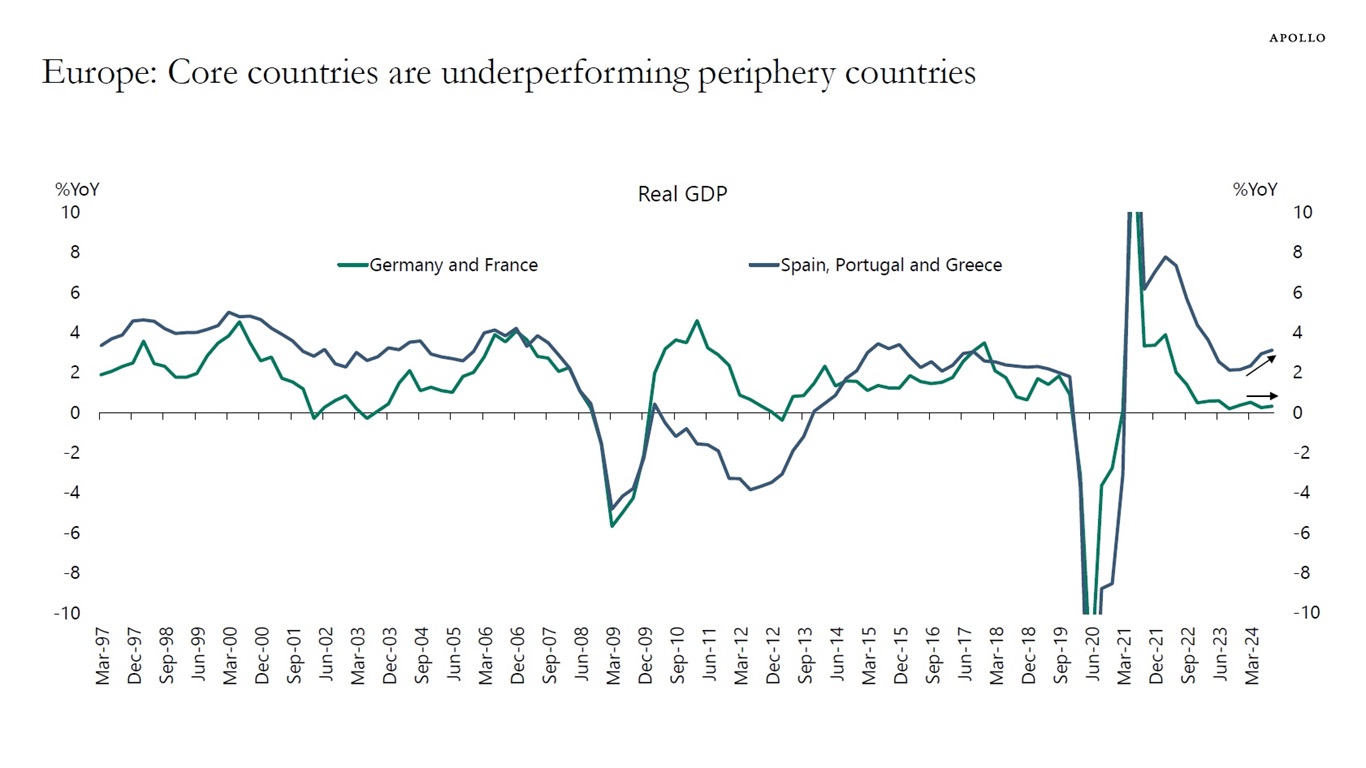

The macro outlook is simple at the moment. The US economy is strong and Europe is weak.

But there are some crucial nuances in the outlook for Europe.

Core countries such as Germany and France are weak, but the periphery countries—Spain, Portugal, and Greece—are strong, see chart below.

This unusual intra-European divergence has important implications for rates, credit, and asset allocation more broadly.

Listen to Apollo Chief Economist Torsten Slok discuss his 2025 Economic Outlook, with forecasts for GDP, inflation, and monetary policy. Plus: What are the implications for capital markets?

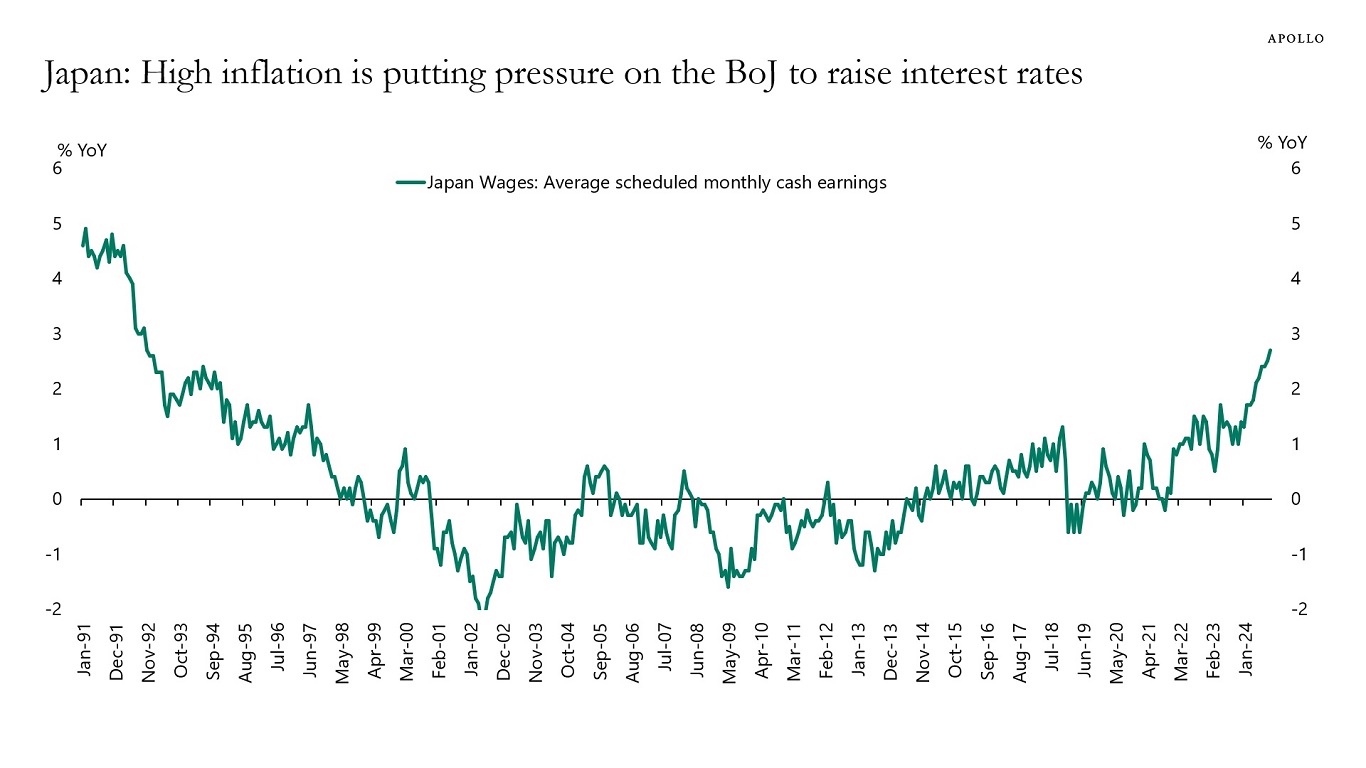

Japan was in deflation for decades. But that has changed over the past year with wage inflation accelerating to almost 3%, see chart below.

The pressure is intensifying on the BoJ to raise interest rates. This has important implications for the global carry trade, in particular in a situation where the BoJ is hiking and the Fed is cutting.

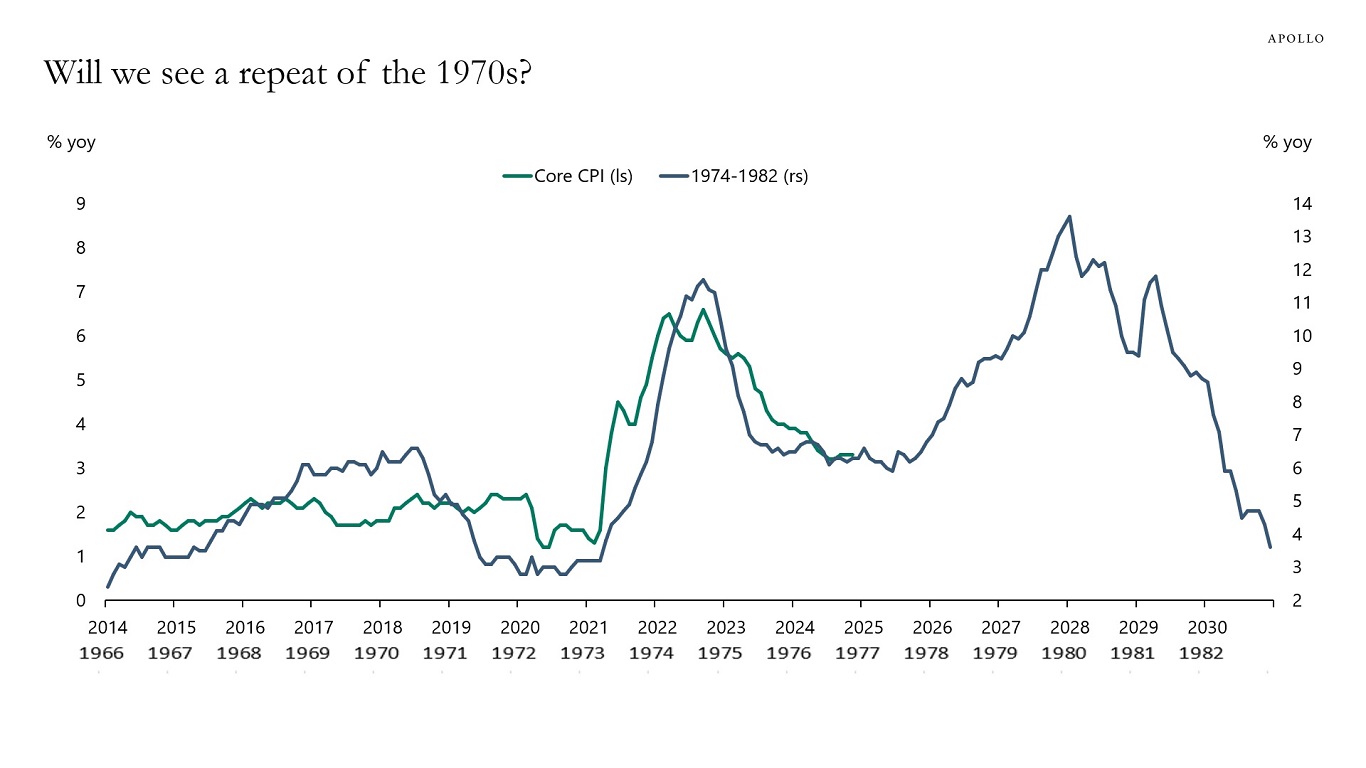

Will we see a repeat of the 1970s with the Fed easing policy too quickly, triggering a rise in inflation in 2025?

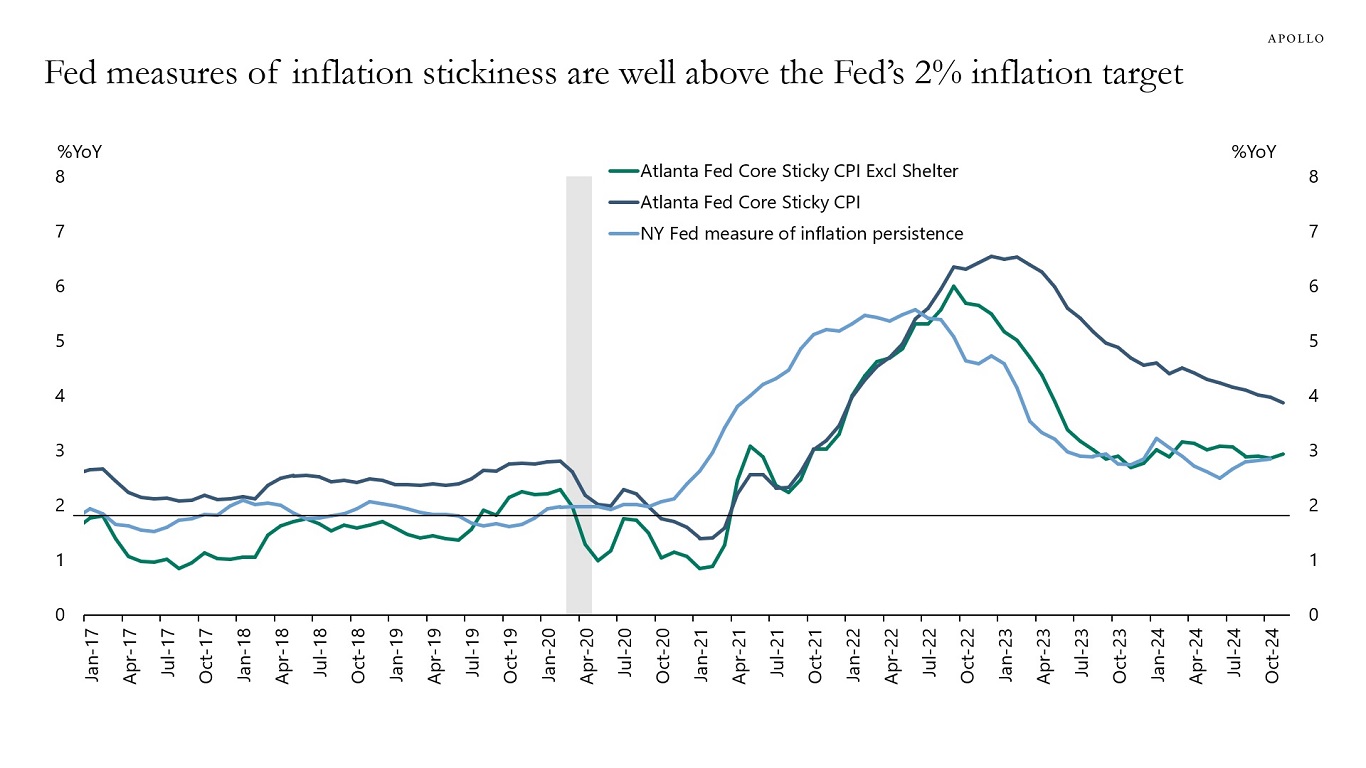

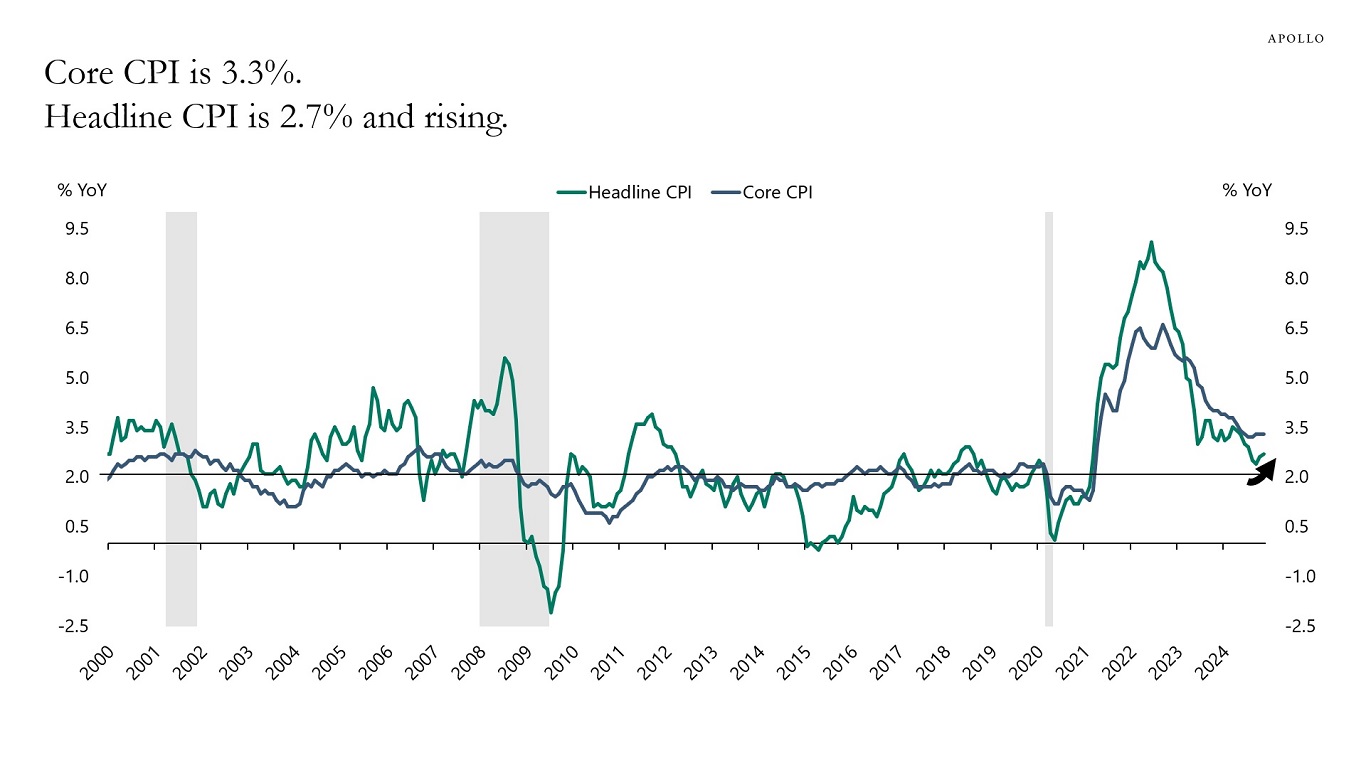

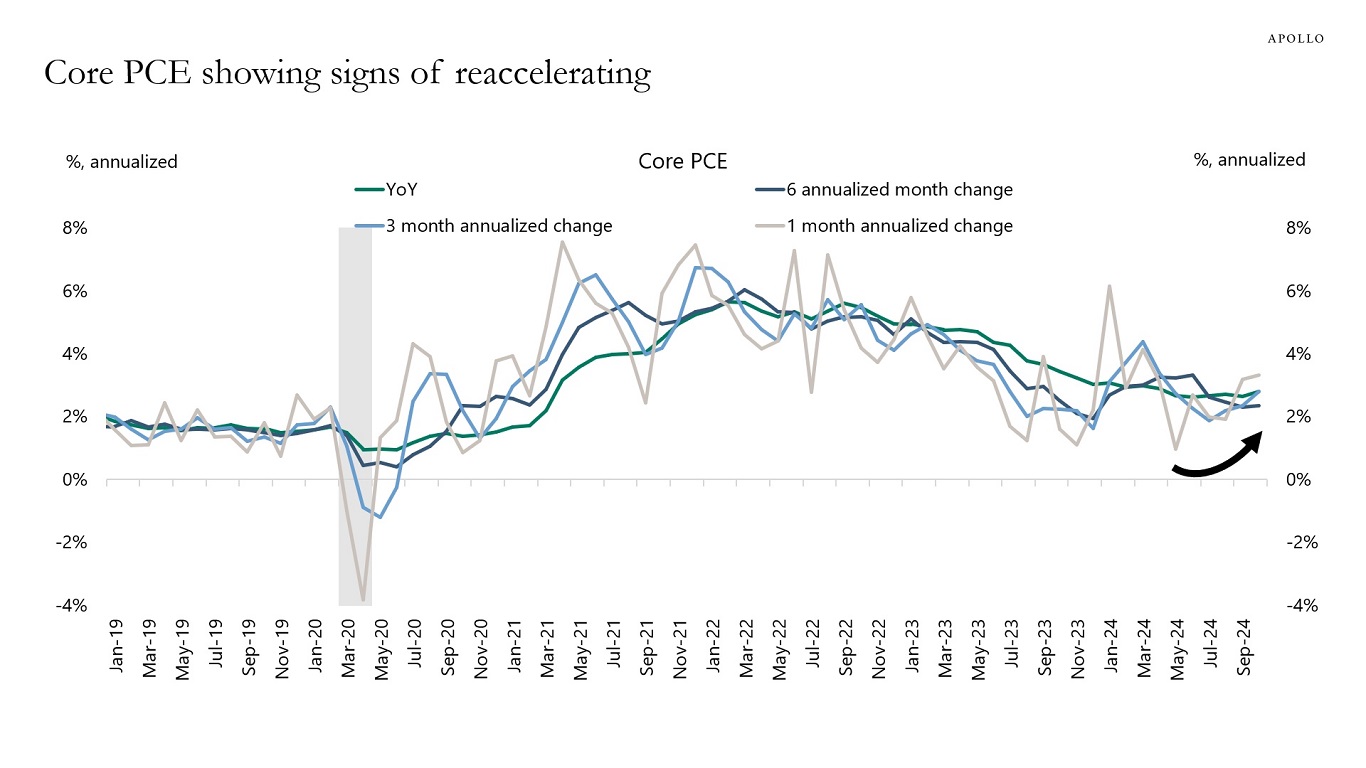

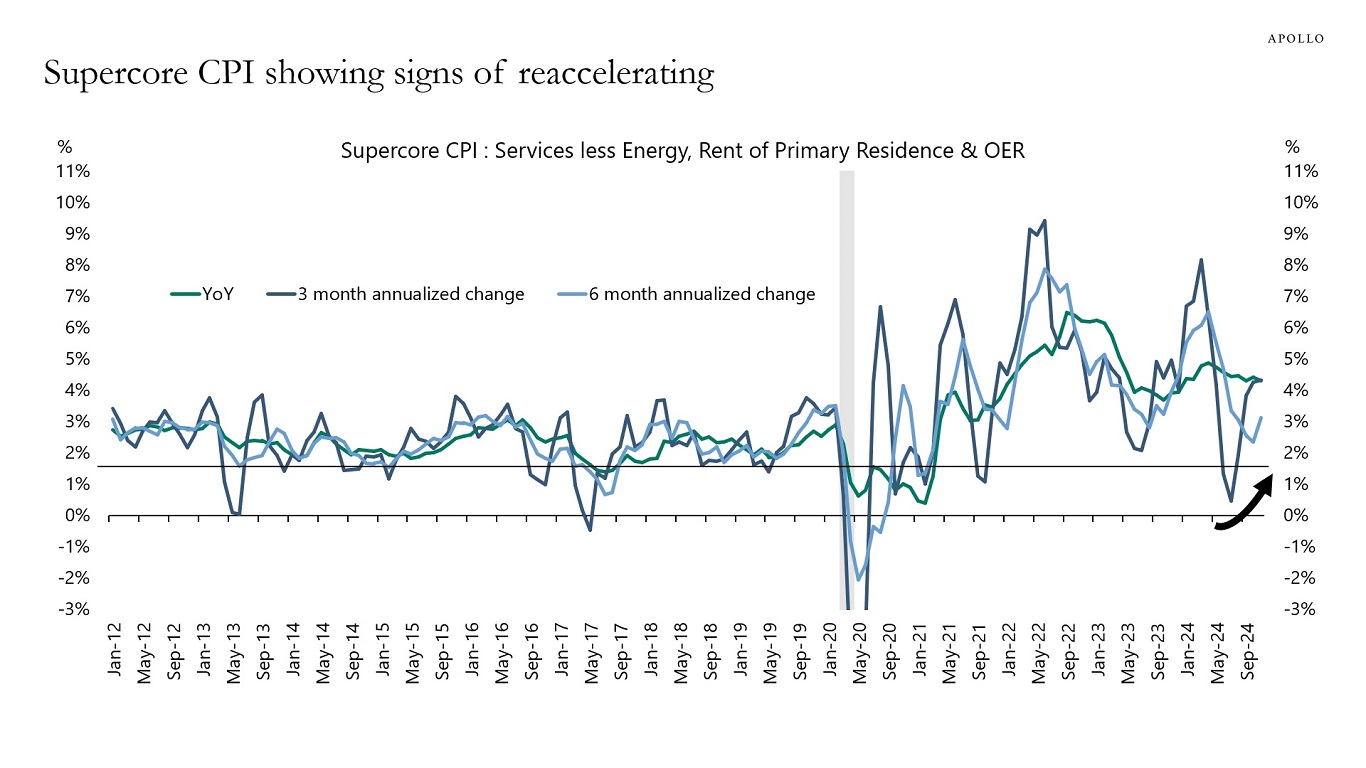

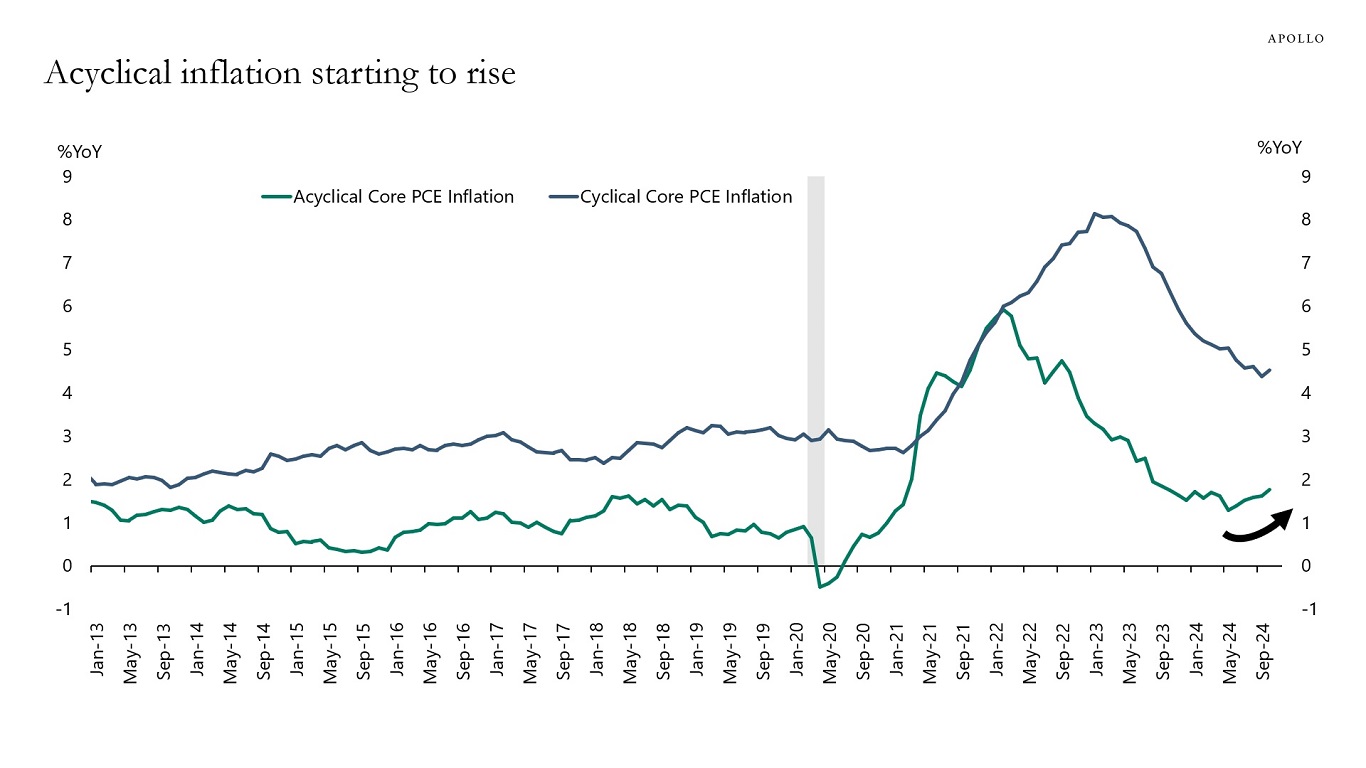

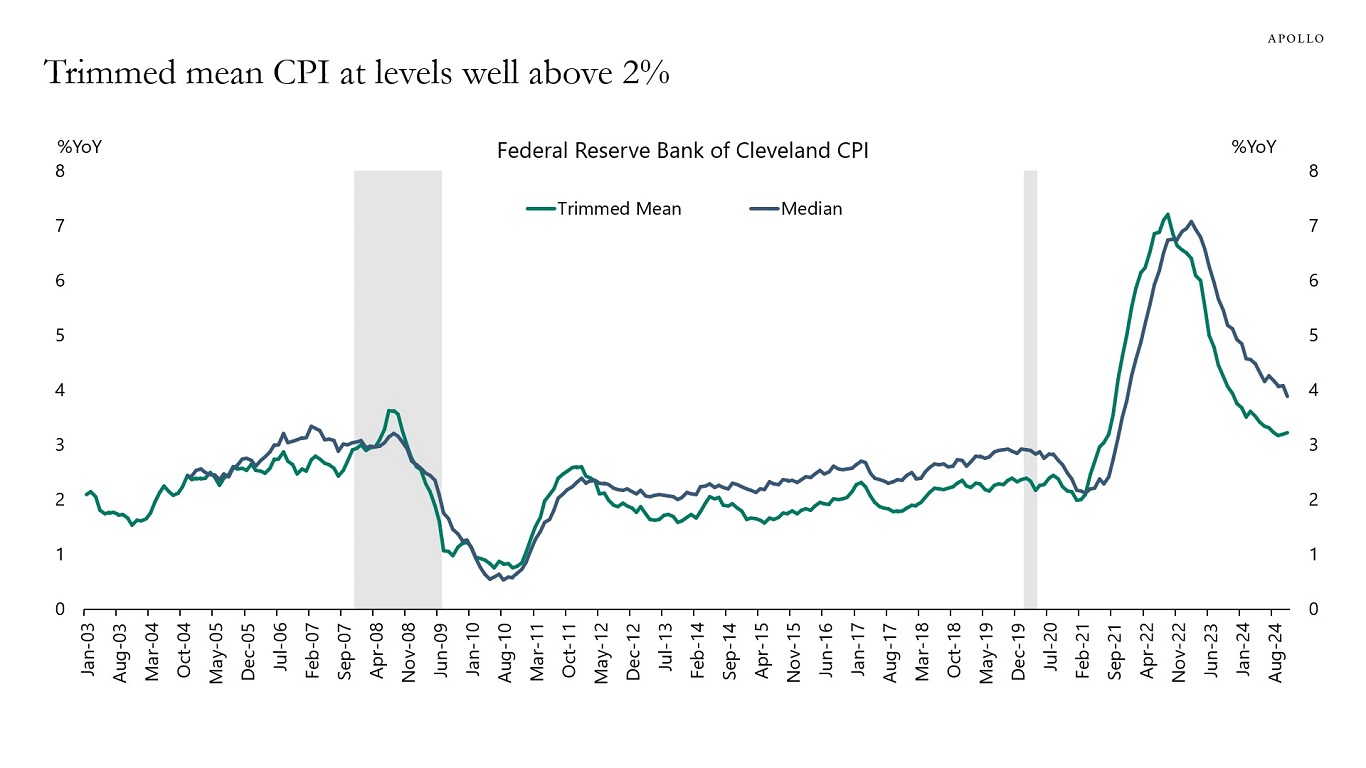

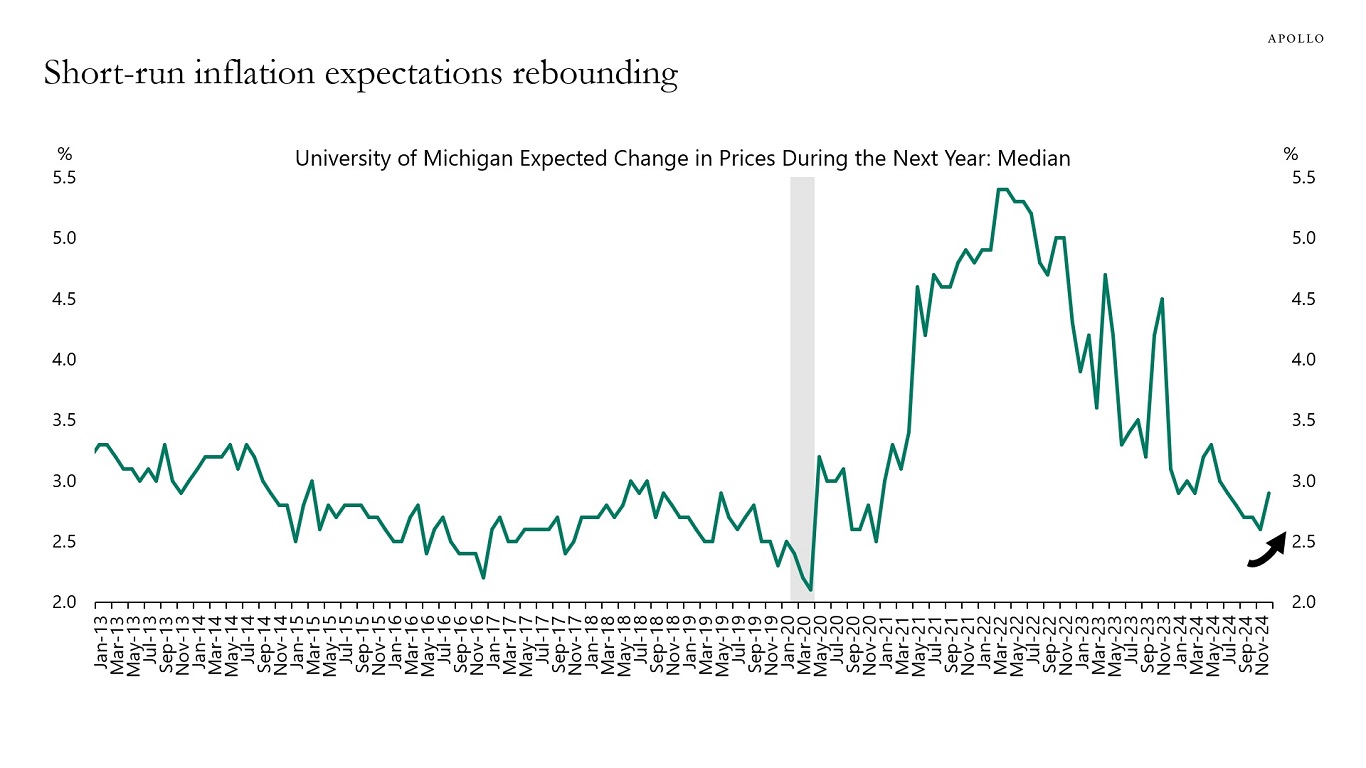

Recent inflation readings show signs that the decline in inflation has stalled, and there is a risk of reacceleration, see charts below. Fed and market-implied measures of inflation are all above the Fed’s 2% target and not showing signs of moving down toward the Fed’s 2% inflation target. Short-run and long-run inflation expectations are also moving higher.

The recent uptrend, combined with strong economic momentum, is pointing towards a rebound in inflation in 2025 and not a softening to justify Fed cuts. The probability is rising that the Fed may have to raise interest rates in 2025.

For investors, the risk is a repeat of 2022, where the 60/40 portfolio underperformed significantly.

Our chartbook with recent measures of inflation is available here.

In the year ahead for real assets, we reiterate our view of the value of a private infrastructure allocation in a diversified investment portfolio. Private infrastructure has shown resilience in times of market stress and provided downside protection with low correlation to other major asset classes.1 There are powerful macroeconomic tailwinds bolstering infrastructure today, including federal spending initiatives and the global need to update aging infrastructure.

We see three key themes in real assets:

1. The global need to update aging infrastructure shows an $88 trillion funding gap by 2040.2

2. Unprecedented regulatory support has catalyzed spending on infrastructure, including the bipartisan infrastructure law that authorized $1.2 trillion for transportation and infrastructure spending with $550 billion of that figure going toward “new” investments and programs.

3. The opportunity set includes digital infrastructure, where increasing computing power from generative AI and related technologies is driving heightened demand for data centers and electricity.

Our real assets chart book is available here.

We also published our 2025 Economic Outlook this week.

For private equity, we see three key themes in the year ahead:

1. Lower interest rates could spark a new wave of deals as, on one hand, sponsors seek to deploy capital raised in the past three years and, on the other, managers may be willing to part with existing investments as cheaper borrowing costs may bolster valuations.

2. We believe the secondary market can offer excess return per unit of risk when compared to other private market strategies due to a variety of factors, including a rapidly evolving secondary investment landscape.

3. There is plentiful demand for hybrid solutions, including M&A financing and capital for growth, re-equitization of over-levered balance sheets, owner and sponsor liquidity solutions, and financing to support public company growth initiatives.

Our private equity chart book is available here.

We also published our 2025 Economic Outlook this week.

The US economy remains strong with no signs of a major slowdown going into 2025. We see interest rates staying higher for longer on a relative basis (regardless of the Fed’s easing campaign) as inflation remains above target, employment strong, and spending robust.

We have published our consolidated views in my newest white paper, 2025 Economic Outlook: Firing on All Cylinders. You can download it here.

I will also be discussing the contents of the paper and my views in detail in an Apollo Academy class today at 11:00 ET (eligible for a CE credit). Register here. The class will be available on demand afterward.