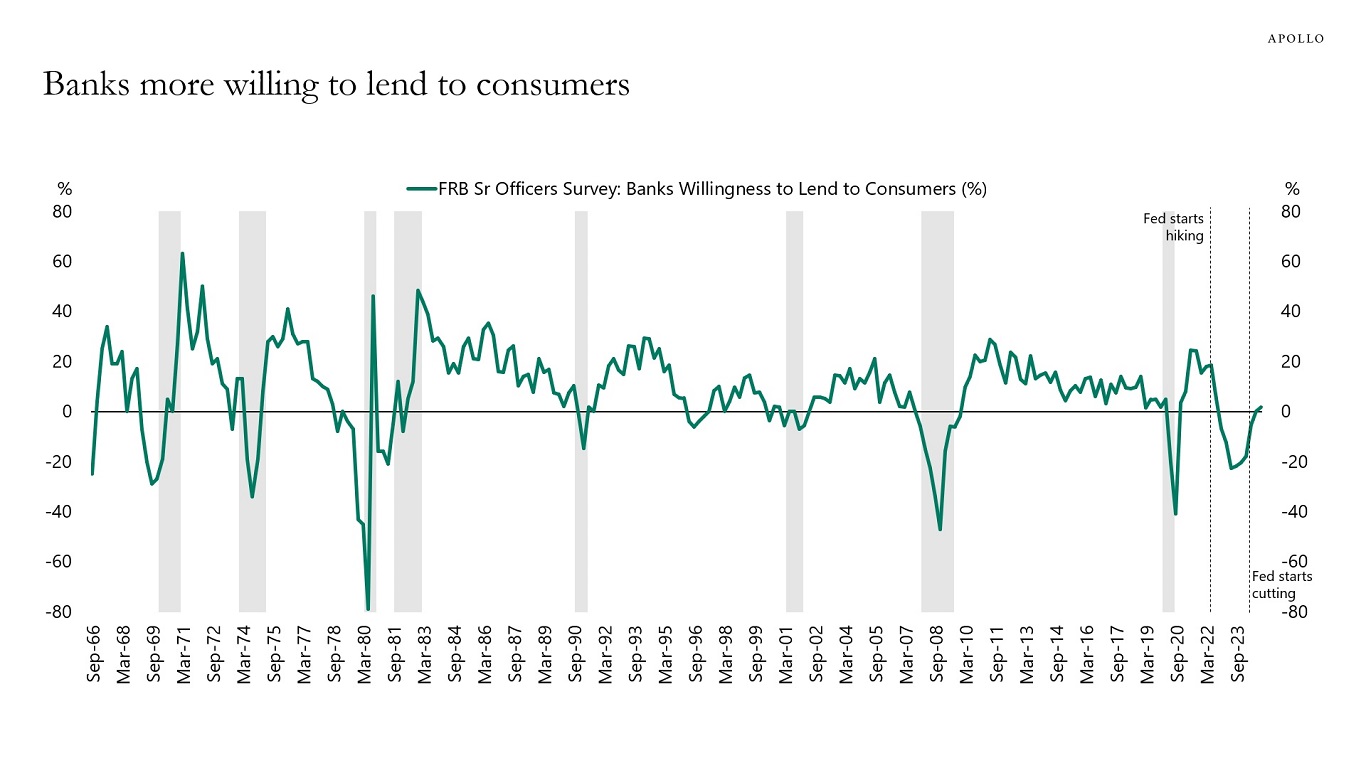

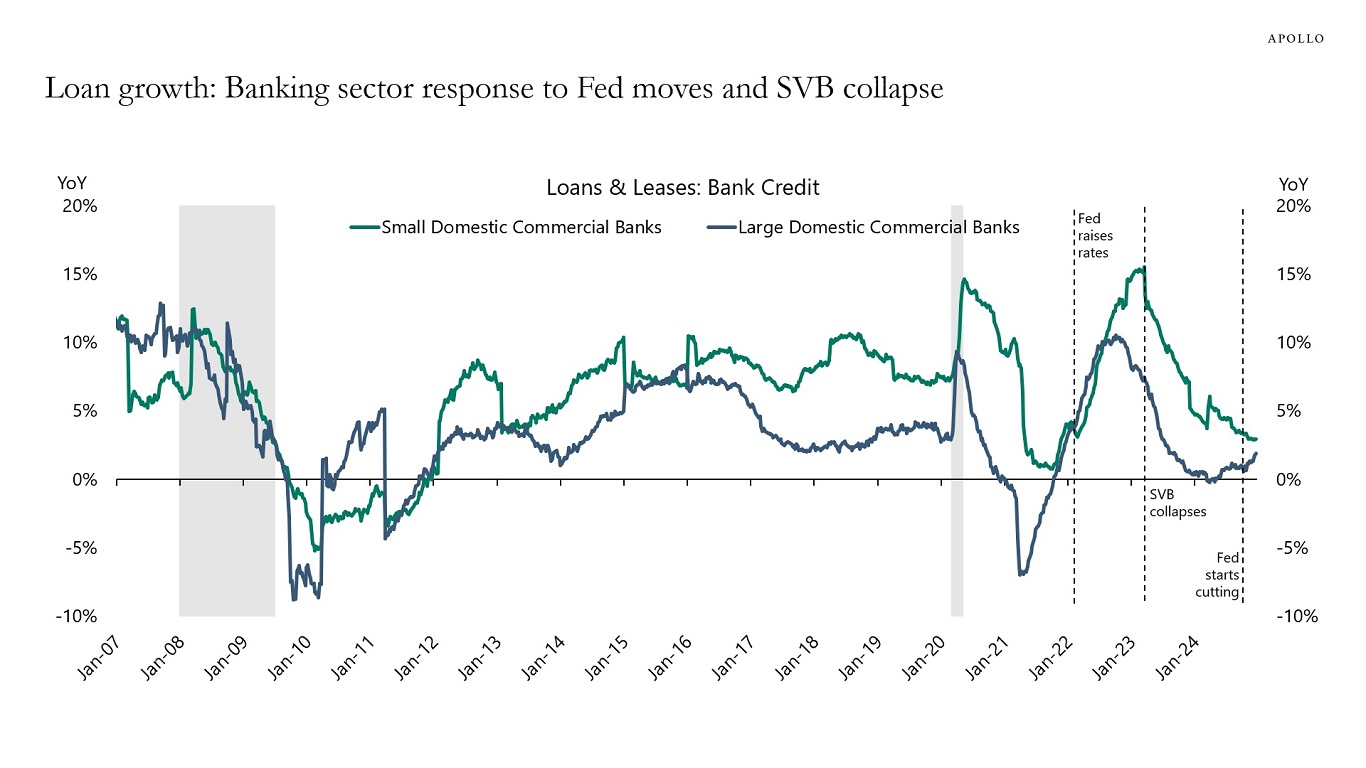

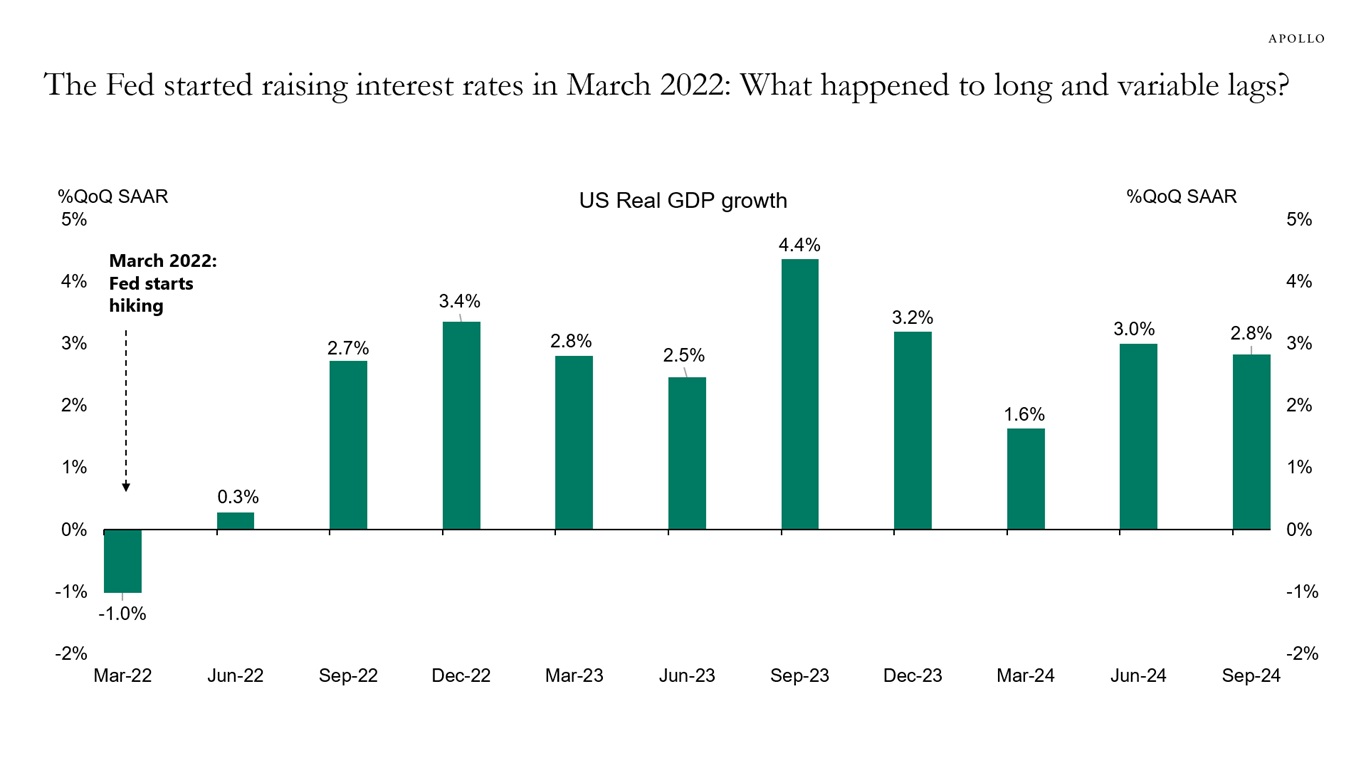

After the Fed started raising interest rates in March 2022, the banking sector started pulling back, and the decline in credit growth was magnified by the regional banking crisis in March 2023.

With the Fed signaling throughout 2024 that rate cuts are coming, banks are now showing more willingness to lend.

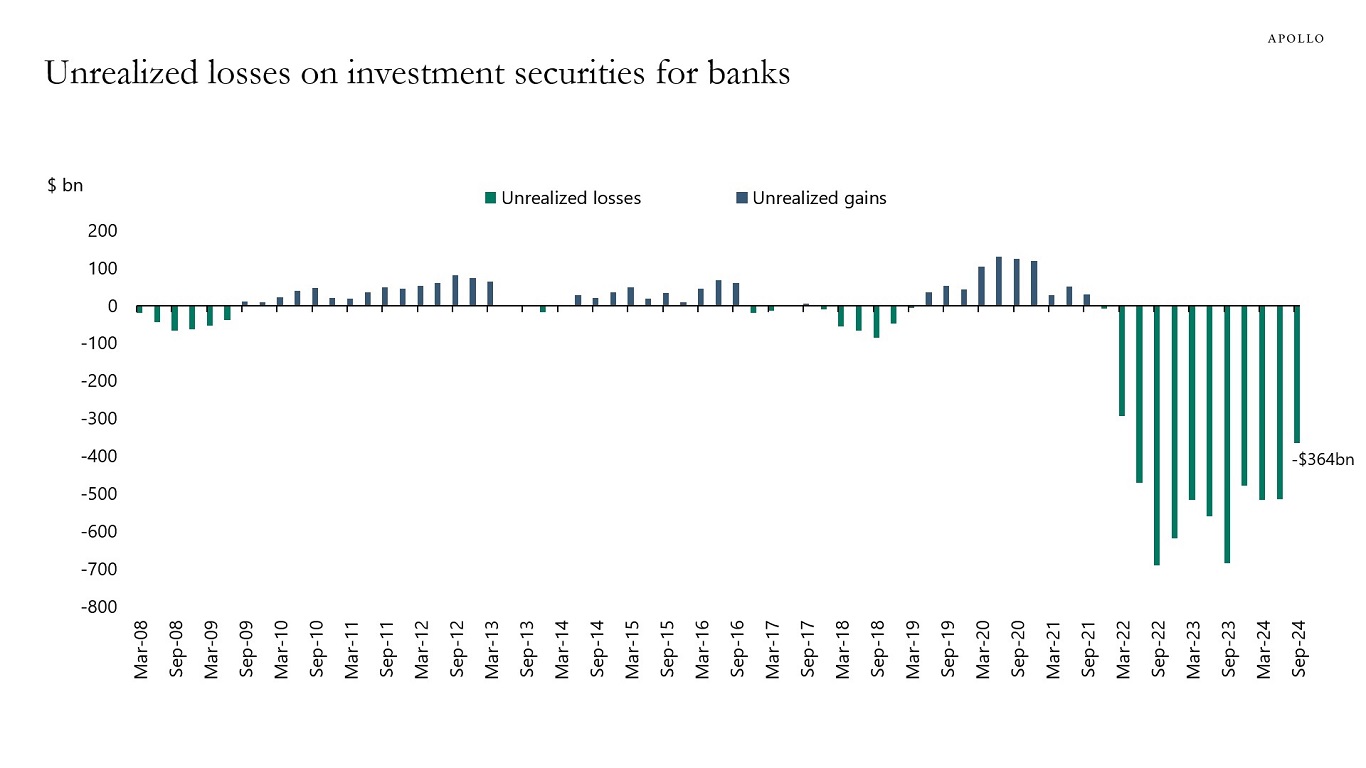

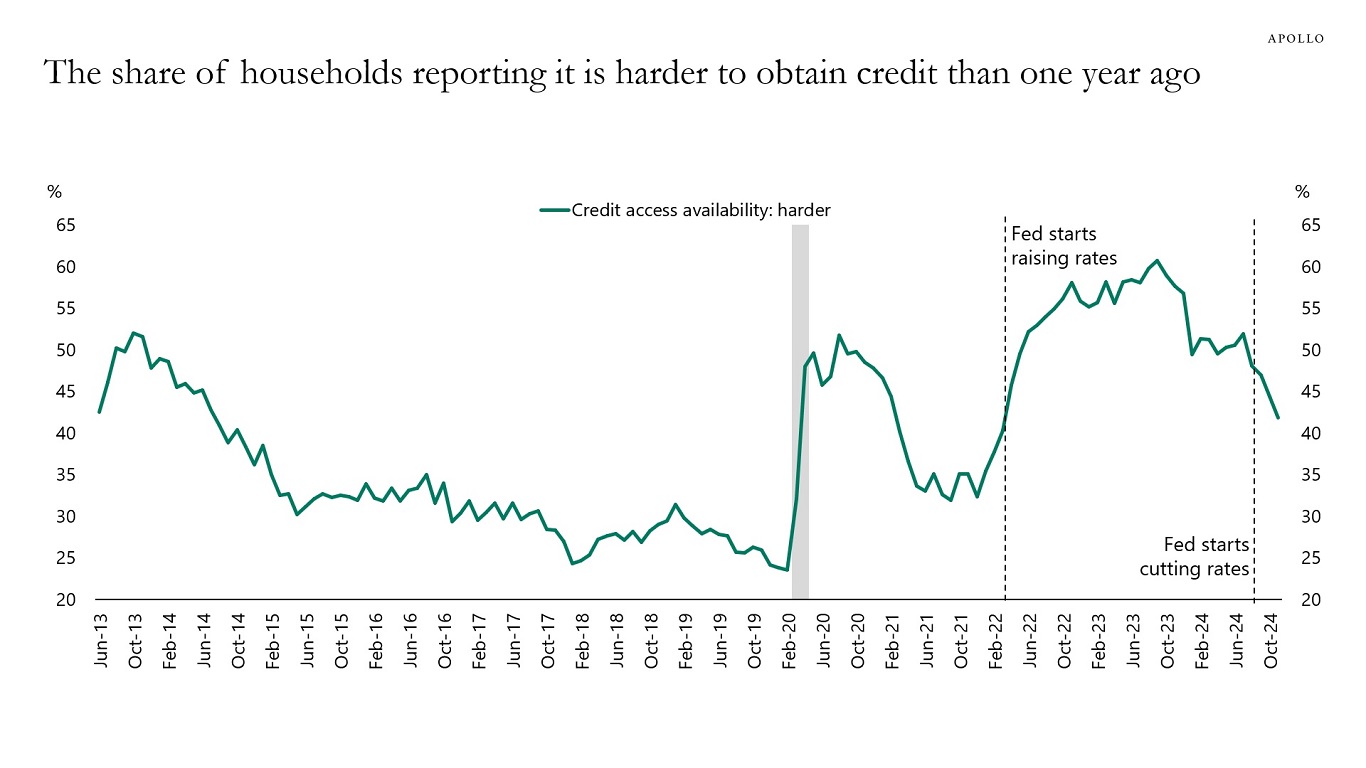

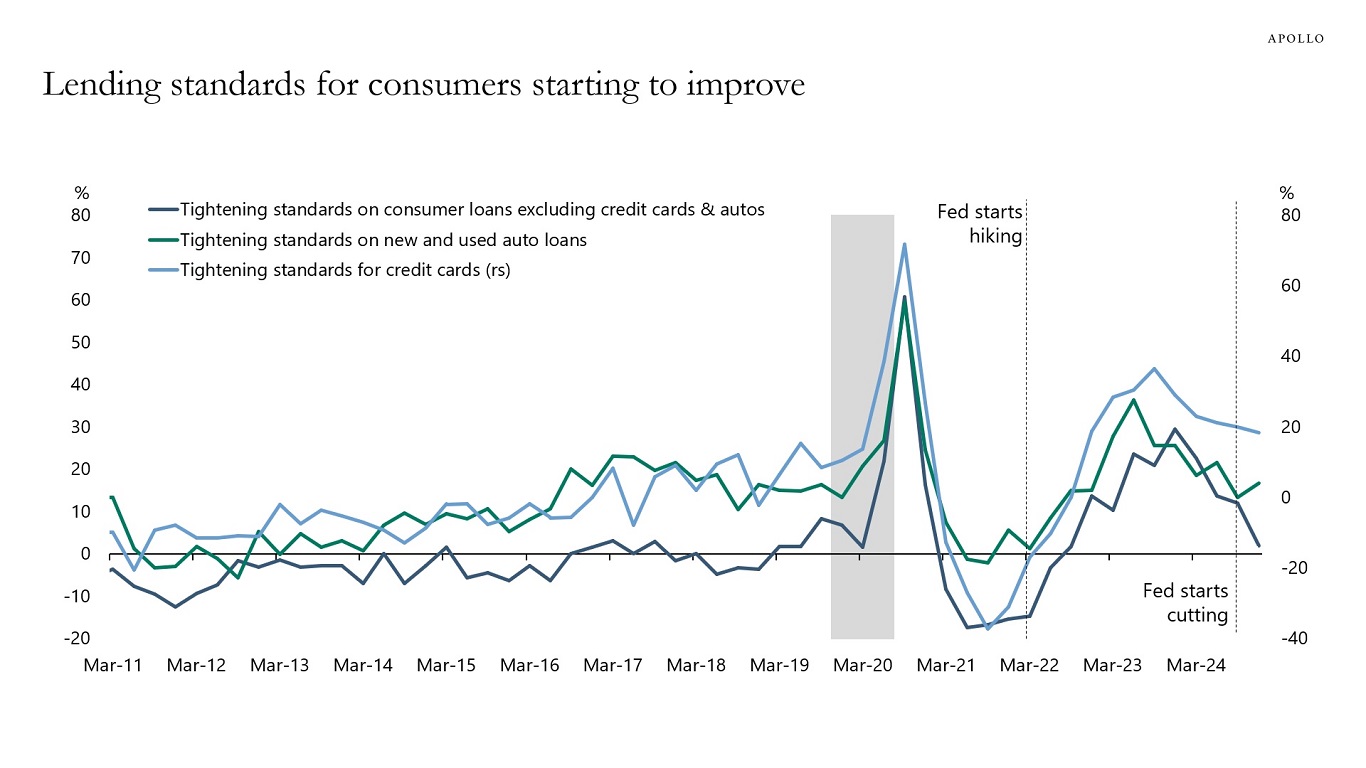

Our updated US banking sector outlook is available here. The charts below show that unrealized losses on investment securities are improving, the share of households reporting that it is harder to obtain credit than a year ago is declining, lending standards on consumer loans are improving, banks are more willing to lend, and loan growth is rising, driven by the large banks.

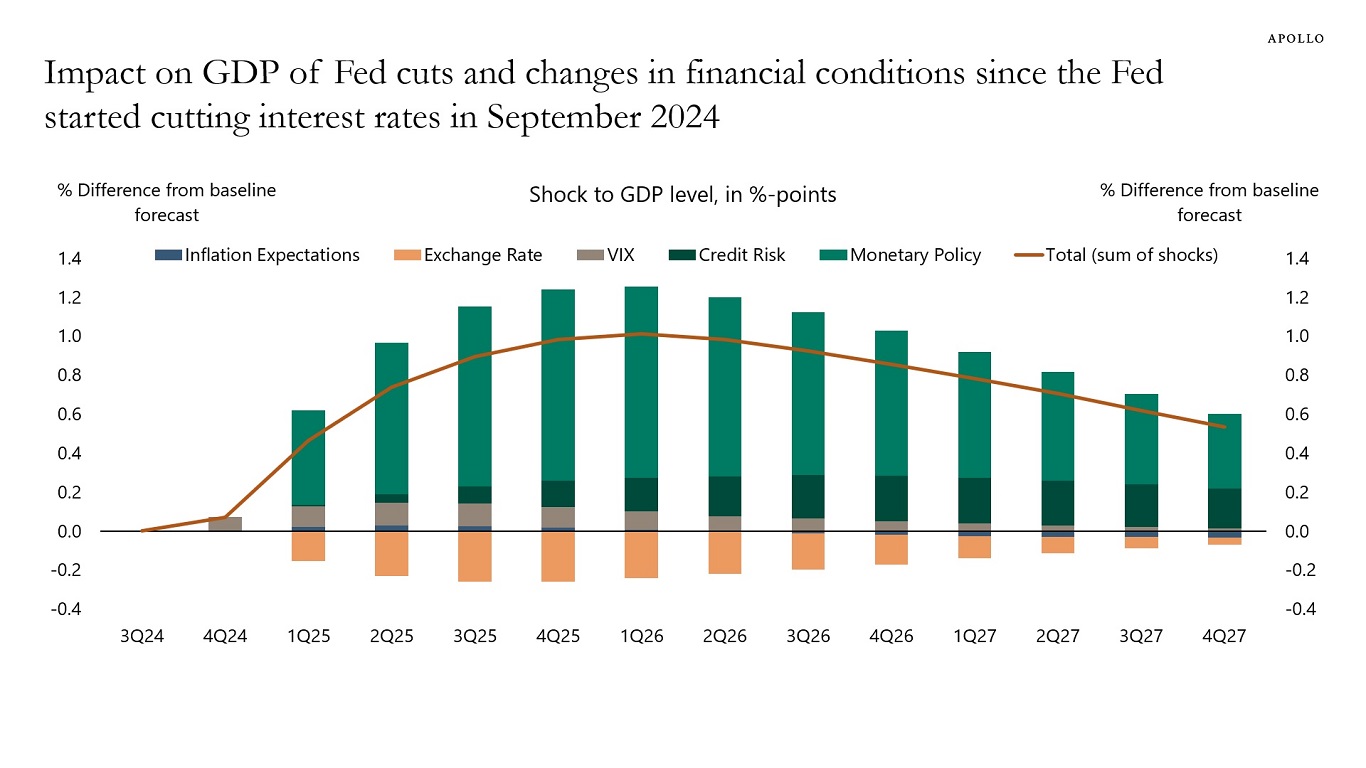

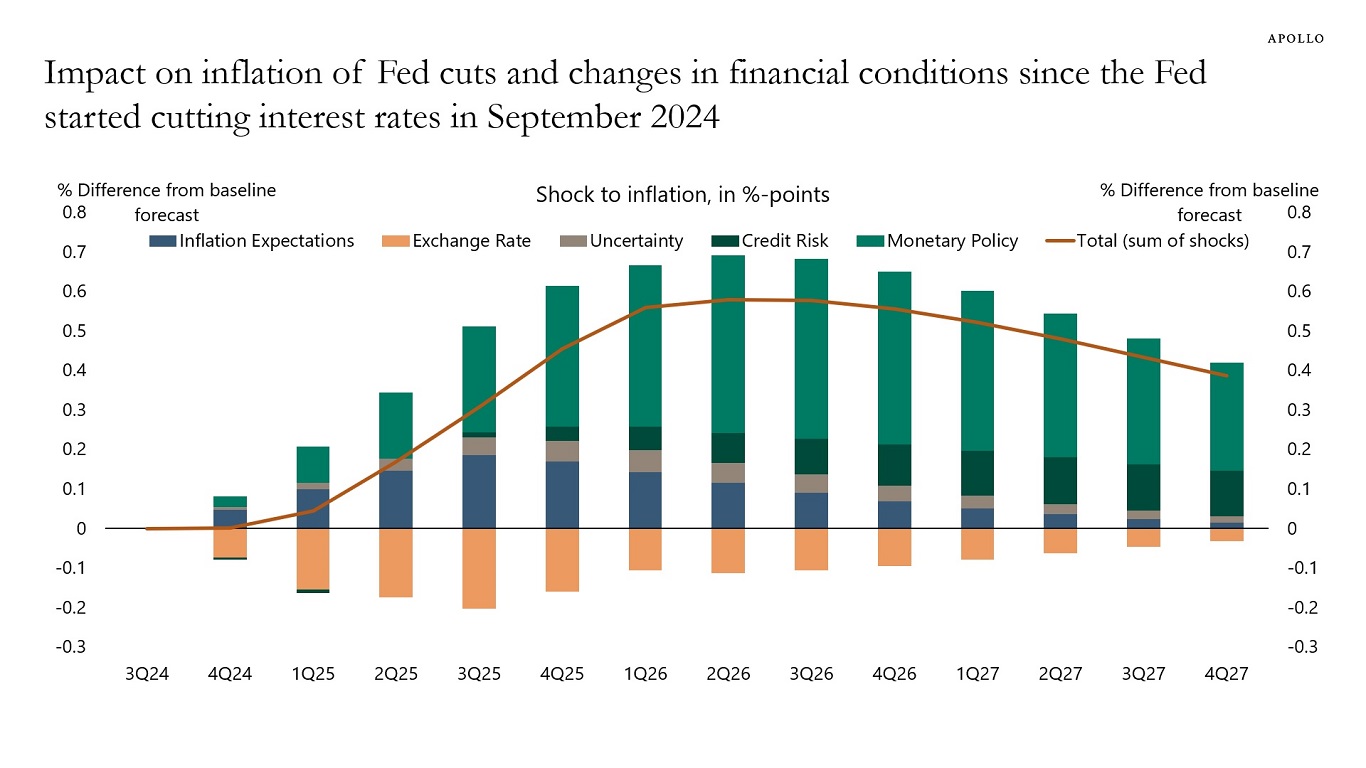

The bottom line is that tailwinds to the economic outlook in 2025 are driven not only by high stock prices, high home prices, low unemployment, and potential Trump economic policies, but also by banks easing credit conditions as a result of the Fed signaling lower rates ahead.