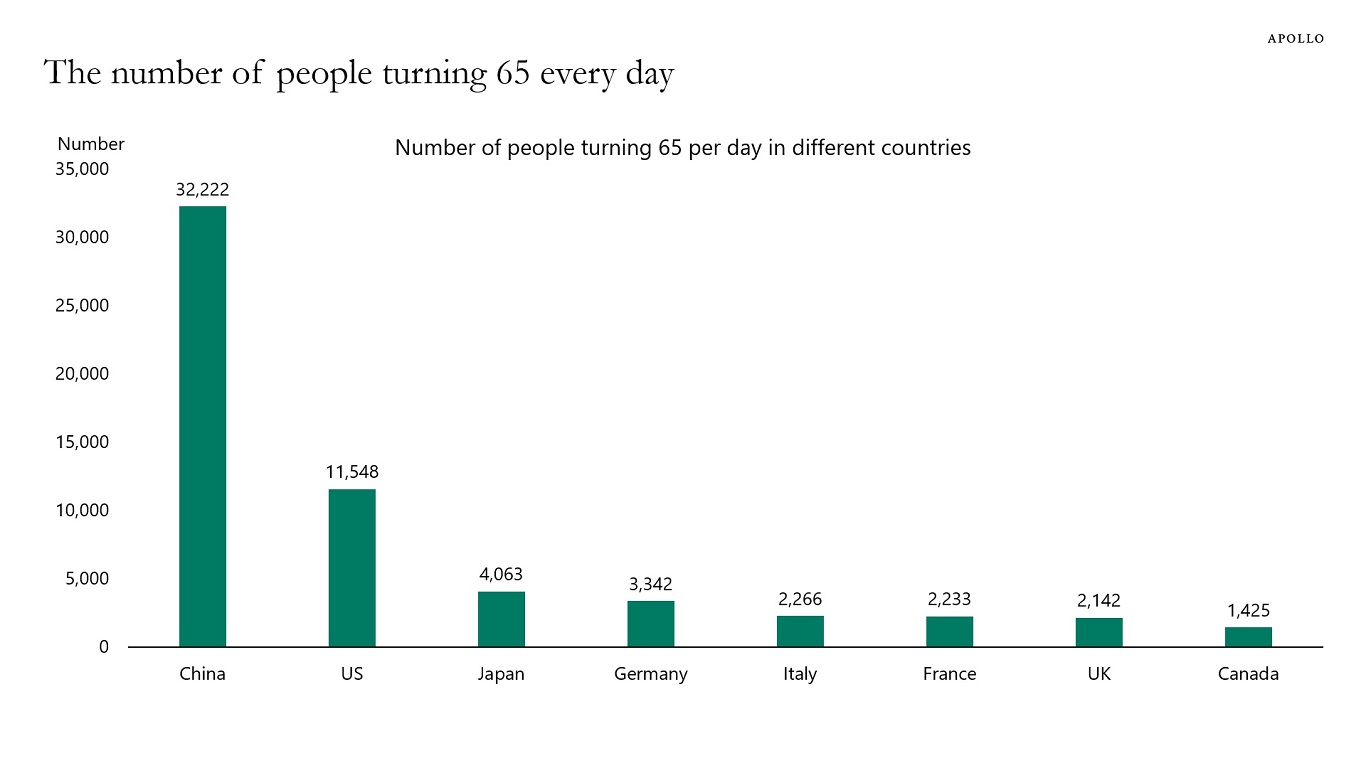

There are 11,500 people who turn 65 years old every day in the US.

In China, it is 32,000; in Japan, it is 4,000; and in Germany, it is 3,300—see the chart below.

The bottom line is that the number of retirees globally is growing rapidly, and there is a need to provide retirement savings for all of them.