It normally takes 18 months on average for the US to negotiate a trade deal, see chart below.

Why does it take so long? Because trade negotiations involve going through what is imported into each country line by line and then negotiating the tariff for each product category (t-shirts, pencils, cars, pharmaceuticals, lawnmowers, services, etc.). The negotiations also involve discussions about non-tariff barriers, tax differences, rules of origin discussions, IP rights, labor standards, environmental standards, anti-dumping, dispute resolution, digital trade and e-commerce, government procurement, and sometimes security and defense considerations.

The bottom line is that trade negotiations take time because they are complex.

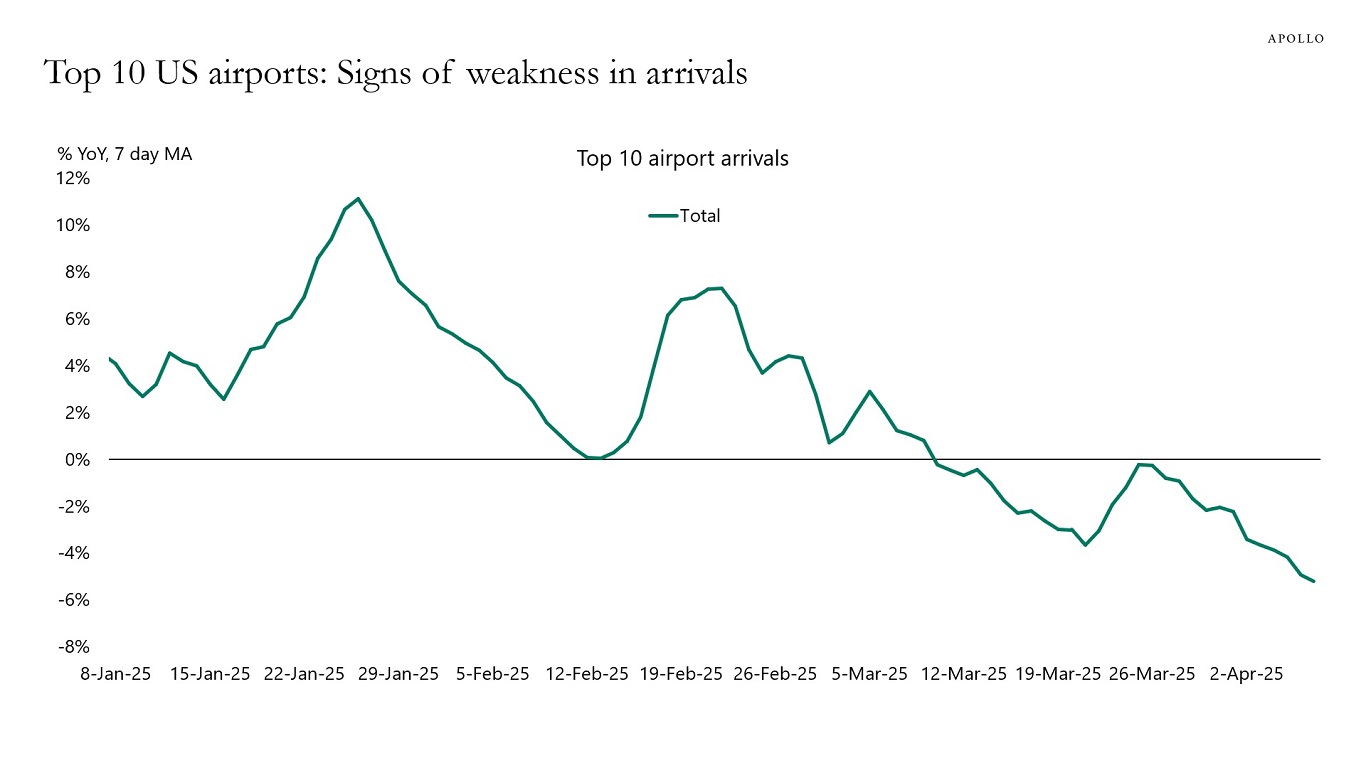

While markets wait for trade negotiations with 90 countries at the same time, global trade is grinding to a standstill with problems similar to what we saw during Covid: growing supply chain challenges with potential shortages in US stores within a few weeks, higher US inflation, and lower tourism to the US. We reiterate our view that if current policies do not change, then the probability of a US recession in 2025 is 90%, see also our discussion in the Daily Spark yesterday.