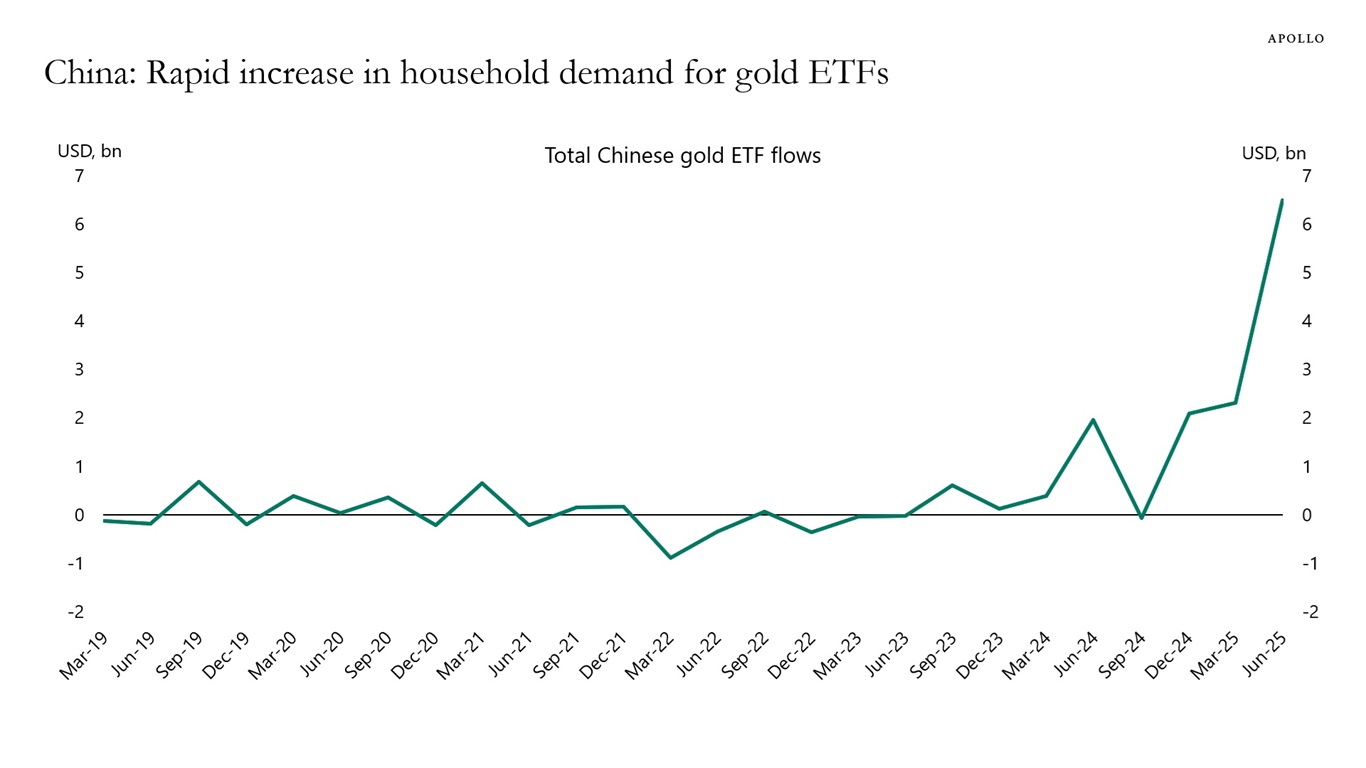

Demand for gold has increased significantly among households in China. This trend likely reflects the strong rally in gold prices, concerns about the ongoing decline in home prices, and worries about deflation and the weakening of the yuan, see chart below.