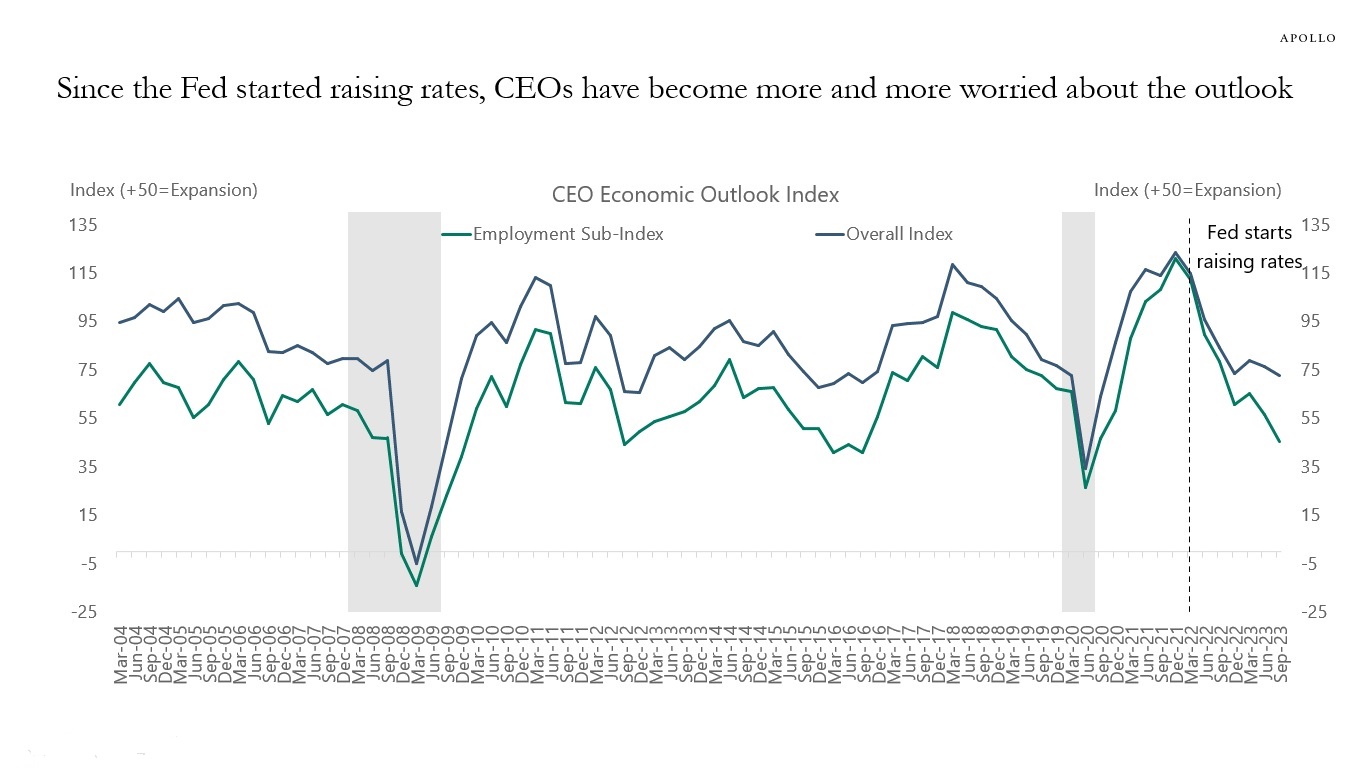

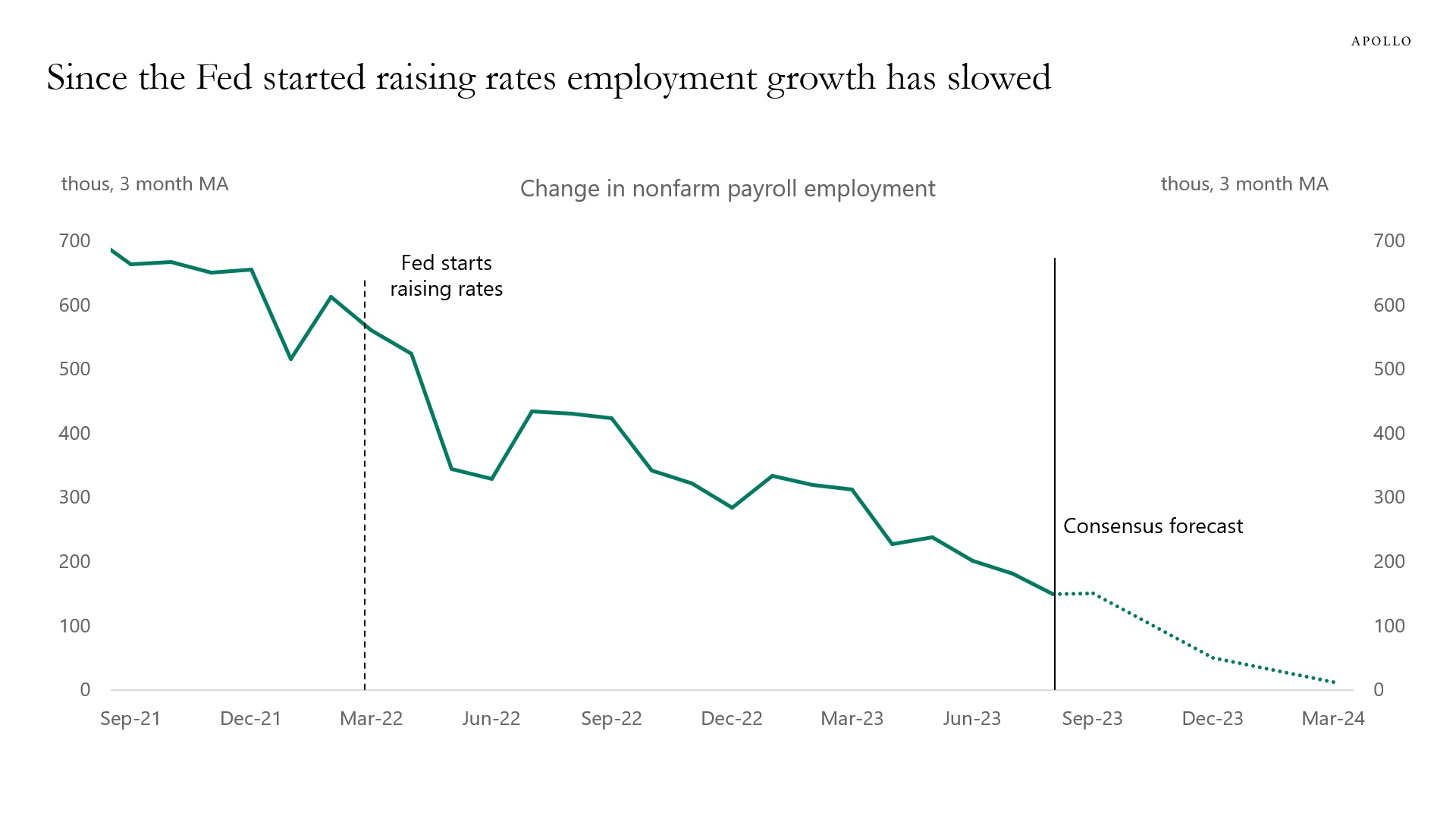

The Business Roundtable CEO survey is designed to provide a picture of the future direction of the US economy by asking CEOs to report their company’s expectations for sales and plans for capital spending and hiring over the next six months.

Since the Fed started raising rates in March 2022, CEOs have gradually worried more and more about the economy slowing, see chart below.

This is how monetary policy works. Higher cost of capital slows down business spending. The decline in the employment sub-index to 2020 levels is particularly noteworthy.