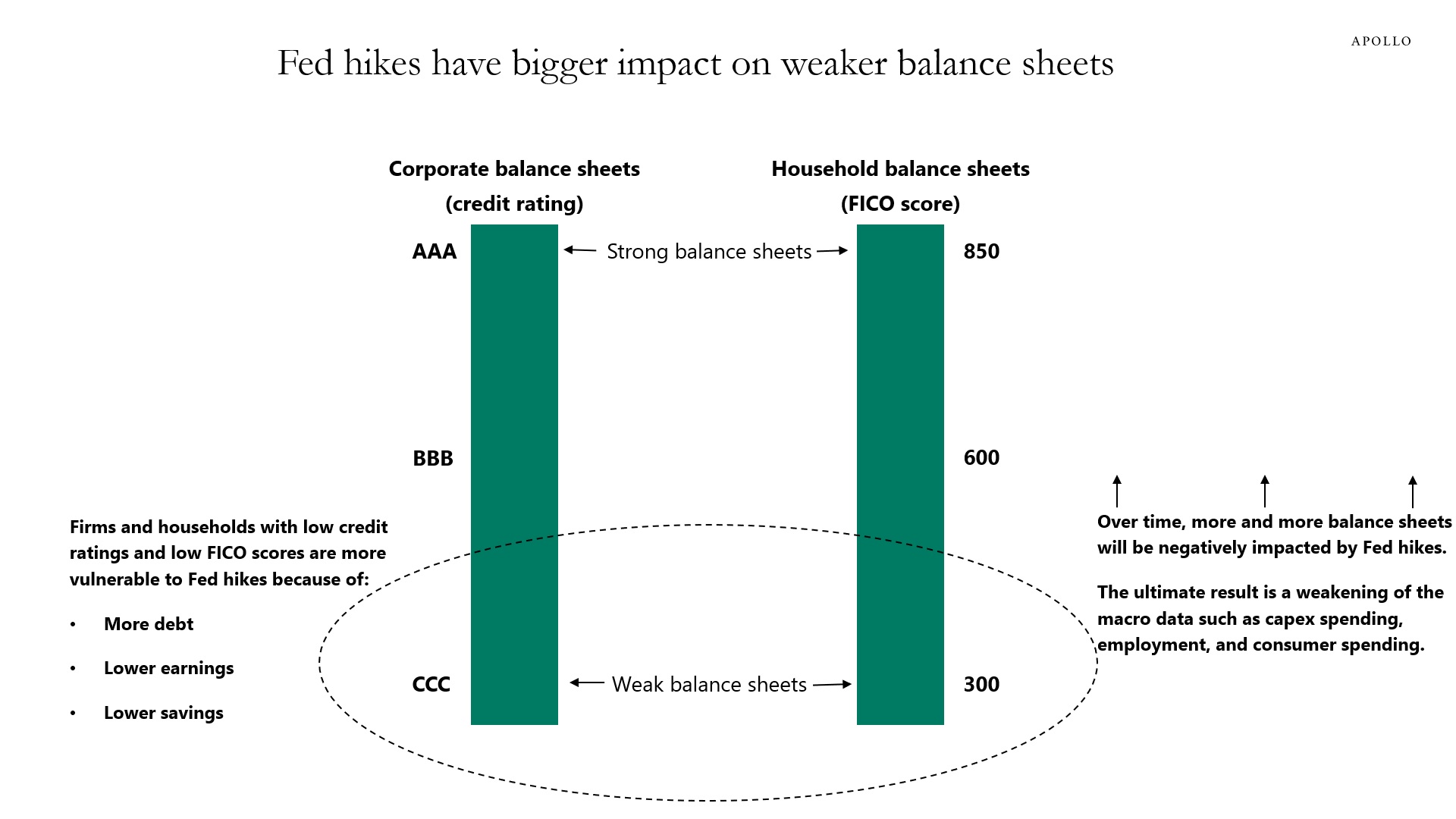

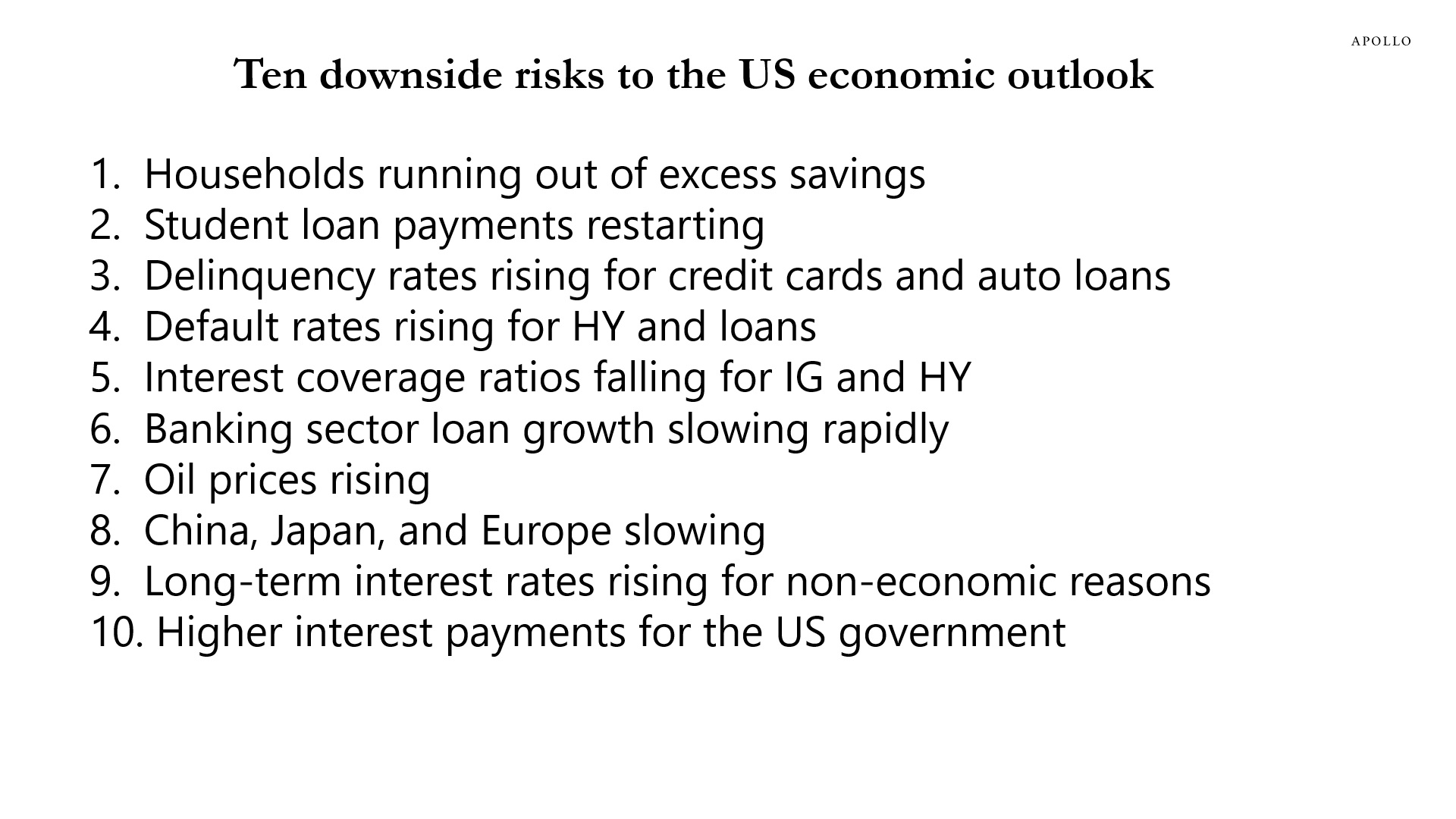

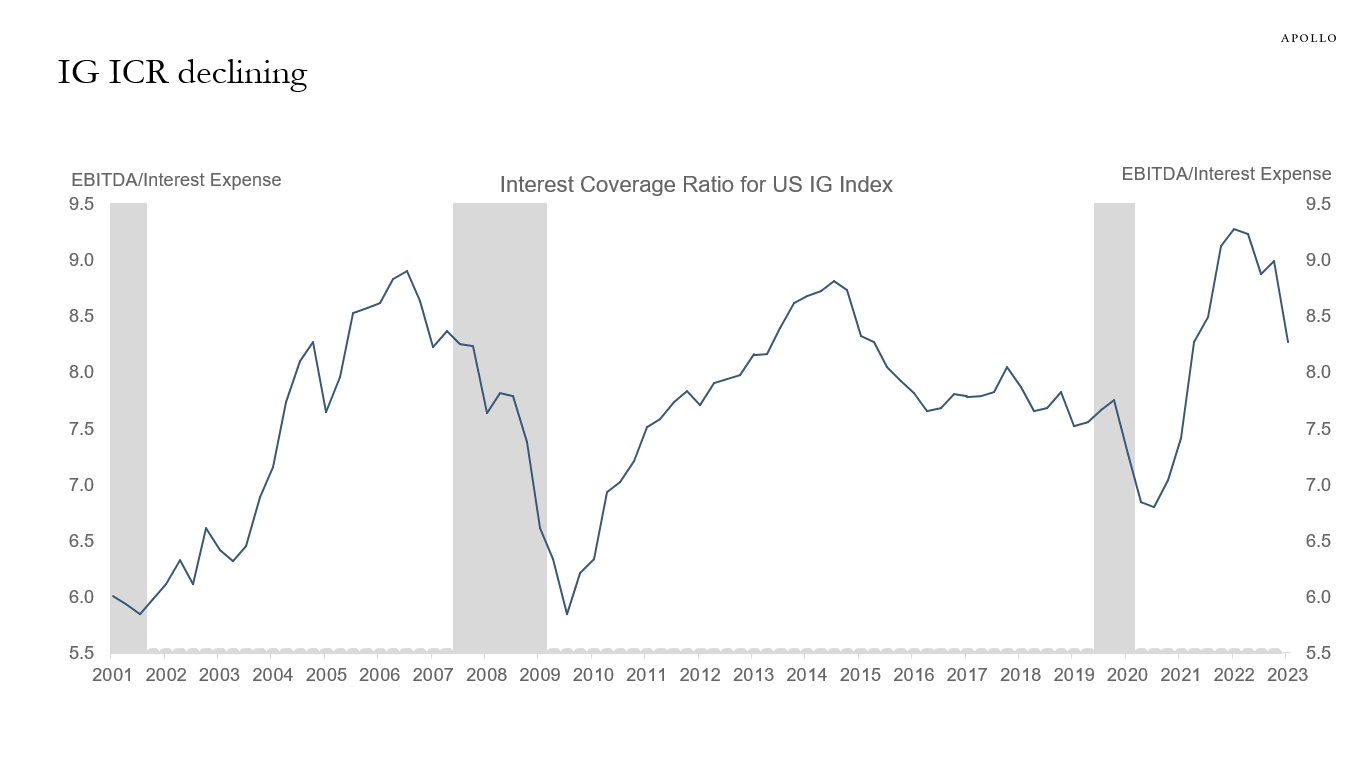

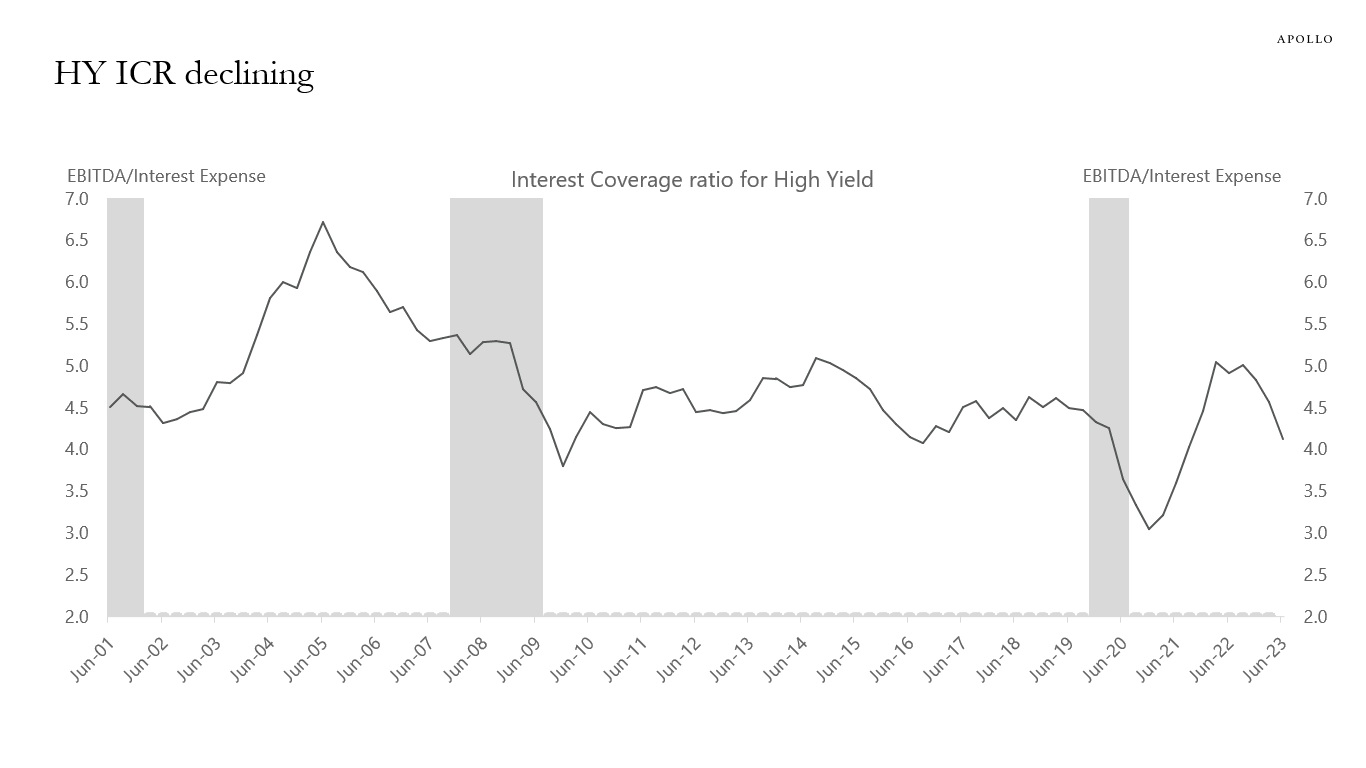

Balance sheets with higher debt, lower earnings, and lower savings will get hit first by Fed hikes, both for consumers and firms, see the first chart below. As this process continues, Fed hikes will gradually impact higher-quality balance sheets over time.

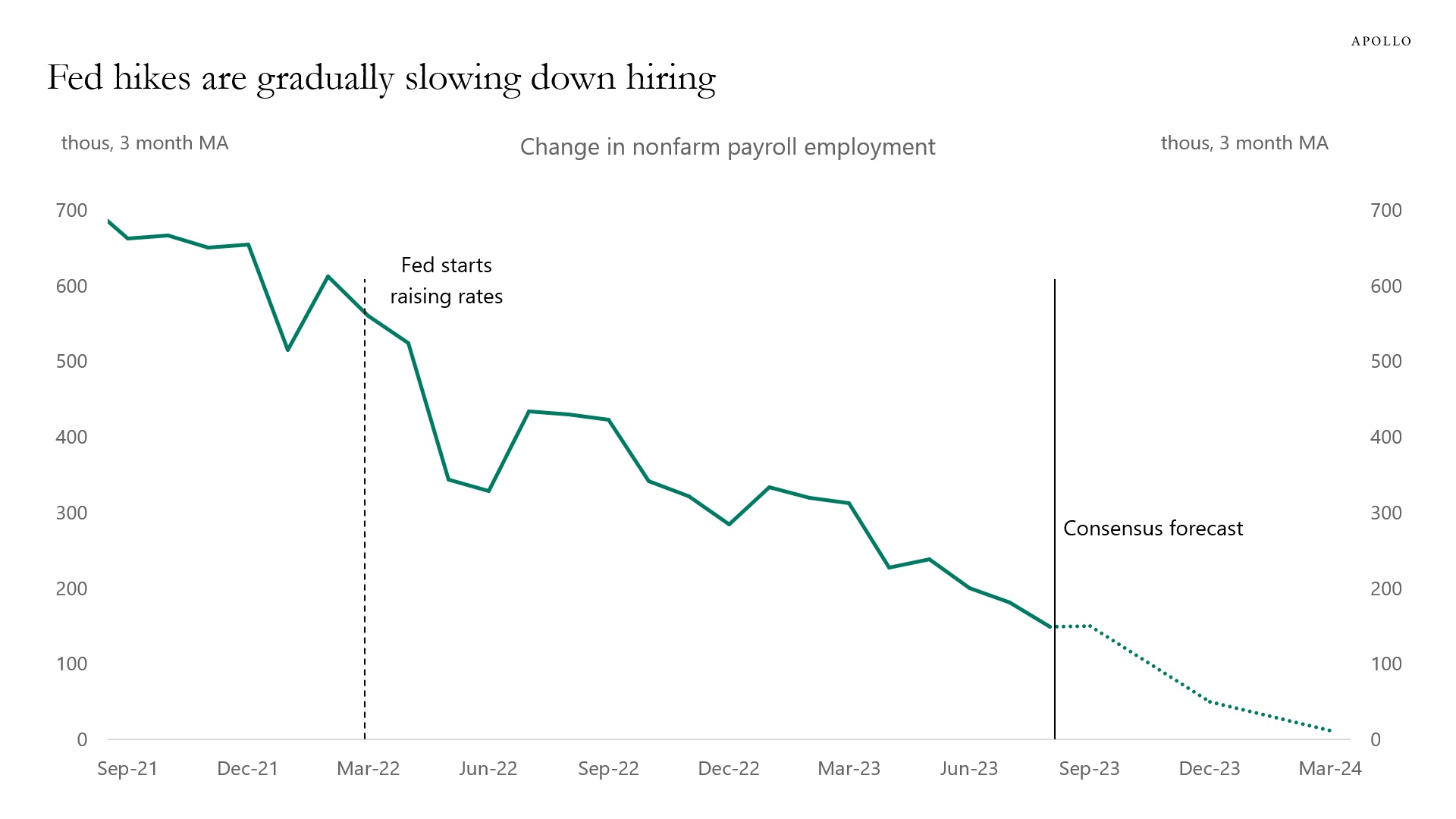

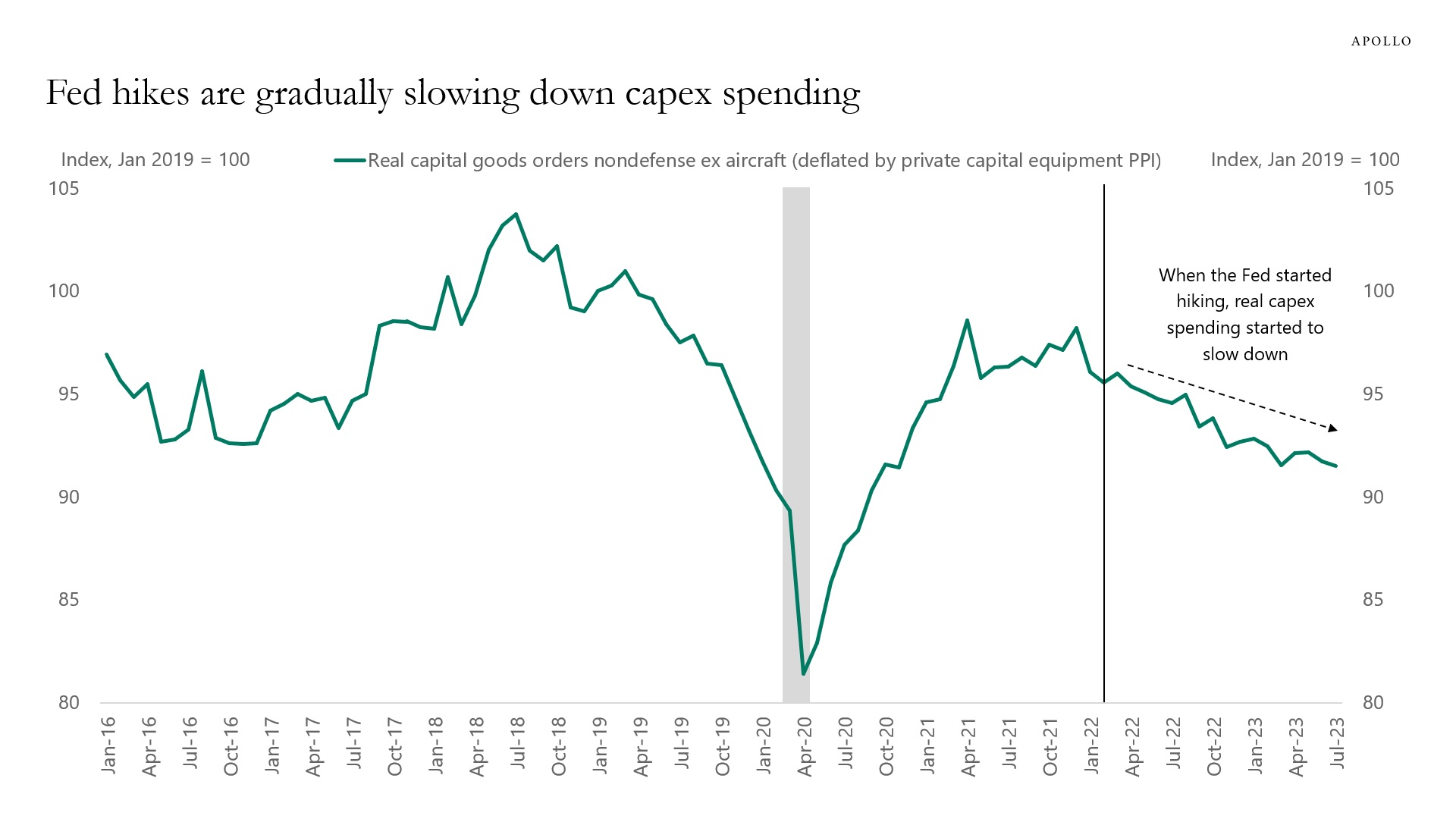

Once the Fed funds rate reaches sufficiently restrictive levels, the macro data will weaken. This is happening now: Delinquency and default rates are increasing for more vulnerable households and firms, and capex spending and nonfarm payrolls are weakening, see the second and third charts below.

This is how monetary policy works, and markets should expect the economic data to weaken further over the coming months as Fed hikes gradually bite harder and harder on consumers and firms.