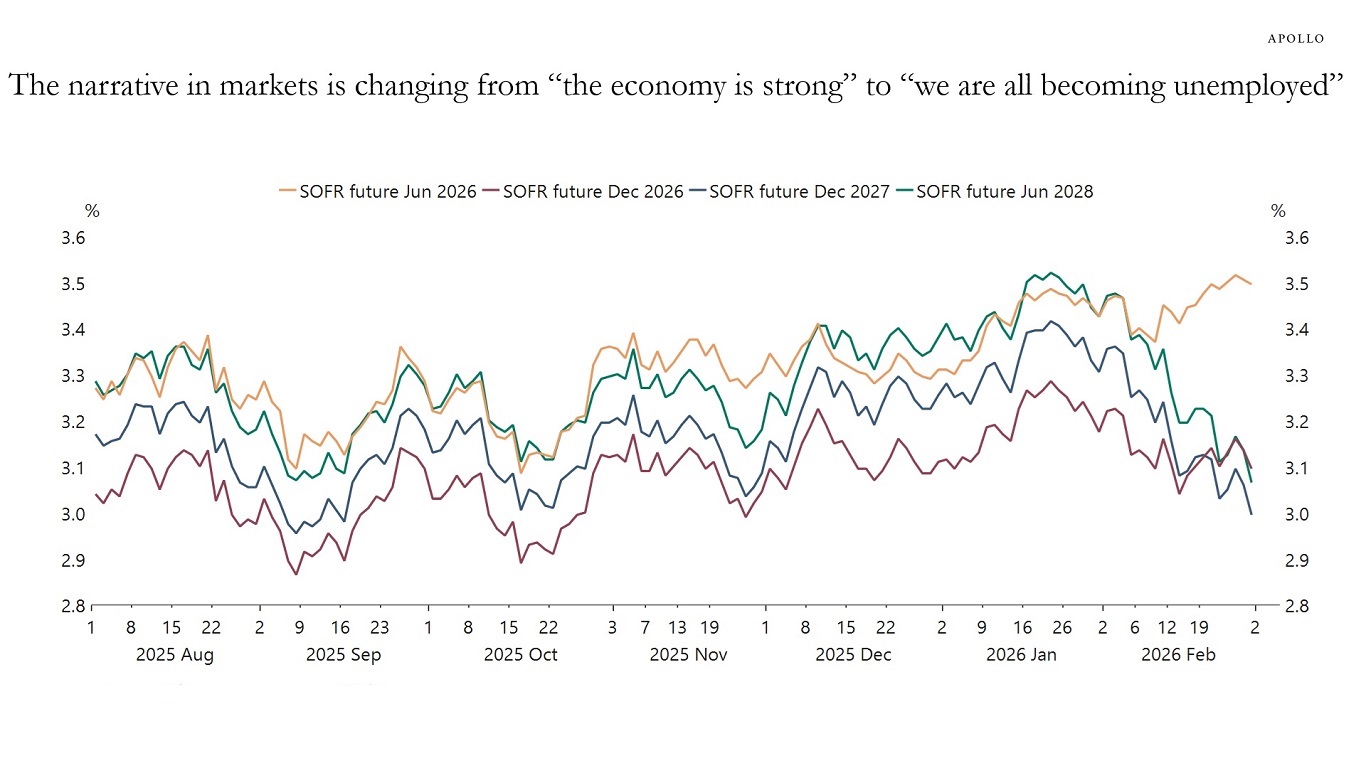

The dramatic change in recent weeks in the narrative in markets from “the economy is strong” to “we are all becoming unemployed” is truly remarkable.

AI expectations are no longer just disrupting the equity market, with sectors such as software under pressure.

AI expectations have also sparked a macro conversation about a coming rise in the unemployment rate, despite no change in the underlying incoming economic story of a strong US economy driven by AI spending, the industrial renaissance and the One Big Beautiful Bill.

The bottom line is that rates investors are now pricing in rapid AI adoption that will push the unemployment rate higher and warrant many more Fed cuts by December 2026, see chart below.

In other words, markets are starting to believe the techno-optimists’ view of the world, rather than the more measured Fed and economist view.

I think the techno-optimists are wrong about the macro impact, and AI adoption is going to take much longer than the 12-18 months they talk about, and the overall impact on productivity will be much more muted.

Put differently, looking ahead to December 2026, the risk of an overheating economy remains larger than the risk of the unemployment rate going to 10%.