The textbook would be saying that when the stock market is going down, long-term interest rates should also be going down.

But this is not what is happening at the moment, see chart below.

What could be the reasons why long-term interest rates are moving higher when the stock market is moving lower?

1) With the yen, euro, and Canadian dollar strengthening at the same time, this could be foreigners selling US Treasuries.

2) With the VIX at elevated levels around 50, there is a lot of hedging activity going on, and it could, therefore, be risk reduction among large asset managers managing rates, credit, and equities.

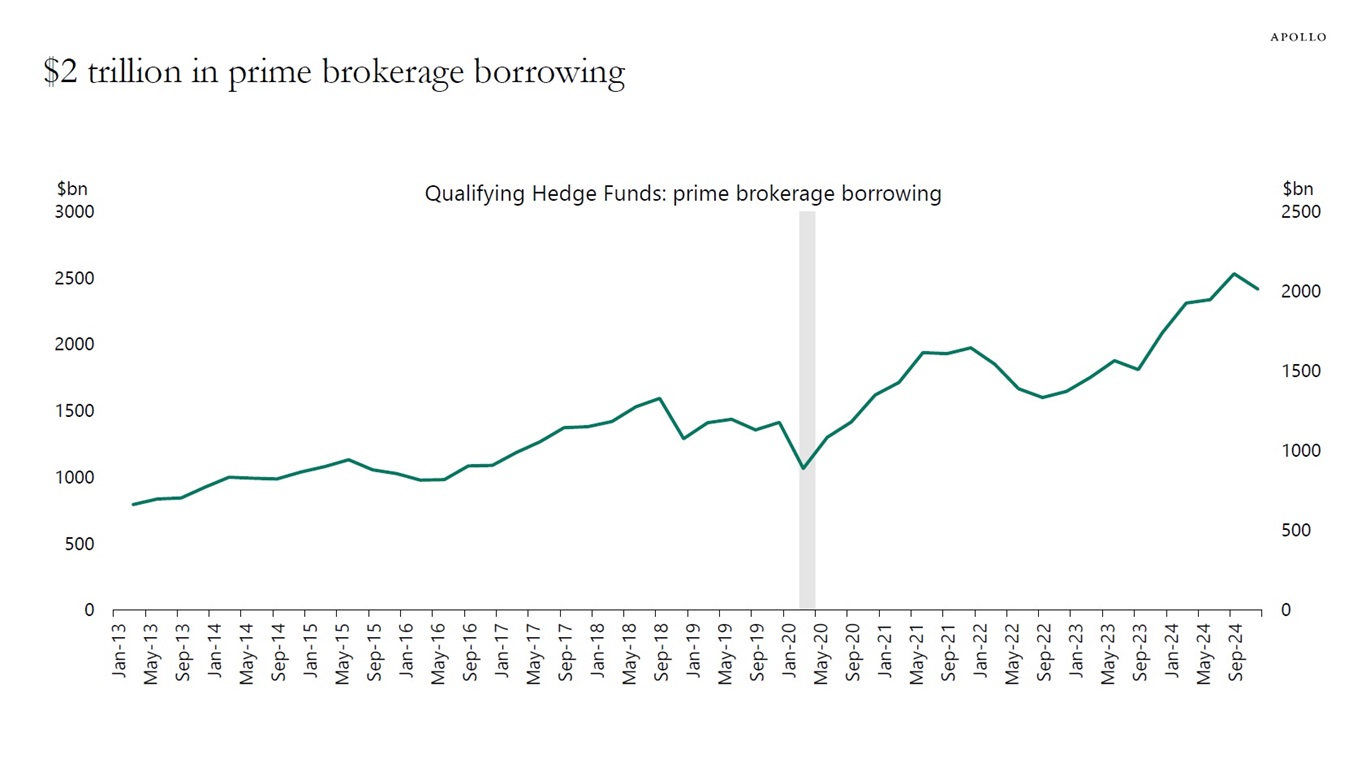

3) With almost $1 trillion in the basis trade, it could be an unwinding of the basis trade among levered hedge funds.

The answer is likely some combination of these three forces.