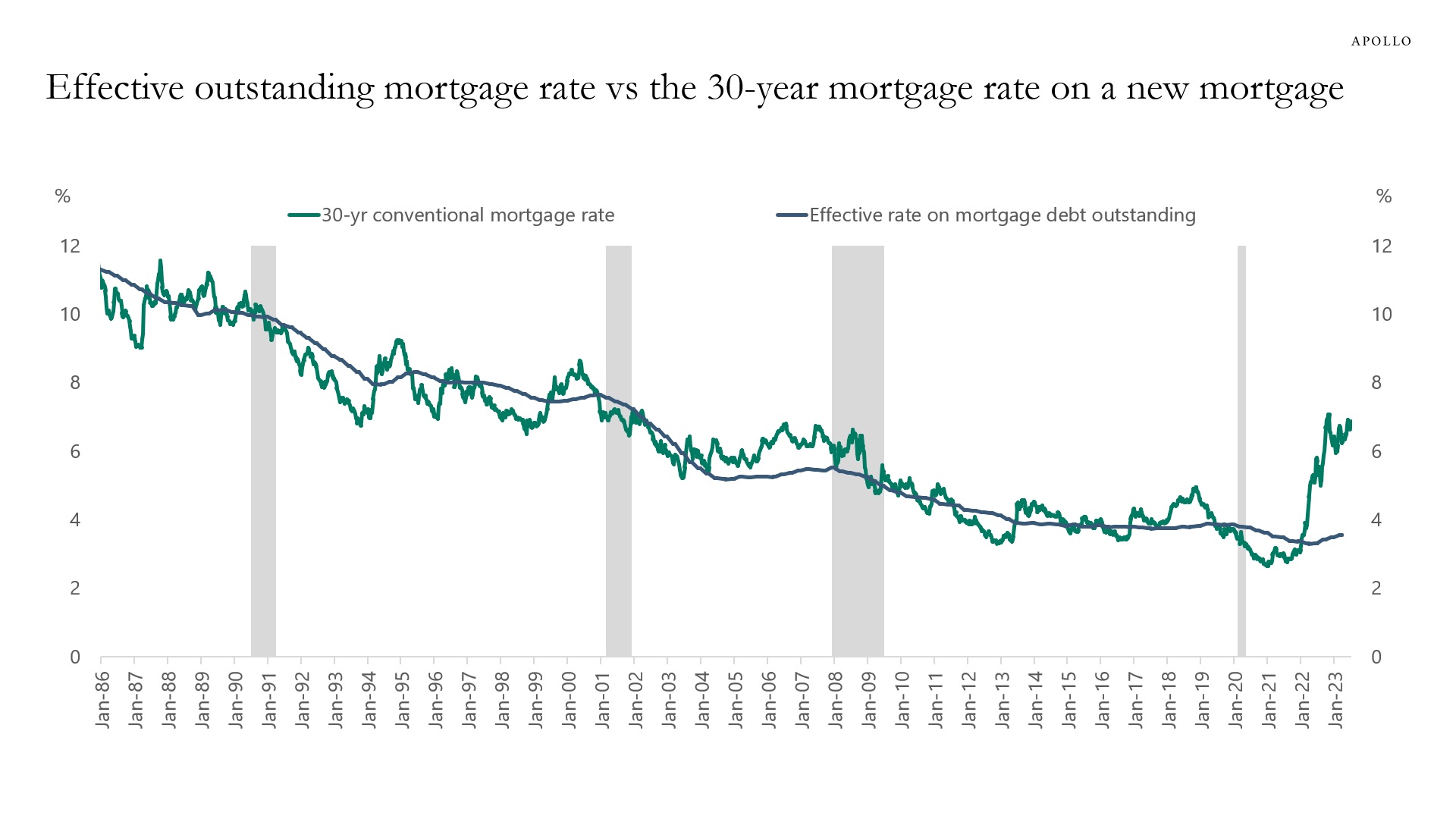

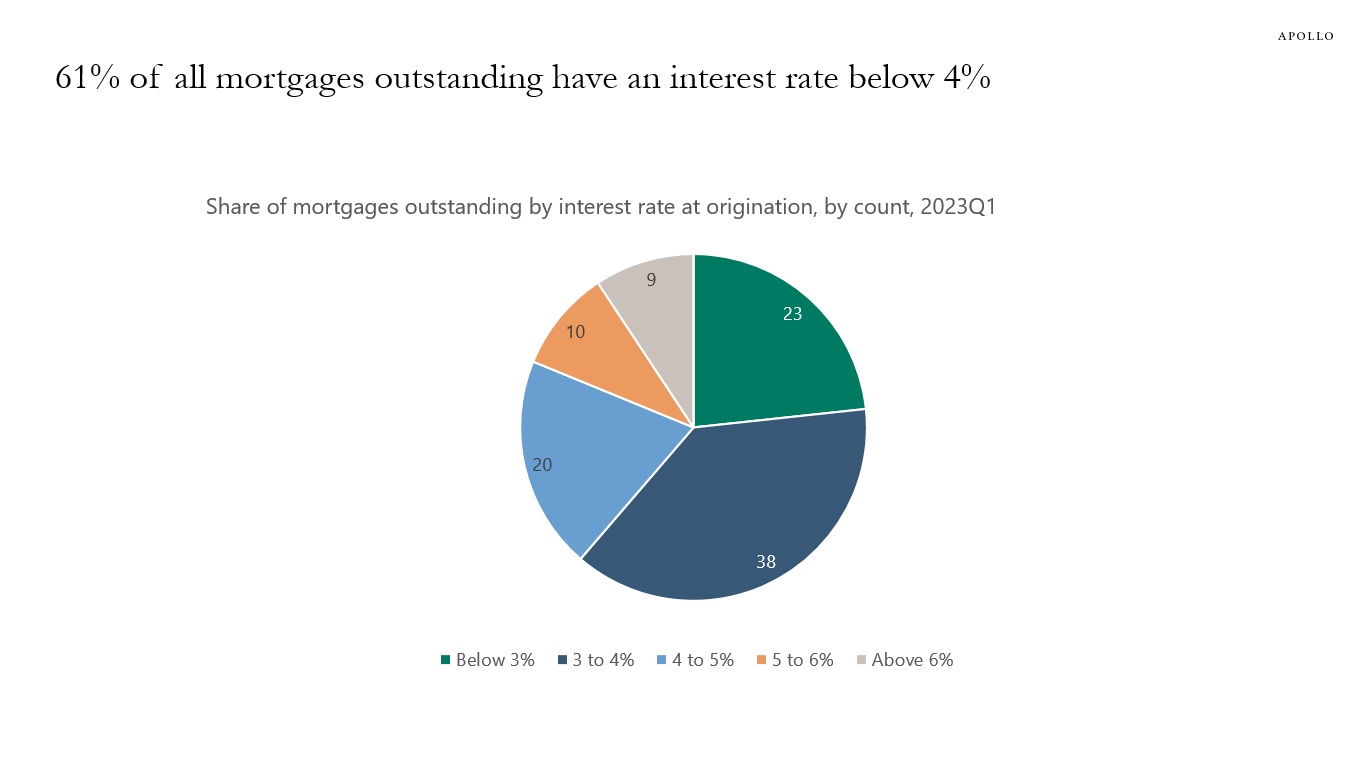

Twenty-three percent of all mortgages outstanding have an interest rate below 3%, 38% are between 3% and 4%, and only 9% of all mortgages outstanding were originated with an interest rate above 6%, see the first chart.

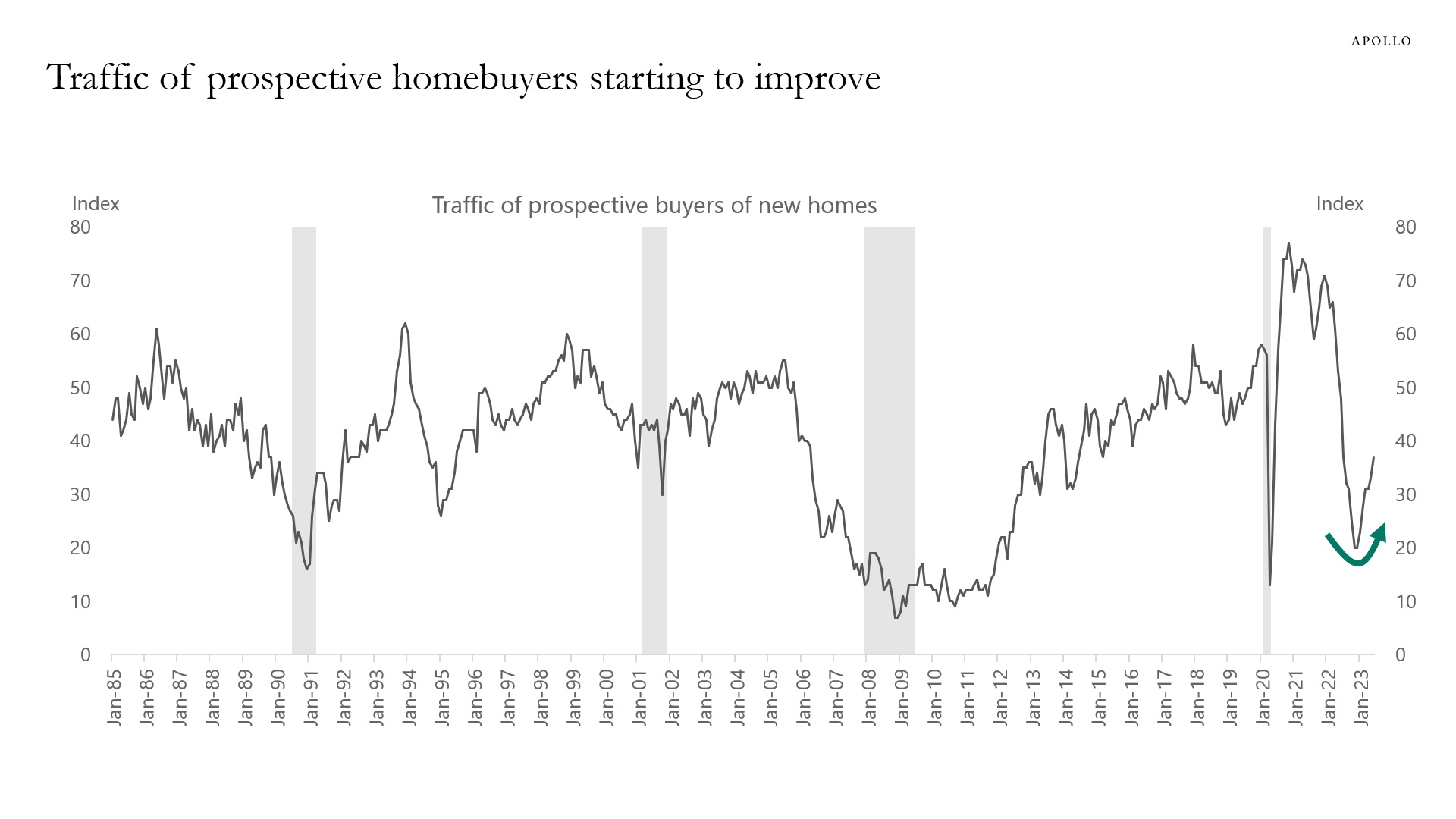

The bottom line is that homeowners across America do not have any incentive to move and get a new mortgage with mortgage rates currently at 7.25%.

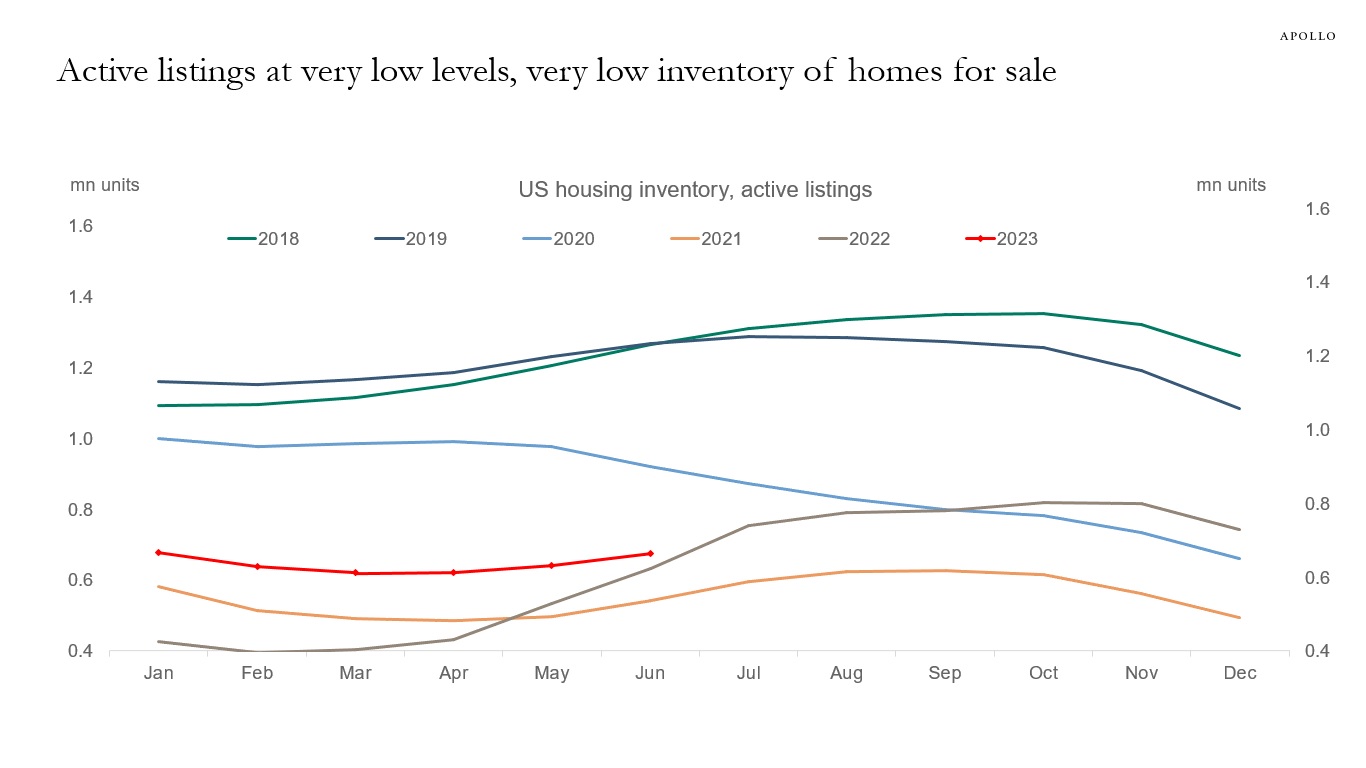

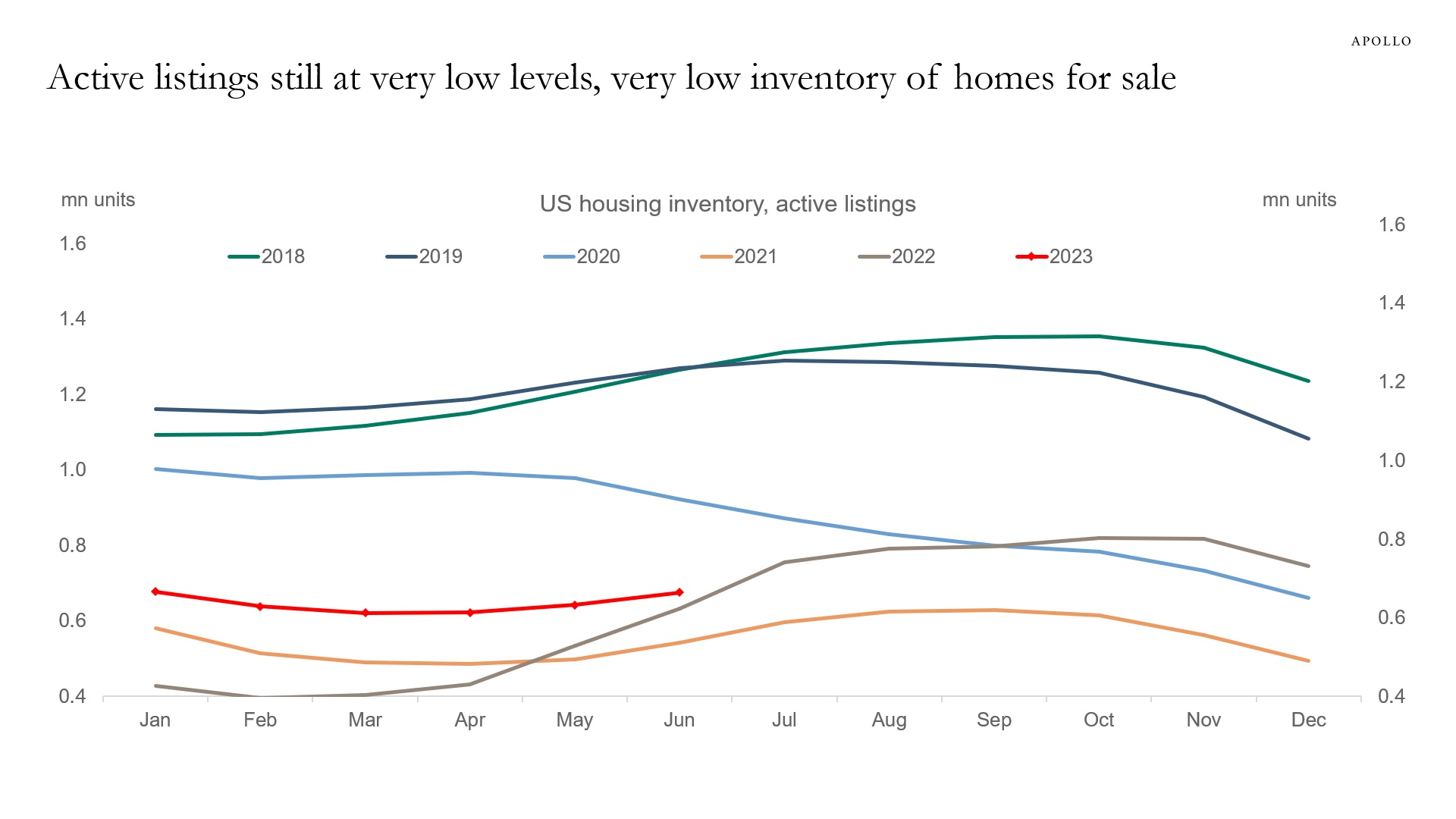

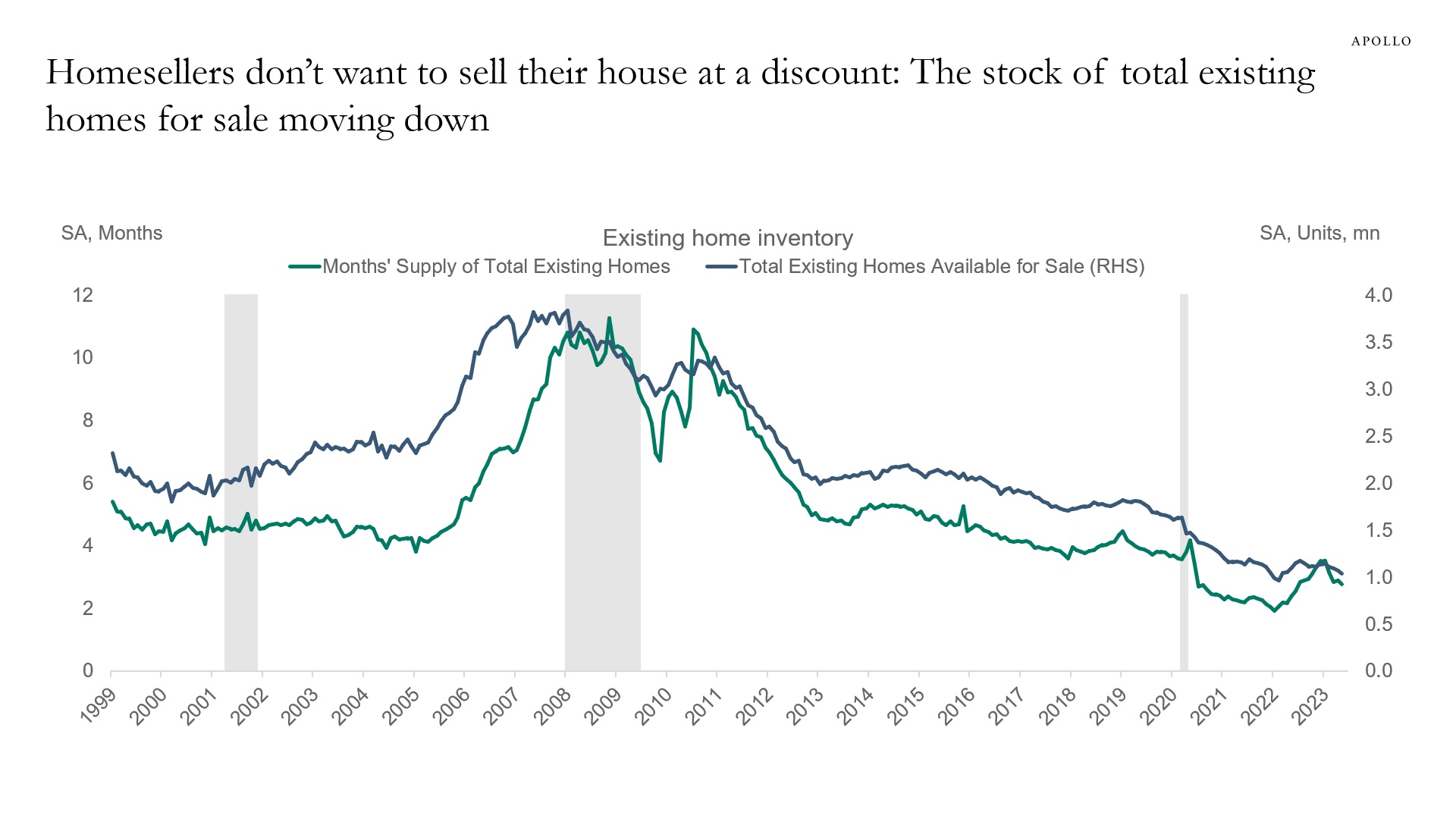

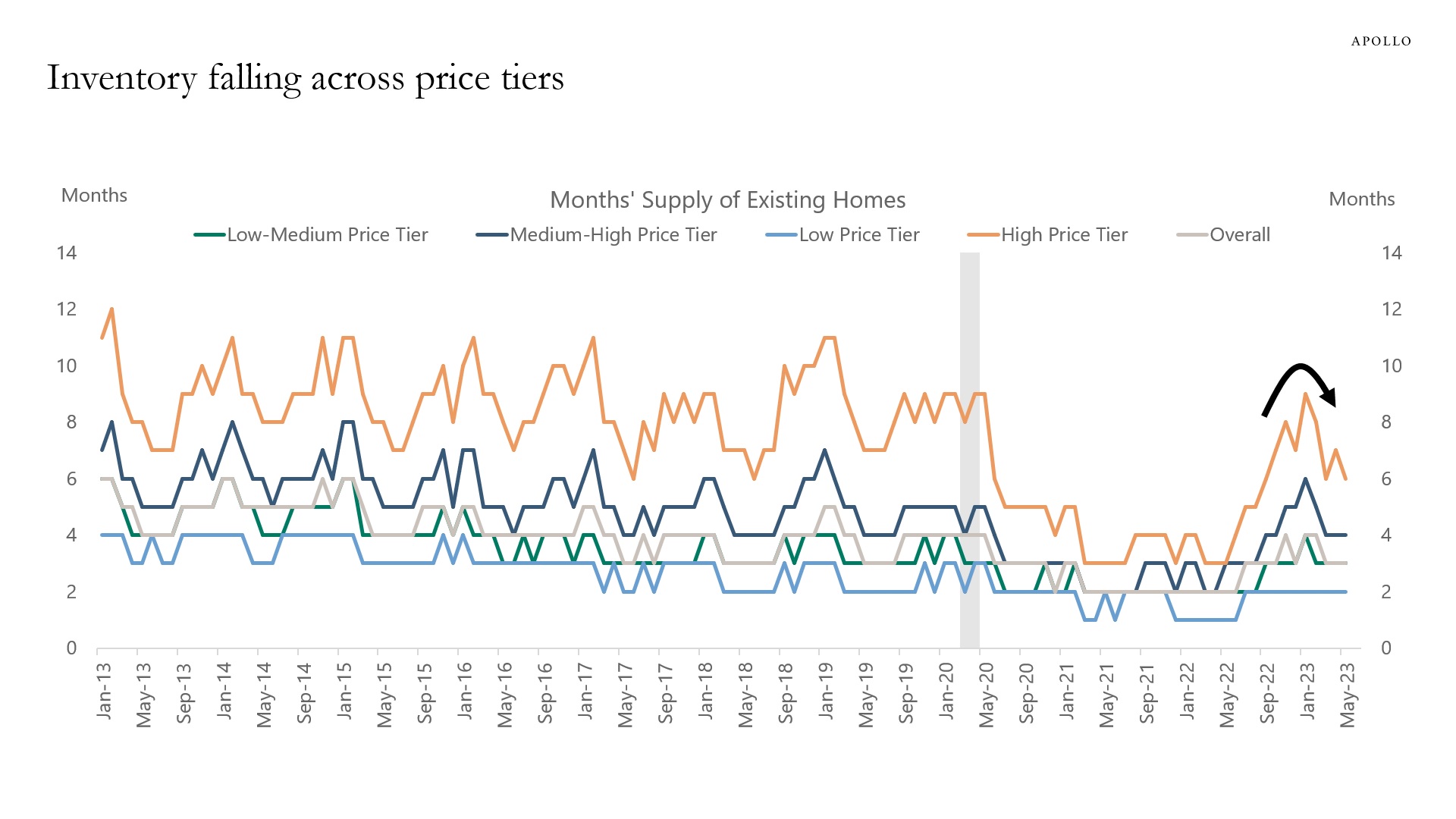

This is a key reason why the supply in the housing market continues to be so low, see the second chart.

Source: FHFA, Apollo Chief Economist